Global AI & digital engineering partner. Agentic AI systems, RAG apps, unified BOT platforms, cloud & DevOps, mobile/web, Web3 & IoT. Enterprise to startup. DM.

Joined April 2013

- Tweets 28,075

- Following 2,903

- Followers 2,400

- Likes 14,630

8,578 Photos and videos

Fine-tuning makes sense when you need consistent task behavior, precise output format, domain language handling, stronger behavior control, or lower cost with a smaller model.

ow.ly/oxGc50Z9VIP

1

Fine-tuning is not for teaching facts.

Facts change. Facts need citations. Facts need updates.

That is what retrieval is for.

Fine-tuning is for behavior.

ow.ly/xiUv50Z9VEU

2

A prototype gets outputs wrong.

The usual reaction: “Fine-tune it on our data.”

Often, that is the wrong move.

First ask: is the issue knowledge, behavior, tools, or evaluation?

ow.ly/K3N850Z9VuN

5

Most enterprises that think they need to fine-tune an LLM probably do not.

Fine-tuning is powerful, but it is not the first lever.

Prompting, RAG, and tools should be tested first.

ow.ly/Wx4j50Z9VfO

3

Co-lending is operationally complex.

Two regulated entities. One borrower. Shared books. Different policies.

AI can reduce friction across eligibility, underwriting, disbursement, servicing, and reconciliation.

Visit: ow.ly/ISGt50Z8FJE

4

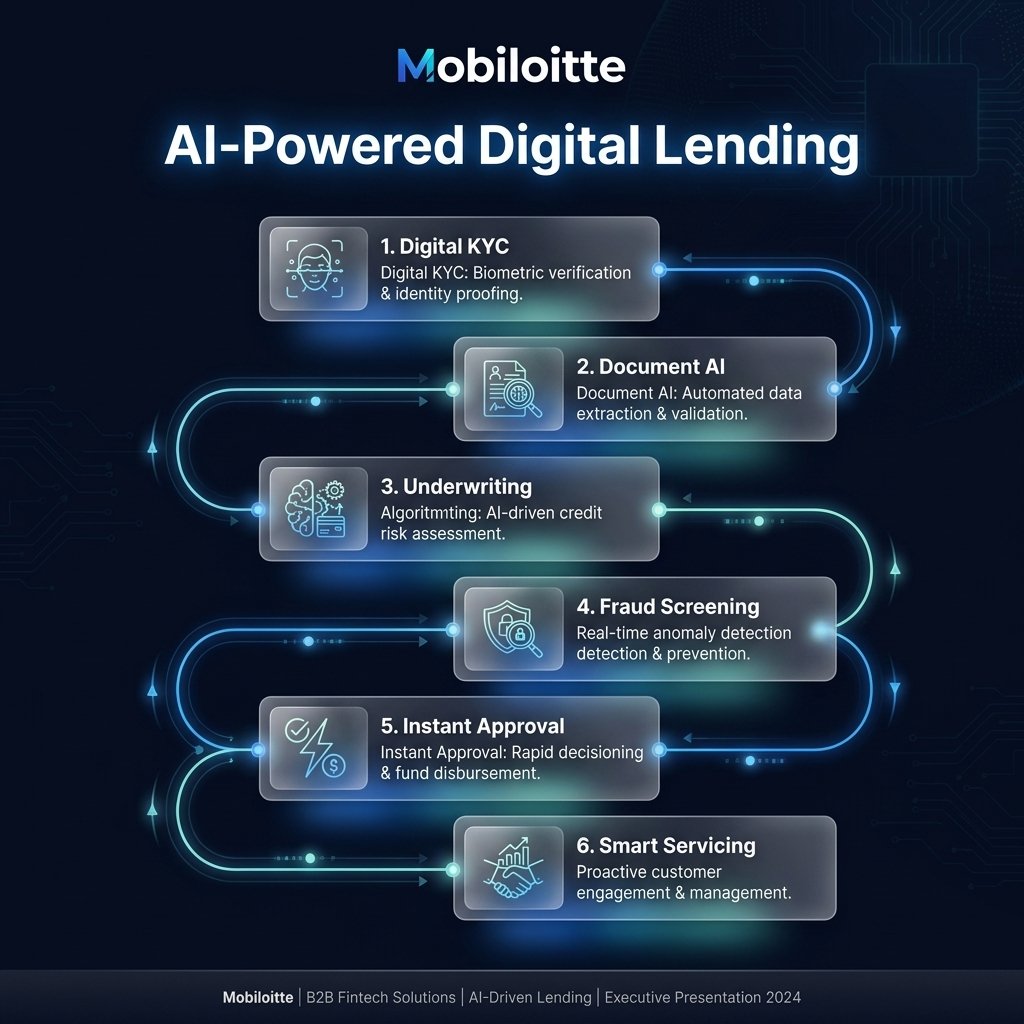

Digital lending in India is one of the clearest AI opportunities.

Underwriting, fraud checks, document AI, vernacular communication, and servicing can improve when built within the regulatory frame.

Visit: ow.ly/Cxnc50Z8FHc

9

AI for NBFCs and banks is not just automation.

It must work inside RBI expectations, customer protection, model risk, digital lending rules, and auditability.

Visit: ow.ly/u5Eb50Z8FCk

7

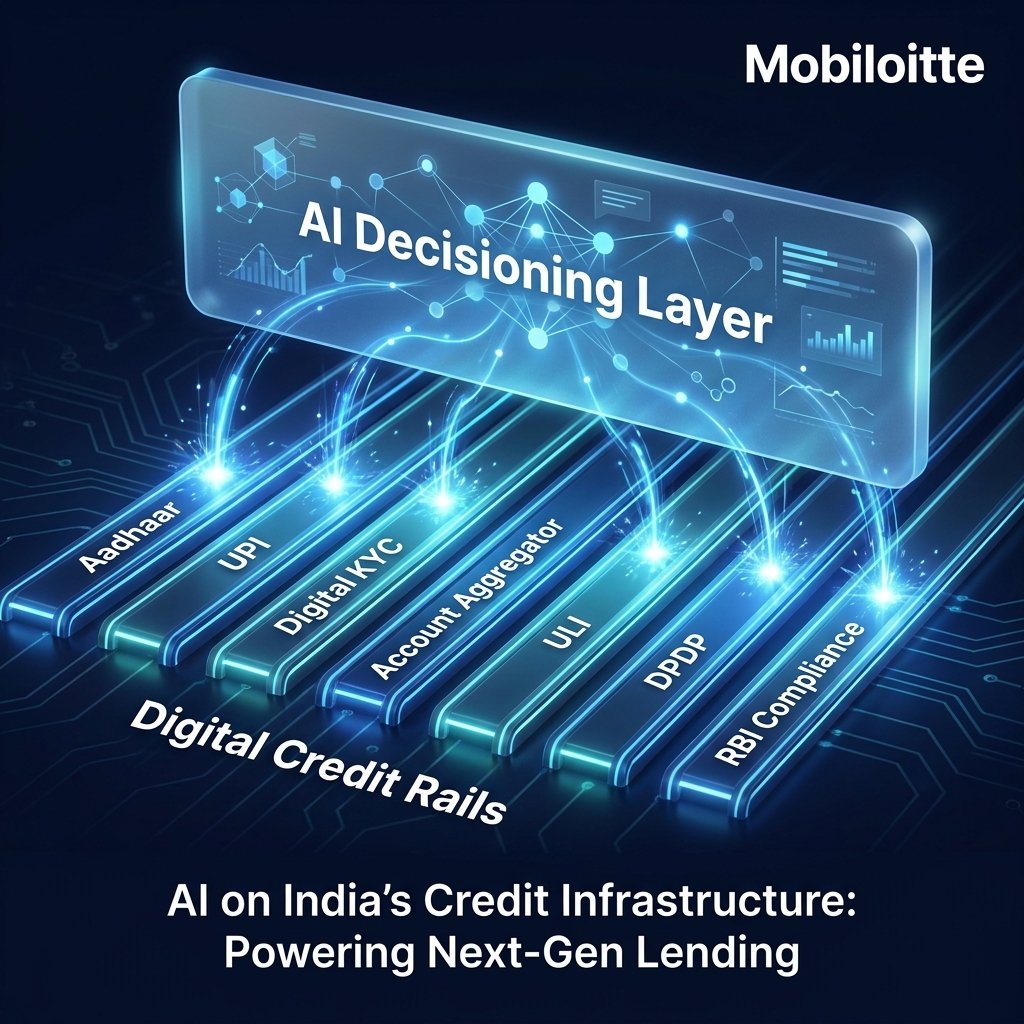

Indian financial services has built powerful credit rails: Aadhaar, UPI, Digital KYC, Account Aggregator, ULI, DPDP, and RBI frameworks.

AI can unlock the next layer of value — if built with discipline.

Visit: ow.ly/OPTB50Z8ENs

13

Collections AI can improve outcomes only when built with discipline.

Right timing. Right channel. Vernacular support. Conduct guardrails. Escalation. Audit trails.

That is where AI becomes operationally useful.

ow.ly/2EPJ50Z8nCw

2

Co-lending is operationally complex.

Two regulated entities. One borrower. Shared books. Different policies.

AI can reduce friction across eligibility, underwriting, disbursement, servicing, and reconciliation.

ow.ly/FR2F50Z8nBM

1

Digital lending in India is one of the clearest AI opportunities.

Underwriting, fraud checks, document AI, vernacular communication, and servicing can improve when built within the regulatory frame.

ow.ly/4Mvx50Z8nAn

9

AI for Indian NBFCs and banks is not just about automation.

It must work inside RBI expectations, customer protection, model risk, digital lending rules, and auditability.

ow.ly/liwa50Z8nzg

3

Indian financial services has built a powerful credit infrastructure.

Aadhaar, UPI, Digital KYC, Account Aggregator, ULI, DPDP, and RBI frameworks have changed the game.

Now AI can unlock the next layer of value.

ow.ly/vJTS50Z8nwB

6

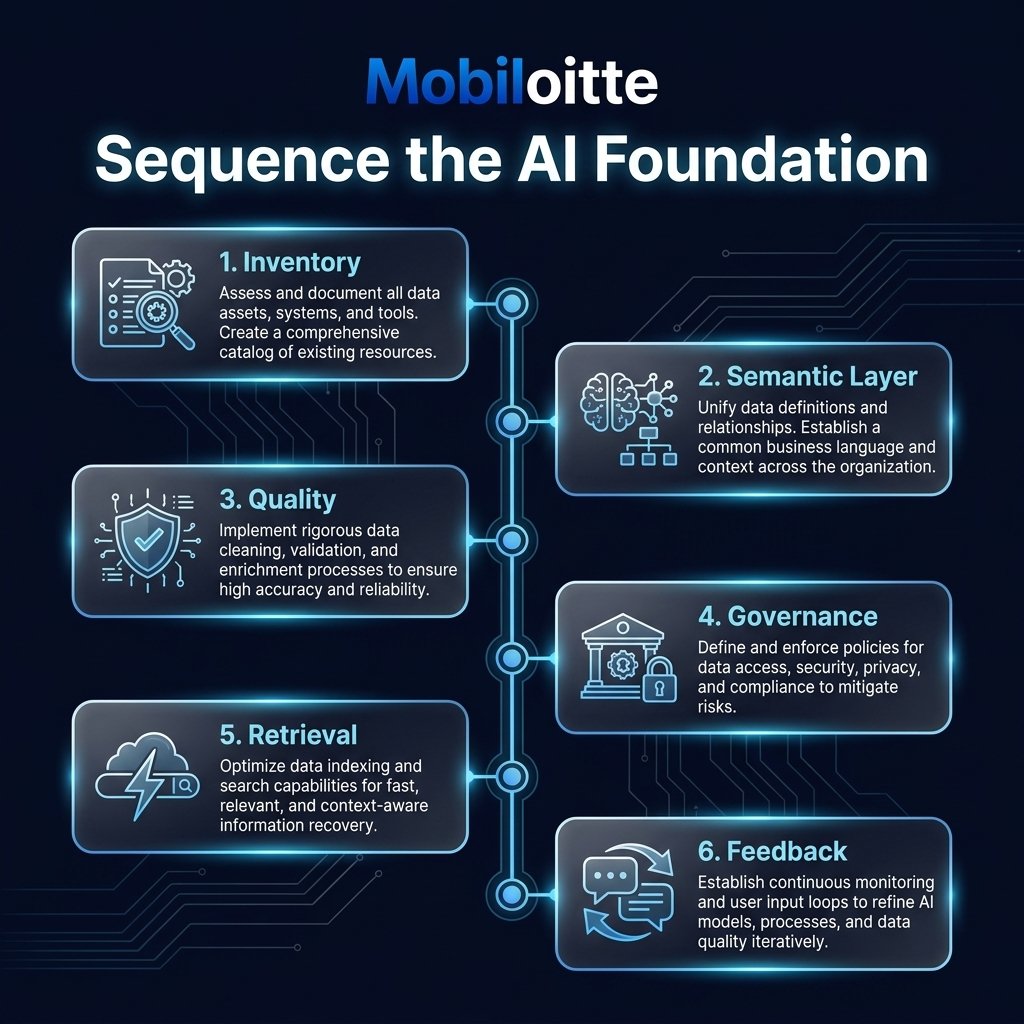

Enterprises do not need to rebuild everything for AI.

They need to sequence the foundation around the use cases that matter most.

ow.ly/qII550Z7z4f

3

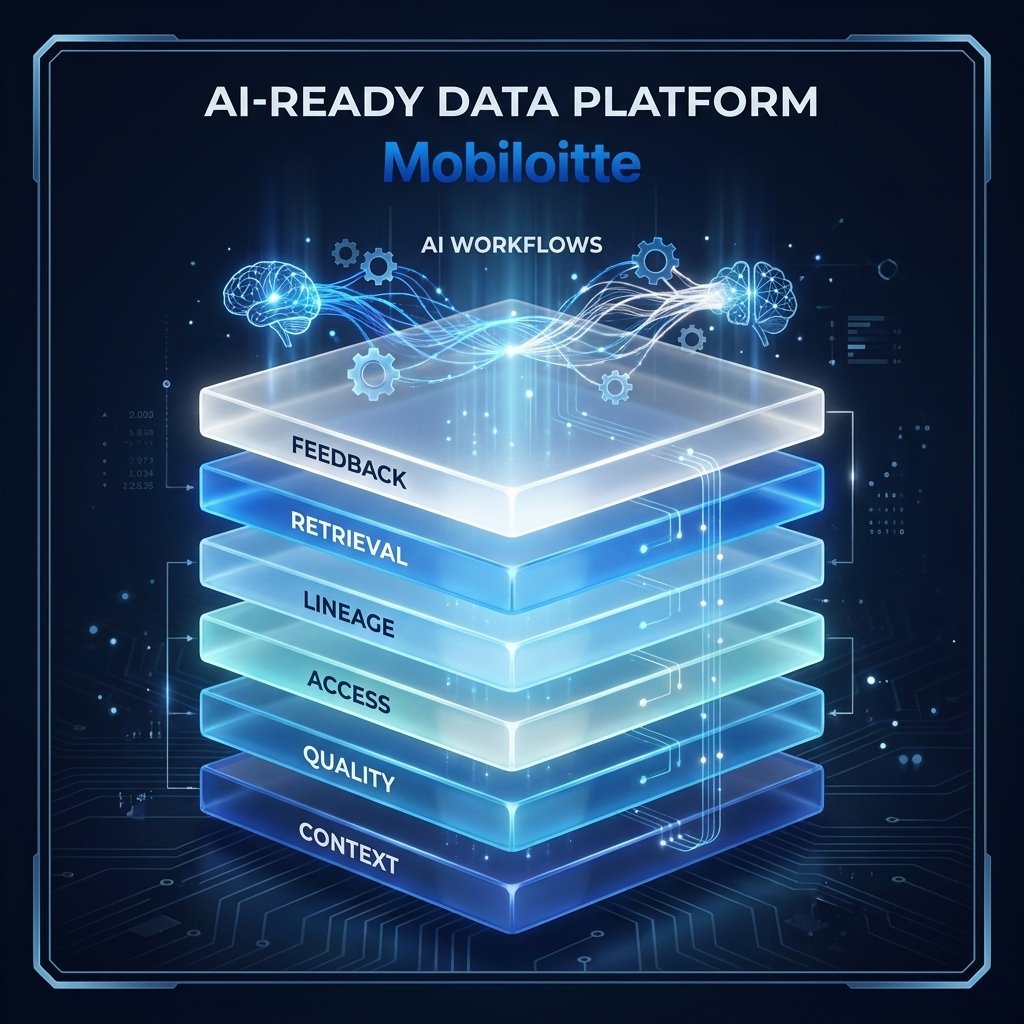

AI-ready data platforms are not tools.

They are engineered layers for context, quality, access, lineage, retrieval, and feedback.

ow.ly/rJIk50Z7z3t

3

Enterprise AI pilots usually stall for one reason:

The data layer was never designed for production AI.

Models need a foundation.

ow.ly/xFsQ50Z7yTu

9

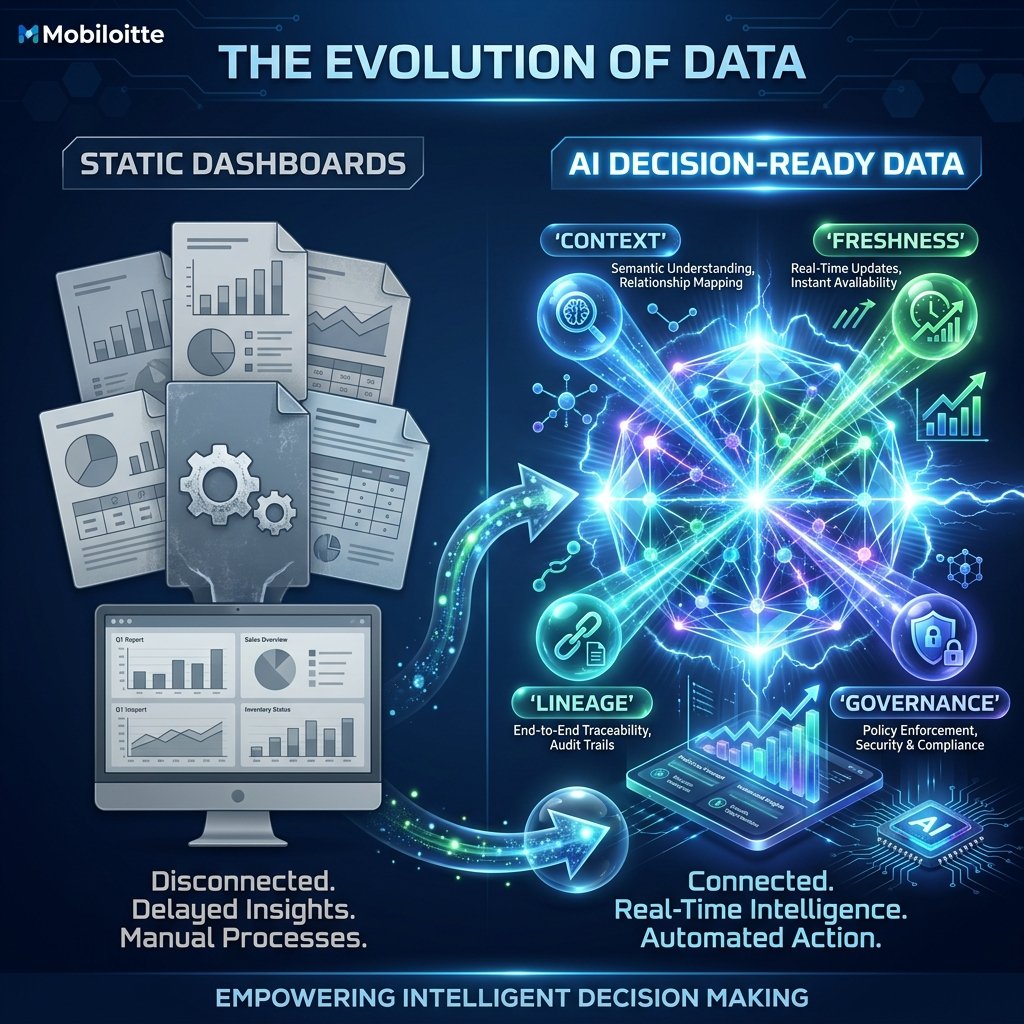

AI does not consume data like a dashboard.

It consumes data like a decision system.

Context, freshness, lineage, and governance matter.

ow.ly/Qr5650Z7yyW

7

Most enterprise AI does not fail on the model.

It fails on the data foundation underneath it.

Fix the foundation before scaling AI.

ow.ly/bMg950Z7yuQ

3

Multi-agent systems sound powerful.

But most enterprise workflows are better served by one strong agent than several weak ones.

Design before adding complexity.

Contact: ow.ly/X7pe50Z61ai

1

22

Guardrails are not friction.

For enterprise AI agents, guardrails are what make action safe, governed, and trusted in production.

Contact: ow.ly/4eNZ50Z617r

15