Looking for niche market leaders with long investment runways. Not financial advice. Always do your own due diligence.

Joined January 2021

- Tweets 228

- Following 327

- Followers 9,417

- Likes 1,570

108 Photos and videos

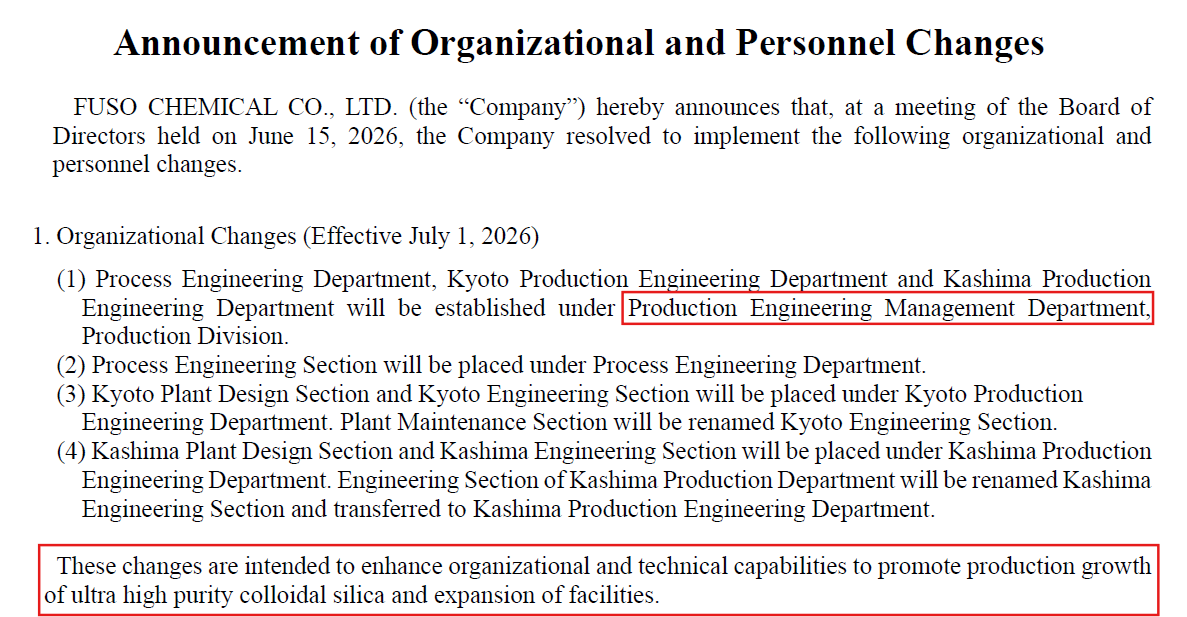

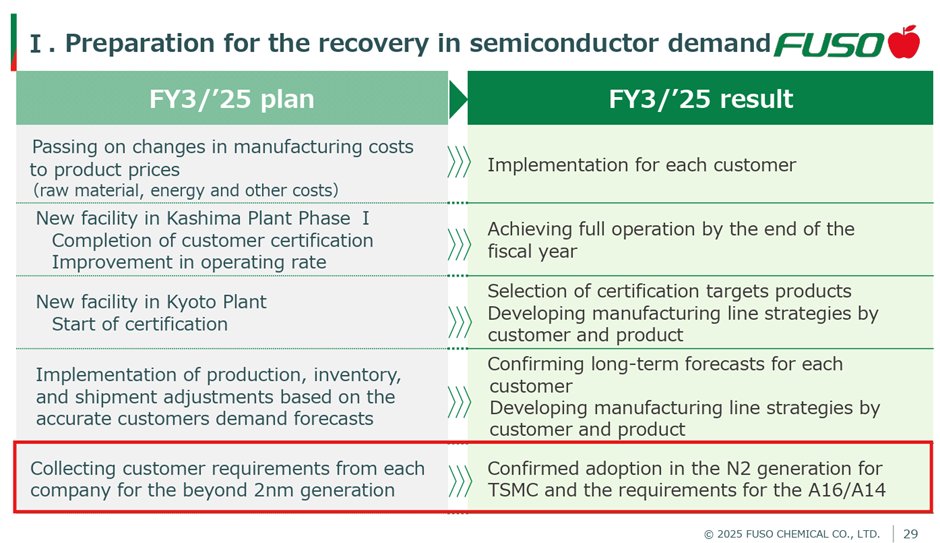

$4368.T FUSO Chemical is scaling new silica facilities into strong wafer-polishing demand from TSMC, Samsung, Intel, and others. Given the high demand, management execution is now the key swing factor.

Apr 11

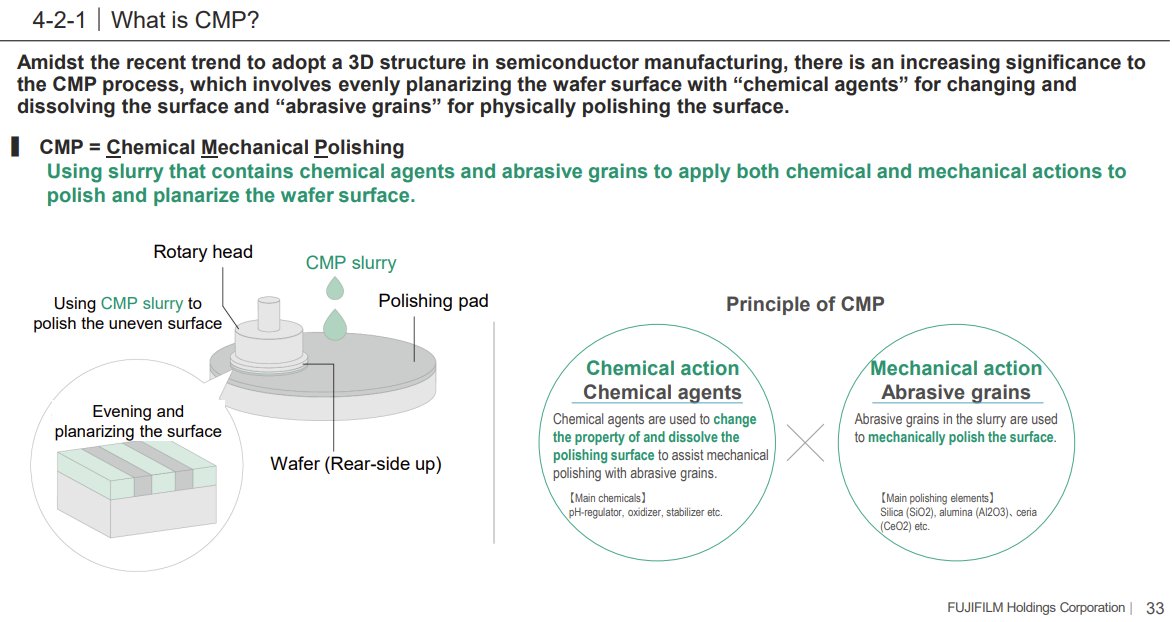

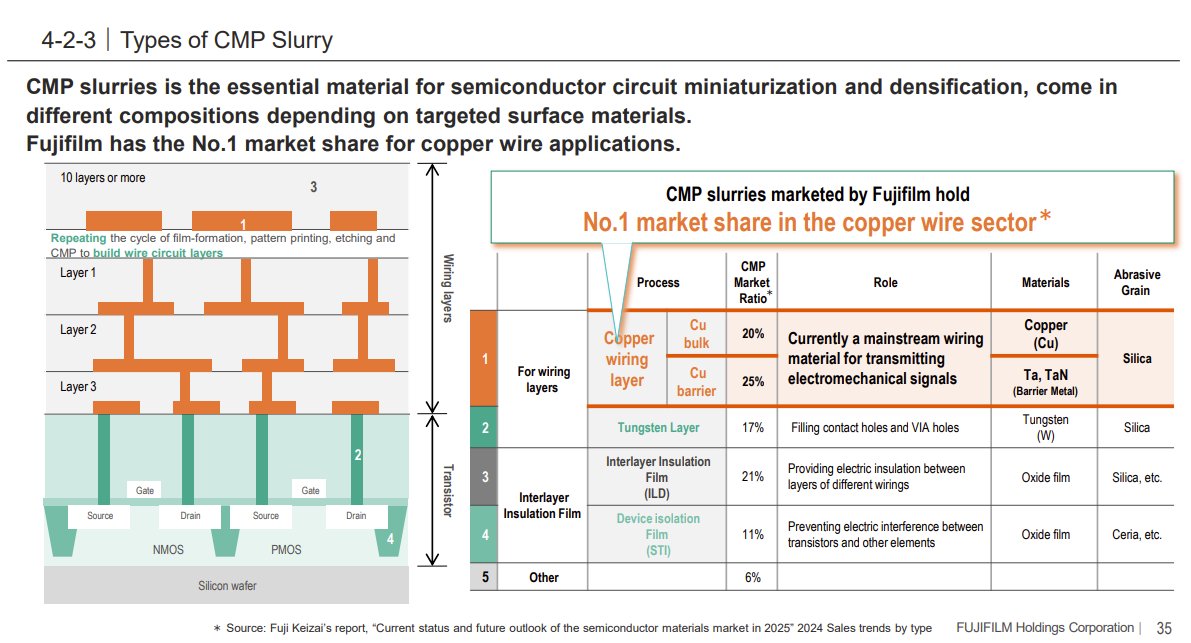

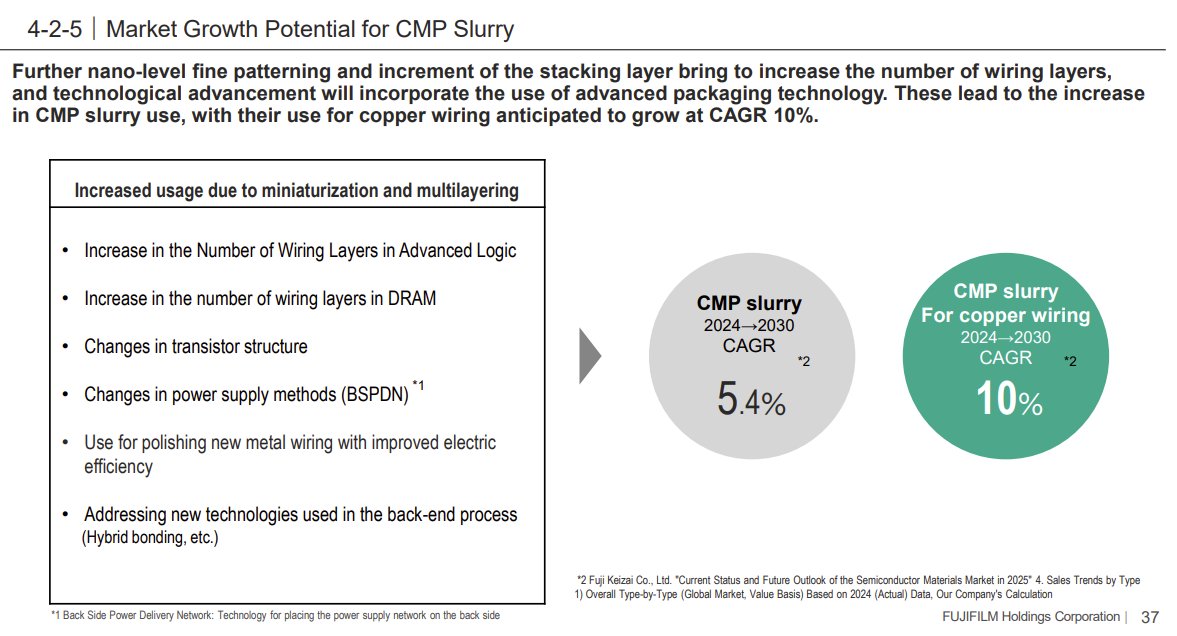

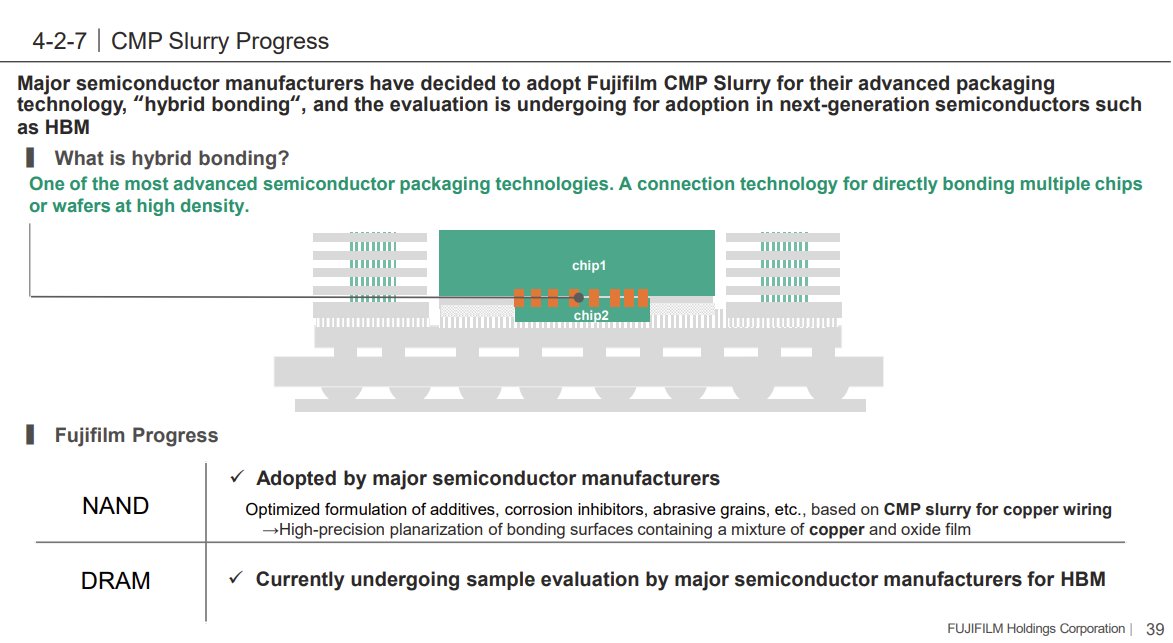

Fujifilm (4901.JP) expects CMP slurry use to intensify in advanced semiconductor manufacturing, directly benefiting suppliers of abrasive grains (FUSO Chemical, 4368.JP) and polishing pads (Fujibo Holdings, 3104.JP).

Fujifilm leads the copper interconnect CMP slurry market and is the second-largest slurry supplier globally. It works closely with FUSO to develop CMP slurries using ultra-high-purity colloidal silica for polishing wiring layers on silicon wafers.

Fujifilm sees several structural drivers behind accelerating slurry demand: (1) increasing layer count in logic and memory chips, (2) proliferation of GAA transistors with complex geometry, (3) adoption of backside power delivery, and (4) transition to more complex bonding processes (hybrid bonding) in chip packaging. The supply can hardly meet this demand, giving the key producers considerable pricing power. I think they will finally use it. This year, FUSO is increasing its silica prices by 5-10% for the first time (to my knowledge).

FUSO Chemical is the second-largest position in my portfolio. I see about 70% upside to ¥5,300 per share. I think investors underestimate the silica demand multipliers, operating leverage price hikes, and the land-grab opportunity in China.

1

11

2,276

Jun 12

However ambitious, these $SPCX targets signal high-volume precision machining. Scaling rockets, satellites, and orbital infrastructure will require advanced machining centers and automated cells from Japanese CNC leaders like Makino $6135.T, DMG Mori $6141.T, and Okuma $6103.T

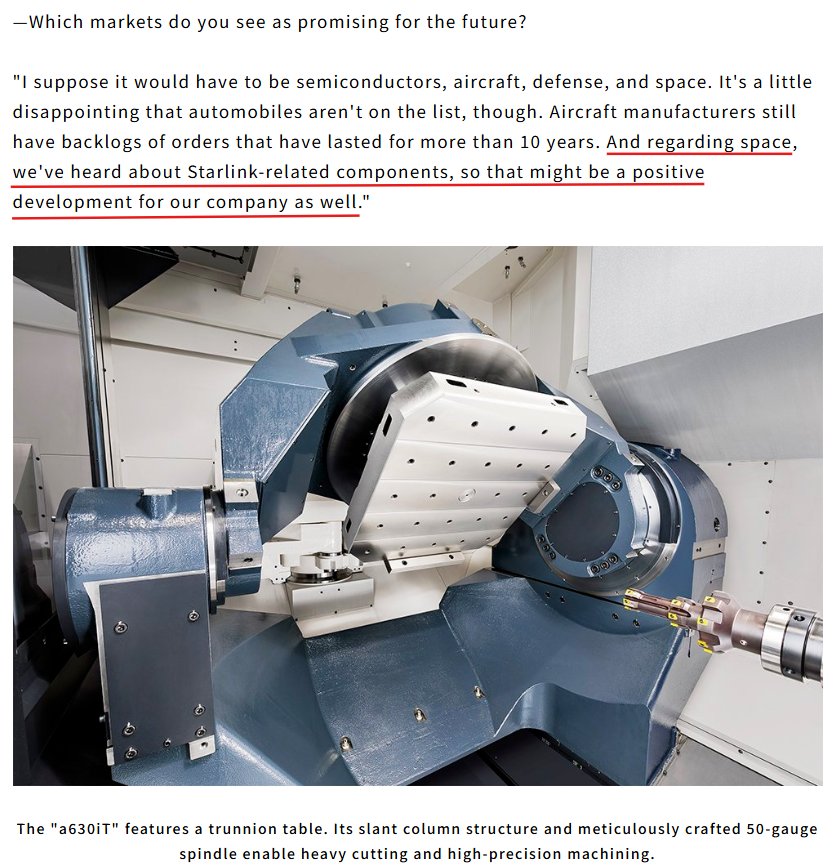

$6135.T In a March interview, Makino's sales executive said: “We’ve heard about Starlink-related components, so that might be a positive development for our company as well.” I checked, and he is right - SpaceX likely uses Makino's machines to make Starlink satellites.

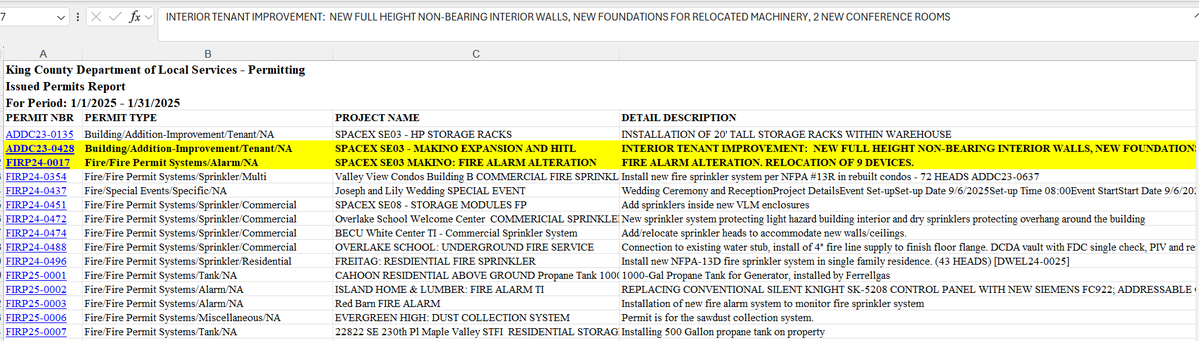

SpaceX manufactures Starlink satellites at the dedicated facility in Redmond, Washington. GPT 5.5 helped me unearth local county permit records, which show new foundations for relocated machinery and related fire-alarm alterations in early 2025 under the project name "SPACEX SE03 - MAKINO EXPANSION AND HITL".

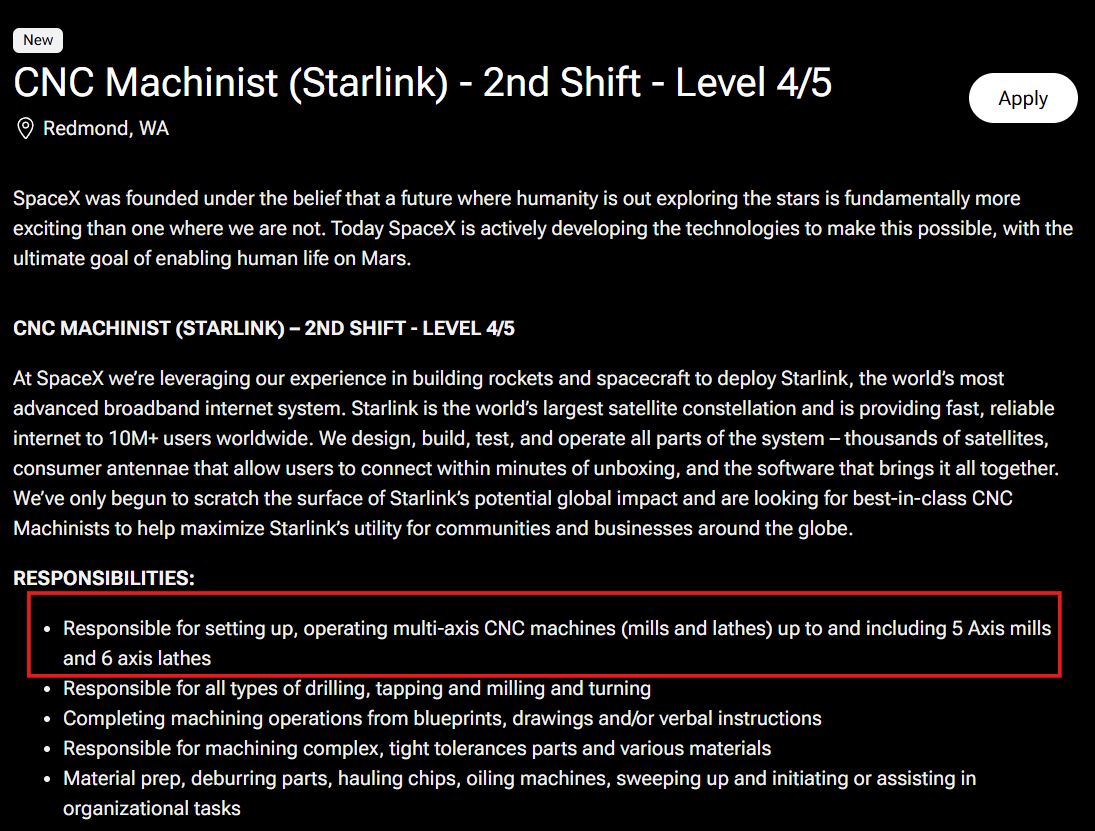

In addition, SpaceX is looking for experienced machinists for the Redmond facility to operate multi-axis CNC machines, including 5-axis mills and 6-axis lathes.

This convinced me that Elon is also a fan of Makino's gigantic "mother machines".

2

23

3,401

Jun 11

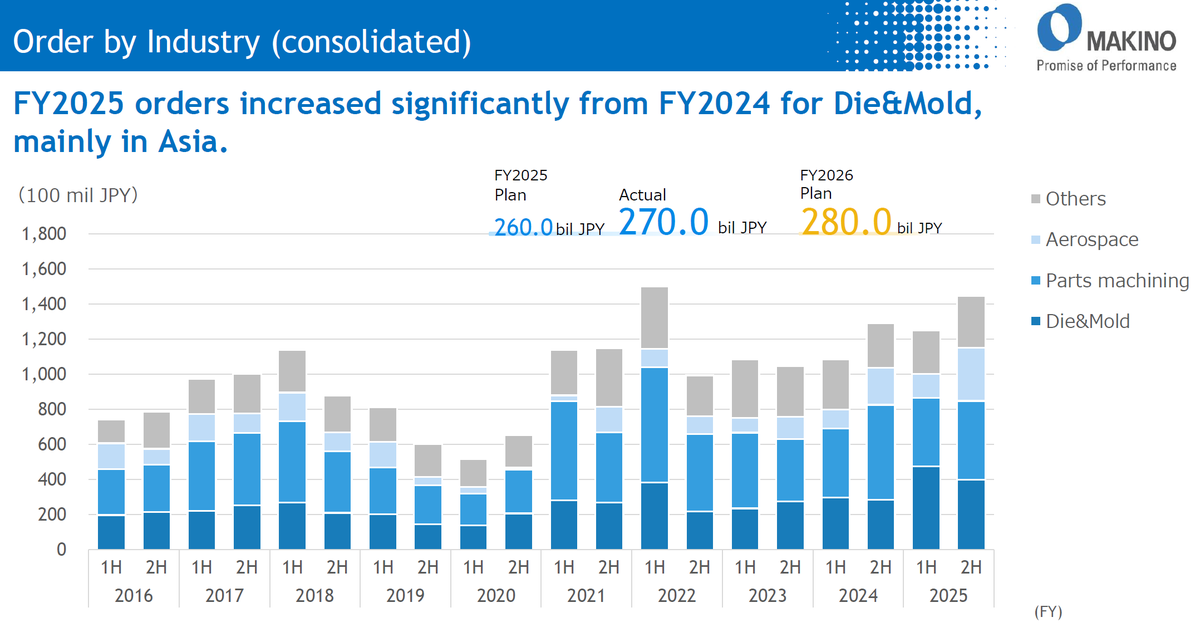

Japanese machine tool makers posted strong May orders, up 37% YoY. $6101.T Tsugami stood out with 153% growth, driven by demand from the automotive and data center clients. $6135.T Makino also delivered a solid 15% increase, supported by aerospace demand in the US and Europe.

2

3

51

5,731

$6135.T Makino hasn’t announced a stock buyback yet because it is still officially in play. NSSK made a non-binding, preliminary acquisition proposal for Makino in April without details. The board is evaluating the proposal and won’t buy back shares in the meantime.

I don’t think this deal will go through.

Unlike MBK Partners, NSSK should clear regulatory hurdles as a Japanese private equity investor. But I don't see it as an obviously superior long-term Makino owner. NSSK has historically focused on healthcare, education, retail, leisure, general manufacturing, and other mid-market businesses. These are very different investments from the world-class machine tools franchise with sensitive defense technologies.

Furthermore, Makino’s share price has increased to ~¥15,000 (market cap ¥350b ex treasury shares) since MBK’s ¥11,751 offer, so NSSK needs to propose a meaningfully higher price today. NSSK’s IV Series Funds closed at ¥250b in March. Given this, a complete Makino buyout will be impossible to pull off without serious financial backing from a local equity consortium and Japanese banks. Getting so many (conservative) parties on board to bid around ¥18,000-20,000 won't be easy.

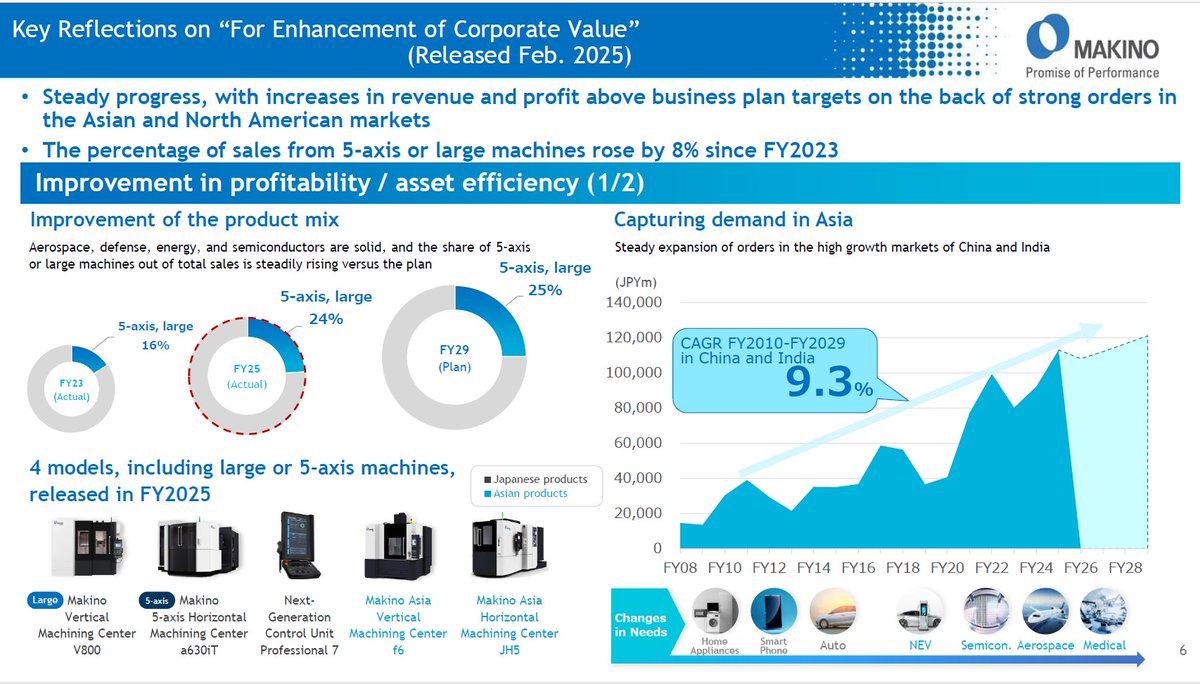

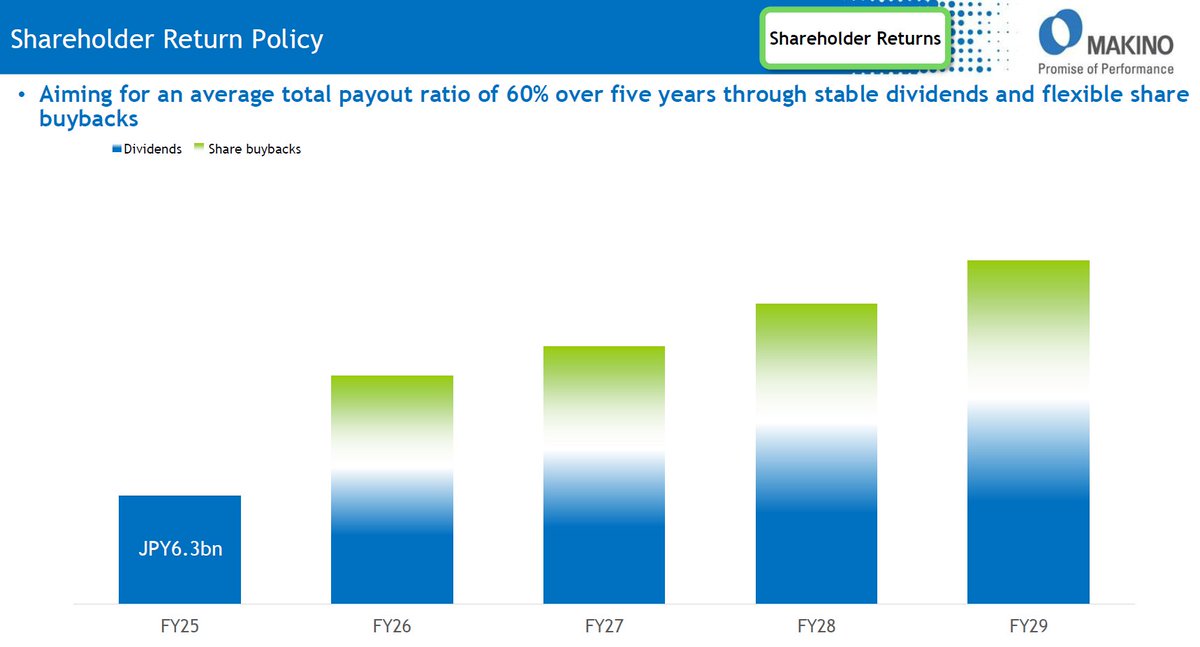

I believe the most likely outcome is that Makino stays an independent, publicly listed entity. This will be the best result for shareholders in the long run. Management now has a credible medium-term plan focused on the right levers. I count on it to expand margins, increase working capital turnover, and reduce lead times, boosting free cash flow. I assume Makino will generate ¥25-30b FCF annually in the next two-three years, creating significant room for shareholder returns.

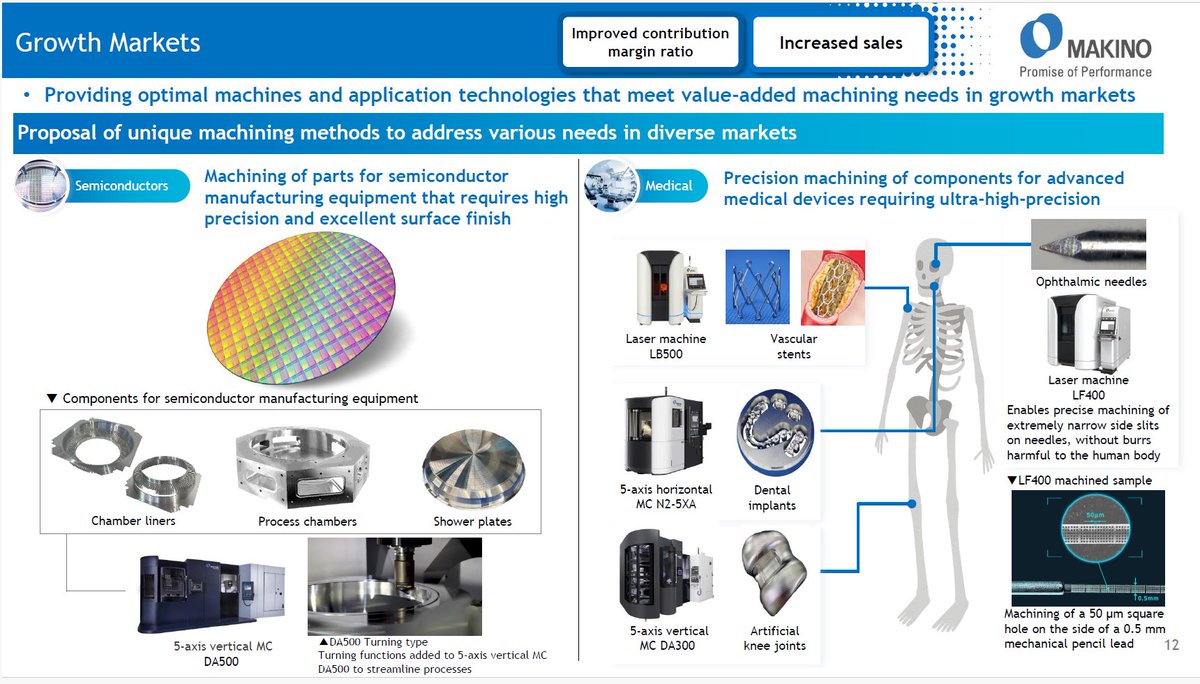

After digging around, I finally settled on my favorite Japanese machine tool producer: Makino $6135.T From giga-casting molds and satellite structures to gas turbine cooling holes and vascular stents, Makino’s tools excel in the toughest machining jobs.

The failed Nidec acquisition in 2025 and the blocked PE buyout in April revealed the company’s strategic value. The Japanese government blocked MBK Partners’ acquisition of Makino on national security grounds, arguing that its machines “are widely utilized by manufacturers of defense equipment in Japan.” I found several examples of Makino machines inside defense manufacturing ecosystems across Japan, Europe, and the US. They are used to make flight-critical structures and propulsion components for F-35 and Typhoon fighter jets, CH-47 and OH-1 helicopter engines, and gas turbines of Japanese destroyers.

Beyond defense, management is also targeting aerospace, energy, semiconductor, and medical markets, where customers need high-precision machining of difficult materials and are willing to pay up for productivity, accuracy, and process know-how. Key applications are aircraft engine parts, gas turbines, semiconductor equipment, and medical devices.

Makino’s opportunity in the emerging space economy deserves a separate post. The US satellite producer Astranis uses Makino MAG3.EX to machine full satellite panels in-house (video linked below). I’m also fairly confident that Makino machines are integrated into the supply chains of SpaceX and Blue Origin.

After the acquisition fiasco, management is under pressure to unlock Makino’s true potential. The “Corporate Value Enhancement” plan announced in May focuses on larger and more complex machines, pricing discipline, shorter lead times, higher-margin engineering and aftermarket services, dividends, and buybacks.

The plan is good, but I think it undersells the opportunity. I assume the company will achieve at least 7% revenue CAGR and reach 15% operating margin by 2030. That gets me to ¥21,500 per share or ~50% upside. At ~13 P/E, Makino looks too cheap for its strategic importance, technical depth, and end-market optionality. I took an initial position this week and will be watching for the buyback announcement and continued order build-up.

1

3

22

7,076

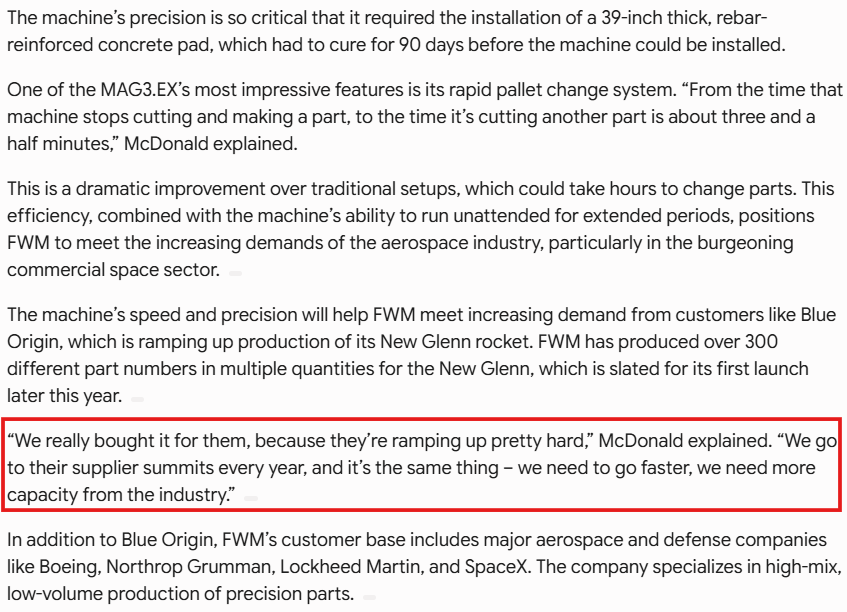

Blue Origin also relies on Makino's ($6135.T) machines for its critical parts. Fort Walton Machining bought Makino's MAG3.EX in early 2024 to keep up with the New Glenn rocket ramp. The CEO, Tim McDonald, talks about unrelenting pressure on the supply chain to increase output.

$6135.T In a March interview, Makino's sales executive said: “We’ve heard about Starlink-related components, so that might be a positive development for our company as well.” I checked, and he is right - SpaceX likely uses Makino's machines to make Starlink satellites.

SpaceX manufactures Starlink satellites at the dedicated facility in Redmond, Washington. GPT 5.5 helped me unearth local county permit records, which show new foundations for relocated machinery and related fire-alarm alterations in early 2025 under the project name "SPACEX SE03 - MAKINO EXPANSION AND HITL".

In addition, SpaceX is looking for experienced machinists for the Redmond facility to operate multi-axis CNC machines, including 5-axis mills and 6-axis lathes.

This convinced me that Elon is also a fan of Makino's gigantic "mother machines".

1

2

38

8,540

Nothing cuts through the noise like direct client feedback. Makino $6135.T

10 Dec 2025

The Makino MAG3.EX (top right image) is a beast.

130 kW spindle. 33,000 rpm. Can remove 75 pounds of aluminum per minute. 5 micron tolerance (!). 1,600 sq ft footprint.

And it lets us make a part in a single day that would take a *year* to get from an outside shop.

10

6,250

$6135.T In a March interview, Makino's sales executive said: “We’ve heard about Starlink-related components, so that might be a positive development for our company as well.” I checked, and he is right - SpaceX likely uses Makino's machines to make Starlink satellites.

SpaceX manufactures Starlink satellites at the dedicated facility in Redmond, Washington. GPT 5.5 helped me unearth local county permit records, which show new foundations for relocated machinery and related fire-alarm alterations in early 2025 under the project name "SPACEX SE03 - MAKINO EXPANSION AND HITL".

In addition, SpaceX is looking for experienced machinists for the Redmond facility to operate multi-axis CNC machines, including 5-axis mills and 6-axis lathes.

This convinced me that Elon is also a fan of Makino's gigantic "mother machines".

After digging around, I finally settled on my favorite Japanese machine tool producer: Makino $6135.T From giga-casting molds and satellite structures to gas turbine cooling holes and vascular stents, Makino’s tools excel in the toughest machining jobs.

The failed Nidec acquisition in 2025 and the blocked PE buyout in April revealed the company’s strategic value. The Japanese government blocked MBK Partners’ acquisition of Makino on national security grounds, arguing that its machines “are widely utilized by manufacturers of defense equipment in Japan.” I found several examples of Makino machines inside defense manufacturing ecosystems across Japan, Europe, and the US. They are used to make flight-critical structures and propulsion components for F-35 and Typhoon fighter jets, CH-47 and OH-1 helicopter engines, and gas turbines of Japanese destroyers.

Beyond defense, management is also targeting aerospace, energy, semiconductor, and medical markets, where customers need high-precision machining of difficult materials and are willing to pay up for productivity, accuracy, and process know-how. Key applications are aircraft engine parts, gas turbines, semiconductor equipment, and medical devices.

Makino’s opportunity in the emerging space economy deserves a separate post. The US satellite producer Astranis uses Makino MAG3.EX to machine full satellite panels in-house (video linked below). I’m also fairly confident that Makino machines are integrated into the supply chains of SpaceX and Blue Origin.

After the acquisition fiasco, management is under pressure to unlock Makino’s true potential. The “Corporate Value Enhancement” plan announced in May focuses on larger and more complex machines, pricing discipline, shorter lead times, higher-margin engineering and aftermarket services, dividends, and buybacks.

The plan is good, but I think it undersells the opportunity. I assume the company will achieve at least 7% revenue CAGR and reach 15% operating margin by 2030. That gets me to ¥21,500 per share or ~50% upside. At ~13 P/E, Makino looks too cheap for its strategic importance, technical depth, and end-market optionality. I took an initial position this week and will be watching for the buyback announcement and continued order build-up.

3

9

74

46,112

After digging around, I finally settled on my favorite Japanese machine tool producer: Makino $6135.T From giga-casting molds and satellite structures to gas turbine cooling holes and vascular stents, Makino’s tools excel in the toughest machining jobs.

The failed Nidec acquisition in 2025 and the blocked PE buyout in April revealed the company’s strategic value. The Japanese government blocked MBK Partners’ acquisition of Makino on national security grounds, arguing that its machines “are widely utilized by manufacturers of defense equipment in Japan.” I found several examples of Makino machines inside defense manufacturing ecosystems across Japan, Europe, and the US. They are used to make flight-critical structures and propulsion components for F-35 and Typhoon fighter jets, CH-47 and OH-1 helicopter engines, and gas turbines of Japanese destroyers.

Beyond defense, management is also targeting aerospace, energy, semiconductor, and medical markets, where customers need high-precision machining of difficult materials and are willing to pay up for productivity, accuracy, and process know-how. Key applications are aircraft engine parts, gas turbines, semiconductor equipment, and medical devices.

Makino’s opportunity in the emerging space economy deserves a separate post. The US satellite producer Astranis uses Makino MAG3.EX to machine full satellite panels in-house (video linked below). I’m also fairly confident that Makino machines are integrated into the supply chains of SpaceX and Blue Origin.

After the acquisition fiasco, management is under pressure to unlock Makino’s true potential. The “Corporate Value Enhancement” plan announced in May focuses on larger and more complex machines, pricing discipline, shorter lead times, higher-margin engineering and aftermarket services, dividends, and buybacks.

The plan is good, but I think it undersells the opportunity. I assume the company will achieve at least 7% revenue CAGR and reach 15% operating margin by 2030. That gets me to ¥21,500 per share or ~50% upside. At ~13 P/E, Makino looks too cheap for its strategic importance, technical depth, and end-market optionality. I took an initial position this week and will be watching for the buyback announcement and continued order build-up.

3

13

87

35,844

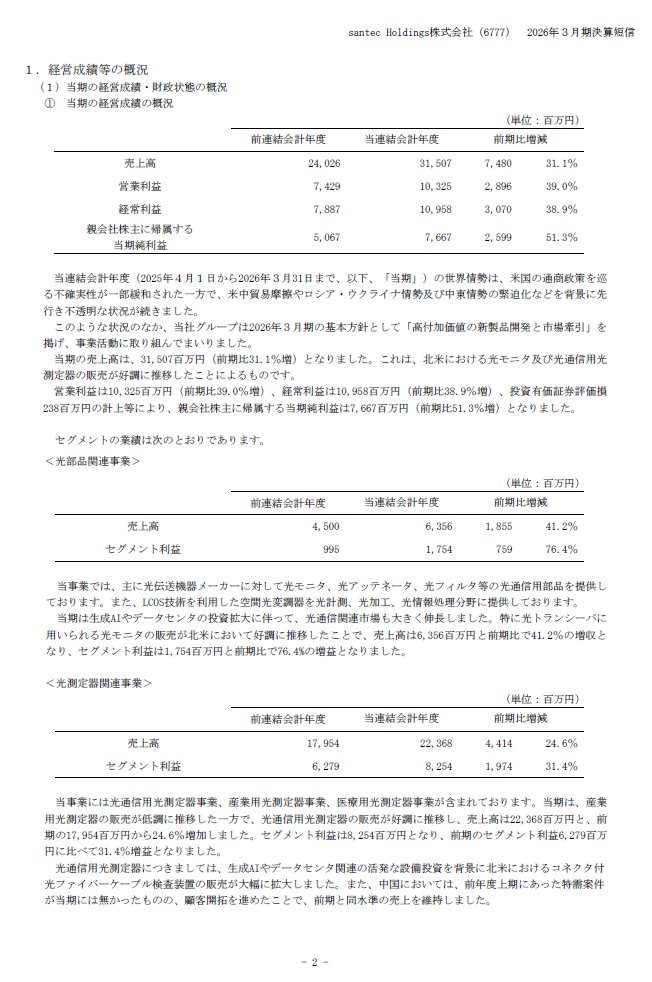

Nothing about CPO production slot wins in Santec’s $6777.T briefing. That’s important for the long term. The near-term earnings drivers are very strong – US demand for optical transceivers and fibre-cable testing is booming. Management is aggressively adding production capacity.

2

1

37

6,237

May 30

This is an insane chart for a construction tool company. MAX $6454.T sells rebar-tying tools and then earns recurring revenue from its custom tie wire. Your favorite SaaS shitco would kill for this NRR.

1

41

8,179

May 28

$255A.T Two useful takeaways from GLTechno briefing:

(1) Analytical instruments have more growth than I gave them credit for. New HPLC columns and PFAS testing consumables greatly boosted sales.

(2) Semiconductor orders are accelerating. The Vietnam plant wasn’t part of the 2024 medium-term plan. The book-to-bill was 1.4 in the last quarter.

May 20

Using proceeds from the Santec $6777.T sale, I built up a sizable position in GLTechno $255A.T GLTechno has two core businesses: (1) analytical instruments and (2) semiconductor equipment parts.

(1) The analytical instruments business, GL Sciences, is a steadily growing cash cow, selling chromatographs and related consumables to chemical producers, government institutions, pharma/biotech firms, and food manufacturers.

(2) The semiconductor business, Techno Quartz, is the main earnings driver and thesis anchor. Techno Quartz manufactures high-precision quartz glass and crystalline silicon components for semiconductor manufacturing equipment primarily used in etching and deposition processes. Applied Materials $AMAT has historically been the largest client, followed by Tokyo Electron $8035.T and Kokusai Electric $6525.T Importantly, repeat purchases of replacement parts account for ~70% of total sales.

The case is straightforward: overwhelming compute demand -> rising foundry utilization rates and expanding production capacity -> accelerated depreciation of installed equipment and increasing orders for new tools -> greater demand for Techno Quartz parts.

This demand is already evident in the company’s backlog: semiconductor orders increased 42% QoQ in the last quarter, after a 27% increase in the previous one. The key clients of Techno Quartz are all guiding for 20-30% growth in new equipment sales and 15% increase in service revenues this year, with demand visibility extending beyond 2027. Just in time for this, Techno Quartz's production capacity is set to expand 30% by January 2027.

At 14 P/E, I think GLTechno is too cheap. I see about 60% upside to ¥9,500 per share in the next 18 months.

1

2

33

13,395

May 26

$4368.T FUSO Chemical delivered - the shares are up ~60% since

Mar 24

Increased my position in FUSO Chemical (4368.JP) by 25% today. For those unfamiliar with the company, FUSO leads the market for ultra-high-purity silica particles used in chemical slurries to polish silicon wafers. After updating the valuation model, I see about 80% upside to ¥16,000 per share. I don’t think investors fully recognize structural changes in FUSO’s electronic materials business and its impact on consolidated figures. I expect this segment to reach 50% operating margins over the next two years, as the recently built silica reactors expand output and management raises prices amid tight supply. The new medium-term plan in May should provide more legs to this story. I’m surprised FUSO hasn’t been discussed much here, despite its vital role in advanced-node polishing processes. Anyway, the numbers will ultimately do the talking.

2

1

30

10,899

May 26

$6777.T Santec’s pitch for wafer-level photonics test is surprisingly ambitious. The company is bundling tunable lasers, optical power meters, swept photonics analyzers and switches for integrated HVM testing. I assumed this story was mostly about tunable lasers.

1

23

7,919

May 23

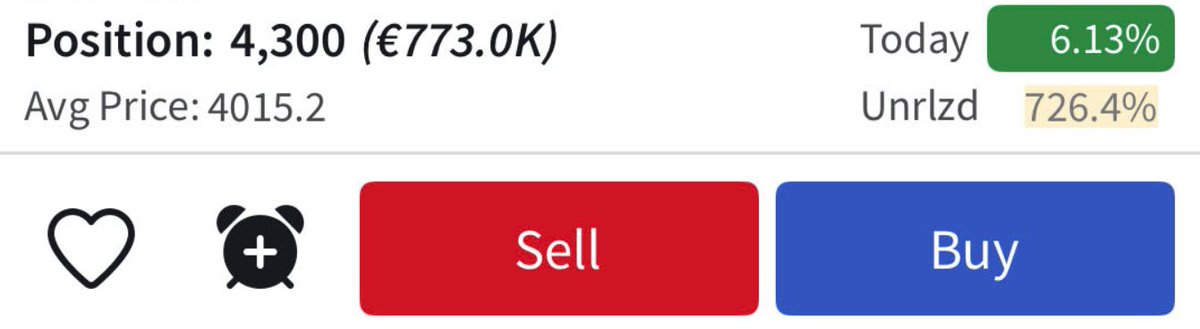

Should've shown the receipts earlier. This was right before I scaled down to 1,800 shares. I'd be lucky to catch another one like Santec $6777.T

May 18

Sold 60% of Santec $6777.T position today, locking a 700% gain. I invested 30% of my portfolio in Santec during 2023-2024 at ¥4,015, before optics exploded. This proven compounder was stupid cheap under 12 P/E. At ~50, the setup is very different. I think the current valuation fully discounts industry demand for transceivers and fiber cable testing. The upside should come from emerging CPO applications. If Santec successfully integrates its optical instruments into high-volume SiPh/CPO manufacturing, it will likely compound for years. I believe management has a fair shot, but it's not worth risking 50% of my capital.

4

1

45

15,871

May 21

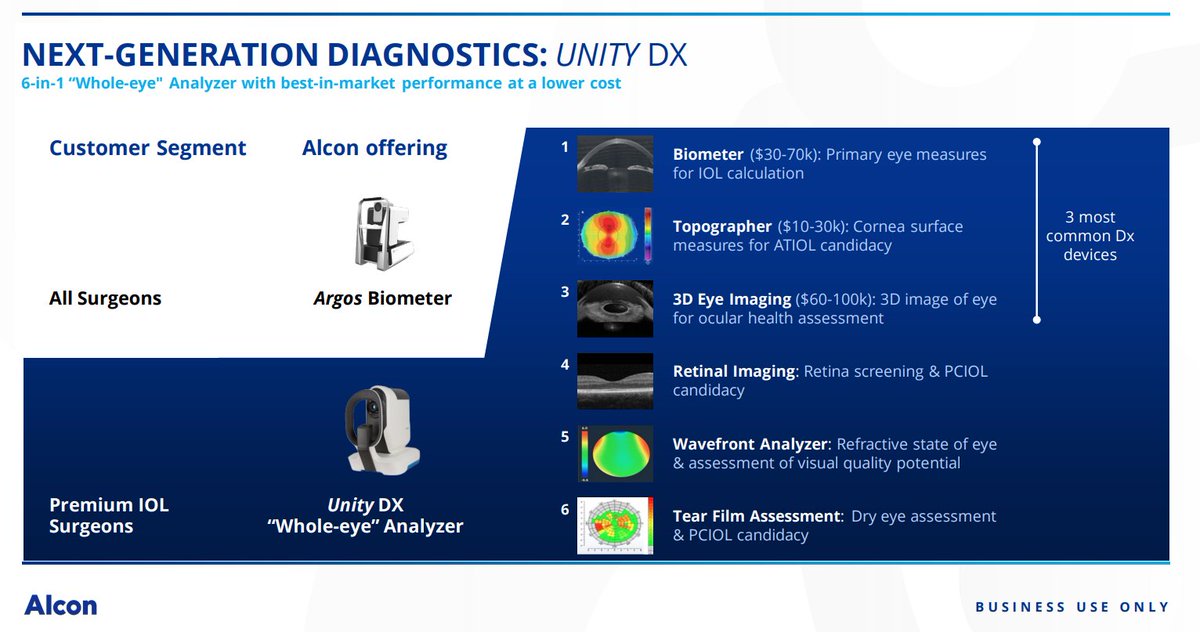

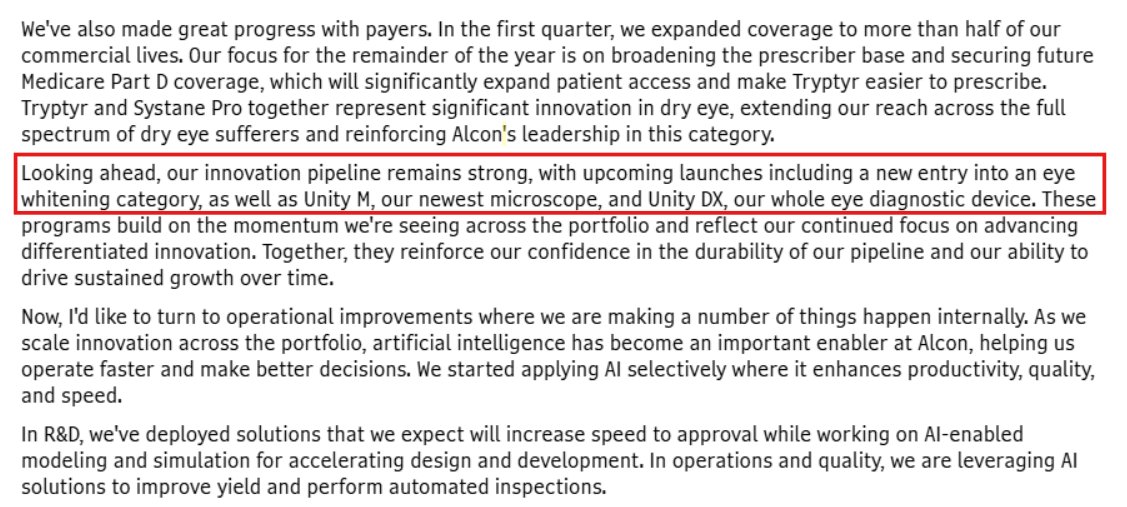

One of the main reasons I invested in Santec $6777.T was its highly lucrative medical business – MOVU. I generally understood where the optics are going, but couldn’t imagine the speed and scale of transition.

On the other hand, Santec’s success in the eye diagnostics market in partnership with Alcon $ALC was evident, but not everyone paid close attention. Two years ago, I thought investors failed to price in the upcoming launch of ARGONAUT – the new multi-modal eye imaging system that would supplement the ARGOS biometer. The irony is that the ARGONAUT is still awaiting FDA approval, while Santec’s share price took off without it. We might finally see the ARGONAUT later this year, though. On the recent earnings call, Alcon’s management indicated that Unity DX whole-eye analyzer (Alcon’s branded version of the ARGONAUT) is about to launch.

Considering Santec's rich valuation, I don’t think this will move the share price much when it happens, but it could still be a nice surprise.

2

26

7,482

May 20

Using proceeds from the Santec $6777.T sale, I built up a sizable position in GLTechno $255A.T GLTechno has two core businesses: (1) analytical instruments and (2) semiconductor equipment parts.

(1) The analytical instruments business, GL Sciences, is a steadily growing cash cow, selling chromatographs and related consumables to chemical producers, government institutions, pharma/biotech firms, and food manufacturers.

(2) The semiconductor business, Techno Quartz, is the main earnings driver and thesis anchor. Techno Quartz manufactures high-precision quartz glass and crystalline silicon components for semiconductor manufacturing equipment primarily used in etching and deposition processes. Applied Materials $AMAT has historically been the largest client, followed by Tokyo Electron $8035.T and Kokusai Electric $6525.T Importantly, repeat purchases of replacement parts account for ~70% of total sales.

The case is straightforward: overwhelming compute demand -> rising foundry utilization rates and expanding production capacity -> accelerated depreciation of installed equipment and increasing orders for new tools -> greater demand for Techno Quartz parts.

This demand is already evident in the company’s backlog: semiconductor orders increased 42% QoQ in the last quarter, after a 27% increase in the previous one. The key clients of Techno Quartz are all guiding for 20-30% growth in new equipment sales and 15% increase in service revenues this year, with demand visibility extending beyond 2027. Just in time for this, Techno Quartz's production capacity is set to expand 30% by January 2027.

At 14 P/E, I think GLTechno is too cheap. I see about 60% upside to ¥9,500 per share in the next 18 months.

2

9

99

25,099

May 20

Positive read-through for Santec from Keysight $KEYS results. The explosive demand for optics made efficient supply chain mgmt a binding constraint on profit growth. I estimate that Santec's optical instrument sales for data center interconnect rose ~70% in Q3 and 90-100% in Q4.

May 15

Very strong execution by Santec $6777.T: sales rose 53% and operating income jumped 74% YoY in Q4. This was driven entirely by the optical instrument business and demand for fiber cable testing in North America. I hope to see some clues about CPO in the management briefing.

1

27

7,917

May 18

Sold 60% of Santec $6777.T position today, locking a 700% gain. I invested 30% of my portfolio in Santec during 2023-2024 at ¥4,015, before optics exploded. This proven compounder was stupid cheap under 12 P/E. At ~50, the setup is very different. I think the current valuation fully discounts industry demand for transceivers and fiber cable testing. The upside should come from emerging CPO applications. If Santec successfully integrates its optical instruments into high-volume SiPh/CPO manufacturing, it will likely compound for years. I believe management has a fair shot, but it's not worth risking 50% of my capital.

16 Aug 2023

Santec Holdings ($6777.JP). Cheap, highly profitable, and rapidly growing producer of optical instruments and components that dominates several niche optoelectronic markets. The company has also successfully expanded into medical and semiconductor devices in the past 10 years.

6

5

144

44,884