sh!t poster and professional gambler // nfa

Joined July 2015

- Tweets 5,501

- Following 1,278

- Followers 4,528

- Likes 48,864

484 Photos and videos

Geld retweeted

Jun 11

SpaceX starts trading tomorrow under $SPCX

Here is everything you need to know

Price: $135 per share

• Valuation: $1,800,000,000,000

• What it raised: $75,000,000,000

• Total orders received: $250,000,000,000

• Oversubscribed: 3.5x

• 30% of shares reserved for retail investors

Available on: Robinhood, Fidelity, Schwab, SoFi, E-Trade

Prepare for the largest IPO in history

149

299

2,810

519,136

Geld retweeted

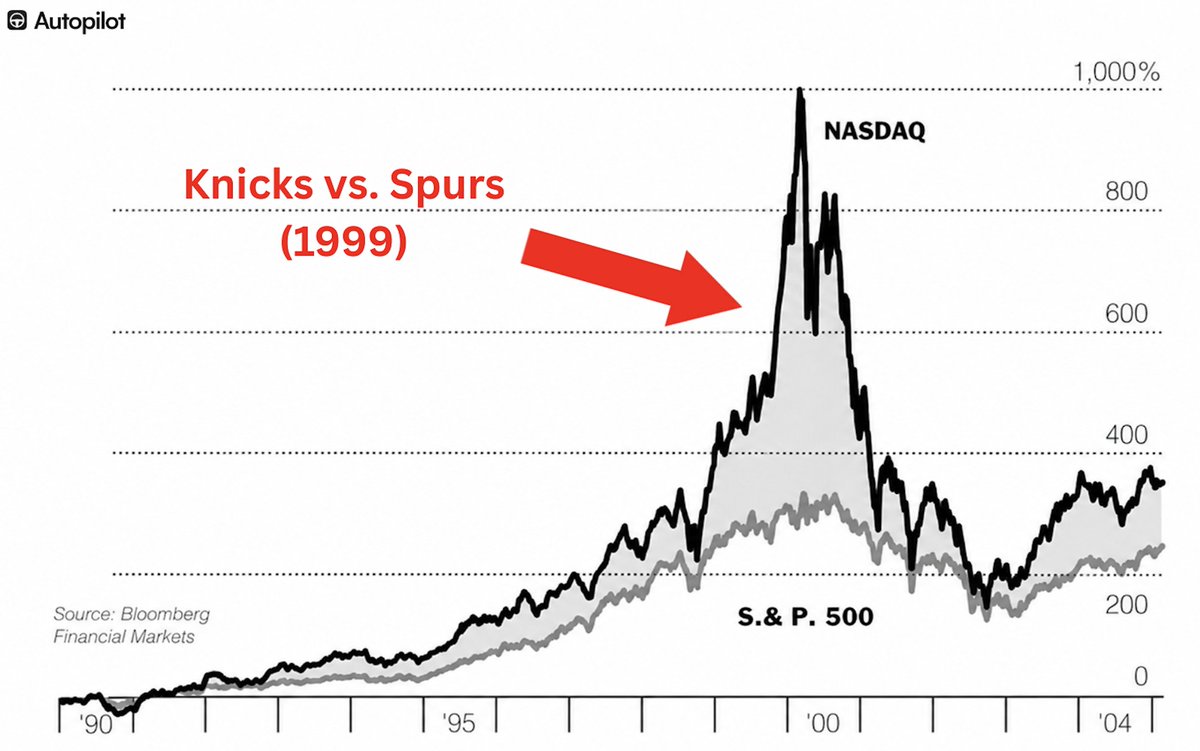

Breaking: Michael Burry said "it feels like the last months of the 1999-2000 bubble"

The last time the Knicks were in the NBA Finals, the Nasdaq peaked 9 months later and fell 78%

History is rhyming hard right now:

1999:

• Knicks are in the NBA Finals

• Nasdaq up 84% that year

• Tech was 33% of the S&P 500

• CAPE ratio hit 40x

• Margin debt at record highs

• Hedge funds had 31% of portfolios in tech

2026:

• Knicks are in the NBA Finals

• Nasdaq up 31% in 12 months

• Tech is 32% of the S&P 500

• CAPE ratio at 40x

• Margin debt at record highs

• Hedge funds have 33% of portfolios in Big Tech

250

392

1,770

206,836

November 19th

Wishlist Now: xbx.lv/4nMfojd

ALT Key Art for Grand Theft Auto VI

3,515

21,441

262,673

38,006,331

Geld retweeted

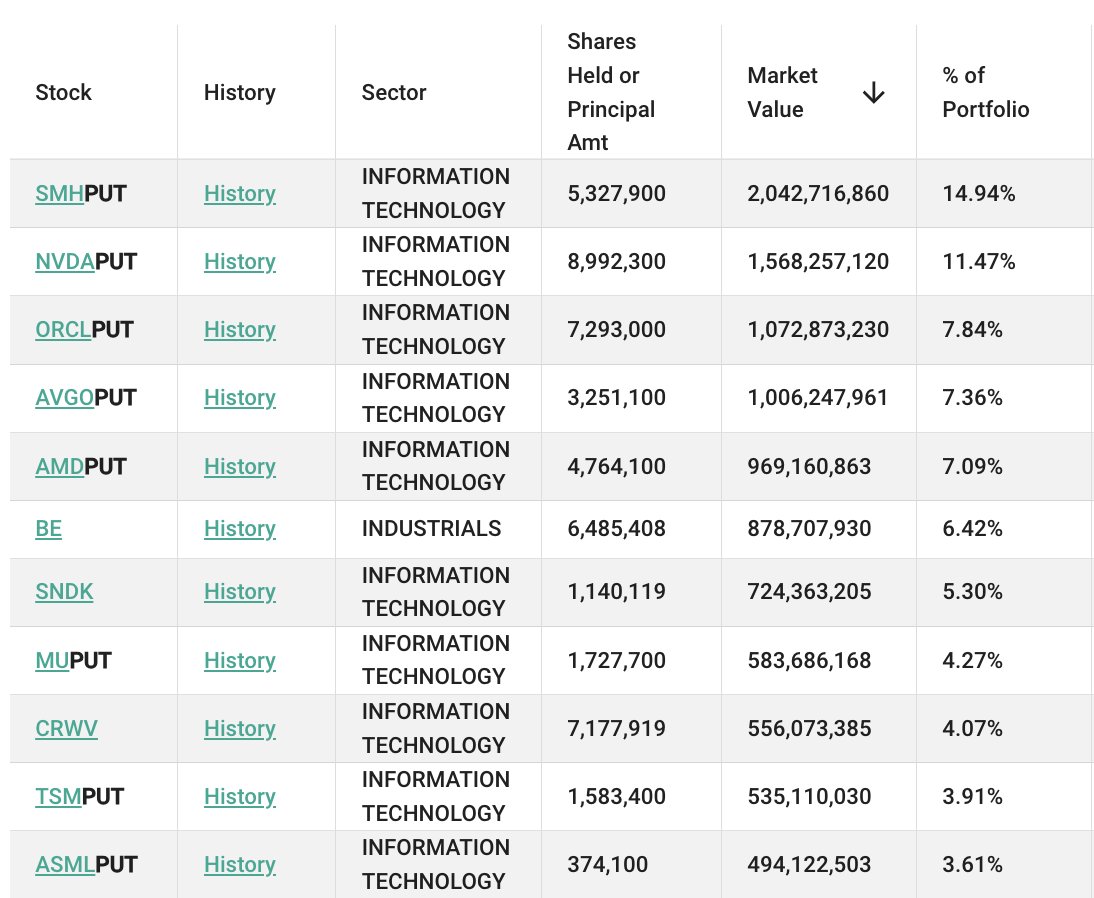

Breaking: Leopold Aschenbrenner just filed his Q1 2026 13F

Here's everything you need to know about his recent 13F

Top 10 positions:

1. VanEck Semiconductor ETF $SMH [Put] — $2.04B

2. Nvidia $NVDA [Put] — $1.57B

3. Oracle $ORCL [Put] — $1.07B

4. Broadcom $AVGO [Put] — $1.01B

5. Advanced Micro Devices $AMD [Put] — $969M

6. Bloom Energy $BE — $879M

7. SanDisk $SNDK — $724M

8. Micron $MU [Put] — $584M

9. CoreWeave $CRWV — $556M

10. Taiwan Semiconductor $TSM [Put] — $535M

New positions:

• $SMH, $NVDA, $ORCL, $AVGO, $AMD, $MU, $TSM, $ASML, $INTC, $GLW — all puts

• $MU [Call] — $422M

• $TSM [Call] — $355M

• $SNDK [Call] — $389M

Biggest adds:

• CleanSpark $CLSK: 648% shares

• Riot Platforms $RIOT: 87% shares

Biggest trims:

• CoreWeave $CRWV [Call]: -83% shares

• Bloom Energy $BE: -36% shares

Full exits:

• Intel $INTC [Call] — was $747M

• Lumentum $LITE — was $479M

• EQT Corp $EQT — was $133M

• Tower Semiconductor $TSEM — was $85M

Summary: He kept his AI infrastructure longs and opened $8.45B in new puts against tech and semiconductor

Community note

13F filings report notional values for option positions (the underlying value controlled by the options) rather than the market value of the options or premiums paid.

whalewisdom.com/filer/situatio… sec.gov/rules-regulati…

334

808

8,075

3,568,941

Geld retweeted

Trump: "Go out and buy a Dell, they're great"

$DELL is up 12% today

226

610

10,822

5,859,461

Geld retweeted

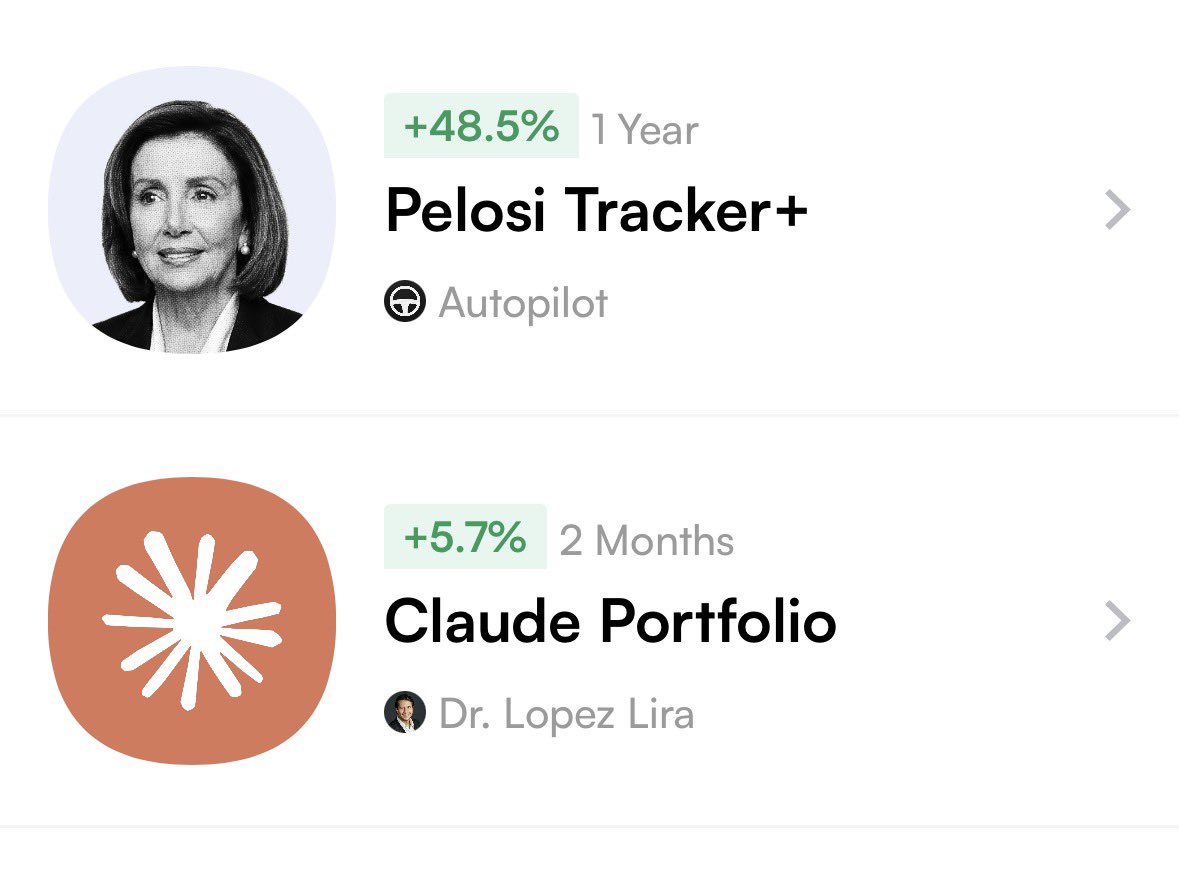

May 6

It started as a fun social media account called the @pelositracker

And it's now a full fledged app with $500M investing alongside your local politician

Because if you can't beat them, join them

S/O CBS News for covering our story

18

53

690

128,933

Geld retweeted

Once again, you’re probably overthinking what stocks to buy

May 5

Breaking: The Trump Administration is up 420% on Intel investment made August 2025

$INTC is projected to have made them ~$40,000,000,000

79

260

8,301

1,091,639

Geld retweeted

May 1

Mfs think an AI come out perform insider trading

Milestone: The Claude Portfolio just passed $15,000,000 in capital on Autopilot.

'Capital' here refers to those who've connected their brokerages and allocated funds to follow Claude’s stock picks automatically.

What started as a $50K experiment to test whether Claude’s agents could outperform the market has grown into a social-driven investing community.

Appreciate everyone following along as it continues to evolve.

74

1,110

25,713

1,722,927

I don’t think people fully understand SoFi’s business model

$SoFi is not just trying to be a bank

It also sells the white-label service other companies use

They help other fintechs handle the accounts, cards, money movement, and backend banking systems while the customer sees another logo

Their clients include:

• Robinhood

• Chime

• Revolut

• TransferWise

SoFi reports earnings on Wednesday morning if you want to watch

324

Geld retweeted

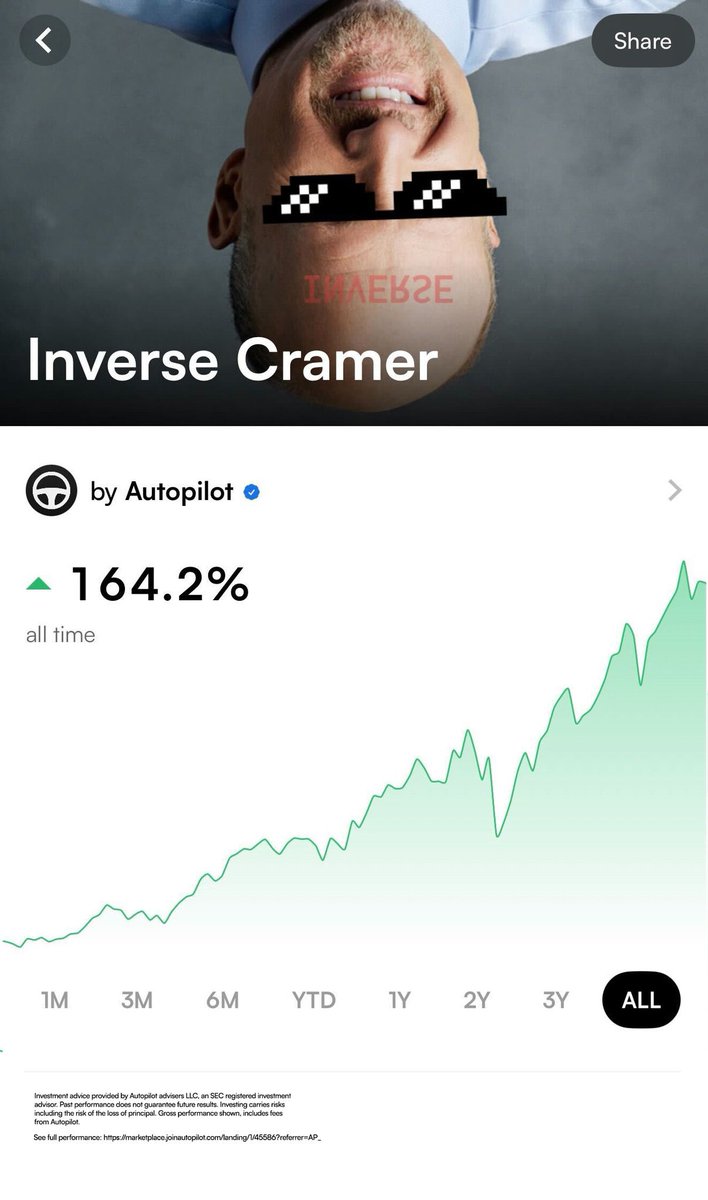

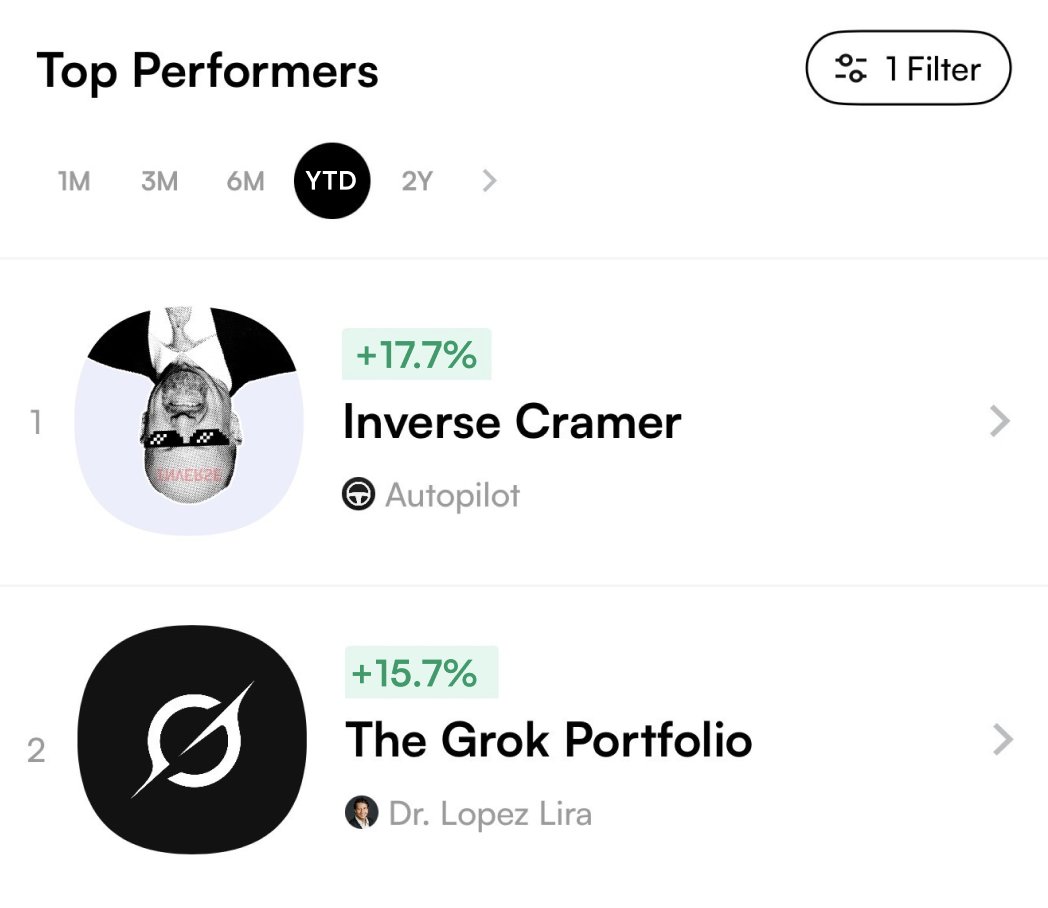

Apr 27

Inverse Cramer is about to be dethroned

6

6

61

17,184

Geld retweeted

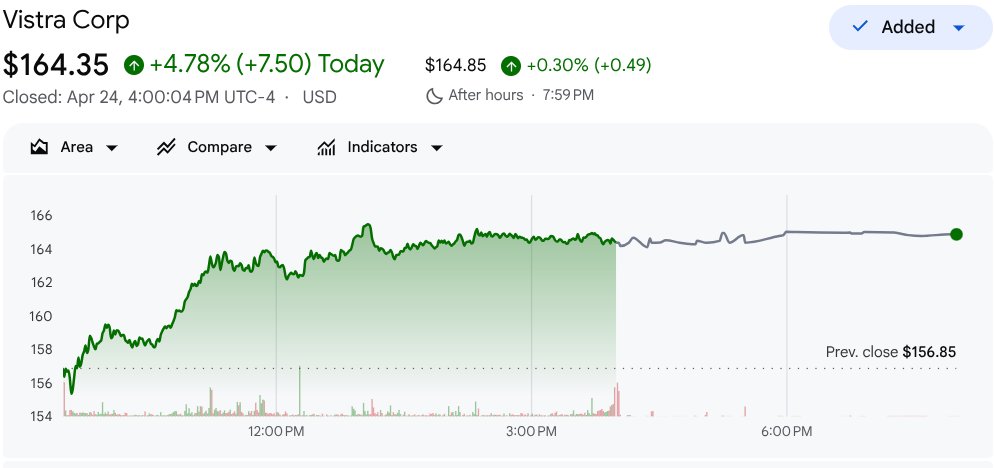

Vistra Corp $VST is the biggest position I carry, about ten percent of the book.

The pitch in one line: VST is the cleanest liquid expression of "who powers the AI." Every gigawatt of new data center load in ERCOT and PJM has to come from somewhere, and VST is the largest independent power producer across those two grids combined. They already have signed twenty-year power purchase agreements with Amazon and Meta tied to the pending Cogentrix acquisition, which adds 5,500 megawatts and is expected to close mid-to-late 2026.

The reason it's been a frustrating hold until very recently: the stock peaked at $220 in February and spent most of March drawing down twenty-five percent on a combination of natural gas at seventeen-month lows compressing merchant margins, a $4 billion debt issuance to fund Cogentrix, and regulatory overhang on PJM capacity pricing. None of those things broke the thesis, but together they took the stock from priced-for-perfection back to priced-for-skepticism.

What's changed in the last week: the $4 billion notes priced cleanly at 4.55 to 5.55 percent, removing the binary refinancing risk Morgan Stanley had been flagging. Jefferies argued in a fresh note that at current levels VST is trading at roughly an eleven percent FY28 free cash flow yield ex buybacks, and that the price is not embedding any future data center contract wins. Sixteen of nineteen analysts still rate it Strong Buy with a mean price target of $234.

What's coming into May:

a) April 27 to May 1, the hyperscaler earnings cluster. Microsoft, Meta, Amazon, Google. If aggregate AI capex is reaffirmed near the $630 billion bar the market has set, VST gets to participate in the AI re-rating without needing to do anything itself.

b) May 7, VST Q1 earnings before the open. Consensus is modeling more than two hundred percent year-over-year EPS growth. Options flow is skewed bullish into the print. The setup carries real binary risk in either direction, but the trailing seventy-two times P/E that scares people normalizes to roughly fourteen times on FY27 estimates if guidance reaffirms.

c) May 12, April CPI. A hot print pushes the ten year back toward 4.55 percent and pressures every duration-sensitive AI infrastructure name including this one. A cool print is the cleaner setup.

My probability-weighted twelve-month target is $184, about thirteen percent above current. That sits below the consensus $234 because I'm carrying a higher bear weight on a possible PJM capacity-cap proposal and on the Martin Lake arc-flash incident from April 21 that has not shown up in price yet. But the asymmetry is what keeps it the largest line: a $225 bull case if Cogentrix closes on schedule and a fresh hyperscaler PPA lands, against a $120 bear case if Q1 misses or PJM acts.

This is what the math says for me, not what it should say for anyone else.

91

77

1,283

339,865

Geld retweeted

Keep an eye on this

Rep. Sheri Biggs (R) just disclosed buying up to $250,000 of Bitcoin $IBIT on March 4th

There's a bill sitting in the Senate right now to create a Strategic Bitcoin Reserve

If it passes, the US government starts buying bitcoin at a large scale

And this isn't her first time buying Bitcoin. Last July her husband bought up to $250,000 of $IBIT one week before pro-crypto legislation passed. She was flagged for disclosing it late

Unsurprising to none, $IBIT was up 12% within 3 months of their purchase

93

285

1,789

282,257