Deep research on companies with 10x potential. Concentrated. Contrarian. | $LMND $TSLA $DUOL $HIMS substack: multibaggerresearch.substack…

Joined January 2016

- Tweets 24,975

- Following 1,534

- Followers 4,905

- Likes 50,444

5,066 Photos and videos

Pinned Tweet

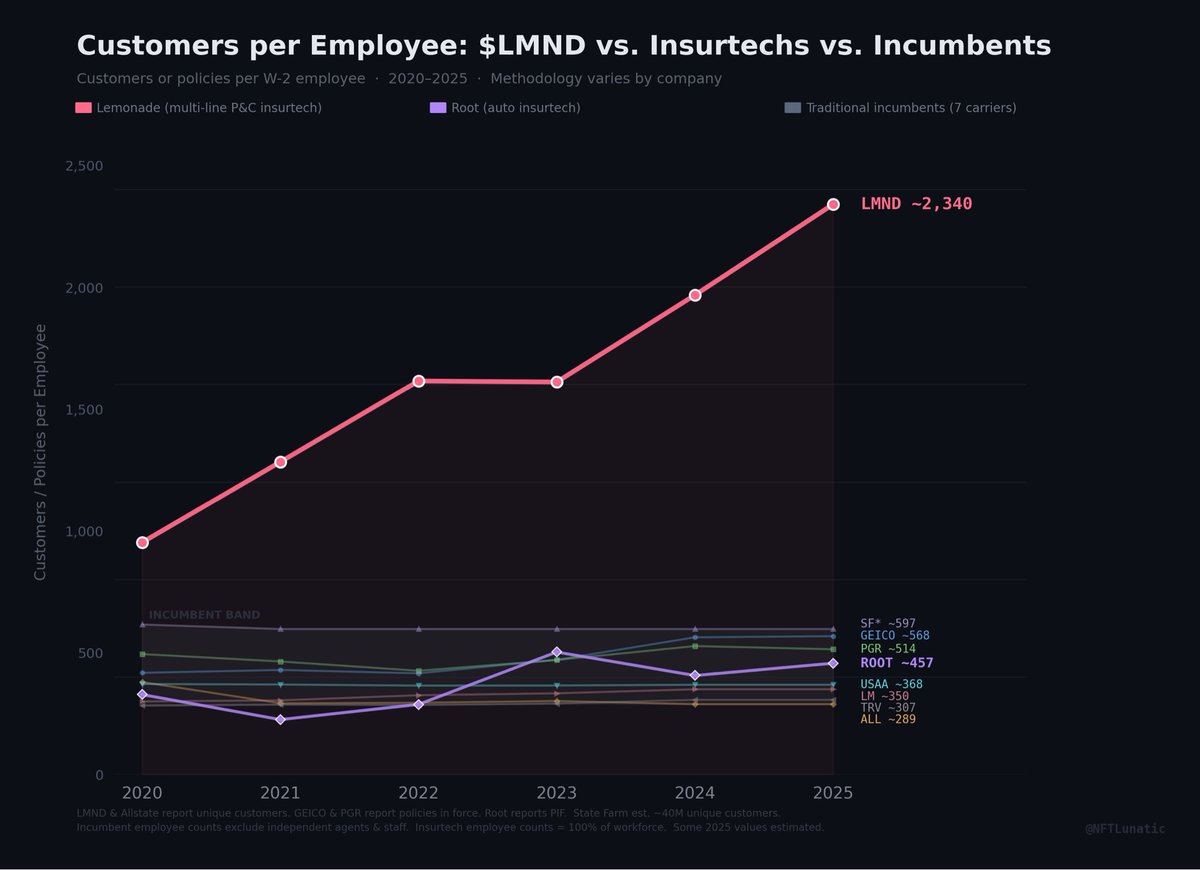

"Isn't $LMND just another insurtech?"

This chart can lay that argument to rest.

Customers per employee, 2020–2025:

$LMND vs. $ROOT vs. 7 major incumbents.

$ROOT is the perfect test case. Same era. Same "insurtech" label. Same direct-to-consumer P&C model. Public company with clean data.

$ROOT at 457 customers per employee.

GEICO at 568.

Progressive at 514.

Root IS the incumbent band.

Why? $ROOT innovation was telematics — better pricing through driving data. That helped them reach profitability. But it didn't change how many humans they need to operate.

Root hired 341 people last year to add 73K policies. $LMND hired 47 to add 570K.

That's not a difference of degree. It's a difference of kind.

$LMND didn't just digitize the front end. AI Maya underwrites. AI Jim handles claims. The marginal customer costs almost nothing to serve.

$ROOT used tech to price better. $LMND used AI to run the company.

That's why one curve compounds and the other flatlines.

This also kills the bear argument that competitors will "just copy $LMND playbook."

$ROOT has been trying for 9 years. Backed by $1.2B in funding. Public since 2020. Building technology from scratch with no legacy constraints.

And they still ended up in the incumbent band.

If a well-funded, tech-native insurtech with zero legacy baggage can't replicate this efficiency curve, what makes anyone think State Farm or Allstate will?

$LMND AI-first architecture isn't a feature. It's a compound advantage that gets harder to replicate every quarter — because every new customer, claim, and interaction feeds the models that make the next one cheaper to serve.

The moat isn’t JUST the AI operating system running the company. It’s 3 million customers (and growing) training the AI.

17

26

160

66,754

$SPCX lockups are going to wreck retail.

Shout out to @PronkDaniel for bringing this to my attention.

1

228

$RBLX

This is one that I’m always feeling FOMO for but am finding complicated to research.

1

4

471

$ADBE $NOW $CRM $PATH $GTLB $DUOL

Software is still largely pricing in an uncertain or bad future.

While semiconductor are pricing in very bullish outcomes.

While I think $NVDA and $AMD still look relatively attractive given their dominant positioning, people are largely momentum trading the smaller names.

We’ve seen semiconductor cycles before and the most dangerous thing to say in the market is “this time is different”.

Software is on the other side of that spectrum and is looking quite cheap.

1

3

699

Eric Bryant | Multibagger Research retweeted

Jun 14

19

17

252

21,812

Eric Bryant | Multibagger Research retweeted

Jun 13

Unstoppable, uncensorable, global decentralized AI seems like a good investment bet to make. The “Bitcoin of AI” so to say…

346

502

2,300

338,427

$TEM is finally looking pretty cheap.

I’m surprised given much of biotech is already running.

1

18

1,375

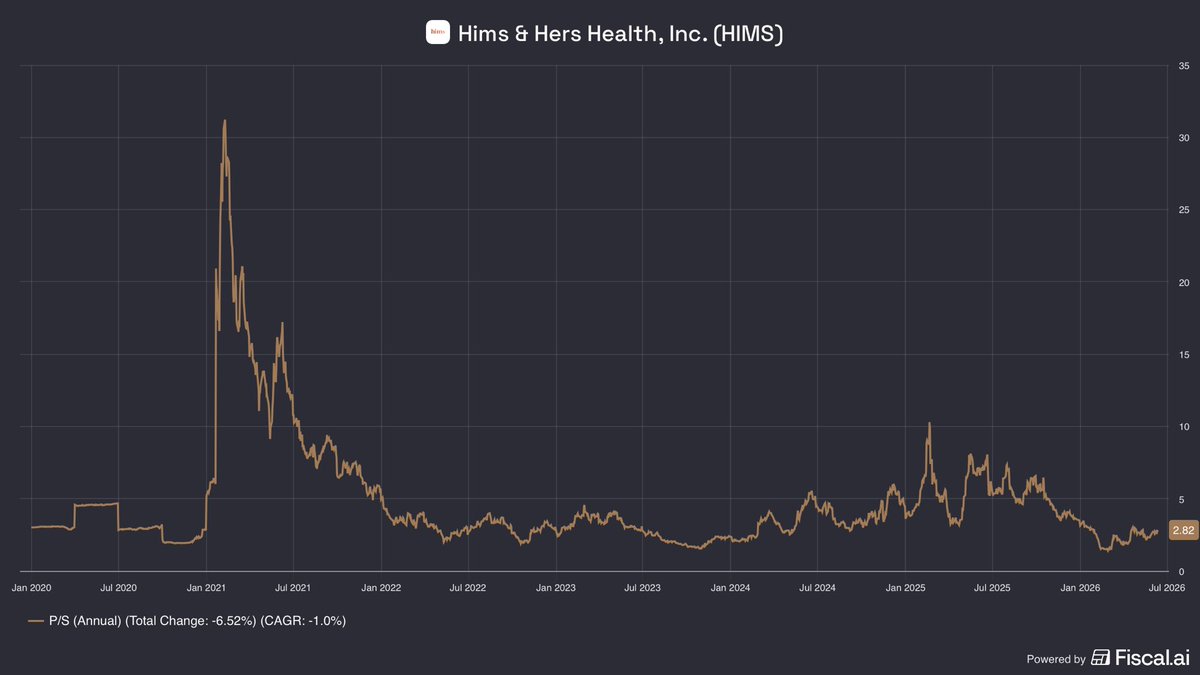

$HIMS will look absurdly cheap at these prices once revenue reaccelerates.

Currently at a P/S below 3.

4

2

101

4,215

Eric Bryant | Multibagger Research retweeted

I think we’re due for a biotech bull run soon.

But if you want downside protection while you wait, look for companies near a profitability inflection point.

Two I love right now: $TEM and $TWST.

Both are approaching profitability. Both have powerful AI tailwinds. But they win in very different ways.

$TEM has a self-reinforcing data moat. More customers generate more data, which makes their platform more valuable, which attracts more customers. This flywheel only accelerates as AI advances. And they’re increasingly embedded into the foundation of the healthcare system — making them very hard to rip out.

$TWST is the world leader in manufacturing synthetic biology at scale. As AI speeds up the rate at which researchers and drug developers can design and run experiments, demand for high-quality synthetic DNA skyrockets. $TWST is the pick-and-shovel play for the entire AI-bio revolution.

Both offer more downside protection than your typical biotech. Both have rapidly expanding TAMs. And both are approaching the point where revenue growth starts flowing to the bottom line.

That’s a rare combination.

2

2

18

2,781

WOW I am absolutely blown away by Fable 5 capabilities.

Great job to the team behind it! 👏

117

9

1,064

$KRKNF / $PNG.V catalyst setup:

Kraken’s C$615M Covelya acquisition is expected to close by the end of Q2, creating a ~1,200-person subsea robotics / maritime autonomy platform.

What changes post-close:

• Kraken standalone FY26 guide: C$165–175M revenue

• Covelya adds a much larger revenue base than Kraken has today

• 2026 order visibility: ~C$97M Kraken C$165M Covelya = ~C$262M

• Combined-company guidance expected at closing

• Defense, subsea infrastructure, mine warfare, autonomy, and ocean sensing all becoming more strategically important

The cleanest near-term catalyst is not just the deal closing — it is management showing what the new pro forma revenue EBITDA profile actually looks like.

This is turning from a niche Canadian subsea robotics company into a scaled maritime technology platform. Still small enough to be inefficiently priced, but now large enough to matter.

1

16

1,332