Developing high-grade lithium brine projects in Argentina | TSXV: NOAL

Joined December 2022

- Tweets 264

- Following 56

- Followers 433

- Likes 31

239 Photos and videos

🚨 𝐍𝐞𝐰𝐬 𝐀𝐥𝐞𝐫𝐭: NOA Lithium is proud to announce that Hatch Ltd. and the company have agreed to make a strategic arrangement in connection with the Company’s recently announced Pre-PFS Process Development Study for NOA's flagship Rio Grande project.

The Study is intended to compare the project's baseline evaporation pond flowsheet with alternative process configurations that incorporate direct lithium extraction (DLE) testwork and concept-level process design.

Read press release: tinyurl.com/ndf66c9e

#Lithium #EV #NOAL #BatteryMetals

3

31

⚡ 𝐖𝐞'𝐫𝐞 𝐠𝐨𝐢𝐧𝐠 𝐋𝐈𝐕𝐄!

Join us Wednesday, June 17, at 11:00 AM ET for a live webinar with @AmvestCap and @RKEquityRocks. We'll discuss NOA's lithium brine assets in Argentina's Lithium Triangle 🇦🇷, our development plans, and upcoming catalysts, followed by investor Q&A.

Register 👇

amvestcapital.com/webinar-di…

$NOAL #Lithium #EV #NOAL #BatteryMetals

4

45

🚨 𝐍𝐞𝐰𝐬 𝐀𝐥𝐞𝐫𝐭: NOA Lithium is pleased to provide an update on its 2026 exploration drilling program at its flagship Rio Grande Project in Salta Province, Argentina.

The company reports that both drilling rigs are operating in accordance with the current drilling program, which is designed to support evaluation of deep brine-bearing aquifers and ongoing refinement of the project’s hydrogeological and resource models.

Read press release: tinyurl.com/yc3zumfp

#Lithium #EV #NOAL #BatteryMetals

4

35

🚨 𝐍𝐞𝐰𝐬 𝐀𝐥𝐞𝐫𝐭: NOA Lithium has completed mobilization of two drilling rigs for NOA’s 2026 exploration drilling campaign at its flagship Rio Grande Project in Salta Province, Argentina. Site preparation activities, including the construction of well pads, have been completed, and drilling is expected to commence early next week. These activities form part of NOA’s work program as it advances toward completion of a Preliminary Feasibility Study.

Read press release: tinyurl.com/frw3kday

#Lithium #EV #NOAL #BatteryMetals

6

105

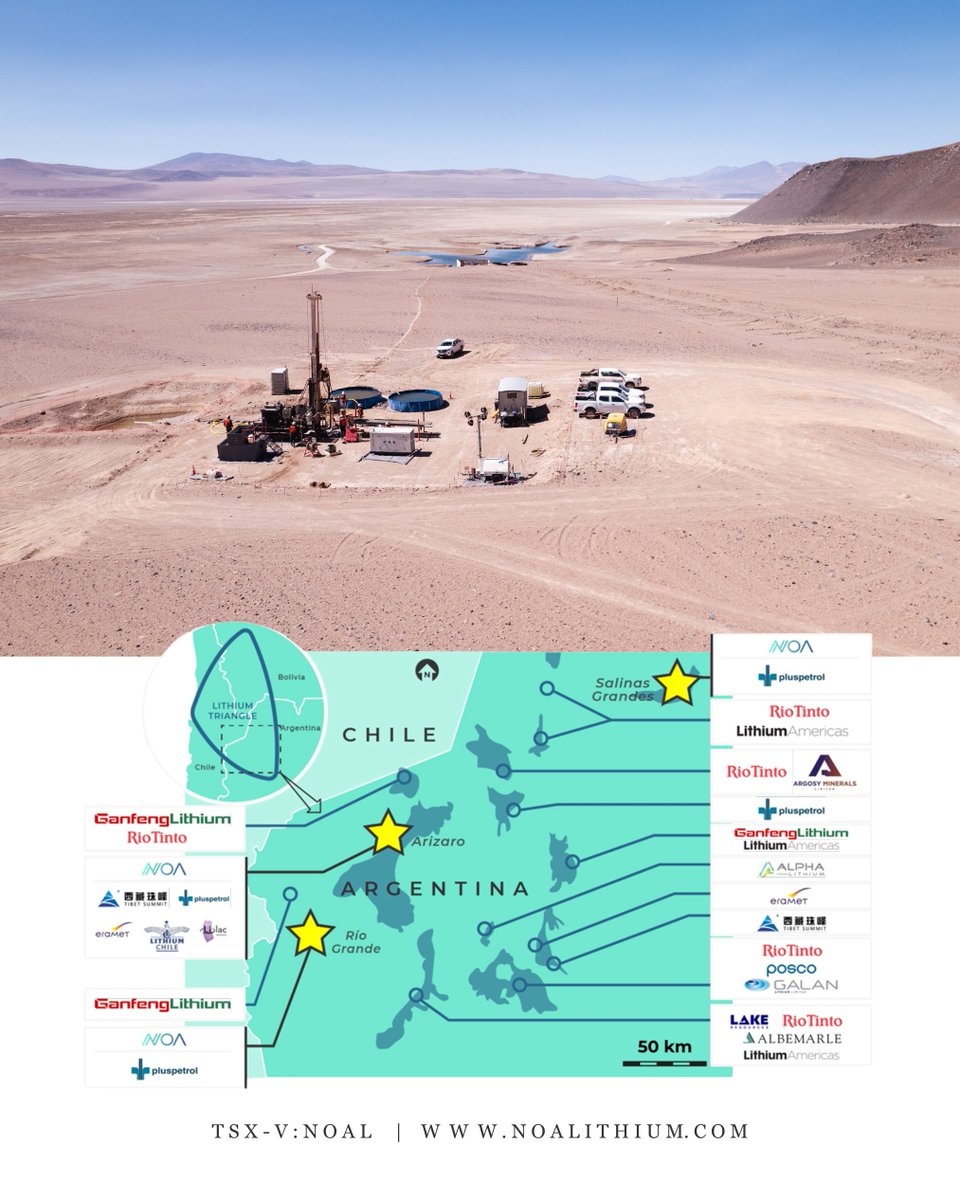

Gabriel Rubacha, CEO of NOA Lithium, joined @RKEquityRocks to break down the Rio Grande project, highlighting development flexibility, product optionality and the broader opportunity across Argentina’s lithium brine sector. The discussion also touches on the path to PFS and the potential upside across Arizaro and Salinas Grandes.

𝐖𝐚𝐭𝐜𝐡 𝐟𝐮𝐥𝐥 𝐢𝐧𝐭𝐞𝐫𝐯𝐢𝐞𝐰: tinyurl.com/4sdjm6wd

#Lithium #EV #NOAL #BatteryMetals #CriticalMetals

𝘍𝘰𝘳 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯𝘢𝘭 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺.

3

11

1,138

NOA Lithium CEO Gabriel Rubacha joins @zac_hartley for a discussion on lithium market dynamics and the company’s strategic positioning.

In this interview, we explore expectations for the lithium market over the next 12 months, how NOA Lithium is navigating current market conditions, and key factors that differentiate the company within the broader lithium sector.

𝐖𝐚𝐭𝐜𝐡 𝐟𝐮𝐥𝐥 𝐢𝐧𝐭𝐞𝐫𝐯𝐢𝐞𝐰: tinyurl.com/4xbwapnx

#Lithium #EV #NOAL #BatteryMetals #CriticalMetals

𝘍𝘰𝘳 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯𝘢𝘭 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺.

5

108

NOA Lithium CEO Gabriel Rubacha joined Kai Hoffmann of @GoldNewsletter, a leading platform for global mining news, to share a corporate update on lithium market trends, supply-demand dynamics, and NOA’s flagship Rio Grande Project in Argentina.

𝐖𝐚𝐭𝐜𝐡 𝐟𝐮𝐥𝐥 𝐢𝐧𝐭𝐞𝐫𝐯𝐢𝐞𝐰: tinyurl.com/49az2hdj

#Lithium #EV #NOAL #BatteryMetals

11

291

NOA Lithium Brines Inc. (TSXV: NOAL) retweeted

May 12

Argentina brines continue to look materially undervalued versus recent transaction benchmarks.

But with $NOAL.V up 30% (1W), might a re-rating be underway?

We discuss why @NOAlithium's Rio Grande may offer a better risk-reward setup than current valuation implies.

📺: youtu.be/1xaxLFVK9uE

Not Investment Advice. DYOR.

3

15

3,785

🚨 𝐍𝐞𝐰𝐬 𝐀𝐥𝐞𝐫𝐭: NOA Lithium is pleased to announce it has agreed to a strategic collaboration framework with Hidrotec S.A., one of Argentina’s leading and most experienced drilling contractors in the lithium brine sector. Under the collaboration, NOA expects to benefit from enhanced access to top quality drilling experience and equipment, with operational support for its planned work programs in Argentina.

Read press release: tinyurl.com/3cm3a8a5

#Lithium #EV #NOAL #BatteryMetals

6

71

🚨 𝐍𝐞𝐰𝐬 𝐀𝐥𝐞𝐫𝐭: NOA Lithium is pleased to announce the appointment of Hatch Limited to lead the Process Development Study for our flagship Rio Grande Project in Salta Province, Argentina. The objective of the Study is to compare the Project's baseline evaporation pond flowsheet against alternative process configurations incorporating direct lithium extraction (DLE) technology.

Read press release: tinyurl.com/bp5jvd69

#Lithium #EV #NOAL #BatteryMetals

8

107

NOA Lithium Brines Inc. (TSXV: NOAL) retweeted

May 1

👇👇 $NOAL. Not advice. DYOR

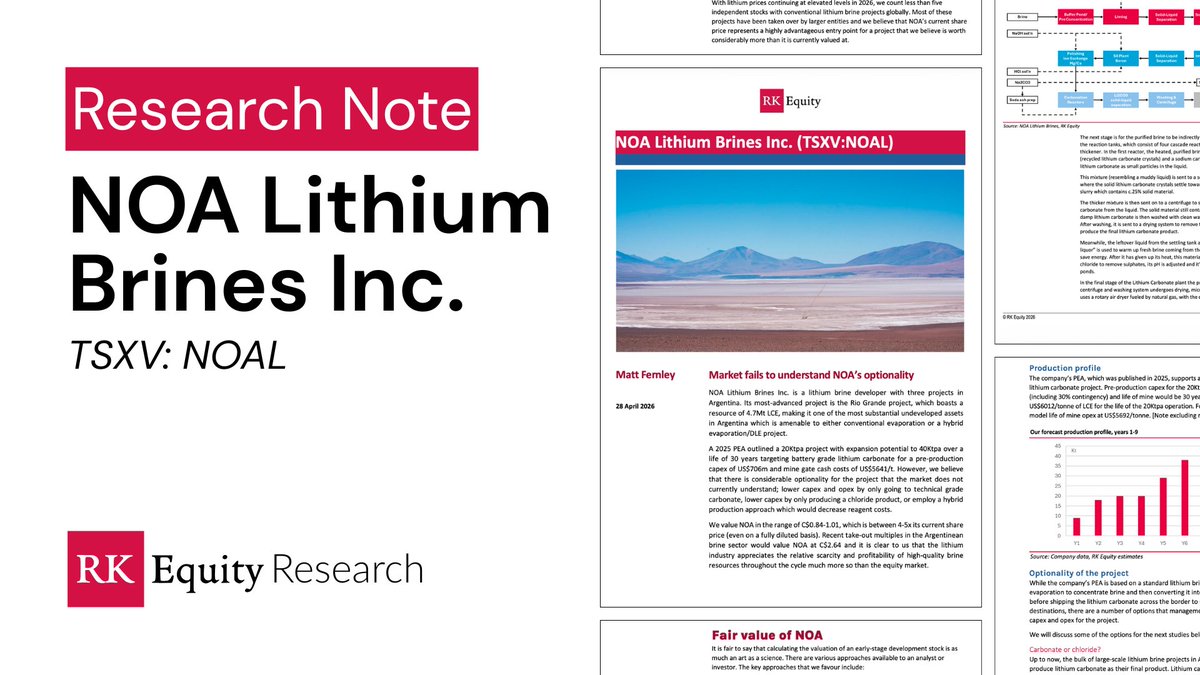

Check out our latest research report on @NOAlithium entitled “Market Fails to Understand NOA’s Optionality”

Our thesis:

•Robust PEA: 20Ktpa lithium carbonate project with potential to expand to 40Ktpa over 30 years life for capex of US$706m and mine gate cash costs of US$5641/t.

•Unrecognized Optionality: Multiple paths to value: technical-grade carbonate, chloride, or hybrid DLE.

•Strategic Scarcity: Argentinian brines are at the bottom of the cost curve and are highly sought after by industry players.

•Valuation Gap: NOA trades at c.$10/t LCE. Recent M&A in the sector was at multiples closer to $50–100/t.

Bottom Line: $NOAL.v is a relatively new entrant in the market which boasts a strong management team, good investor support and a good asset base with plenty of optionality to benefit from higher lithium prices.

Read the full research report here: link.rkequity.com/noal-repor…

3

10

3,167

🚨 𝐍𝐞𝐰𝐬 𝐀𝐥𝐞𝐫𝐭: NOA Lithium is pleased to announce that Matt Fernley from @RKEquityRocks has initiated research coverage on the company. RK Equity has published an initial report, which can be accessed with the following link: link.rkequity.com/noal-repor…

Read press release: tinyurl.com/rh5ru97u

#Lithium #EV #NOAL #BatteryMetals

1

1

16

2,195

𝐀 𝐝𝐞𝐞𝐩𝐞𝐫 𝐝𝐢𝐯𝐞 𝐢𝐧𝐭𝐨 𝐨𝐧𝐞 𝐨𝐟 𝐀𝐫𝐠𝐞𝐧𝐭𝐢𝐧𝐚’𝐬 𝐞𝐦𝐞𝐫𝐠𝐢𝐧𝐠 𝐥𝐢𝐭𝐡𝐢𝐮𝐦 𝐬𝐭𝐨𝐫𝐢𝐞𝐬.

In this conversation with @McnallieM, Gabriel Rubacha, CEO of NOA Lithium, shares his perspective on our company’s growing position in the Lithium Triangle and the fundamentals behind our flagship Rio Grande Project.

Watch the full interview: tinyurl.com/3vv4kkvw

#Lithium #EV #NOAL #BatteryMaterials

1

9

617

𝐈𝐧 𝐜𝐚𝐬𝐞 𝐲𝐨𝐮 𝐦𝐢𝐬𝐬𝐞𝐝 𝐢𝐭 | Our April update is out!

Check out our latest monthly newsletter, where we share recent milestones, highlights from investor and industry engagements, and what’s ahead as we advance our portfolio in one of the world’s most prolific lithium regions.

Read more: tinyurl.com/fwce5ztn

$NOAL #Lithium #CriticalMinerals #Mining #LithiumStocks #TSXV #NOALithium #EV #Argentina

7

87

🚨 𝐍𝐞𝐰𝐬 𝐀𝐥𝐞𝐫𝐭: NOA Lithium is pleased to announce that our drilling contractor has commenced mobilization to the site for our upcoming 2026 exploration drilling campaign at our flagship Rio Grande Project in Salta Province, Argentina. These drilling activities are part of the plan to complete a Preliminary Feasibility Study by year-end 2026.

Read more: tinyurl.com/ykxaxkb6

#Lithium #EV #NOAL #BatteryMetals

6

129

𝐄𝐱𝐩𝐥𝐨𝐫𝐢𝐧𝐠 𝐭𝐡𝐞 𝐟𝐮𝐭𝐮𝐫𝐞 𝐨𝐟 𝐥𝐢𝐭𝐡𝐢𝐮𝐦 𝐬𝐭𝐚𝐫𝐭𝐬 𝐰𝐢𝐭𝐡 𝐭𝐡𝐞 𝐫𝐢𝐠𝐡𝐭 𝐚𝐬𝐬𝐞𝐭𝐬 𝐚𝐧𝐝 𝐬𝐭𝐫𝐚𝐭𝐞𝐠𝐲.

NOA Lithium is advancing a portfolio of lithium brine projects in Argentina’s Lithium Triangle, anchored by its Rio Grande Project, as it moves toward a 2026 Pre-Feasibility Study. Most recently, Red Cloud Securities Inc. initiated research coverage on the company.

Learn more and connect with the story: noalithium.com

$NOAL #Lithium #CriticalMinerals #Mining #LithiumStocks #TSXV #NOALithium #EV #Argentina

Forward-looking statements apply.

6

82

🎥 Watch our Executive Chairman, Hernan Zaballa, as he shares insights on Argentina’s mining and permitting framework, the importance of hydrogeology and community engagement in lithium brines, and how NOA is approaching project development with a long-term, disciplined strategy.

Watch full interview: youtu.be/BZX2gI7m9ig

🔗 Learn more: noalithium.com/

#Lithium #CriticalMinerals #Mining #LithiumStocks #TSXV #NOALithium #EV #Argentina

7

154

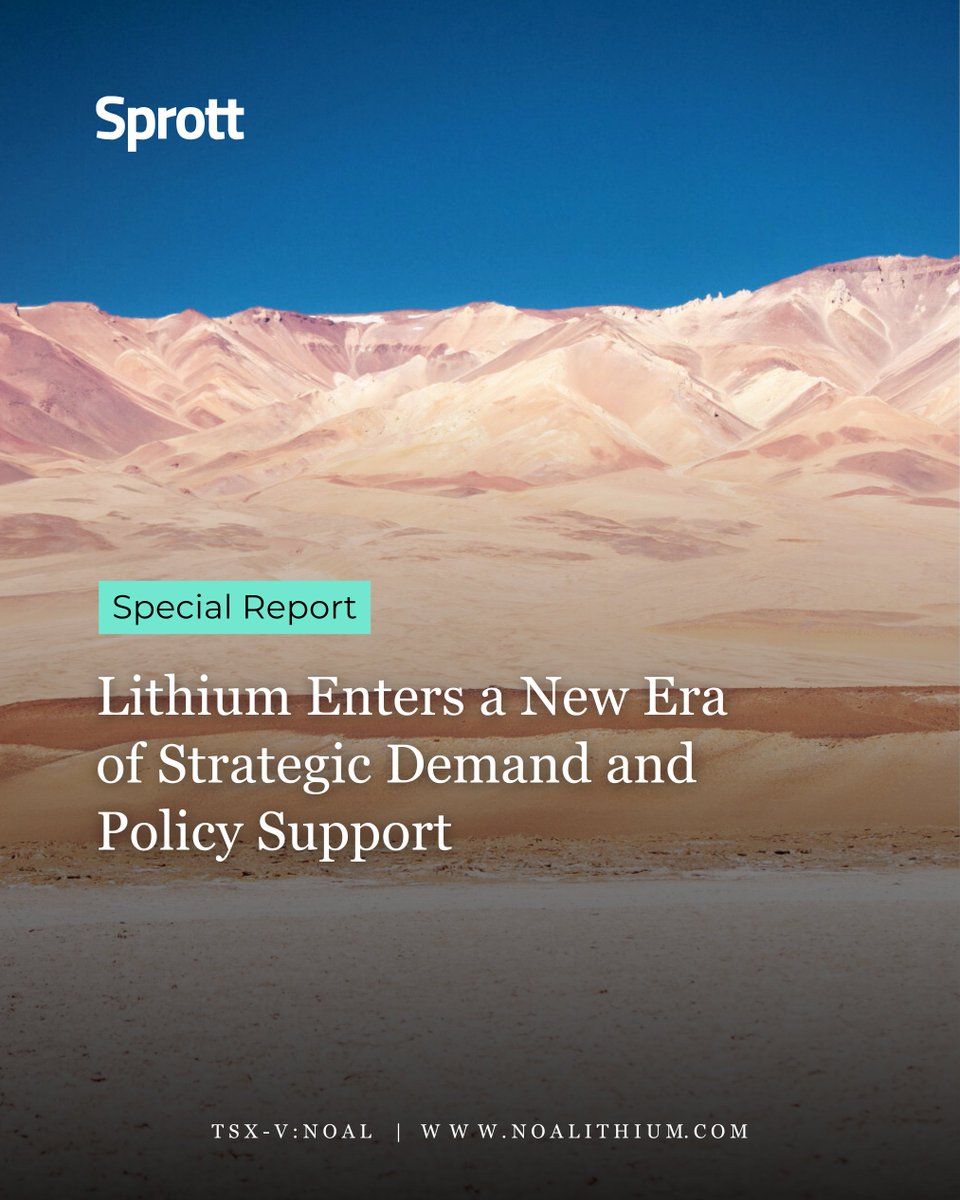

A new report from @sprott explores the 𝐬𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐢𝐦𝐩𝐨𝐫𝐭𝐚𝐧𝐜𝐞 𝐨𝐟 𝐥𝐢𝐭𝐡𝐢𝐮𝐦 as demand from EVs, energy storage, and critical mineral supply chains continues to evolve. It also highlights Argentina's 𝐠𝐫𝐨𝐰𝐢𝐧𝐠 𝐫𝐨𝐥𝐞 𝐢𝐧 𝐠𝐥𝐨𝐛𝐚𝐥 𝐥𝐢𝐭𝐡𝐢𝐮𝐦 𝐬𝐮𝐩𝐩𝐥𝐲, including the strengthening relationship with the U.S. on critical minerals.

An important backdrop for companies advancing projects in 𝐀𝐫𝐠𝐞𝐧𝐭𝐢𝐧𝐚’𝐬 𝐋𝐢𝐭𝐡𝐢𝐮𝐦 𝐓𝐫𝐢𝐚𝐧𝐠𝐥𝐞, like NOA Lithium.

Read the insight → tinyurl.com/3a43t8my

#Lithium #EV #NOAL #CriticalMinerals

𝘐𝘯𝘥𝘶𝘴𝘵𝘳𝘺 𝘤𝘰𝘮𝘮𝘦𝘯𝘵𝘢𝘳𝘺; 𝘯𝘰𝘵 𝘢𝘯 𝘰𝘧𝘧𝘦𝘳 𝘵𝘰 𝘣𝘶𝘺 𝘰𝘳 𝘴𝘦𝘭𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

6

207

🎥 During PDAC 2026 in Toronto, NOA Lithium CEO Gabriel Rubacha joined @RKEquityRocks for a conversation on our company’s progress and what lies ahead. The discussion highlights key developments across NOA’s lithium brine portfolio in Argentina and upcoming milestones.

▶️ 𝐖𝐚𝐭𝐜𝐡 𝐭𝐡𝐞 𝐟𝐮𝐥𝐥 𝐢𝐧𝐭𝐞𝐫𝐯𝐢𝐞𝐰: tinyurl.com/3c6a223x

🔎 𝐋𝐞𝐚𝐫𝐧 𝐦𝐨𝐫𝐞 𝐚𝐛𝐨𝐮𝐭 𝐍𝐎𝐀 𝐋𝐢𝐭𝐡𝐢𝐮𝐦: noalithium.com/

#Lithium #EV #NOAL #BatteryMaterials

1

1

7

1,401