Small business tools that solves big needs.

Joined October 2022

- Tweets 2,111

- Following 67

- Followers 4,926

- Likes 302

88 Photos and videos

NameRiffle retweeted

5 Jun 2025

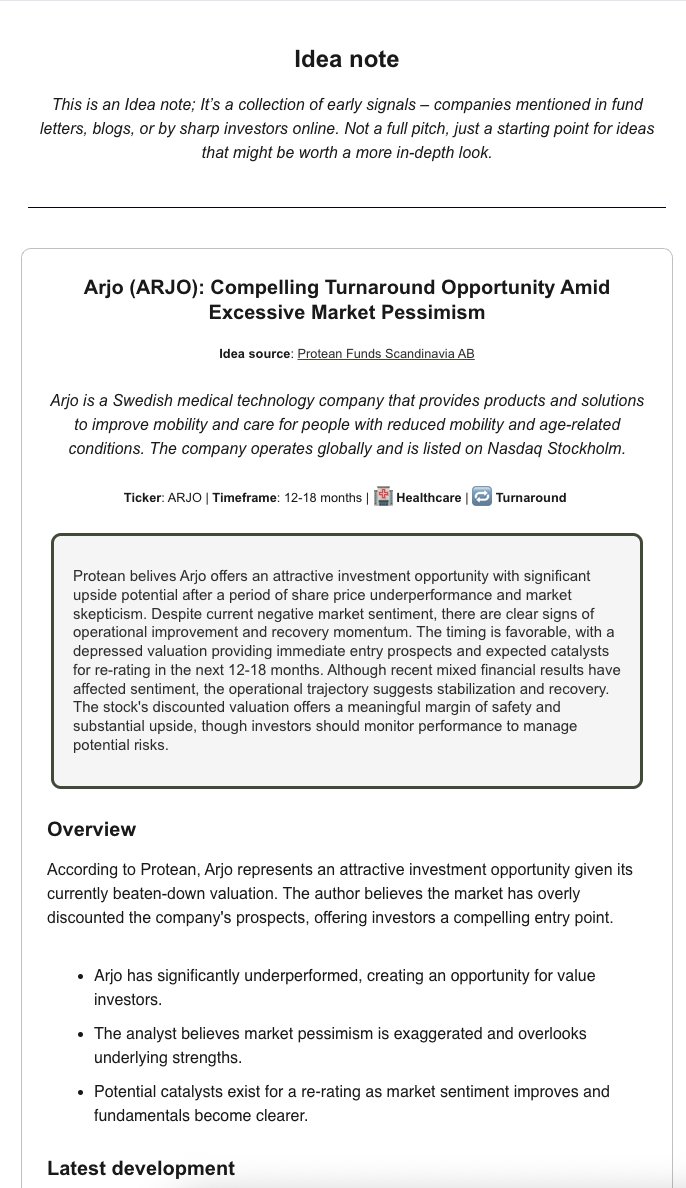

Månadsrapporter från duktiga fonder kan vara en bra källa för att hitta intressanta case, men används för lite tycker jag.

Tänkte lösa det med något jag kallar Idea notes.

Se $ARJO från @stckpkr och Protean som första exempel: lindresearch.com/p/arjo-arjo…

Är detta ett intressant format?

1

1

5

1,668

21 Feb 2025

Read it!

21 Feb 2025

I sent out an update on following their Q4 report. Sadly, so far, our caution has been proved correct, and 2025 does not seem to be any different.

See link here: lindresearch.com/p/betco-sof…

Key takeaways:

➡️ As the results in BETCO’s Q4 ’24 report were already known, the most important new information related to the guidance for 2025 and beyond. Overall, management expects a flat development during the year, burdened by the Brazilian market.

➡️ We also believe that Media Partnerships are a key driver. Still, management finds that the issue is deliberately omitted from their communications, as there are still active partnerships that are not compliant with Google policy.

➡️ On the brighter side, BETCO expects to have excellent cost control, strengthen cash conversion, and focus more on paying down debt than on new M&A.

➡️ As stated only six months ago, the guided revenue for 2025 is about 20% below what the company expected to earn in 2024. This shows the inherent issue with a business susceptible to Google updates and new iGaming regulations.

➡️ We still see a significant downside risk from today’s share price levels. Given that 2025 is expected to be very rocky for the company, we expect the same for the share price. Therefore, we have adjusted our price target down further.

1

154

NameRiffle retweeted

14 Feb 2025

I just published a comment on $BETCO; see the link in the first comment. (Did this thread previously in Swedish)

Downside Risk, Stay Cautious

- BETCO announced a reversed profit warning on February 6th, causing the share price to soar. However, we question whether the “Partner Publishing” issue is truly resolved.

- We believe it is likely that “Partners” still exist, representing a significant portion of Publishing revenue; to keep them “hidden,” non-compliant tactics in violation of Google’s spam policy are utilized.

- We estimate that around 20% of Publishing EBITDA for 2025 will be tied to Partners and should be valued close to zero.

- Using fairly lofty consensus EBITDA estimates for 2025, our SOTP valuation suggests a price of 86 SEK per share, approximately 25% lower than BETCO's current trading price. We urge caution, as the risks presently outweigh the potential, at least in our opinion.

1

1

5

1,667

NameRiffle retweeted

30 Jan 2025

$EMBRAC stock continues to show strength, at least during the last 12 months.

With the spin-off of Asmodee coming it's an interesting time ahead.

However, what really matters is game releases, and #KCD2 will be one of the biggest during the year for the Group.

I have looked into the available data for Google search interests, Steam followers, budgets, and more, compared it to the first game in the series, #KCD1, and created a report.

See some of the slides below, and follow the link in the first comment to access the full report.

1

1

20

3,363

5 Jul 2024

#Meta plans to boost its #Metaverse platform! Integrating generative #AI tech into VR, AR, and mixed reality games should offer new experiences and improve workflows. Will this pivot help overcome their user attraction challenges?🧐 Find out more at frontresearch.com/p/meta-gea…

#TechNews

161

5 Jul 2024

Amazon is partnering with Australia to establish a $1.3Bn high-security cloud data system, boosting the defense sector and creating 2,000 jobs! 🌐💼#CloudComputing #JobCreation Interested in learning more? Visit ➡️ frontresearch.com/p/amazon-p…

122

5 Jul 2024

EU regulators serve #ElonMusk's X with a formal warning over alleged mishandling of dangerous content. The tech giant could face penalties of 6% of revenue if changes aren't made. This comes amid the EU's strengthened enforcement of #DSA and #DMA. More at👉 frontresearch.com/p/eu-hands…

#RegTech

91

5 Jul 2024

#Meta unleashes groundbreaking multi-token AI models, aiming to streamline #LLMs. Enhancing performance while reducing training time, it's a step towards making #AI more accessible & sustainable.🚀 But, it's not without challenges. How will we prevent misuse?🔒 Dive in to learn more at frontresearch.com/p/meta-unv… #AIFuture

2

77

2 Jul 2024

Robinhood amps up its #AI game by acquiring Pluto Capital. The move brings real-time portfolio optimization and personalized #investment strategies to your fingertips. Sansbury, Pluto's founder, to fuel AI adoption at Robinhood. Dive deeper at [frontresearch.com/p/robinhoo… #fintech #technews

105

2 Jul 2024

Savvy play by #BigTech! Amazon and Microsoft reel in AI startups by hiring their teams and licensing tech, avoiding antitrust watch. The chase is on for the next big AI breakthrough. #AI #innovation. Learn more about this new tactic 👉 frontresearch.com/p/eu-tight…

5

113

2 Jul 2024

In a volatile market, bootstrapped #SaaS companies show resilience and adaptability, while VC-backed firms outpace in growth, according to ChartMogul. With new biz on the decline, both leverage expansion for growth. #TechInvestments. Read more: frontresearch.com/p/chartmog…

91

24 Jun 2024

Google is testing a direct product comparison feature in search results, even for broad terms such as "best credit cards."

frontresearch.com/p/google-s…

1

79

22 Feb 2024

NVIDIA beats expectations, and the market breathes a sigh of relief.

I've extracted the most interesting information from their earnings call:

"Gross margin is expected to decrease from Q2 onwards."

"40% of Data Center revenue comes from AI Inference."

#Nvidia $NVDA

Check it out at: frontresearch.com/p/nvidia-q…

1

258

21 Feb 2024

A new stock idea on Shopify $SHOP is featured in today's newsletter!

Despite a post-earnings dip, its unmatched eCommerce strength, innovative drive, and strategic expansions shine bright.

#Investing #Shopify

frontresearch.com/p/shopify-…

182

25 Dec 2023

The Guide to Competitor Intelligence and Research from @patticus has been insanely valuable.

You can find it here: patticus.com/2023/12/16/comp…

201

18 Dec 2023

Business Edge update 18/12-23

• Apple Pay Lawsuit - Antitrust allegations against Apple, Visa, and Mastercard.

• App Store Overhaul - Apple redefines pricing models.

• Google AI Studio - Streamlined app and chatbot development.

• Self-Developing AI - AI models autonomously create smaller versions.

• ByteDance AI Controversy - OpenAI terms were breached in a secret AI project.

• Microsoft's Phi-2 AI - A new compact AI revolutionizes the market.

• 2024 AI Market Outlook - Anticipating AI-driven economic recovery.

(1/10)

#TechNews

2

1

283

18 Dec 2023

If you like this thread of tech news...

1) Follow @Businessedge_co

for more daily updates

2) Subscribe to our free email newsletter: businessedge.co/subscribe

96

18 Dec 2023

2024 Market Outlook: Potential Rolling Recoveries and AI Adoption on the Rise (7-minute read)

(9/10)

schwab.com/learn/story/outlo…

1

75

18 Dec 2023

Stunning 7-Week Rally Bolsters Tech Markets Amid Fed's Projected Rate Cuts (12-minute read)

(10/10)

schwab.com/learn/story/stock…

61