Joined March 2014

- Tweets 1,929

- Following 96

- Followers 1,759

- Likes 594

441 Photos and videos

Pinned Tweet

Mar 30

Reason to buy in Dip: India’s growth is inevitable.

8

2,423

BHEL

Any stock which makes a move after 3-5-8-10-15 years of Consolidation doesn't just stop being a doubler or a tripler,it roars much more.

Name companies which are breaking out after a very long time.

1

271

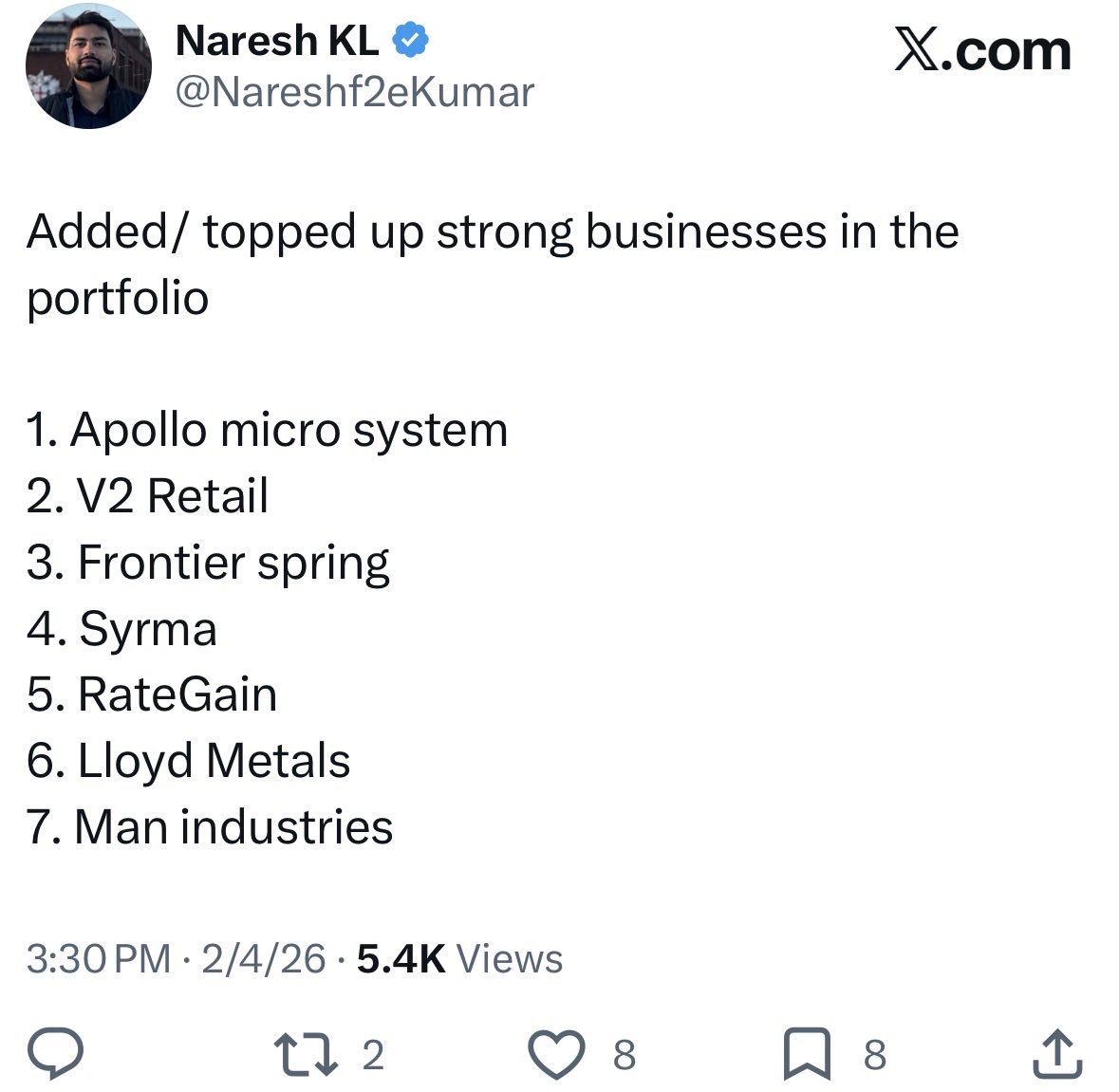

Topped up

1. Amanta Healthcare

2. Rategain

Enjoying my time reading Unihealth Hospitals concall. Definitely recommend reading.

DYOR!!

10

891

Ek time tha jab aise order news pe stock double ho jata tha.

3

43

5,190

Jun 15

Minor Topup and trimming

1) Apollo Micro - Trim

2) Frontier Spring - Trim

3) Viviana - Top up

4) Rate gain - Top up

1

13

2,022

Jun 14

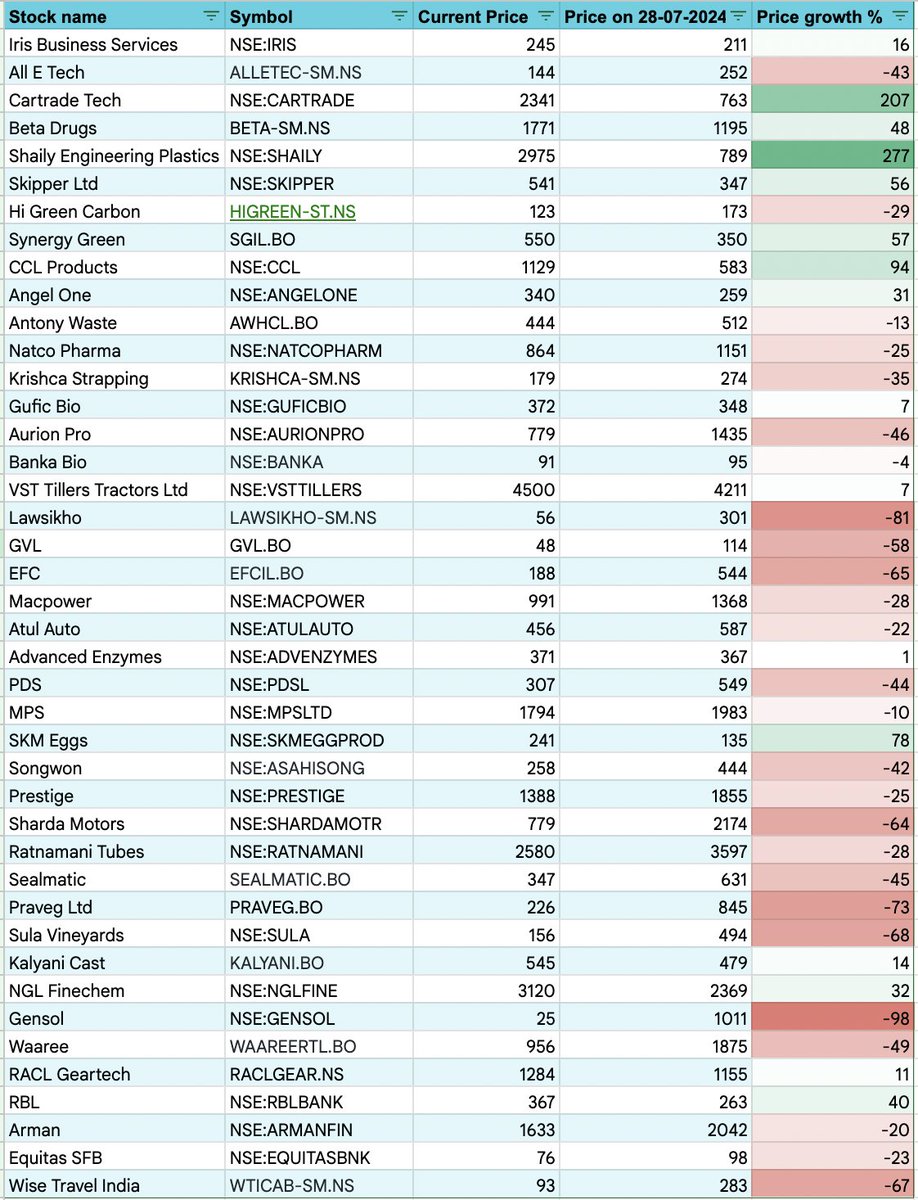

Revisiting my "Best Promoters" portfolio after 1.5 years 📈

Back in Dec '24, I shared a list of companies known for strong management/promoters.

June '26 Update:

🏆 Clear Winners

#Shaily #CarTrade #CCL

✅ Held Up Well

#BetaDrugs #Skipper

🔄 Nice Turnarounds

#SKMEgg #RBL

📉 Most others have given up their earlier gains and are now in the red.

Big Lesson:

Great management is important, but it's not enough.

Only a handful become multibaggers because execution, industry tailwinds, and valuation discipline matter just as much.

Management quality is a filter, not a guarantee.

Who would you add to the "Best Management" list today?

Drop your names below 👇

Let's track them together over the next year!

#StockMarket #Investing #Promoters #LongTermInvesting

11 Dec 2024

On June 27, 2024, I came across an insightful post discussing the best promoters in the industry with people sharing their perspectives.

I compiled data to analyze the current performance of companies led by these highly regarded promoters.

While it’s been just over five months since the post, I understand this isn’t a long enough period to draw firm conclusions. I plan to revisit this fun analysis next year to gain a deeper perspective."

Best performers:

#Iris (Iris Business Services)

#AllETech (All E Tech)

#CarTrade (Car Trade Tech)

#BetaDrugs (Beta Drugs)

#Shaily (Shaily Engineering Plastics)

@DEBU_NEOGI Thank you for the interesting post.

BhulChukMaaf

1

4

1,787

Jun 13

You know investing has become an obsession when you walk into an IKEA store and instantly start wondering which listed companies are part of its supply chain. 😅

1

429

Jun 12

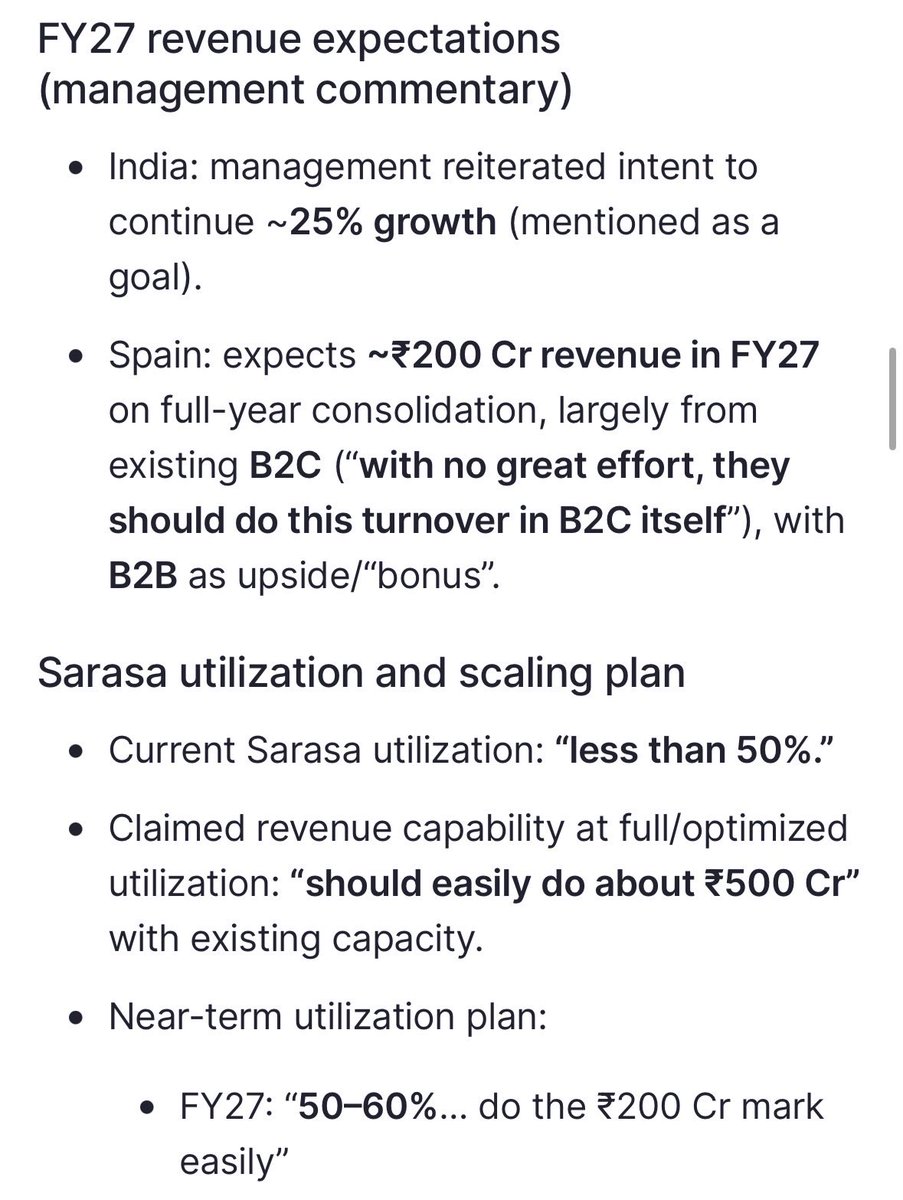

💊 Innova Captab: A pharma company where future earnings may look very different from current earnings.

Got the hint from @vandit_jain1994 post about this company.

✅ FY26 Revenue: ₹1,630 Cr ( 31%)

✅ CDMO Revenue: ₹1,133 Cr ( 24%)

✅ Branded Generics Revenue: ₹497 Cr ( 51%)

✅ 350 CDMO customers

✅ Presence in 60 countries

The key growth driver is the Jammu facility:

🏭 ₹480 Cr invested

📈 FY26 Revenue: ~₹300 Cr

📊 Q4 exit run-rate: ₹90 Cr/quarter

⚙️ Utilization only ~10%

💰 Near EBITDA breakeven

Management expects 20% revenue growth ahead and believes EBITDA growth should outpace revenue growth as Jammu scales.

🔹 Government incentives include GST-linked benefits and interest subvention, improving project economics.

🔹 Jammu contributed ~₹300 Cr revenue in FY26 despite being in the early stages of ramp-up.

🔹 Management expects EBITDA growth > Revenue growth and PAT growth > EBITDA growth as utilization rises.

Why? Because most fixed costs (employees, utilities, depreciation & finance cost) are already sitting in the P&L. Incremental revenue should drive operating leverage.

🔹 Ex-Jammu EBITDA margins are estimated at ~18%, suggesting the core business is stronger than reported numbers indicate.

Other positives:

🌍 Growing exports (~31% of FY26 revenue)

🧪 UK MHRA approval

🏥 Presence in regulated markets like UK, Europe, Canada & Australia

📈 New Baddi expansion under evaluation with potential ₹450-500 Cr revenue capacity

The market currently sees a 15.4% EBITDA margin business.

The real question is: What does Innova look like when a ₹480 Cr plant running at ~10% utilization starts moving towards optimal utilization?

#InnovaCaptab #Pharma #CDMO #MicrocapBreakdown #Investing

4

17

1,520

Jun 11

Freshara Agro

FY 26 revenue : 342 Cr

Next year 600 crore looks easy peasy.

Interesting thing to watch out will be the margins for Spain plant.

Disclosure : Invested.

DYOR!!

2

10

1,522

Jun 11

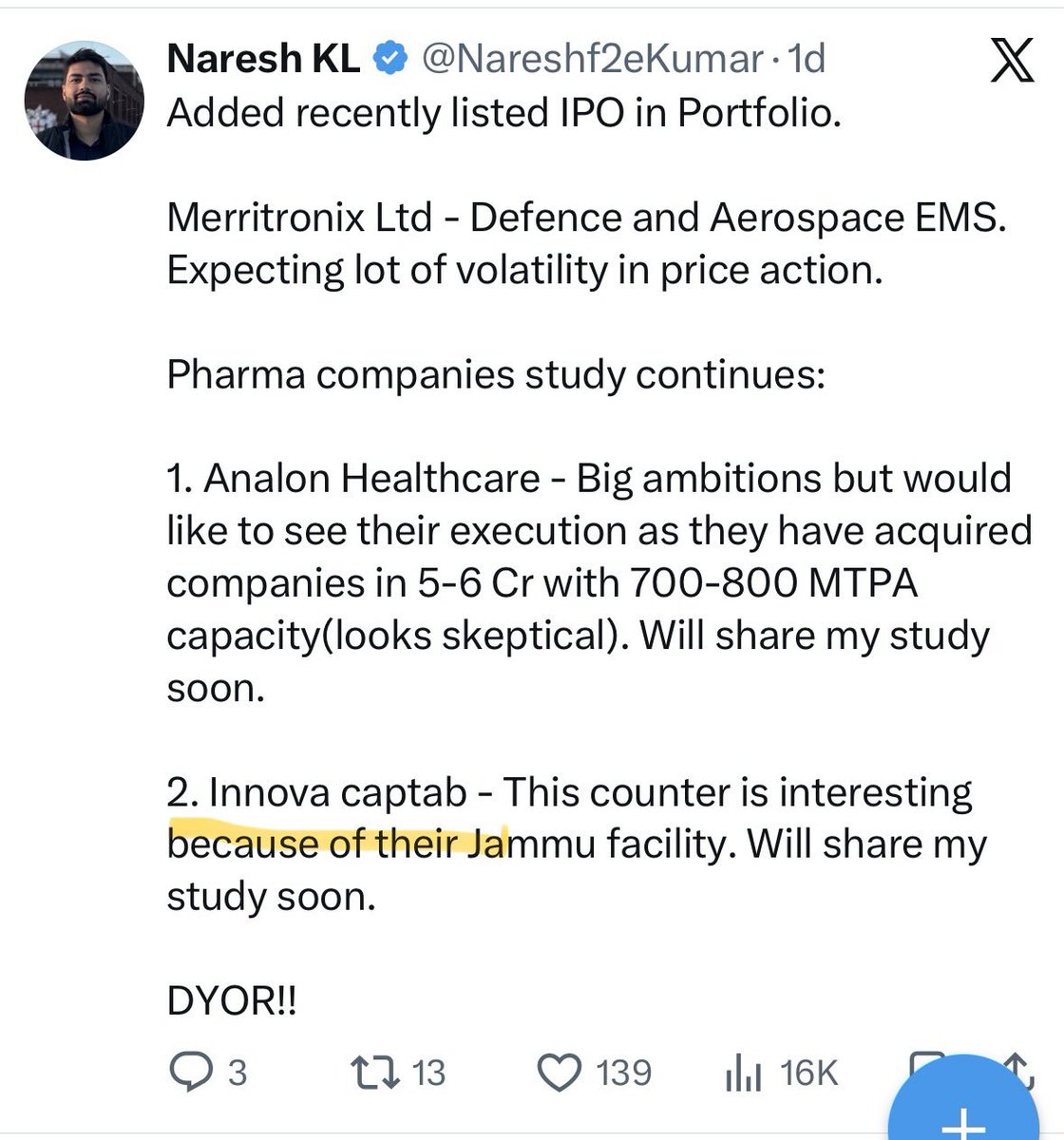

Added recently listed IPO in Portfolio.

Merritronix Ltd - Defence and Aerospace EMS. Expecting lot of volatility in price action.

Pharma companies study continues:

1. Analon Healthcare - Big ambitions but would like to see their execution as they have acquired companies in 5-6 Cr with 700-800 MTPA capacity(looks skeptical). Will share my study soon.

2. Innova captab - This counter is interesting because of their Jammu facility. Will share my study soon.

DYOR!!

3

12

139

16,398

Jun 10

Added first Pharma company in Portfolio.

Amanta healthcare

Other additions:

Inox India - Deep tech

Sky gold - Topping up

Viviana - Topping up

Buying in chunks

DYOR!!

5

19

248

22,918

Jun 11

My thesis on Amanta Healthcare

x.com/nareshf2ekumar/status/…

Jun 11

Why Amanta Healthcare?? My investment thesis

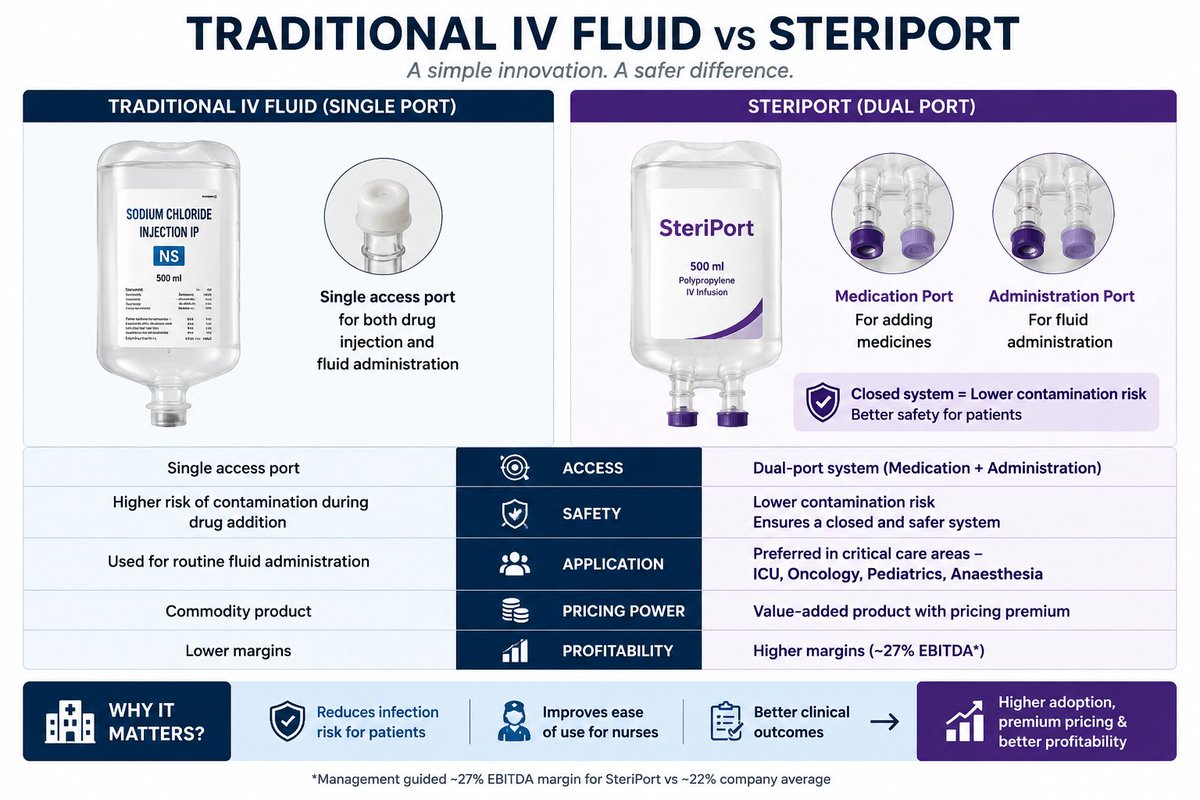

Amanta Healthcare is a sterile pharma company specializing in IV fluids, injectables, respiratory and ophthalmic products. Its key differentiator is SteriPort, a premium two-port IV bottle platform that contributes ~42% of revenue.

1️⃣ SteriPort is the real story

Amanta pioneered ISBM-based polypropylene IV bottles in India.

Today, SteriPort contributes ~42% of revenue and is preferred in oncology, ICU, pediatrics and critical care due to lower contamination risk.

Current utilization is at 96%; that itself means the product is in demand.

2️⃣ Capacity expansion is about to go live

SteriPort capacity is increasing from:

📈 6.6 Cr bottles ➝ 11.6 Cr bottles

Management expects commercial production to start by June 2026.

3️⃣ This single expansion can be transformative

Management expects:

💰 Additional revenue: ₹110-120 Cr annually

Production is starting in June; that means it will add 80-90 Cr in revenue.

Against FY26 revenue of ₹288 Cr, that's nearly 30% incremental revenue potential from one project alone.

4️⃣ Margins should improve

Current EBITDA Margin: 22%

New SteriPort line EBITDA Margin: 26-27% (New line in same place results in efficiency.)

Management is guiding for 25% company-level EBITDA margins over the next few years. Current is 22%.

5️⃣ Solar project adds another tailwind

A 10.8 MW captive solar plant is being commissioned.

Expected annual savings:

⚡ ~₹9 Cr

Direct boost to profitability without requiring additional sales.

6️⃣ Balance sheet has improved significantly

Debt/Equity:

FY23: 3.43x ➡️ FY26: 1.06x

Finance costs are falling and management expects further refinancing benefits.

➡️ Finance costs likely to fall further as debt reduced from ₹234 Cr to ₹204 Cr, ~90% of borrowings are now at single-digit rates, and management plans to refinance another ₹30-40 Cr of debt at lower costs.

7️⃣ PAT is growing much faster than revenue

FY26:

Revenue growth: 5%

PAT growth: 42%

A sign that operating leverage and lower interest costs are starting to kick in.

8️⃣ Next growth engine already under development

The company has:

✅ 20 products in pipeline

Focus areas:

👁️ Ophthalmics

🌬️ Inhalation therapies

💊 Specialty sterile formulations

These are typically higher-margin categories.

9️⃣ The investment thesis

This isn't a bet on IV fluids.

It's a bet that Amanta can transform from a commodity IV-fluid manufacturer into a higher-margin sterile pharma company through:

• SteriPort expansion

• Product mix improvement

• Solar-led cost savings

• Export growth

• Deleveraging

The next 12-24 months could be the most important phase in the company's history.

#AmantaHealthcare

#Pharma #Healthcare #Oncology

DYOR!!

5

896

Jun 11

Why Amanta Healthcare?? My investment thesis

Amanta Healthcare is a sterile pharma company specializing in IV fluids, injectables, respiratory and ophthalmic products. Its key differentiator is SteriPort, a premium two-port IV bottle platform that contributes ~42% of revenue.

1️⃣ SteriPort is the real story

Amanta pioneered ISBM-based polypropylene IV bottles in India.

Today, SteriPort contributes ~42% of revenue and is preferred in oncology, ICU, pediatrics and critical care due to lower contamination risk.

Current utilization is at 96%; that itself means the product is in demand.

2️⃣ Capacity expansion is about to go live

SteriPort capacity is increasing from:

📈 6.6 Cr bottles ➝ 11.6 Cr bottles

Management expects commercial production to start by June 2026.

3️⃣ This single expansion can be transformative

Management expects:

💰 Additional revenue: ₹110-120 Cr annually

Production is starting in June; that means it will add 80-90 Cr in revenue.

Against FY26 revenue of ₹288 Cr, that's nearly 30% incremental revenue potential from one project alone.

4️⃣ Margins should improve

Current EBITDA Margin: 22%

New SteriPort line EBITDA Margin: 26-27% (New line in same place results in efficiency.)

Management is guiding for 25% company-level EBITDA margins over the next few years. Current is 22%.

5️⃣ Solar project adds another tailwind

A 10.8 MW captive solar plant is being commissioned.

Expected annual savings:

⚡ ~₹9 Cr

Direct boost to profitability without requiring additional sales.

6️⃣ Balance sheet has improved significantly

Debt/Equity:

FY23: 3.43x ➡️ FY26: 1.06x

Finance costs are falling and management expects further refinancing benefits.

➡️ Finance costs likely to fall further as debt reduced from ₹234 Cr to ₹204 Cr, ~90% of borrowings are now at single-digit rates, and management plans to refinance another ₹30-40 Cr of debt at lower costs.

7️⃣ PAT is growing much faster than revenue

FY26:

Revenue growth: 5%

PAT growth: 42%

A sign that operating leverage and lower interest costs are starting to kick in.

8️⃣ Next growth engine already under development

The company has:

✅ 20 products in pipeline

Focus areas:

👁️ Ophthalmics

🌬️ Inhalation therapies

💊 Specialty sterile formulations

These are typically higher-margin categories.

9️⃣ The investment thesis

This isn't a bet on IV fluids.

It's a bet that Amanta can transform from a commodity IV-fluid manufacturer into a higher-margin sterile pharma company through:

• SteriPort expansion

• Product mix improvement

• Solar-led cost savings

• Export growth

• Deleveraging

The next 12-24 months could be the most important phase in the company's history.

#AmantaHealthcare

#Pharma #Healthcare #Oncology

DYOR!!

1

13

48

5,163

Jun 10

Good read - Inox India

#INOXINDIA

One aspect of INOX India that many investors still underestimate is that it is not really an LNG equipment company. It is actually a cryogenic technology platform company.

Most investors only focus on LNG tanks, LNG trailers and LNG infrastructure. But the same core cryogenic expertise is applicable across multiple futuristic industries.

1. Space Industry Exposure 🚀

Many investors know about the recent order linked to a global private space exploration company (widely believed to be related to SpaceX programs) but they may not fully appreciate what it means. Rocket fuels such as liquid oxygen and liquid methane require storage at extremely low temperatures. Only a handful of companies globally can design and manufacture such large scale cryogenic systems. INOX is increasingly becoming part of this ecosystem.

This is not a one time opportunity. If commercial space launches continue growing, cryogenic infrastructure demand could rise significantly.

2. Fusion Energy Opportunity

Very few investors discuss this.

INOX has worked on projects connected to major international scientific organizations such as CERN and ITER. These projects require some of the most sophisticated cryogenic systems in the world.

If fusion energy becomes commercially viable over the next decade, INOX already possesses relevant engineering credentials.

3. Export Story Is Bigger Than Most Think

Many investors still view it as a domestic manufacturing company.

However, exports have become a major contributor and a large share of its order book comes from overseas markets. The company serves customers across numerous countries and has manufacturing/service footprints beyond India.

This gives it a larger addressable market than most Indian industrial companies.

4. Hydrogen Could Be The Real Long Term Trigger

Everyone talks about green hydrogen.

Very few companies can handle liquid hydrogen which must be stored at around -253°C.

Cryogenic capability becomes the key bottleneck.

If the hydrogen economy scales globally, INOX may benefit not because it produces hydrogen, but because it supplies the infrastructure needed to store and transport it.

5. Intellectual Property Is Slowly Growing

The market generally values INOX as a manufacturing company. However, the company has also been building proprietary know how and patents in cryogenic technologies. These are difficult capabilities to replicate because they are based on decades of engineering experience and safety certifications.

What the market may still be missing

Many investors value INOX India as:

"An LNG equipment manufacturer."

A potentially more accurate description may be:

"A niche global cryogenic technology company with exposure to LNG, industrial gases, space exploration, liquid hydrogen, fusion research and advanced scientific infrastructure."

If that broader narrative continues to gain recognition over the next 5-10 years, the market could eventually assign a very different valuation framework to the business.

2

20

4,778

Jun 9

Booked Full/Partial profit in

1. Apollo micro

2. QPower

3. AbsMarine

4. Policy Bazaar

Will add healthcare, pharma and deeptech companies.

Will share new additions soon.

4

1

26

3,068

Jun 9

I have to dive into the things that i don’t understand.

Pharma

Biotech

CDMO

5

625

Jun 9

SGMart: Now it all make sense why share price doubled while business remains same.

Sanjay Gupta is enough 🔥

3

3

55

12,361

Jun 9

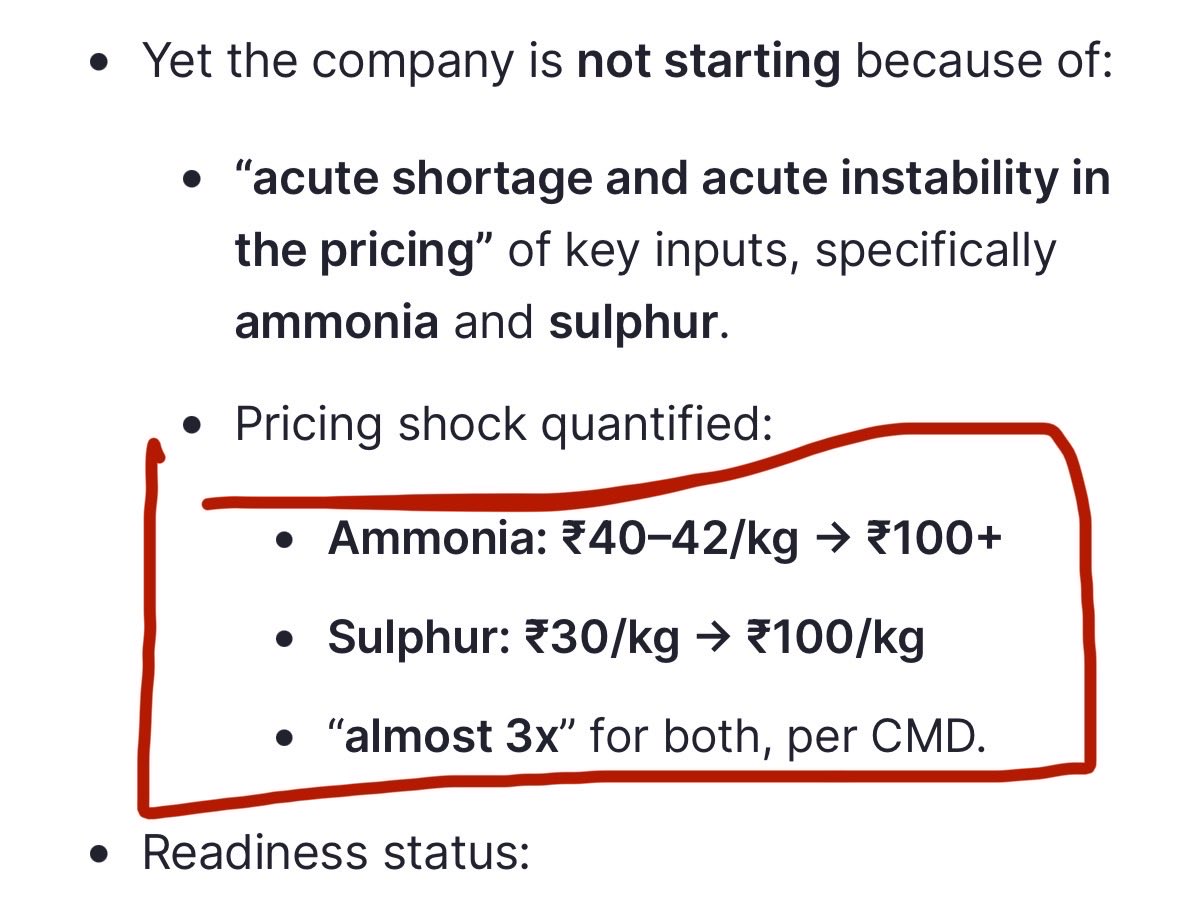

Ammonia and Sulphur prices rises almost 3x.

Who are the beneficiaries??

2

625

Jun 9

1

5

439