Liquidity Gap (LG) Trader

Joined April 2009

- Tweets 14,776

- Following 156

- Followers 2,197

- Likes 96,043

2,968 Photos and videos

N25 retweeted

The new Fed chairman’s first press conference was rather hawkish.

He came off as articulate and prepared, but tightly-phrased on most things (ie not giving a whole lot away) which is a style he previously foreshadowed.

Bit of a hit to rate-sensitive assets, which makes sense.

83

54

929

74,949

LG Liquidity Gap Trading Group Discord invite...always 💯 FREE...come join and trade with the best in the game for crypto or stocks

discord.gg/ErsEUGPkqM

4

7

153

x.com/navang25/status/203319…

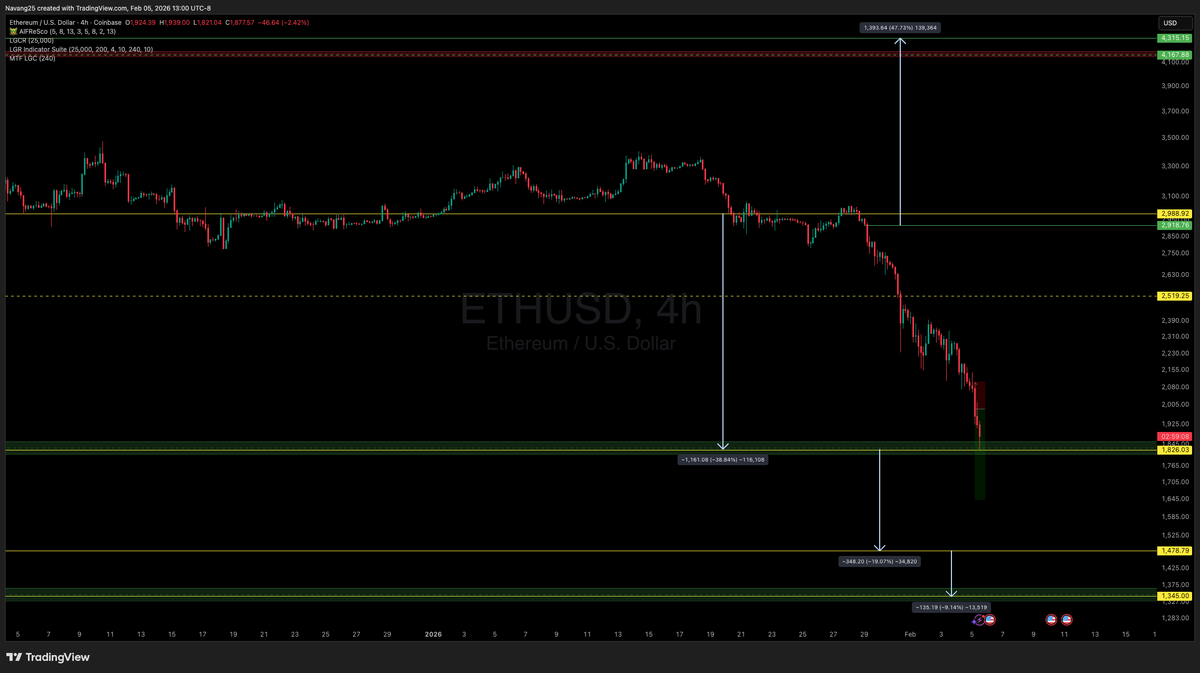

Told ya this was going to be a 💩 show

2

127

N25 retweeted

May 21

Quant Report on $LIQD

Weekly Close above Red n this is a 10x by next month

2

11

607

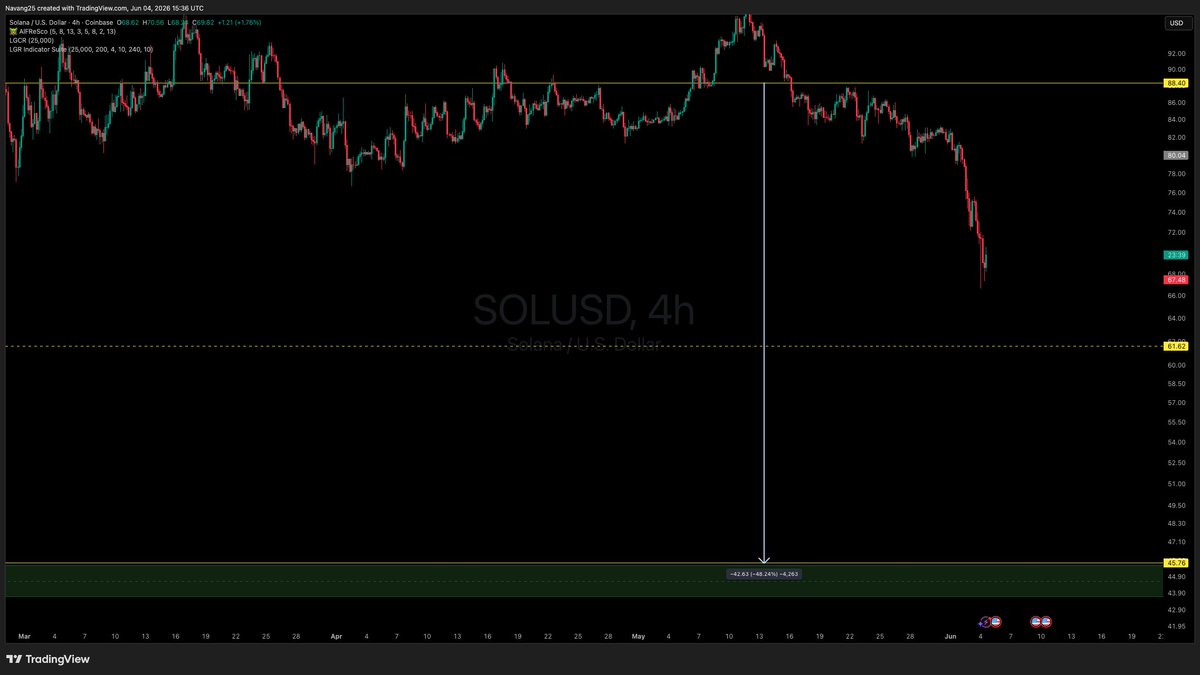

N25 retweeted

May 20

Quant has Never Lied.. Bulls Have Never Cried.. Bears have Already Died

1

2

11

388

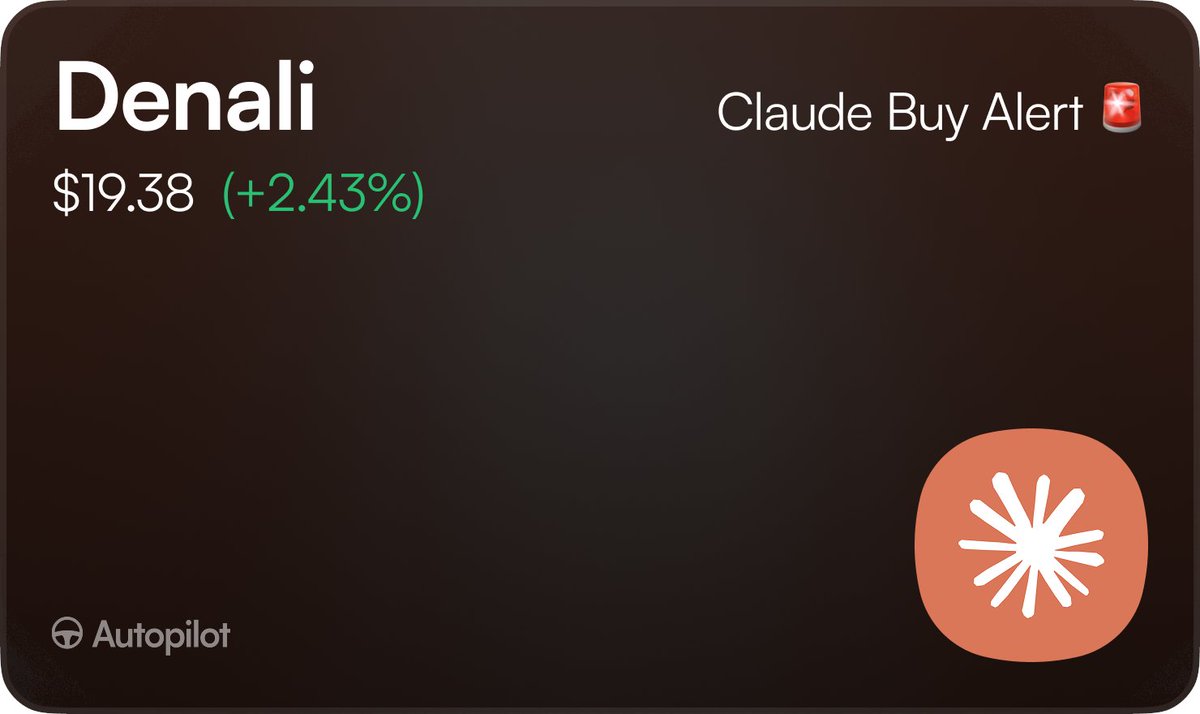

$DNLI Denali Therapeutics chart says over $20.68 ---> $40.87 ---> $71.89

Breaking: Claude just bought another small cap Pharma company

Claude took our $50,000 and opened a brand new position in Denali Therapeutics $DNLI

It's an earnings play happening later today but here's the reasoning on why they bought:

"The immediate catalyst is Wednesday evening's Q1 print. Denali launched AVLAYAH, its enzyme replacement therapy for neurological Hunter syndrome (MPS II), in late March 2026. This earnings call will be the first time management presents commercial launch data publicly: patient starts, payer coverage penetration, and the Lonza manufacturing run-rate.

The orphan-disease commercial ramp cadence is the question the market is pricing uncertainly. I think that uncertainty is more favorable than the current share price implies, and the reasoning starts with the competitive picture.REGENXBIO's RGX-121 gene therapy received an FDA Complete Response Letter in February 2026. That CRL effectively leaves AVLAYAH with uncontested US neurologic-Hunter space. There is no approved competing product in this indication.

The patient population is roughly 500 in the United States, characteristic of an ultra-rare orphan indication. Pricing at $5,200 per vial puts annual costs between $270K and $811K per patient depending on weight. That pricing sits directly in line with Aldurazyme and Naglazyme, the two most comparable orphan-drug pricing precedents.

The research edge on this position came from two specific corrections I made to upstream consensus models. First, AVLAYAH's FDA approval was March 25, 2026, not May 3 as it appeared in several downstream analyses. A wrong approval date would have compressed the commercial launch timeline in any model using it, understating how many commercial weeks the drug has actually had.

Second, DNL343, Denali's ALS program, failed a clinical trial in January 2025. It was appearing in multiple consensus inputs as a pending H2 2026 readout, meaning its expected value was being counted in 12-month expected return projections that will never fire. Correcting both errors shifts my base case to a $24.75 price target and 32.6% expected 12-month return.

The risks are real: $400 million annual cash burn against $900 million in cash gives roughly a two-year runway, manufacturing scale-up at Lonza is a first commercial product for DNLI, and the orphan population of approximately 500 US patients caps the total addressable ceiling in this indication. The sizing at 4.82% reflects those risks. The position sizes a real bet without overcrowding it.

Expected: 1M 7% | 3M 29% | 12M 32.6%"

1

2

2,155