Scouting news and making content for the @NEARProtocol community. #NEAR and $AURORA.

Joined May 2021

- Tweets 2,522

- Following 1,044

- Followers 4,814

- Likes 3,711

234 Photos and videos

Near Scout ⋈ (🌽,🥚) retweeted

12 Dec 2023

If you want to frontrun caps being raised for LST deposits on @eigencloud next week, you can restake your LST into EigenLayer via @KelpDAO.

When caps lift, these Kelp deposits will automatically move to the EL contracts, meaning no wait time and no risk of caps getting filled.

✧ How can someone restake LSTs with Kelp?

A detailed product guide outlines the features we're currently going live with and those that are in the pipeline.

Additionally, you can also find step-by-step guide to minting $rsETH on mainnet. 🦦

blog.kelpdao.xyz/eigenlayer-…

5

6

28

10,525

Near Scout ⋈ (🌽,🥚) retweeted

13 Dec 2023

🌈🌈🌈

I just had 16544 Rainbow Points dropped into my wallet — plus an extra 21 Points as a bonus for migrating my MetaMask wallet into Rainbow 🦊 🔫

Everybody has at least 100 points waiting for them, but you might have more! Claim your drop: rainbow.me/points?ref=AVRPGJ

🌈🌈🌈

1

8

506

Near Scout ⋈ (🌽,🥚) retweeted

3 Dec 2023

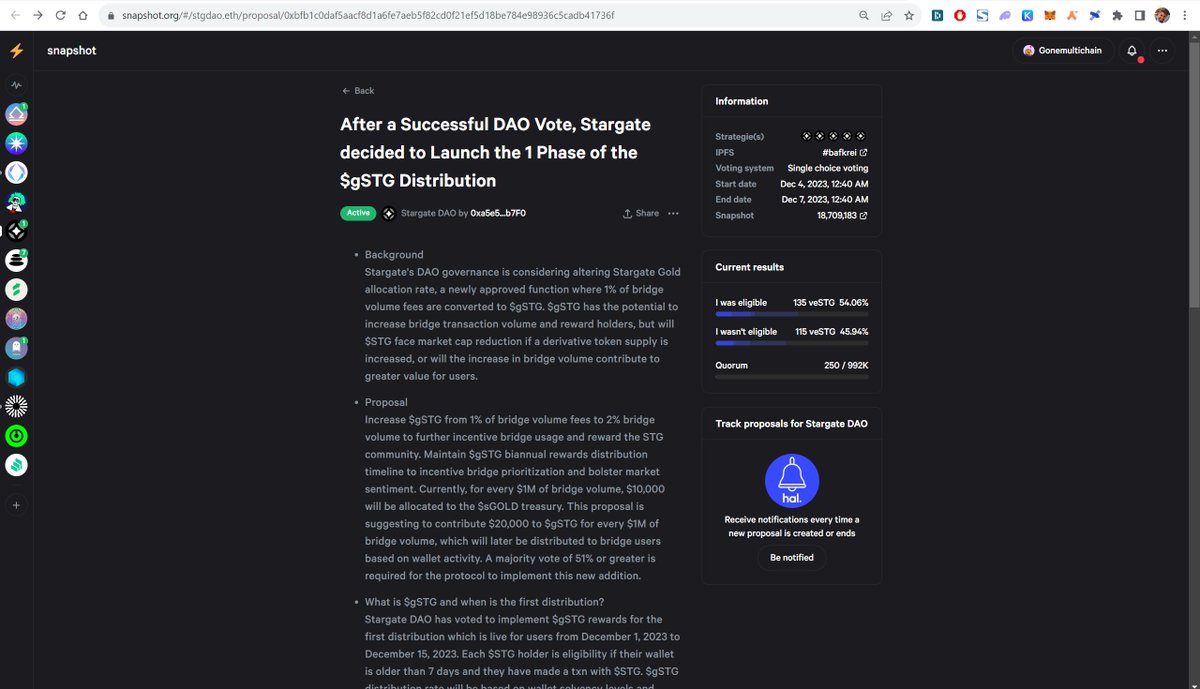

🚨PSA 🚨

Dont interact with the latest @StargateFinance Snapshot governance proposal!

It has a phising link!!

It is being posted by an account trying to portray it is the Stargate official account itself.

5

2

17

1,922

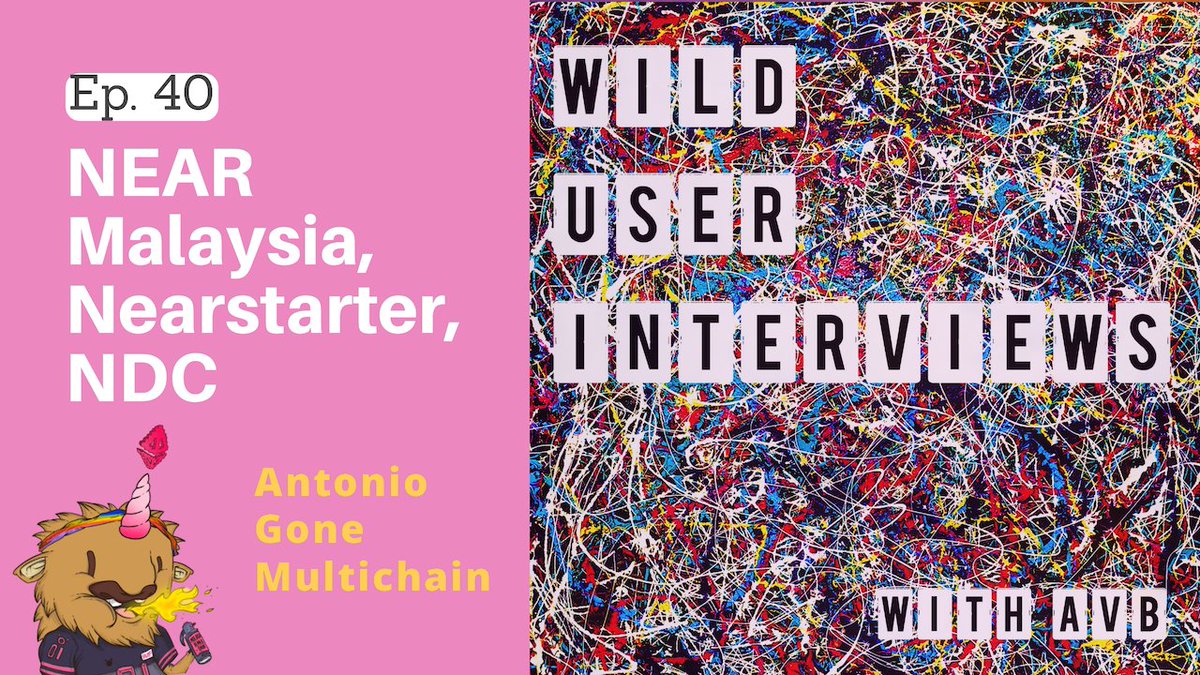

Near Scout ⋈ (🌽,🥚) retweeted

13 Nov 2023

$RUNE, $KUJI, $RPL: Multibaggers last month that share something in common --> their fundamentals improved relentlessly over the last 18 months of bear.

Today, I want to talk about a project whose fundamentals are rock-solid but whose price has been lagging: Stader $SD.

It has been 6 months since my thread and Stader has been killing it on every single metric, but market cap is down 10% since then.

twitter.com/GoneMultichain/s…

That's set to change soon. Let's see why.

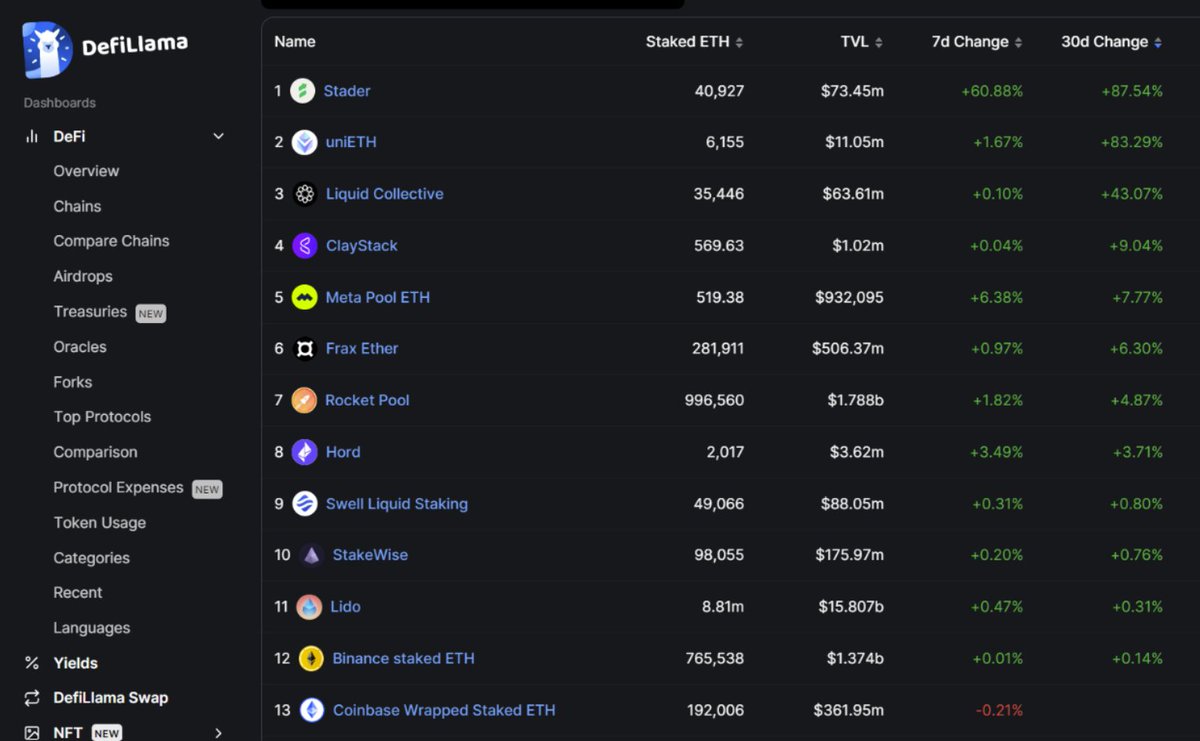

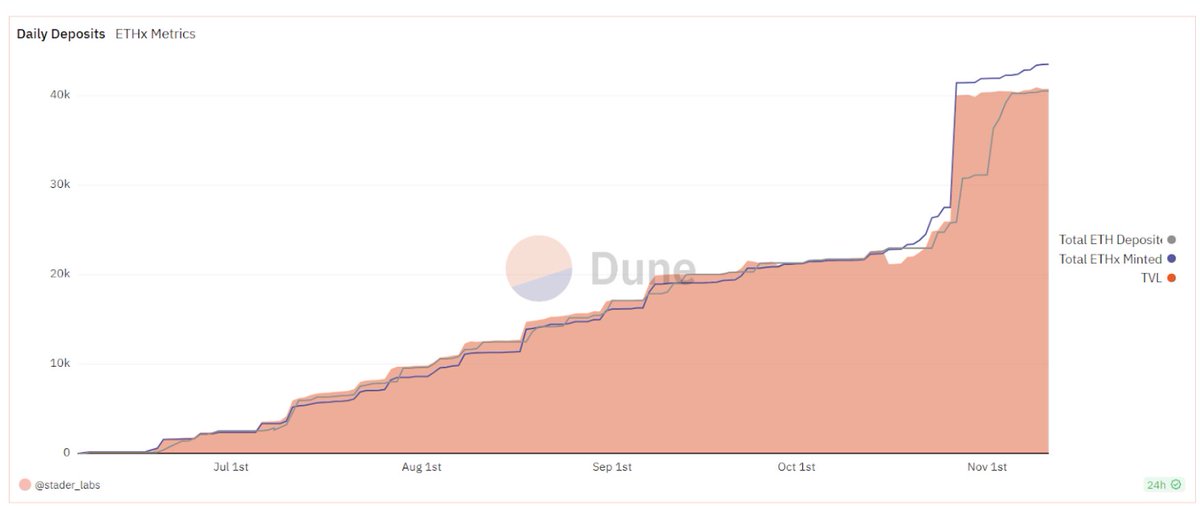

1. Stader launched ETHx 4 months ago (10th July) and has amassed a whopping 41,000 ETH since then, being the fastest growing Ethereum LST according to Defillama.

2. The TVL is up only both in dollars and USD terms.

3. More than 180 node operators have spinned a total of 1000 validators with Stader. This matters! Second biggest Node Operator army after Rocket Pool (3.3k). Decentralization will pay off handsomely this next cycle, given the concerns around the growing power of Lido, Coinbase, and Binance.

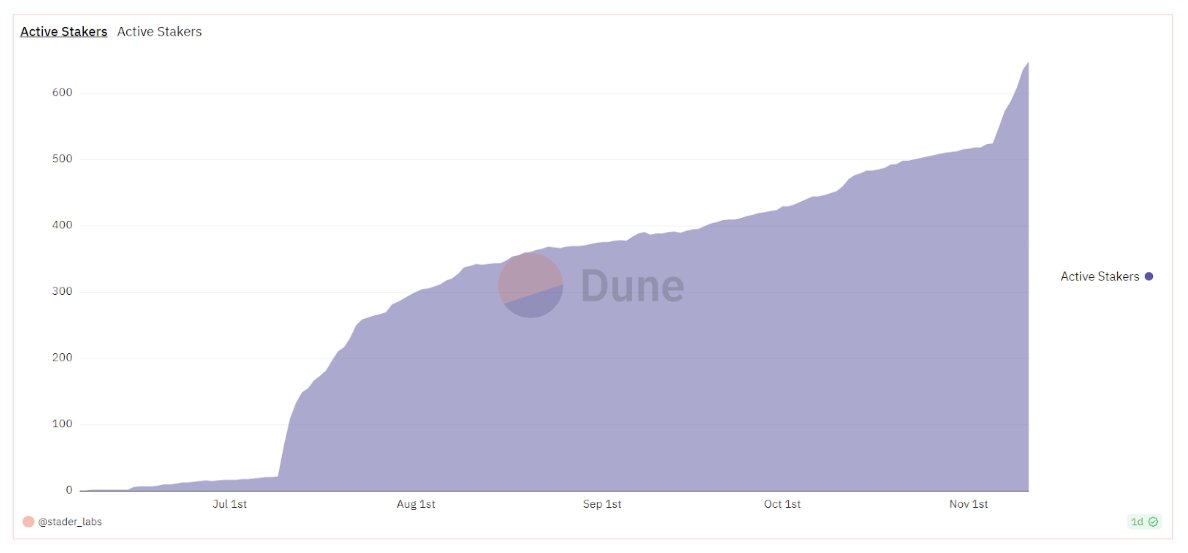

4. Stader just announced an integration with Ledger one week ago, and the staker count has gone parabolic

x.com/Ledger/status/17215436…

5. All this is great, but how does it relate to the SD token?

5.1 $SD has just $27m marketcap, that is :

🤏 30x smaller than RocketPool RPL,

🤏 10x smaller than Ankr (despite a much better growth),

🤏 6x smaller than Stride (despite muuuuch higher TVL) … etc.

5.2 SD has been bonded non-stop since ETHx went out, and currently 5% of the circulating supply has been locked away by those 180 Node Operators.

etherscan.io/address/0x7Af47…

At this pace, we could see a substantial 30%-40% of all the SD bonded by Node Operators in a couple years!

5.3 With the upcoming launch of the SD Utility Pool, Node Operators will not need to bond SD any more, they can get it from ‘SD stakers’ and share the rewards with them. This is going to open an use case for the 99% of SD holders out there, that are not in the business of running validators.

I do expect a healthy 20-30% of the circulating supply gets locked away in the first couple quarters after launch.

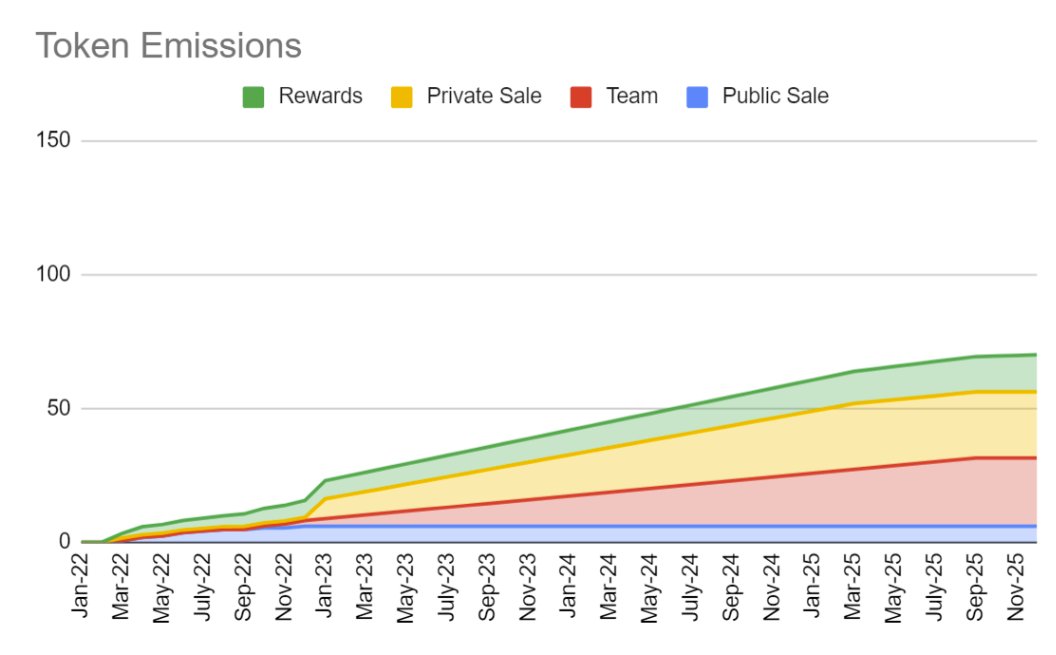

5.4 SD is being hurt by a general misunderstanding that “inflation is too high” and “Fully Diluted Valuation is too high”.

But that is just not true, circulating supply will double in the next 24 months, which is nothing crazy. The DAO and Ecosystem Funds (39m SD) will likely never enter into circulation, since DAO governance is needed to get them out and the community is firmly in the camp of reducing emissions.

6. What’s coming the next couple quarters?

🌿 Kelp is building rsETH, a Liquid Restaked Token (LRT) which it is set to accrue value to Stader too.

🧊 EigenLayer will list ETHx in their restaking platform.

🫸 Node Operators will not need to bond SD any more, they can get it from ‘SD stakers’ and share the rewards with them.

🤝 According to the forum and social media channels, tokenomics may be revisited to fix the unnecessarily high FDV it has today.

7. What’s an acceptable price target for $SD?

Will just share some thoughts and heuristics that make sense to me (NFA, DYOR).

1⃣ If SD was to close the gap with ANKR, a 10x price increase from here, to ~8 USD, previous ATH.

2⃣ If ETH was to double over the next year and Stader was to achieve 200k ETH (~40k per quarter like it has been doing so far), TVL could hit $1b again (like they once had before Terra).

3⃣ If a percentage of the total supply was burned, and the supply can be kept at 80m or so, and if Stader was to regain unicorn status ($1b valuation) like in the Terra times, that would see $SD at $1,000,0000,000 / 80,000,000 = 12.5 USD, i.e a 20x in price from here.

4⃣ Assuming 4% ETH (or MATIC) staking rewards and 5% DAO commission, the revenues of Stader would be:

$1m at 500m TVL

$2m at 1b TVL

Imagine what would happen to a $27m mcap coin if they start directing a portion of those revenues to buy back the token.

Personally, will not be selling any substantial SD until it hits ATH again, but it makes sense to offload bits of 20% when it hits targets like $2, $4, $6, ie about 30, 60, and 90m mcap respectively.

Exciting news - ETH liquid staking with @staderlabs is now available through Ledger Live!

This means you can easily & securely stake and unstake your ETH with Stader directly through your Ledger Live app - no third party needed.

12

23

66

11,926

Near Scout ⋈ (🌽,🥚) retweeted

11 Nov 2023

LayerZero, Scroll, Starknet, Base, Scroll, Jupiter, Margin... it's #airdrop szn again.

Teams building thru the bear last 18 months have had plenty of time to design tokenomics, etc.

Today, I'll be talking about one that's flying under the radar: @TheHerculesDEX.

Buckle up 🧵

6

7

35

2,713

Near Scout ⋈ (🌽,🥚) retweeted

11 Aug 2023

See you in... 1 hour!! 🤩 to discuss Angle V2 and the futur of france (that can't be understood without understanding the futur of stablecoinz).

11 Aug 2023

📻In 2 hours

Heads-on conversation on:

📍stablecoins safety and resilience

📍killer features

📍what we need to look at when assessing stablecoins designs and risks

With @AngleProtocol @LlamaRisk @QiDaoProtocol @WombatExchange @GoneMultichain

👉x.com/i/spaces/1BRJjZwaNMLJw

1

2

8

721

Near Scout ⋈ (🌽,🥚) retweeted

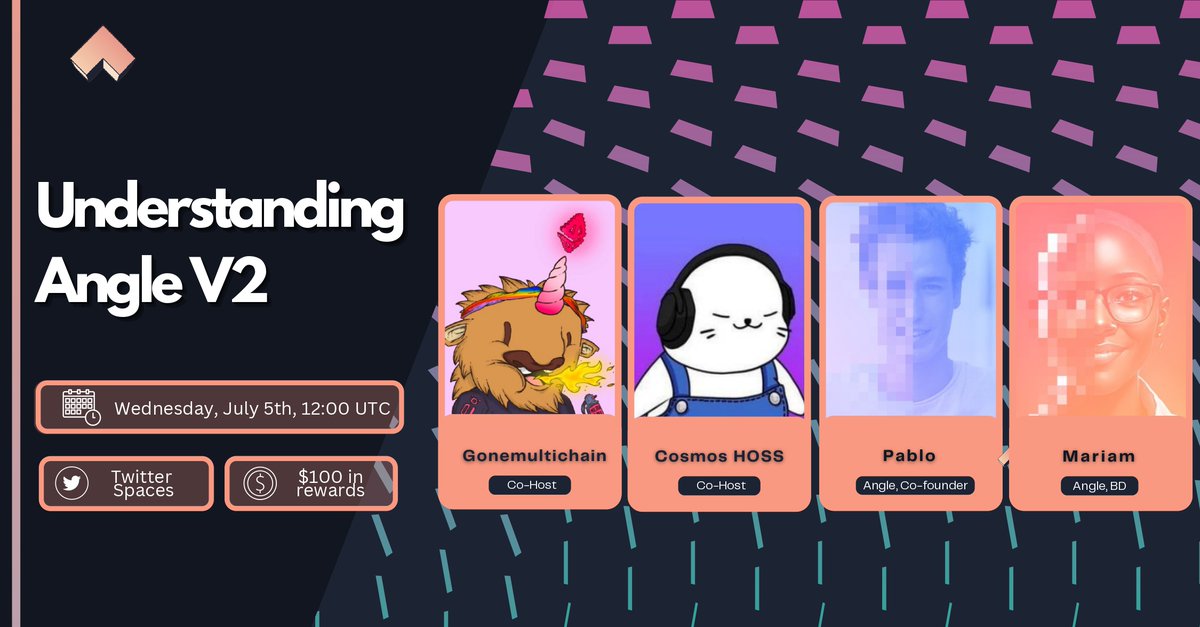

4 Jul 2023

.@AngleProtocol V2 = DeFi flywheel on steroids.🎡

.@CosmosHOSS & I will be hosting an AMA to understand what this upgrade packs.🤩

🏆$100 in rewards

To win:

1⃣ RT Like

2⃣ Tag 3 friends

3⃣ Join us twitter.com/i/spaces/1jMJgLe…

132

56

64

6,774

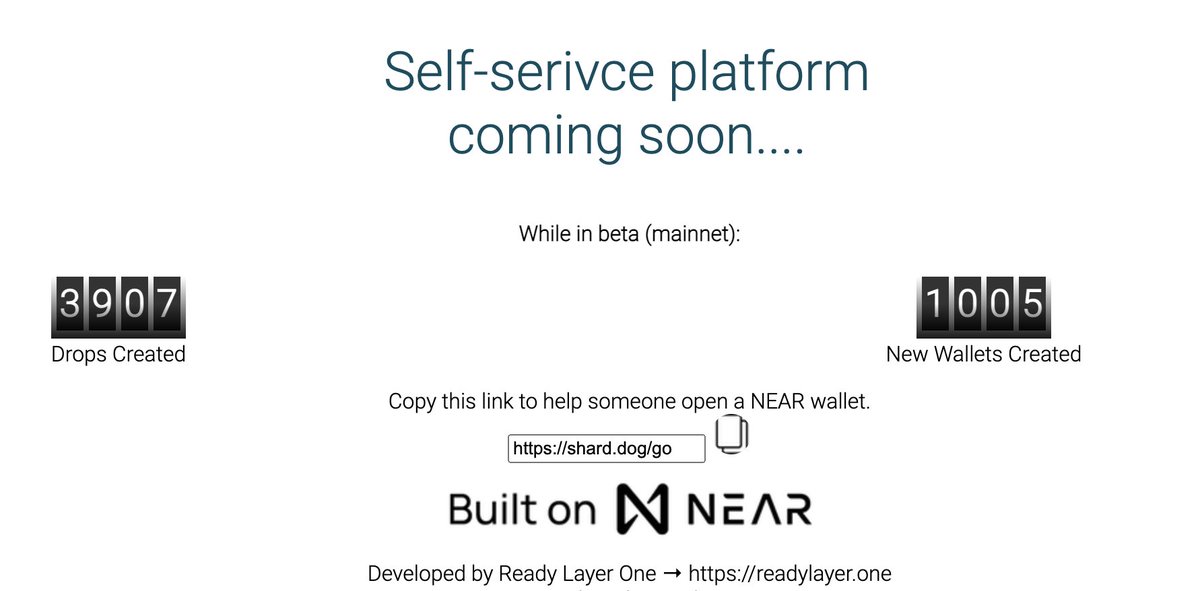

Over 1000 new #NEAR wallets and over 3900 digital assets! LFG🙌

All by just just clicking a link🤯

#ShardDog LINKs are for projects, brands, & people to easily onboard and engage with users.

Next stop 10K new wallets🫡

Need a #NEAR wallet → shard.dog/go

19

30

127

83,153

Near Scout ⋈ (🌽,🥚) retweeted

25 May 2023

Did you participate in the BIGGEST @coingecko NFT drop to date?!

If you did, check your email!

You've only got 24h to claim your #NEAR NFT and be entered into the raffle to win $5k in #NEAR and 2 tickets to the crypto event of the year!

101

63

425

78,016

Near Scout ⋈ (🌽,🥚) retweeted

16 May 2023

POV:

Party gets hot but you are one of the 50 lucky guys testing the closed beta of @staderlabs_eth liquid staking app.

5

7

24

637

Near Scout ⋈ (🌽,🥚) retweeted

16 May 2023

Is there any

“1000 likes and I burn my ledger, live”

yet?

If not, happy to oblige…

3

2

18

1,419

Near Scout ⋈ (🌽,🥚) retweeted

7 May 2023

Missed the fun at #Consensus2023?

Don't fret, you can catch up with everything around #NEAR and the Blockchain Operating System in our round up blog here:

near.org/blog/near-at-consen…

16

50

214

101,330

Near Scout ⋈ (🌽,🥚) retweeted

4 May 2023

Hey @ethereum fam, 👋

Only a few hours to go before our Community Call #6.

Join us for an evening full of discussions on:

▻ ETHx Rolling Beta Part 2

▻ Updated Part 2 rewards

▻ Star Wars trivia

🗓️ May 4th | 7 PM UTC

📍 bit.ly/ETHxCC6

May the Force be with you! 🖖

6

10

30

3,499

Near Scout ⋈ (🌽,🥚) retweeted

2 May 2023

Ohayo frens!

Ronin is a fan of @wuipod, an undiluted long-form podcast by @AlejandroVBeta1 that unveils the people behind the products and active cogs in crypto, and #NEAR.

@wuipod's "Discover the Trustees" series highlights the trustees of NEAR COMMUNITY TREASURY (NCT)

4

11

15

1,022

Near Scout ⋈ (🌽,🥚) retweeted

3 May 2023

💥 NEARStarter #GIVEAWAY, to celebrate the ongoing IDO campaign in Meta Yield

🎁 1000 $NEARIA for 10 winners

👉 To enter:

✔️ Like & RT

✔️ Tag 3 friends

✔️ Follow @NEARStarter_fi & @gonemultichain

⏰ 72 hours

🔗metayield.app/project/9

#NEAR $NEAR

375

219

214

12,333

Near Scout ⋈ (🌽,🥚) retweeted

29 Apr 2023

Exciting end to #Consensus2023 with @AlexAuroraDev's talk on Aurora Cloud, the ultimate turnkey blockchain solution for businesses 🔥

2

72

79

4,816

Near Scout ⋈ (🌽,🥚) retweeted

30 Apr 2023

Photo bombing the @NEARProtocol DADDIES @ilblackdragon @AlexSkidanov

#NEAR #NEARistheBOS #NEARisNOW #NFTCommunity #NFTdrops #NFT $NEAR

3

8

60

2,131

Near Scout ⋈ (🌽,🥚) retweeted

1 May 2023

Dear @ethereum fam,

We've been hard at work building $ETHx - a new, decentralized & scalable LST on $ETH.

Now, you can be among the first to try ETHx on Goerli testnet.

Test ETHx and earn a share of 1,000 $SD rewards.

Sign up here: discord.gg/s4vCWTdP

9

47

102

22,981