The next generation of crypto-native yield

Joined January 2025

- Tweets 885

- Following 30

- Followers 14,711

- Likes 3,621

103 Photos and videos

Neutrl retweeted

Jun 10

The Neutrl sNUSD market just hit 99% utilization.

Almost all Junior capital is actively backing Senior deposits, and the yield curve is adjusting to bring more in.

Worth understanding what's going on.

3

2

21

4,656

Neutrl retweeted

Neutrl (@Neutrl) has been an unproblematic stablecoin in a sea of nonsense this last year.

One of the first to adopt fully transparent & real time proof of reserves, they're now in S2 heading towards TGE.

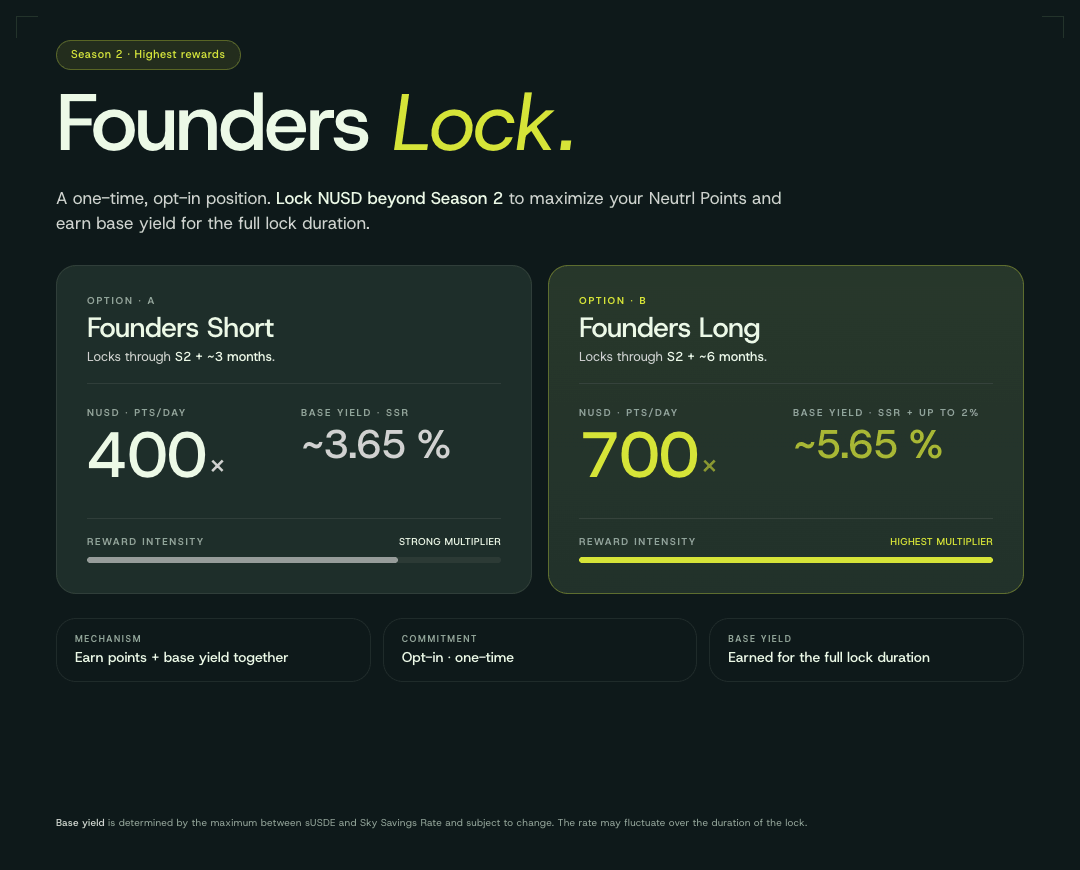

► 5.15% Base APR

► 6-7% Pendle Fixed Rate

► 400-700x Points for Locks

8

4

62

8,596

A quick clarification regarding recent discussion around APYX.

Neutrl does not have exposure to APYX or STRC products within our reserve portfolio.

As always, users can independently verify reserves through the Neutrl transparency dashboard powered by @AccountableData.

accountable.neutrl.finance/

Hi @andrewhong5297, this is great stuff, but I just want to clarify that Neutrl does not have direct exposure to APYX.

A third-party curator has allocated roughly $800K of capital into ptsNUSD and srNUSD as part of their vault strategy. Neutrl itself does not hold APYX on our balance sheet and have not been affected by the STRC depeg in any way.

This can be verified here:

app.morpho.org/ethereum/vaul…

Our reserves can also be verified through our @AccountableData dashboard:

accountable.neutrl.finance/

Would love to play around with doubleclick myself.

6

1

26

6,243

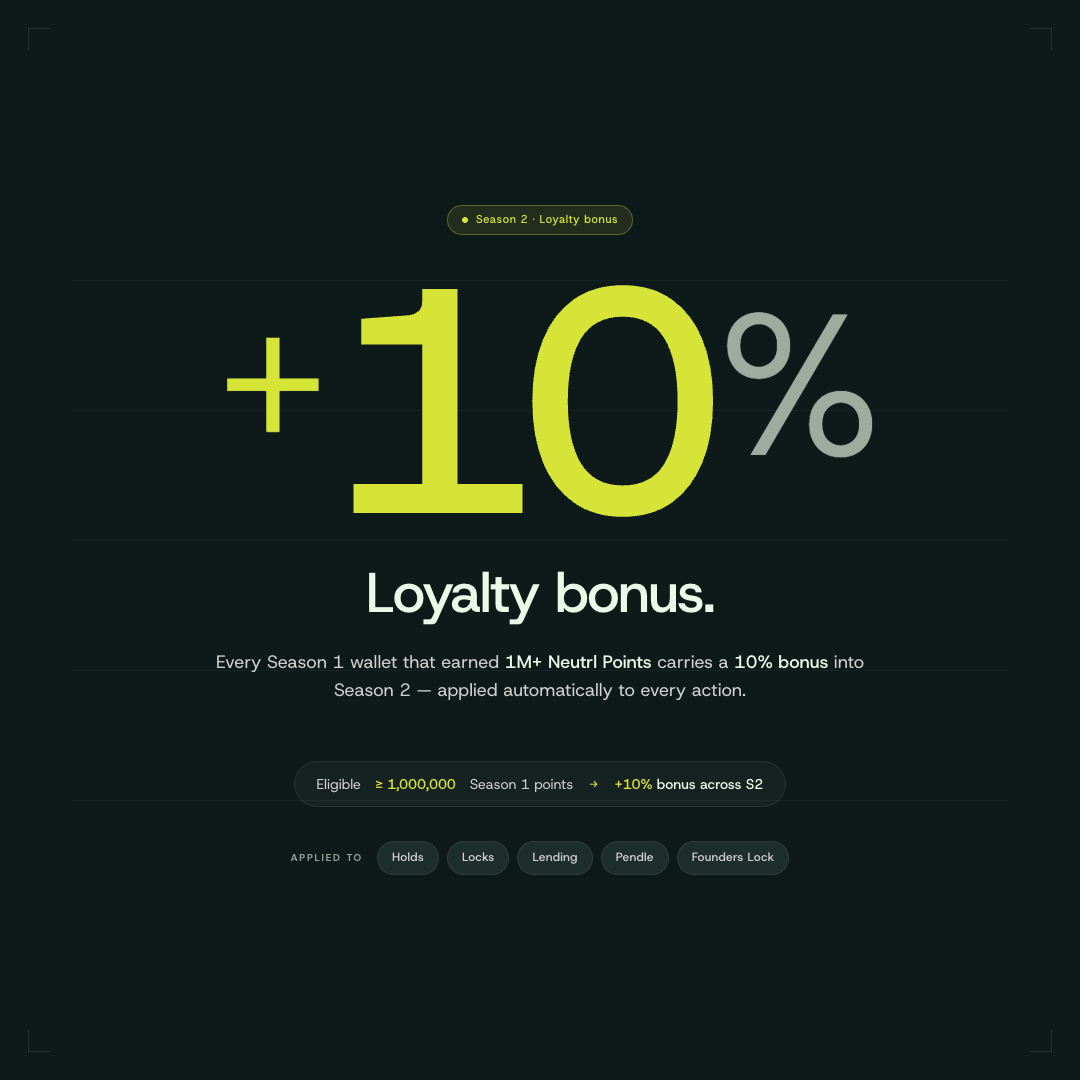

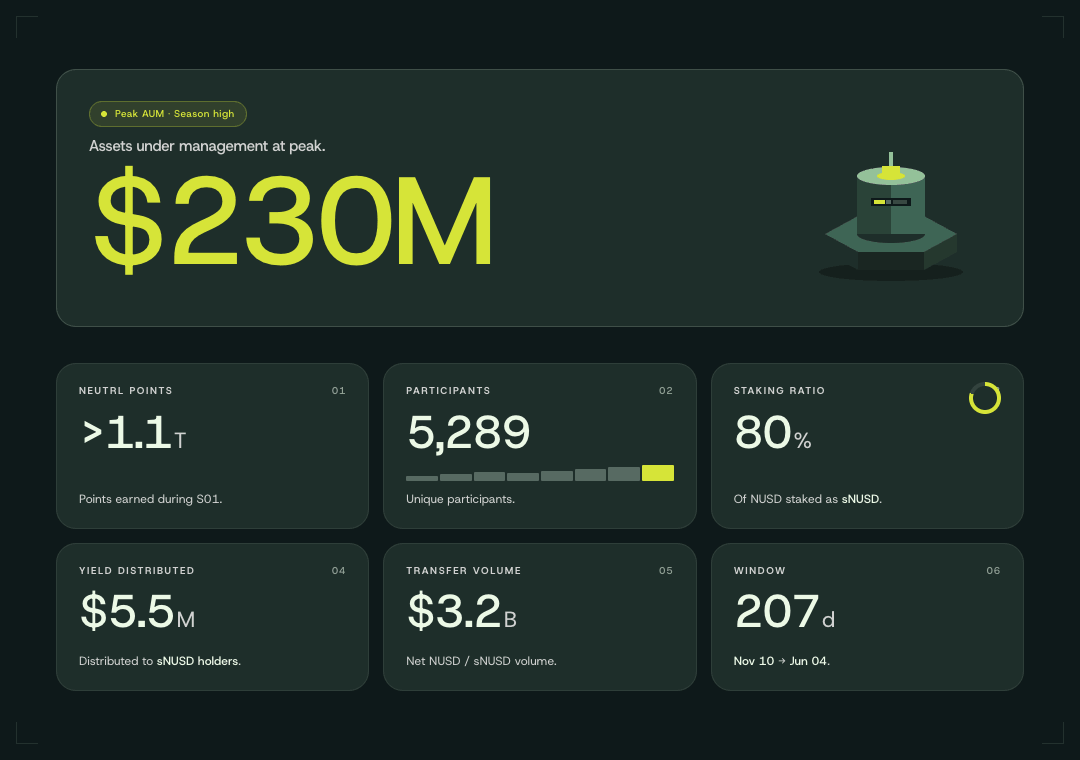

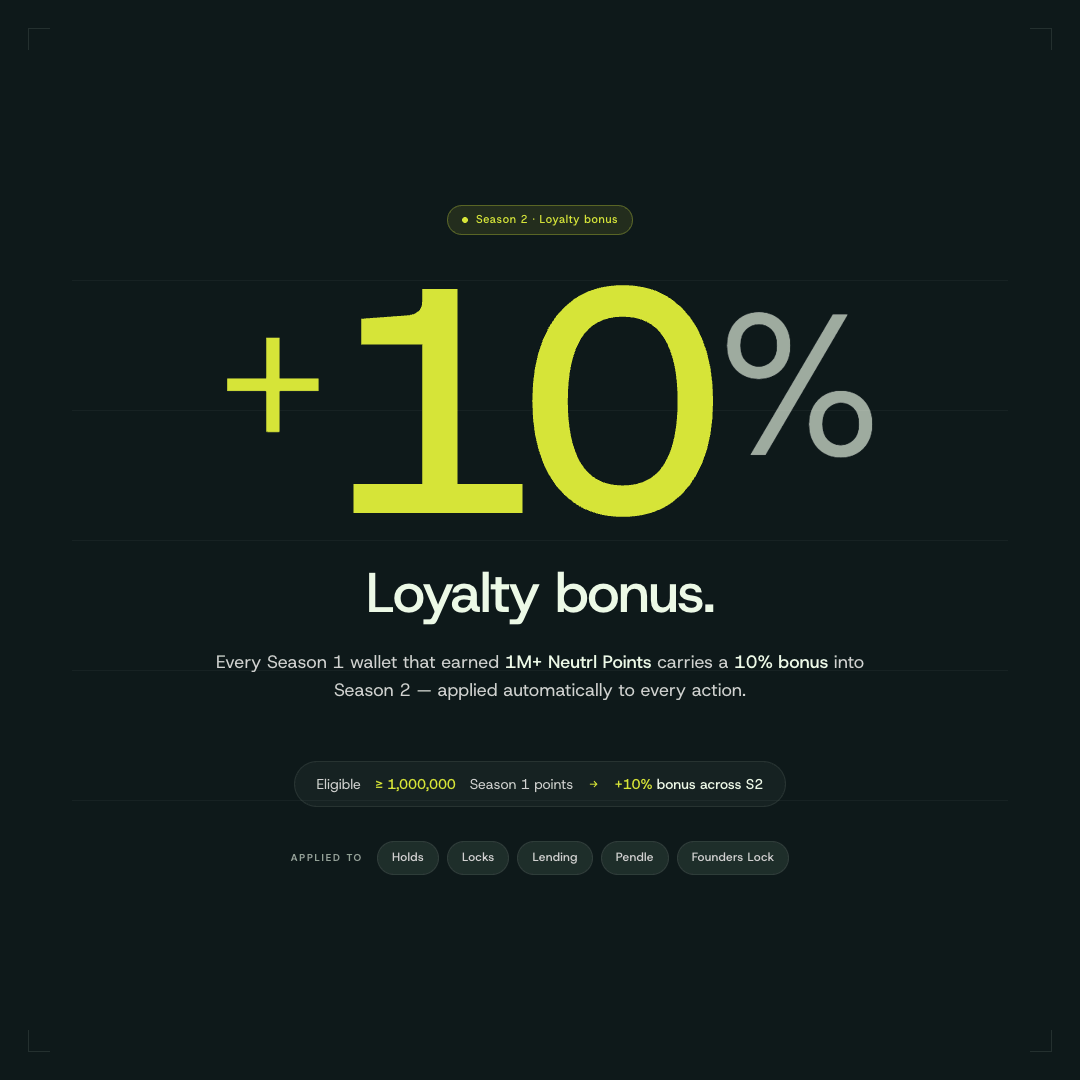

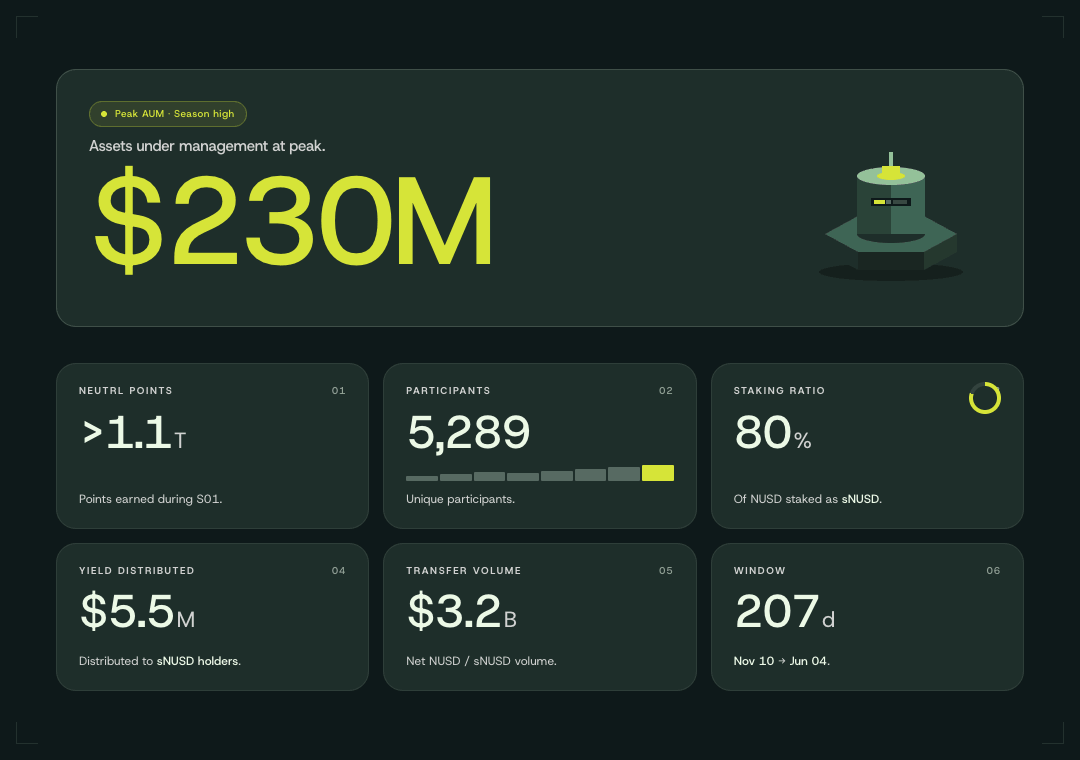

Season 1 helped establish Neutrl as one of the fastest-growing synthetic dollars to date.

Season 2 is focused on alignment, commitment, and preparing for the next chapter.

The road to TGE starts now.

1

8

1,082

Season 1 was about growth.

Season 2 is about alignment.

Learn more about the next phase of Neutrl here. 👇

Season 2 will run for approximately 3.5 months and conclude with Neutrl’s TGE in mid-September.

The mechanics introduced here are designed to position participants for the next phase.

More details on the protocol token and new developments will be shared throughout S2.

neutrl.finance/blog/origin-p…

1

1

5

1,220

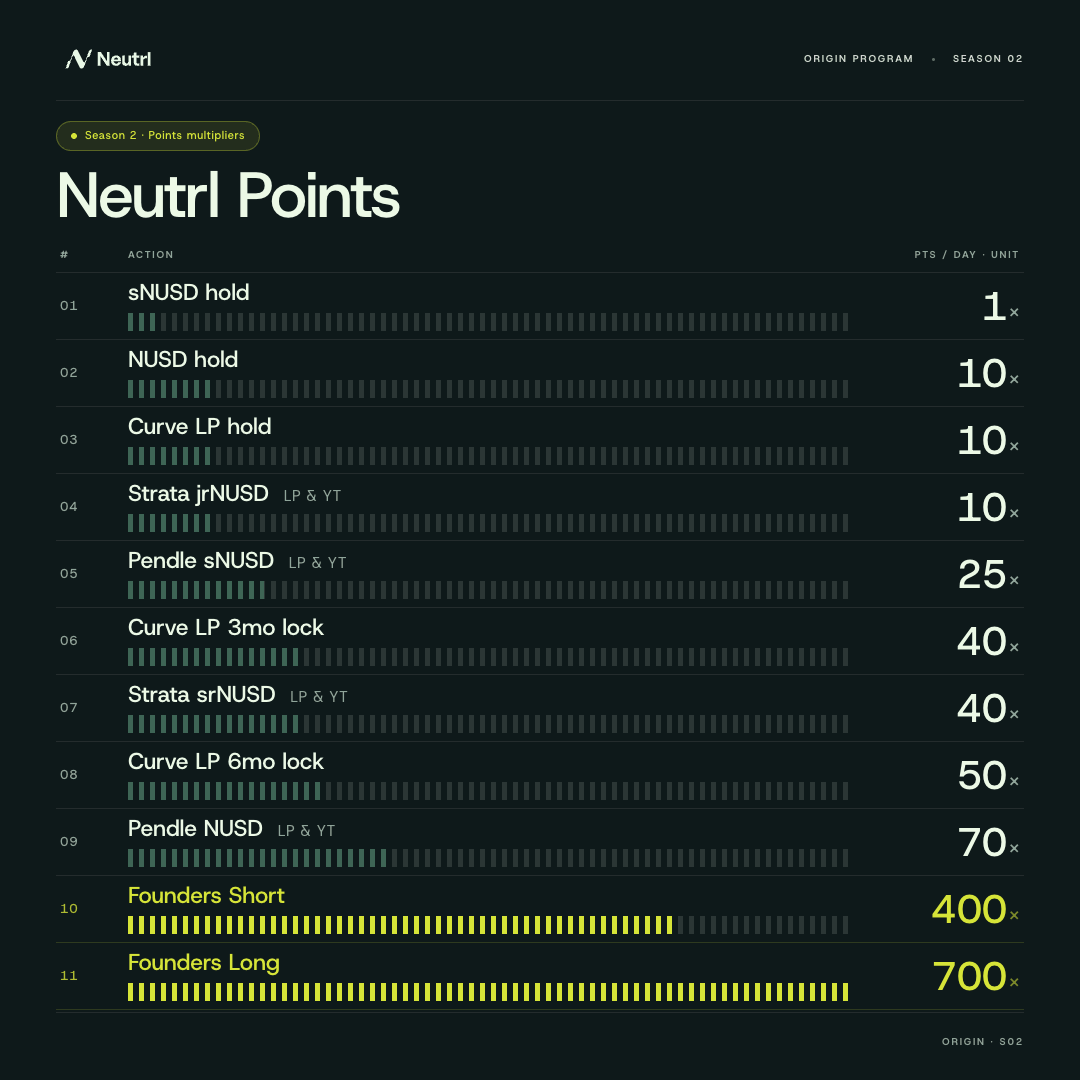

New NUSD and sNUSD pools are now live on @pendle_fi.

The new maturity date of 24 Sep 2026 has been aligned with the end of Season 2 of the Origin Program.

Neutrl Points for the LP & YT NUSD have also been increased to 70x.

4

4

35

2,920

You can roll over before maturity.

Swap your existing PT or LP into the new market by selecting your current position as the input token.

Or wait until maturity and redeem and roll over directly from your Pendle dashboard in 1-click.

NUSD (24 Sep 2026): app.pendle.finance/trade/poo…

sNUSD (24 Sep 2026): app.pendle.finance/trade/poo…

1

2

1,071

We have been getting some questions from LPs why we carry the otc amounts at a discount to current spot. We only do trades on highly liquid spot/perp with multiple tier 1 venues and enough history.

The discount collateral formula:

For a deal with n vesting tranches:

Total Value = Σ vᵢ × spot price × min((1 − discount)^(days to vestᵢ ÷ 365), cap)

Each tranche is valued independently, then summed. For every tranche we take the lesser of the time discounted value or the cap, whichever is more conservative.

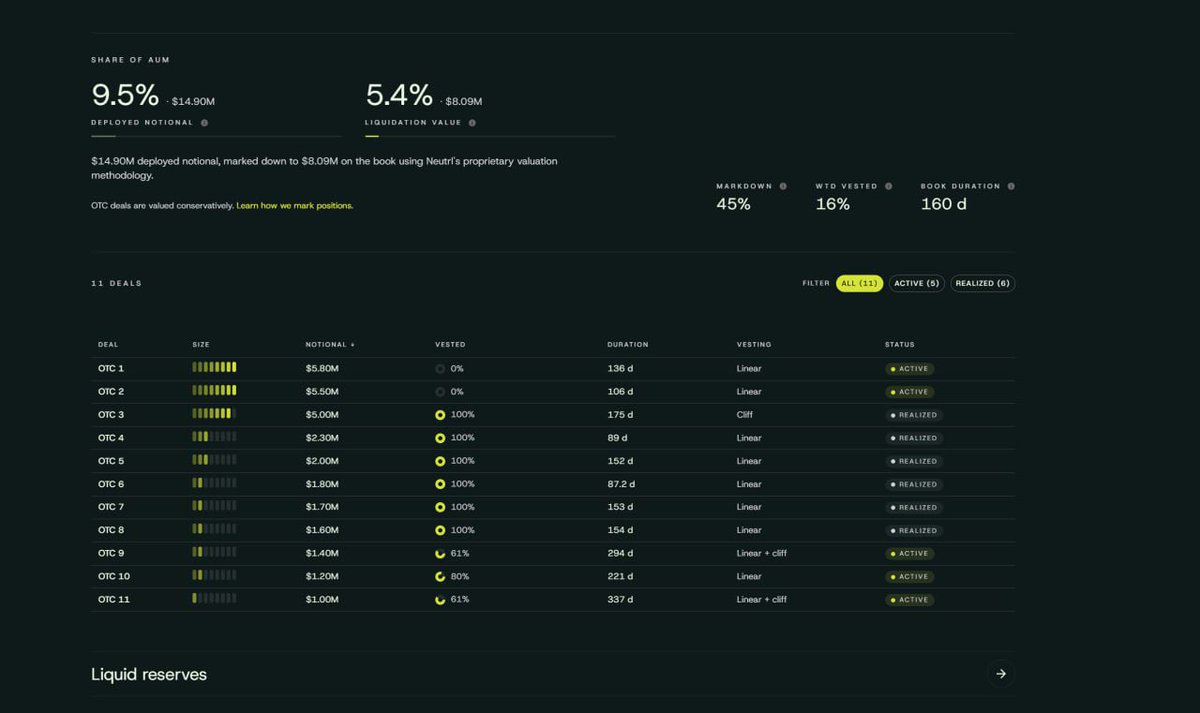

Worked theoretical example using OTC 9 from the dashboard

OTC 9 is active, 61% vested, 294 day duration, Linear Cliff vesting. Let's assume it has just 2 remaining tranches:

Tranche A

Tokens (vᵢ) - 5000

Days to vest - 90

Spot Price - $1

Tranche B

Tokens (vᵢ) - 5,000

Days to vest - 294 days

Spot Price - $1

Using a 35% discount and cap = 0.75:

Tranche A: 5,000 × $1.00 × min((0.65)^(90/365), 0.75) ->(0.65)^0.247 = 0.888

We us min(0.888, 0.75) = 0.75 cap kicks in so value carried at in reserves = $3,750

Tranche B: 5,000 × $1.00 × min((0.65)^(294/365), 0.75) (0.65)^0.805 = 0.693

Min(0.693, 0.75) = 0.69 Time weighted discount used so value in reserves = $3,465

Total booked value = $7,215 vs $10,000 market price ~28% markdown.

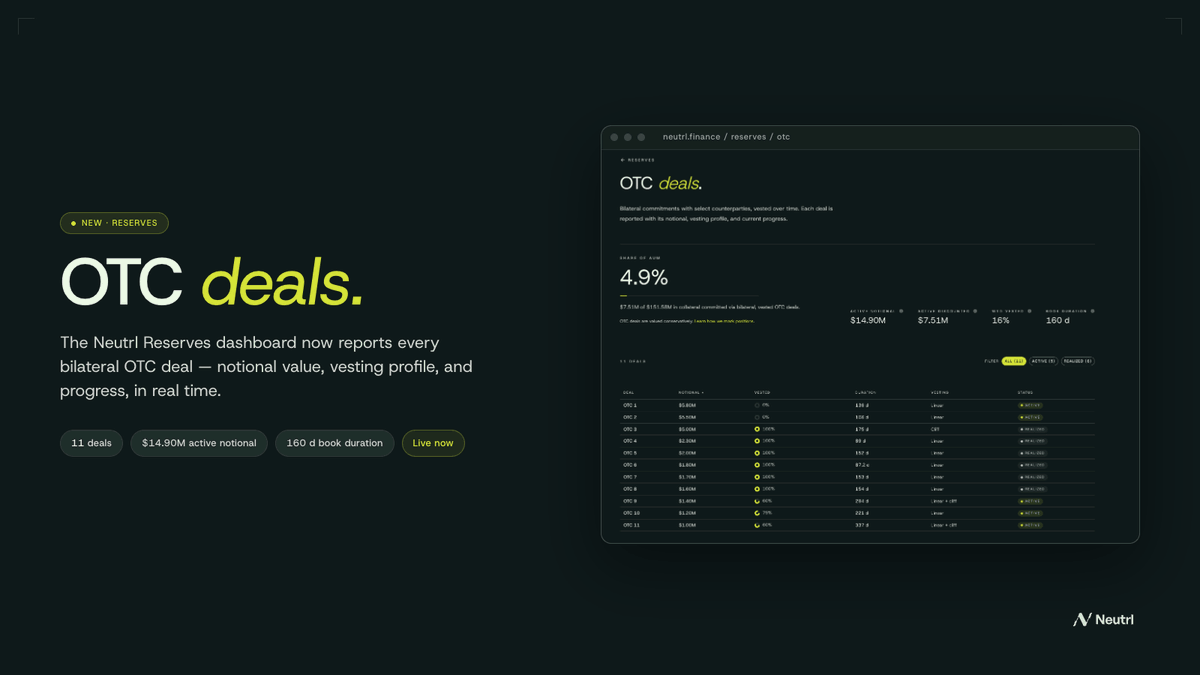

The dashboard shows this in action at scale:

$14.90M deployed (notional for current live deals) ~ 9.5%

$8.09M liquidation value (what it's booked at after discounts to be conservative) - 5.4% shown in reserves

The further out the vest, the harsher the haircut. Even near vesting tranches get capped below spot.

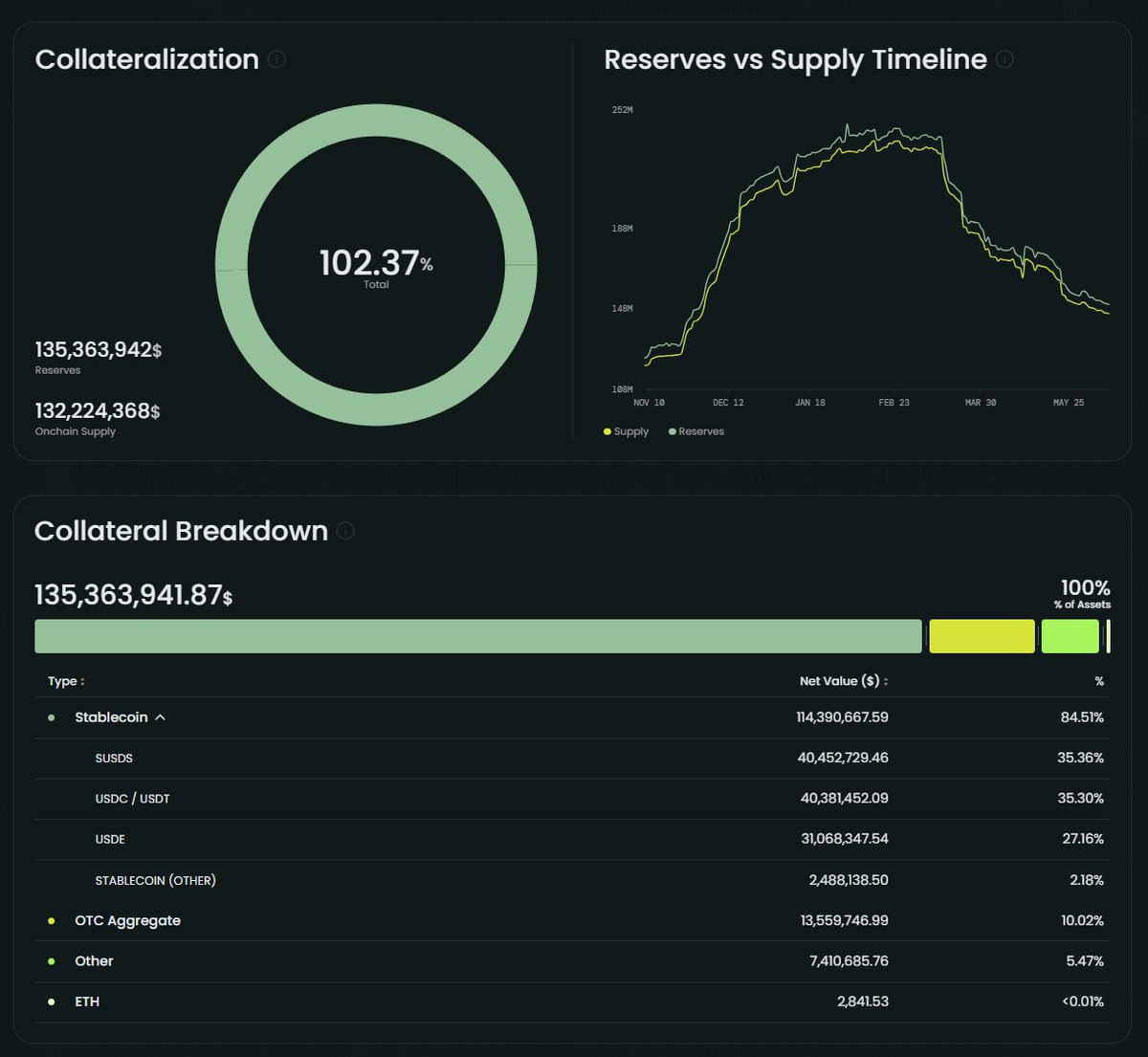

This is intentional conservatism, it means NUSD's collateral is never overstated even at the current 103% .

4

3

21

2,538

Neutrl retweeted

May 27

srNUSD and jrNUSD Pendle pool migration is LIVE!

Rollover your LP and continue earning:

• LP-srNUSD-SEP26: 4.94% APY 60x Strata 40x Neutrl

• LP-jrNUSD-SEP26: 7.9% APY 20x Strata 10x Neutrl

Explore our @pendle_fi x @Neutrl pools 👇

5

4

23

3,484

Season 2 will run for approximately 3.5 months and conclude with Neutrl’s TGE in mid-September.

The mechanics introduced here are designed to position participants for the next phase.

More details on the protocol token and new developments will be shared throughout S2.

neutrl.finance/blog/origin-p…

2

1

12

2,447