SOC1-audited, enterprise-grade platform for crypto protocols addressing the unique compliance needs of CPAs, fund managers, high volume traders and more.

Joined February 2015

- Tweets 3,261

- Following 884

- Followers 2,669

- Likes 2,688

467 Photos and videos

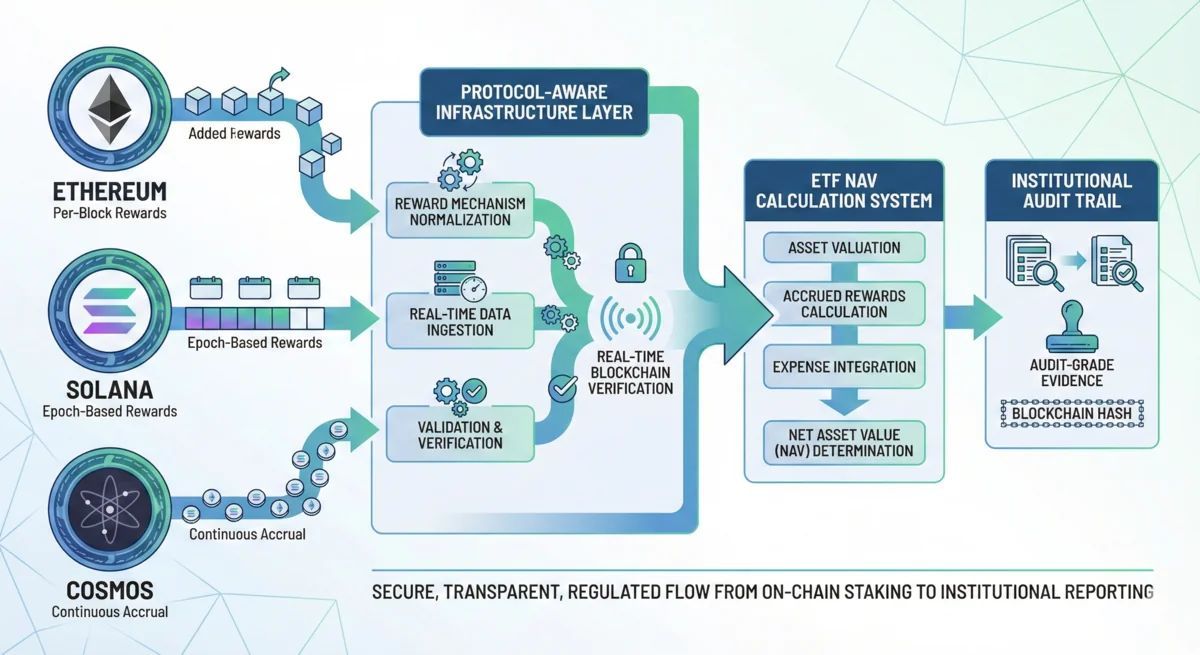

CME launched crypto index futures including SOL on June 10. Regulated access brings regulated expectations. Institutional counterparties will eventually need staking reward attribution and subledger records from validators. Most validators don't produce them. coinmarketcap.com/cmc-ai/sol…

2

9

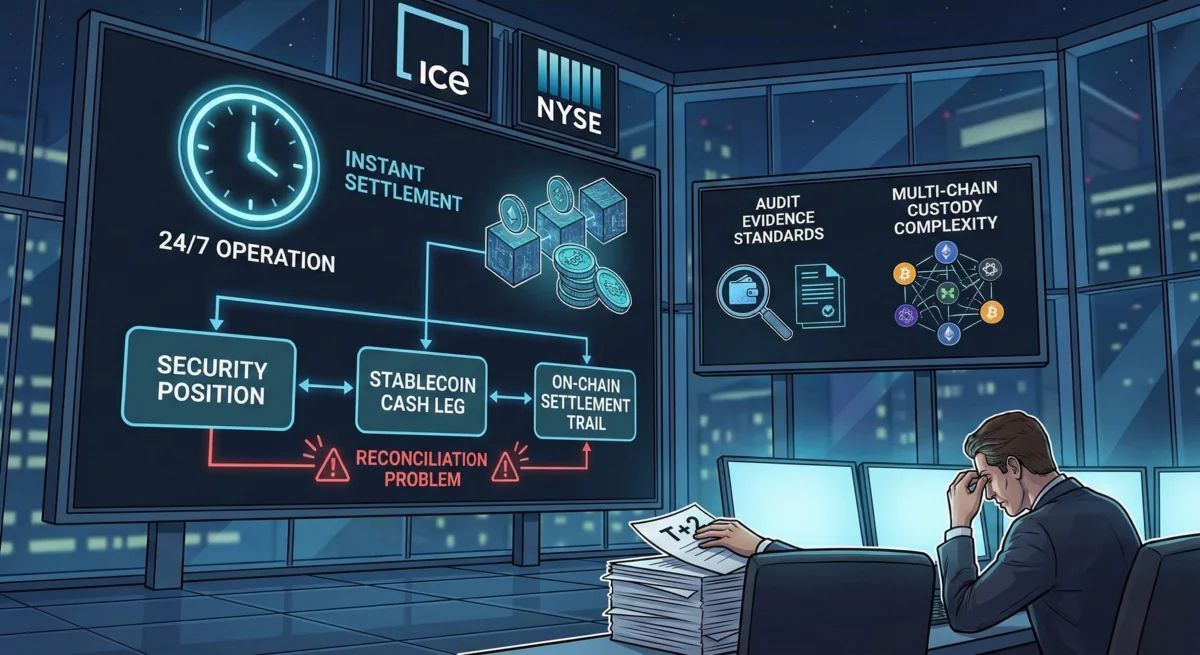

Digital asset adoption keeps moving from access into operations.

The practical question for institutions is not whether they can hold or move assets. It is whether wallet, custody, treasury, and accounting records reconcile into one defensible view.

That is the layer finance and audit teams eventually have to trust.

coinlaw.io/crypto-laws-resha…

1

30

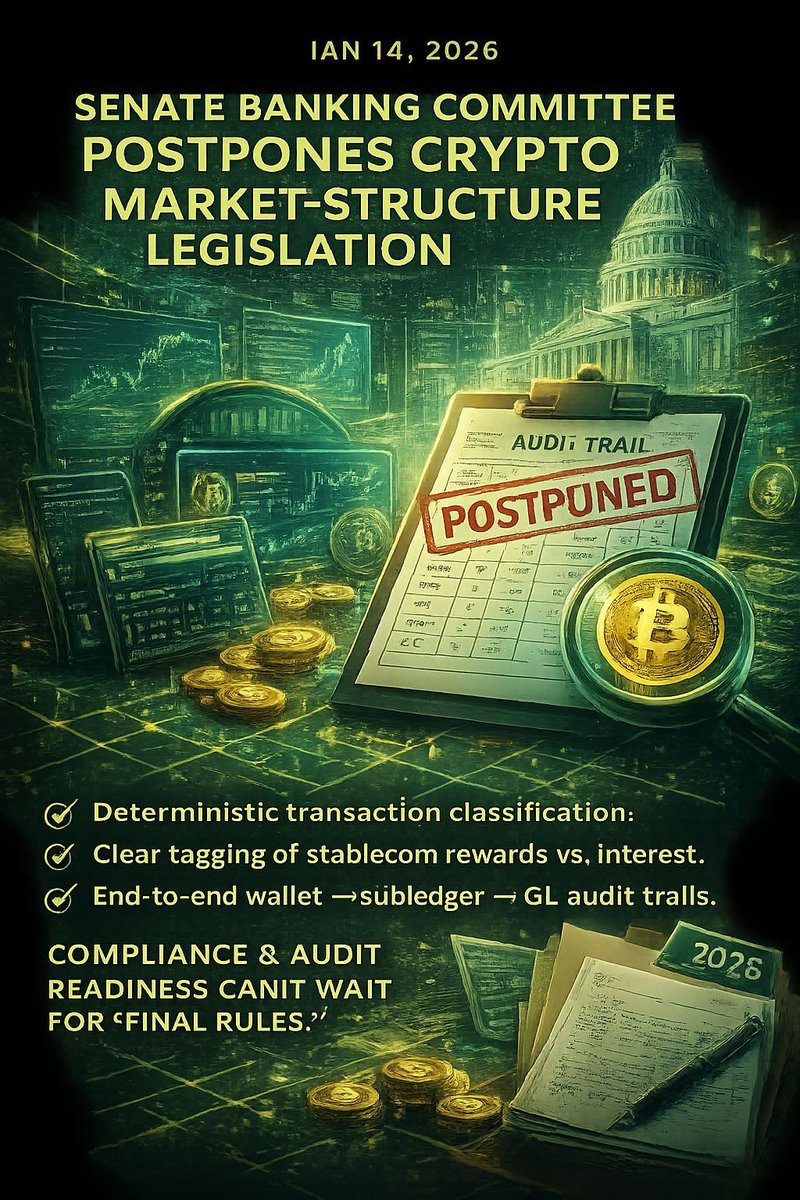

Audit readiness in 2026 is not a documentation problem. It is a controls problem.

Timestamped records. Approval trails. Transaction-level history that can answer an examiner's question without starting from a spreadsheet.

Firms with digital-asset exposure that rely on dashboard views are carrying a gap they have not measured yet. Dashboards show balances. Examiners need history. A subledger closes that gap. A dashboard does not.

investglass.com/how-financia…

3

20

FinCEN and OFAC closed public comments on GENIUS Act stablecoin AML requirements June 9.

For finance teams: stablecoin activity now carries the same examination readiness expectation as traditional bank rails. Books and records. Sanctions screening. Audit trail on every transaction.

That burden lands on whoever runs the subledger.

coinpaprika.com/news/fincen-…

1

2

112

Visa built a formal registry of AI agents authorized to initiate payments.

For accounting firms and treasury teams: a transaction initiated by an agent is still a transaction that needs to be classified, attributed, and reconciled.

The counterparty class changed. The records obligation did not.

usa.visa.com/about-visa/news…

1

13

Paradigm and Hyperliquid just filed a comment letter asking Treasury to narrow its stablecoin AML rule.

The industry argument: broad surveillance requirements make programmable money unworkable.

What that debate means operationally: granular transaction records are about to become a formal compliance requirement, not just an accounting preference.

en.cryptonomist.ch/2026/06/1…

1

14

Stablecoins moving into corporate and agentic payment workflows will create a records problem before most teams call it one.

Every payment rail still needs transaction purpose, counterparty context, wallet attribution, fees, and accounting treatment that survive review.

Faster settlement does not reduce the need for a defensible ledger. It raises the cost of not having one.

americanbar.org/groups/busin…

1

13

FASB is evaluating whether stablecoins qualify as cash equivalents.

The accounting question that matters more: does the classification outcome change what's required? Both treatments require defensible records, reconciled positions, and audit-ready subledger data.

The ruling arrives before most finance teams have the infrastructure to support it.

en.bitcoinhaber.net/new-cryp…

1

21

NODE40 retweeted

Jun 10

Introducing Holdfast: a non-custodial Solana stake manager for Chrome.

Every operation in the stake program. Activate, split, merge, deactivate, withdraw, transfer authority. Ledger, Keystone, and Trezor on day one.

Private beta opens soon → holdfast.valigator.tech/

5

2

9

392

Morgan Stanley clients can now lend SOL for ETF shares.

What that creates operationally: reward attribution across custodians, subledger reconciliation for positions moving between protocols, and audit records for a tax treatment that hasn't been fully settled.

The access problem is solved. The reporting infrastructure behind it is a different question.

morganstanley.com/press-rele…

2

28

Institutional custody options keep expanding. That is useful, but it is not the same thing as a complete control environment.

Once assets move across custodians, wallets, exchanges, funds, and treasury systems, the hard question becomes whether finance can reconcile the activity into one defensible record.

Custody solves safekeeping. Reporting still has to solve evidence.

transatlanticlaw.com/content…

12

IRS examiners auditing cryptocurrency accounts do not stop at the tax return. They pull cost-basis methodology consistency across the full transaction history, check for unreported foreign exchange holdings that trigger FBAR and Form 8938 obligations, and compare the return summary against underlying chain records.

A reconciled transaction history, traceable to the blockchain, is what survives examination. A tax software summary report is not that.

For accounting firms carrying clients with meaningful crypto exposure, this is the gap between what clients believe they have prepared and what an examiner is trained to ask for.

kugelmanlaw.com/blog/irs-cry…

2

29

The SEC's 2026-2030 strategic plan formally designates digital asset oversight as a regulatory priority. Coverage has focused on market access and price implications. The operational question matters more: which institutions have the reconciled transaction histories, defensible cost-basis methodology, and subledger infrastructure to satisfy an examiner when that oversight arrives in practice? The plan sets a timeline. The infrastructure either exists before the examiner asks for it or it does not.

1

15

The SEC's 2026-2030 strategic plan formally includes digital asset oversight as a regulatory priority. For institutional operators, this establishes a timeline -- not a thesis. Audit-ready transaction histories, reconciled subledger data, and defensible cost-basis methodology are moving from best practices to examination requirements. The accounting infrastructure needs to be in place before the examiner asks for it.

bitcoinmagazine.com/news/sec…

2

19

Institutional custody options keep expanding. That is useful, but it is not the same thing as a complete control environment.

Once assets move across custodians, wallets, exchanges, funds, and treasury systems, the hard question becomes whether finance can reconcile the activity into one defensible record.

Custody solves safekeeping. Reporting still has to solve evidence.

cryptobreaking.com/sec-strat…

2

17

The SEC's 2026-2030 plan calls crypto financial infrastructure and requires "consistent oversight" of staking services.

For validators, consistent oversight means an examiner needs to understand your reward attribution, not just your staking balance. Dashboard-only visibility does not pass that bar.

en.spaziocrypto.com/regulati…

1

20

Digital asset adoption keeps moving from access into operations.

The practical question for institutions is not whether they can hold or move assets. It is whether wallet, custody, treasury, and accounting records reconcile into one defensible view.

That is the layer finance and audit teams eventually have to trust.

coinmarketcap.com/cmc-ai/sol…

1

22

Schwab entering crypto custody for financial advisors expands institutional access significantly.

The accounting burden expands with it. Advisors managing client crypto positions need clean books, staking attribution, and audit-ready records across multiple accounts and chains. Custody does not provide that. The back-office gap is where firms get caught during audits and regulatory reviews.

thecurrencyanalytics.com/cry…

2

102

Goldman Sachs holds BSOL. Fidelity runs a Solana validator.

Both are generating staking rewards that have to flow through institutional accounting systems designed for equities and fixed income, not on-chain reward attribution.

Reconciliation at that scale requires more than a dashboard. The back-office infrastructure question for TradFi validator operations is not theoretical anymore.

1

47

FinCEN and OFAC just proposed exam-ready compliance requirements for stablecoin issuers. Public comment closes June 9.

This is not a payments story. It is a books-and-records, sanctions screening, and transaction-history story.

Any treasury team, accounting firm, or digital-asset company with stablecoin activity on the books should be asking right now whether their records could survive a regulatory examination, not just a routine audit.

1

54