Modeller at Cornwall Insight, all views are my own and do not reflect the position of my employer or the BSC panel.

Joined July 2011

- Tweets 7,168

- Following 464

- Followers 4,220

- Likes 227

1,224 Photos and videos

Pinned Tweet

26 Sep 2018

Energy Geek? Gamer? Ever wished these passions intersected? Check out the video demo below of my latest hobby project - a management simulator for operating a power network, PM me if your interested in getting a copy of the demo for play-testing!

youtube.com/watch?v=UPM98Qyg…

12

3

61

May 21

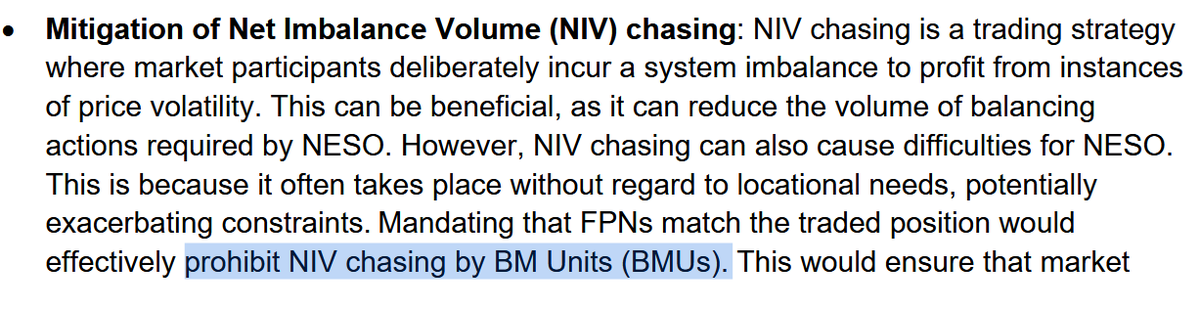

You can't prohibit something you can't do, if I have a BMU with a ve FPN Flag I can't NIV chase anyway.

1

1

187

May 21

This is NESO conflating trading with NIV chasing, which is two different things. If I signal a physical position (i.e. FPN of 100) and spill (i.e.ECVN of 0) then I get paid the imbalance price, but I still have told NESO an accurate FPN, so no re-dispatch needed.

2

146

Centrica completes acquisition of Severn Power 850MW CCGT from Calon Energy

centrica.com/media-centre/ne…

3

2

7

1,390

£370mn for 850MW is about £435/kW, which you could buy a new recip gas engine or most of a new OCGT for.

2

6

505

If we assume it has 10 years left (built in 2010) of CM payments left I think it would need £60/kW each year at an 85% de-rating factor to make back that £370mn. Which seems like a reasonably achievable outcome, with other revenues paying for Gas and Network charges. a

1

1

189

Apr 21

I know this is fruitless but I think we are agreeing here, Renewables are growing but they aren't going to displace gas entirely from the system by 2030, and my point is that breaking the link between gas and power prices is therefore difficult.

1

8

782

Apr 21

Also, where is the breaking of the link between gas and power? By the government own ambition gas will still be running in 50% of hours (generous reading 30% of the time?)

3

1

9

1,399

Apr 21

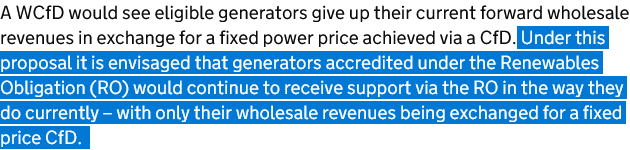

New GB wholesale mechanism being consulted on - the Wholesale CfD - RO genertors get to keep their ROCs, but exchange their current PPAs for a government backed one at a fixed price

2

1

3

569

Apr 21

Seems odd, as there would be little saving to the customer here, unless the generator accepted a WCfD with a haircut. A generator would be under a PPA with a discount to the day-ahead price, say 90%. So what discount would a generator be willing to accept for a longer agreement?

1

2

272

Apr 21

A ROC generator probably only has 15 years of useful life left, so the agreement length is probably around 10 years at least? We put the long-term PPA market for a index linked discount around 85% for a wind farm, so if thats where the market is offering the Govt has to be higher

1

250

Apr 20

What practical short-term options might exist for capping or de-linking gas from power prices? Three spring to mind from recent REMA discussions, converting RoCs to CfDs, iberian gas price caps and moving CCGT to a RAB model.

4

2

5

1,148

Apr 20

CCGT RAB: Make gas plant no-longer self dispatch, owners make gas plant available for NESO to dispatch at receive fixed payments. Doesn't necessarily remove gas price influence as other generators are well aware of what the gas cost is and when gas is running.

2

1

266

Apr 20

Also NESO has to step up a gas purchasing operation, what do you do with all the gas already bought by traders?

1

2

247

Apr 17

CPS is a tax on fuel at the gate, the £18/t duty is equivalent of £7-8/MWh based on the efficiency of the power station. As gas plant are normally the marginal fuel we would expect this to be reflected into a reduction in nearly all traded wholesale power products.

2

3

570

Apr 17

In markets dominated by Gas, or when nuclear output and renewables are lower, and demand higher we would expect to now increase our exports, and potentially increase our gas burn, reducing the overall impact of the measure.

1

144

Apr 17

Not to mention the gas price will come down by 2028 when this is implemented, so the impact would be much lower than if it were implemented immediately.

139