Founder and CEO Nutstuff | 30 Years of Writing and Investing | Market Expert | Trial nutstuff.co.uk/subscribe | t.me/nutstuff

Joined August 2021

- Tweets 1,345

- Following 531

- Followers 2,419

- Likes 750

234 Photos and videos

Pinned Tweet

5 Dec 2024

We all get so much news, much of it fake. It is, however, really all about the conclusion and the “so what”? especially if an investor. Nutstuffs 3x weekly is exactly this. I look at news, themes , stock ideas and off the wall issues, and there is no clutter with advertising. It is short and very readable. I aggregate, originate and then conclude. My aim is very simple: to make my readers; question, think, laugh and of course make money from the market and stock ideas.

1

3

3,165

May 25

IN THE NEXT FEW DAYS, 2 NUTSTUFF LIVE EVENTS.

1. Today is Bank Holiday Monday, 4.00 PM UK TIME. Nutstuff sits down “Live” with Raoul Pal:

Register here: luma.com/nf9fvwg0?_kx=1VXkSW…

2. Next Saturday, 30th May, 1 PM -5 PM: My old friend Piers Buckworth has put this 1-day event together in Mayfair. Nutstuff is one of the 3 Presenters/Hosts.

Register Here: eventbrite.co.uk/e/inside-th…

Get FREE 30 Day Trial: nutstuff.co.uk/

ALT Mastermind Interview: Will Nutting x Raoul Pal

227

May 11

The electorate is no longer choosing governments so much as hurling bricks at an entire political class it regards as useless, vain, self-serving and faintly ridiculous. Britain now feels like a decaying provincial department store staffed entirely by DEI officers and communications managers. At the same time, the escalators fail, the lights flicker, and someone is being stabbed in the car park. Keir Starmer, with all the charisma of a cancelled train announcement, has somehow become the perfect symbol of it.

Britain now feels less like a country with the political class remaining hypnotised by pronouns, “lived experience”, Net Zero sermonising, and whichever imported grievance is currently fashionable among middle managers in North London. This has all the hallmarks of late-imperial decay: too much debt, too little purpose, collapsing demographics and a governing elite which has spent so long marinating in taxpayer-funded abstraction that it no longer recognises reality when it crashes through the window carrying a machete.

4

269

Apr 23

👉 READ HERE: commonsensestocks01.substack…

In the glittering circus of an indebted, entitled, increasingly materialistic, and morally bankrupt USA, where the masses stay blissfully plugged into their glowing screens, puffing cannabis, and micro-dosing psychedelics like it’s the new national pastime, there’s a deliciously brutal irony at play: President Trump, with his signature blend of chaotic communication and unfiltered bravado, has thrown policy lifelines to both industries. Gosh, Nutstuff cannot think why!?

• Subscribe for more: commonsensestocks01.substack…

• FREE 30 Day Trial: nutstuff.co.uk/

• Get 40% Off: nutstuff.co.uk/pricing-plans…

• Disclaimer: nutstuff.co.uk/about/disclai…

ALT Puffing Weed & Micro-Dosing! Cannabis Rescheduling, the Psychedelics Boom & Stock Picks 2026

249

Mar 13

This Business Is About To Explode!

Click to watch the full video: commonsensestocks01.substack…

Subscribe here: commonsensestocks01.substack…

FREE 30 Day TRIAL: nutstuff.co.uk/

Disclaimer: nutstuff.co.uk/about/disclai…

1

422

Mar 5

Reminder: Inside the Investment Minds: Macro, Markets & Opportunity

📅 TODAY 16:00 UK [11:00 EST]

Raoul Pal (Real Vision), Nick Finegold (The Fat Gladiator) and Will Nutting (Nutstuff) will share their views on the macro landscape, market positioning and where the next opportunities may lie.

This will be an open discussion, members are encouraged to contribute directly and engage in the conversation in real time.

Given recent market turmoil, the timing couldn’t be more relevant.

Expect a candid exchange between three investors who think independently and aren’t afraid to challenge consensus.

👉 Register: luma.com/xq3o2pxi

1

1

284

Mar 2

As Iran-West tensions escalate, Nutstuff’s Will Nutting breaks down the "Unknown Unknowns" facing the Middle East. From Brent Oil hitting $90 to a potential "run on Dubai," here is how to position your portfolio for a multipolar world.

WATCH HERE: commonsensestocks01.substack…

Subscribe to get more investment insights: commonsensestocks01.substack…

Nutstuff Portfolio: nutstuff.co.uk/subscribe

Disclaimer: nutstuff.co.uk/about/disclai…

ALT Nuttuff springs to life in Switzerland, featuring dynamic scenes and engaging moments against stunning backdrops.

1

443

Feb 25

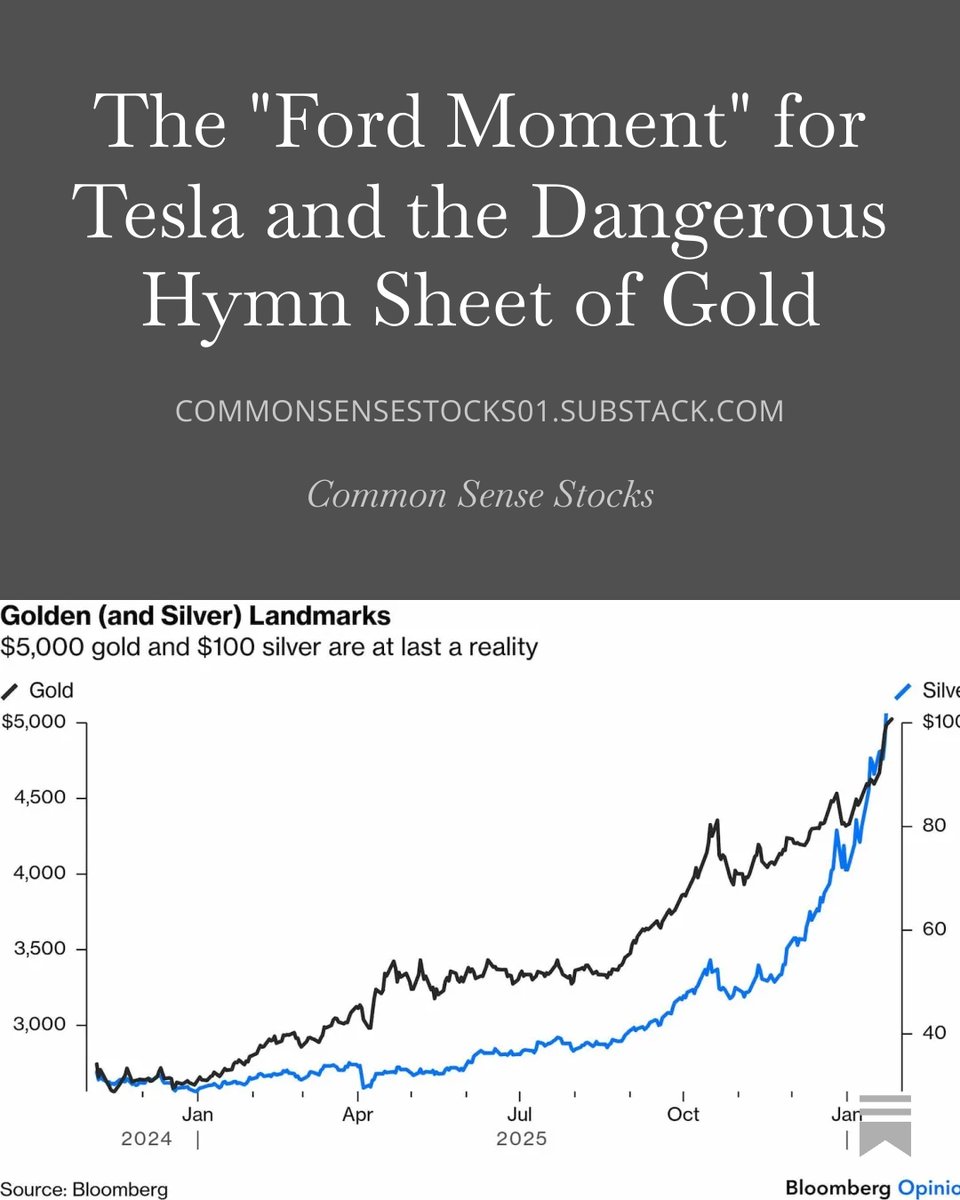

AN OBSERVATION - GOLD MINERS: Are arguably still priced for $2,000 gold. GDX trades at roughly the same multiple it did two years ago, despite gold running from $2,000 to $5,000 . If even a fraction of this revaluation thesis plays out, it is the miners have the most operational leverage.

3

623

Feb 20

Let’s talk about Helium ($HNT). 📡

It’s up 65% off the lows. Why? Because it’s no longer a "crypto experiment."

Today, 3.4M users connected to Helium. 1M added in the last month.

That is roughly 1 in every 100 Americans using the network without even knowing it.

READ HERE: commonsensestocks01.substack…

Disclaimer: nutstuff.co.uk/about/disclai…

FREE 30 Day Trial: nutstuff.co.uk/

ALT Illustration explaining the agent economy and the differences in infrastructure needs.

1

317

Feb 18

Why energy and logistics beat apparent dominance.

Click to watch the full video: commonsensestocks01.substack…

Subscribe: commonsensestocks01.substack…

Disclaimer: nutstuff.co.uk/about/disclai…

2

428

Feb 9

RIG buying VALARIS!

Honestly this deal is not a one-off curiosity; it is absolutely the template for how capital reallocates when constraint finally ‘trumps’ narrative. Nutstuff went through this entire rationale this morning. Offshore drillers have survived a decade of starvation, wrote off balance sheets, scrapped fleets and outlasted the ESG purge and are now finally discovering that scarcity has a price. A $5.8bn all-stock take-out is not a cyclical top signal but a simple reset of terminal value: public markets were still pricing decline while corporate buyers are underwriting permanence. Transocean, Noble and Seadrill still trade on optically cautious multiples despite replacement costs and forward cash flows that private buyers already capitalise at materially higher rates. The same mispricing runs through offshore services and OSVs, specialty shipping, and yes even coal ( see thoughts earlier!), all where listed equities sit on 2–3× cash flow while private capital quietly assumes terminal value and harvests yield. I’d own these assets not because they are fashionable, but simply because they are real and cannot be replaced. This is not really a bet on oil prices ( clearly not in 2026! ) or on macro heroics; it is simple arithmetic. When public multiples imply extinction and take-out multiples imply some value of infrastructure, I salivate!

11

993

Jan 30

Read and Subscribe: commonsensestocks01.substack…

Get Free 30 day trial: nutstuff.co.uk

Disclaimer: nutstuff.co.uk/disclaimer

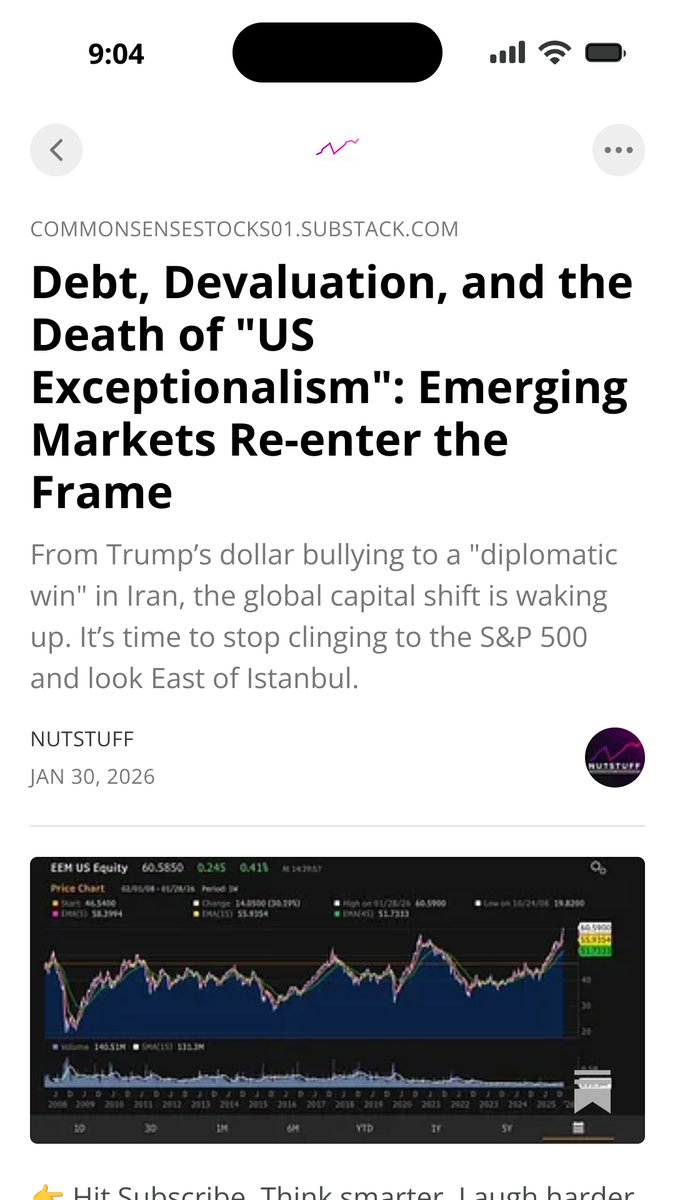

ALT Debt, Devaluation, and the Death of "US Exceptionalism": Emerging Markets Re-enter the Frame

297

Jan 26

Read and Subscribe: commonsensestocks01.substack…

Get Free 30 day trial: nutstuff.co.uk/

Disclaimer: nutstuff.co.uk/disclaimer

343

Jan 22

Nutstuff in Daily Mail on Why Now it might be time for Bitcoin. mol.im/a/15485953

Early comments show few Mail readers are buying it!

The lack of even basic understanding of what it is amazes still:

Herewith some education for a Central Banker from Brian @COINBASE.

x.com/birdfiip/status/201395…

Brian sounds like a Bitcoin Maximalist, but offers Fartcoin on his exchange — it’s impossible to be taken seriously when 99% of what you sell is a joke.

If he were a serious person, @coinbase would be Bitcoin only.

447

Jan 13

“How about Bitcoin with a seatbelt?!”

Well done Charlie Morris at Byte tree.

BOLD just launched in UK!🇬🇧

Yes, think of BOLD as Bitcoin with a seatbelt. Instead of raw exposure to crypto’s volatility, it pairs Bitcoin with Gold and forces monthly discipline trimming what’s run hot, topping up what’s been left behind. Analogically same destination, fewer crashes. Since 2022 it’s quietly delivered Bitcoin-like returns with Gold-like nerves, using volatility-weighting rather than gut feel.

Ask Why it matters? Well, in a world of expanding money supply, debt-soaked governments and financial repression, scarce assets win but timing kills most investors.

BOLD automates the hard bit.

What to buy: 21Shares Bitcoin & Gold ETP (BOLD in GBP, BOLU in USD) on the LSE. How to buy: any UK investment platform, intraday like a share.

In a world of monetary debasement, think of it as owning the engine (Bitcoin) and the shock absorbers (Gold) in one vehicle built to go the distance without throwing you through the windscreen!

1

342

12 Dec 2025

On Marijuana/ Cannabis: Nutstuff has had this contrarian ve call for 2yrs! Trump it seems now is resolute on de-classifying marijuana. This is the biggest policy change since 1970! My horse is WEED/ GLASF US but feel sure MSOS US ETF might fly (dead man’s heart-beat chart see below, 31% pre-open!)

washingtonpost.com/business/…

On GLASF:The longer the spring coils, the more energy should be released as the industry matures under overbearing regulation. Glass House Brands is my biggest exposure in the space and from end ‘23 entry has been beyond dull. The underlying business is however on fire. As they grow; costs are lowest in industry; $100/lb and so operating cash flow really inflects higher (over the next 12m) and the company will have a handful of avenues it can progress down. Further if they pursue hemp production in the future, or we see more on legalisation and that elusive NYSE (most likely) this could arguably become a $20-$30 stock in short order.

1

424

8 Dec 2025

Why Digital Assets Are Leading the Financial Market Recovery and What High-Conviction Investment Decisions Come Next.

Listen here: commonsensestocks01.substack…

Subscribe: commonsensestocks01.substack…

FREE 3O Day Trial: shorturl.at/KDpHkAccess Past Newsletters - nutstuff.co.uk/sample

*Disclaimer: nutstuff.co.uk/disclaimer

314

8 Dec 2025

As markets brace for gloom, the numbers say otherwise, here’s why Britain’s macro fundamentals still deliver. Read here: commonsensestocks01.substack…

FREE 3O Day Trial: shorturl.at/KDpHk

Access Past Newsletters - nutstuff.co.uk/sample

*Disclaimer: nutstuff.co.uk/disclaimer

ALT Why Britain’s Economic Collapse Meme Is Wrong — Contrarian Case for a UK Rebound

364

1 Dec 2025

Honestly the market chatter around MSTR today is a perfect case study in how psychological resentment gets misdiagnosed as liquidity analysis: Michael Saylor has put his head so far above the parapet that a whole constituency in markets is desperate to see him fall the brilliant overachiever who somehow dodged being “bog-washed” and never learned the social lesson that you’re meant to keep your ambition quiet; much of the hostility isn’t however really analytical, in fact most of the analysis is dire, and simply emotional, because every time Bitcoin survives another cycle his critics are forced to confront the possibility that he simply understood the monetary transition earlier than they did.

So here’s facts……

Sign up!!!

438

1 Dec 2025

Sorry not tweeting much.

nutstuff.co.uk sign up for a Black Friday deal! BUT this is worthy of a tweet..

Cardiol Therapeutics / CRDL US : The Two-Year Buy Case.

Why Nutstuff stayed in the trade and why the risk/reward is now better than at any point since 2023.

For more than two years Cardiol has been the quintessential Nutstuff position: unfashionable, under-owned, scientifically coherent, and completely mispriced. Through 2023–24 the market dismissed Cardiol as “a cannabidiol story” and priced it accordingly as if it were yet another wellness derivative. But that was always the misunderstanding. Cardiol was never about cannabis; it was about cardiac anti-inflammatory biology, and the company now has two human datasets proving that point. The new ARCHER read-out, a statistically significant reduction in left-ventricular mass of –9.2 g (p=0.0117), supported by coherent improvements across extracellular volume, intracellular volume, atrial size and ventricular filling is the moment the thesis crystallises. This is structural remodelling in human myocarditis, a feat achieved by only a microscopic handful of small-cap biotechs in the last decade. It confirms what anyone who has held the stock for two years already believed: the mechanism works in heart tissue, not just in symptomatic pericarditis. Importantly, owning Cardiol through the grind meant watching the company do the one thing retail biotechs almost never do: run clean studies with clean safety, build a methodical clinical stack, and preserve balance-sheet runway into 3Q27 even while market cap fell towards $100m. The HCW note just published ( I have!) makes the point explicitly: the market is assigning “little to no value” to ARCHER despite the fact it de-risks recurrent pericarditis, upgrades confidence in CRD-38, and gives Cardiol a “translational bridge” into the heart-failure arena where LV mass is a validated prognostic marker . If you own Cardiol, this is precisely the moment you were waiting for. And CRD-38 is where the multi-bagger lives. The injectable formulation is built for HFpEF, a multi-billion market starved of effective anti-inflammatory solutions, dominated by majors who would rather partner or acquire than spend ten years building a mechanistic competitor from basic research. ARCHER’s structural data is the currency those majors require. The biology is now contiguous across myocarditis, pericarditis, cardiomyopathies and the inflammatory component of HFpEF. Few sub-$200 million companies ever get this far. Two years of owning Cardiol has taught me one key lesson: the market waits for forced proof not stories, not mechanisms, not animal data but visible, MRI-confirmed remodelling of human heart tissue. Cardiol now has that. At $1 the stock trades below cash-adjusted rNPV, below any rational valuation for a company with two validated cardiac signals, and far below HCW’s and likely others’ $9 target, which itself uses conservative probabilities (20% myocarditis, 10% heart failure) and a 13.4% WACC . It is as asymmetric a setup as exists in small-cap biotech: limited downside after two years of derating, but explosive optionality if CRD-38 enters partnered development in HF. In short: holding Cardiol for two years was the price of admission. ARCHER is the payoff. The roadmap is now industrial rather than speculative, the mechanism is validated, and the valuation is absurd relative to the platform. If you liked it at $2 in 2023, you should love it at $1 with structural cardiac MRI data in hand. Cardiol is finally what we always said it was: a real cardiology company trading at a cosmetic-product valuation!

4

494