55 Photos and videos

OmxBerry retweeted

May 19

💰 13F filings just dropped!

What was Wall Street buying in Q1?

🧱 AI moved down the stack.

☁️ Software was still on probation.

⚡ Physical infrastructure stood out.

🏎️ Formula 1 wasn't on our bingo card.

Full breakdown 👇

appeconomyinsights.com/p/wal…

3

21

13,079

OmxBerry retweeted

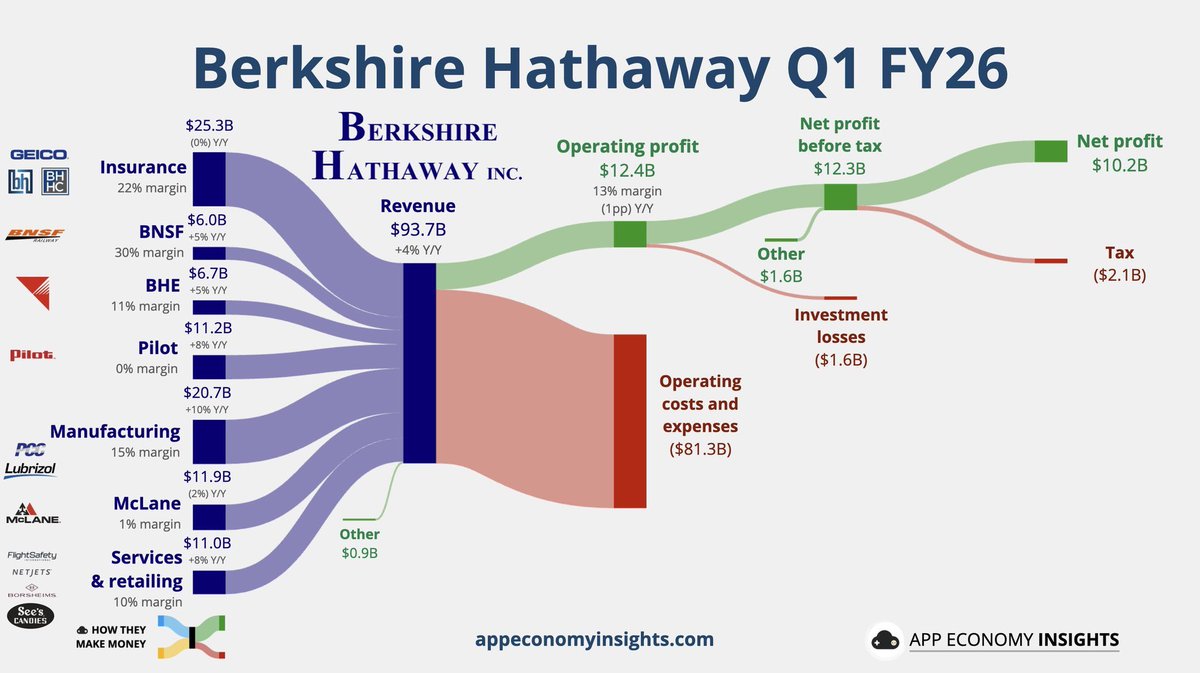

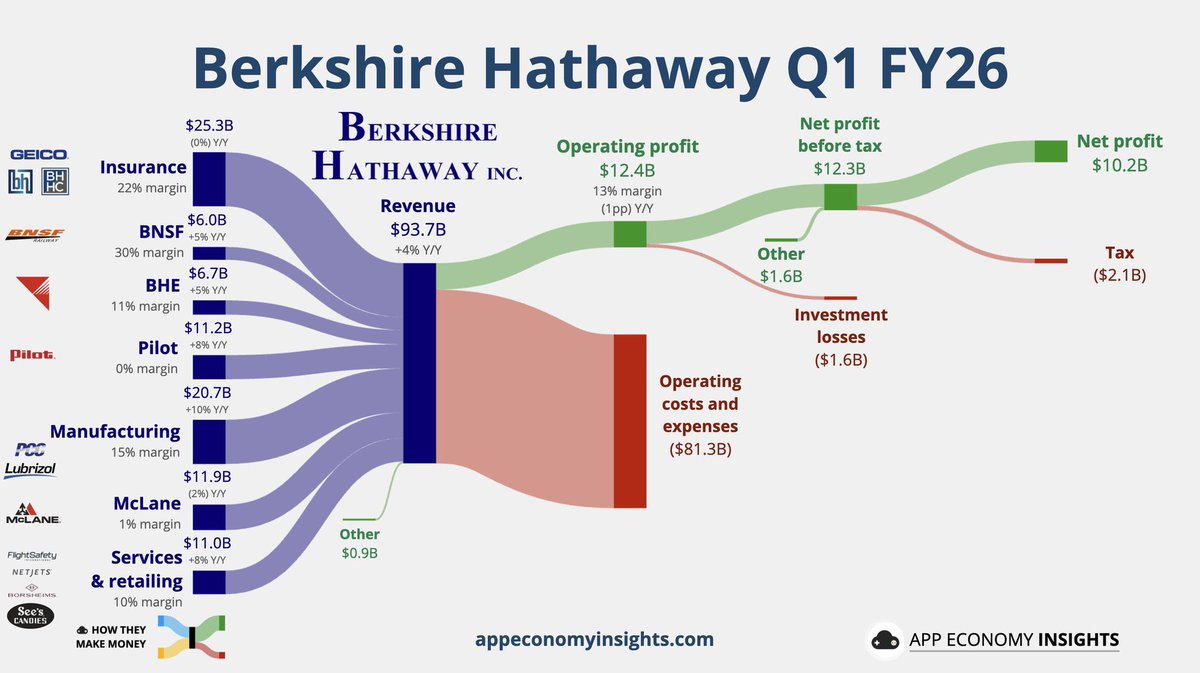

My thoughts on $BRK

People overcomplicate $BRK because they try to value every piece perfectly down to the decimal. They debate price to book, intrinsic value formulas, and build giant spreadsheets modeling every subsidiary. Meanwhile I look at it much more simply. $BRK has roughly $400b in cash and around $300b in stocks.

That’s about $700b right there between cash and equities alone. So when the company is worth around $1t, you’re basically paying roughly $300b for everything else. That includes the railroad, the energy business, insurance operations, manufacturing, distribution, service businesses, and one of the greatest collections of operating assets ever assembled.

And honestly I think people massively underestimate the value of the insurance float. The float is one of the greatest financial assets ever created because $BRK gets access to enormous amounts of capital at extremely attractive economics. Most people do not fully understand how powerful that becomes over decades. That float has quietly fueled one of the greatest compounding machines in financial history.

But the part that fascinates me most is the discipline. Almost every CEO on earth would have cracked by now sitting on $400b of cash. Most management teams would feel pressure to force acquisitions just to appear active. $BRK has basically said if we cannot find something intelligent to buy at scale, we are willing to wait.

People look at the cash and think it’s dead money, but optionality matters. $BRK effectively owns a giant call option on future chaos. When markets panic and liquidity disappears, $BRK becomes one of the only entities on earth capable of writing enormous checks instantly without relying on financing markets. That is a huge strategic advantage.

The other thing people miss is how rare true permanence is in capitalism. Most corporations optimize for optics. CEOs rotate, incentives change, cultures decay, and strategies constantly shift depending on sentiment. $BRK was built differently.

It was designed almost like an anti Wall Street structure where long term thinking itself became the competitive advantage. In many ways that culture may end up being Buffett’s greatest creation, even bigger than the stock portfolio itself. A lot of companies talk about long term thinking. $BRK actually structured the organization around it.

I also think people misunderstand what $BRK really is. They think it’s just “an insurance company that owns stocks.” But $BRK is basically a giant ecosystem of real world economic activity. Railroads, energy infrastructure, manufacturing, freight movement, insurance, distribution, consumer spending, and financial assets all under one umbrella.

In many ways it’s almost like owning a miniature version of the American economy. But unlike an index fund, the capital allocation is centralized under highly disciplined operators. You get diversification without complete chaos along with durability, liquidity, tax efficiency, reinvestment flexibility, and world class balance sheet.

And honestly the most underrated asset may simply be trust. If $BRK calls during a crisis, people pick up the phone. If $BRK wants to buy a family owned business, sellers trust the company will preserve the culture and operate responsibly.

I also think people are underestimating Greg Abel. Nobody is Warren Buffett and nobody ever will be, but that doesn’t mean $BRK suddenly stops being $BRK. Greg already understands the culture, operational discipline, and capital allocation philosophy better than almost anyone alive.

That’s why $BRK almost a forever asset or a savings account on steroids. No, it’s not going to triple overnight and no, it’s not some hyper growth AI stock. But when I look at over $700b between cash and equities, elite operating businesses, insurance float, fortress balance sheet strength, world class reputation, and disciplined reinvestment talent, I have a hard time viewing it as expensive.

🌹

78

105

883

74,216

OmxBerry retweeted

Det sista du ser innan du får;

Höjd skatt på ISK

Ökad kostnad för ditt bolån

Ökad invandring

Mildare straff

Höjda bidrag

Höjt bistånd

Högre bränslepriser

Förmögenhetsskatt

Höjd fastighetsskatt

(För att nämna några saker som partierna på bild vill åstadkomma efter valet)

61

327

1,691

29,146

Yes $MKL start buying back shares please.

prnewswire.com/news-releases…

275

Snittpriset för olja har legat över $100 i snart 2 månader och marknaden har helt stoppat huvudet i sanden #finanstwitter

1

118

Marknaden väljer att stoppa huvudet i sanden ..

BREAKING: The European Union has now spent an additional $32 billion on fossil fuel imports since the Iran War began.

The IEA is now calling the situation the biggest energy security threat in history.

69

OmxBerry retweeted

Apr 18

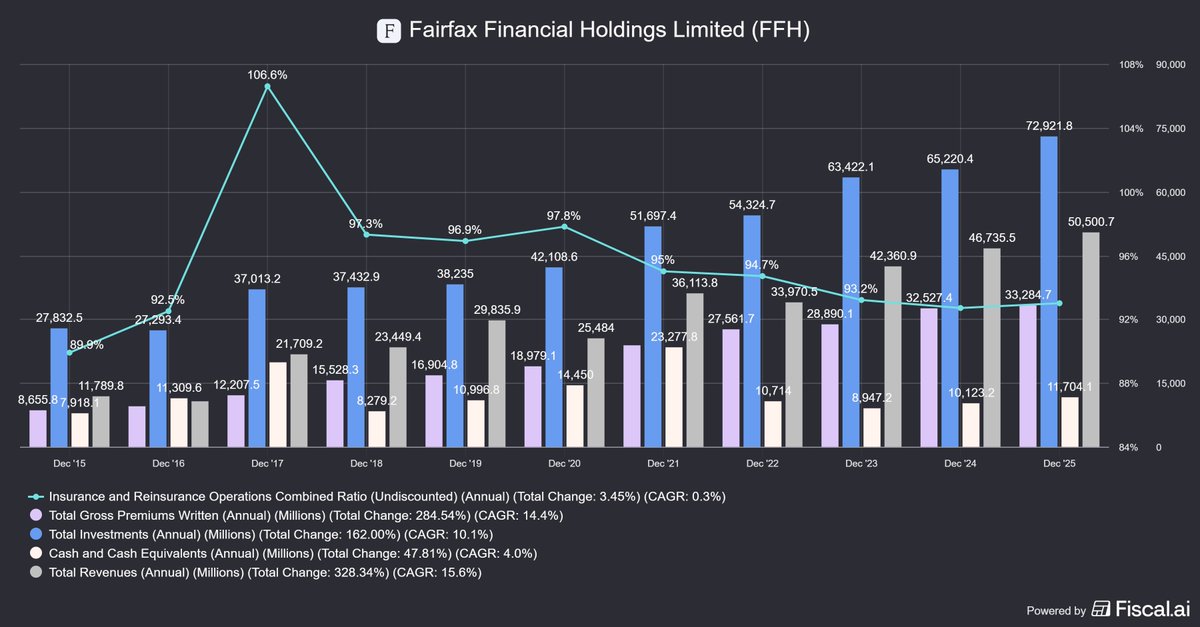

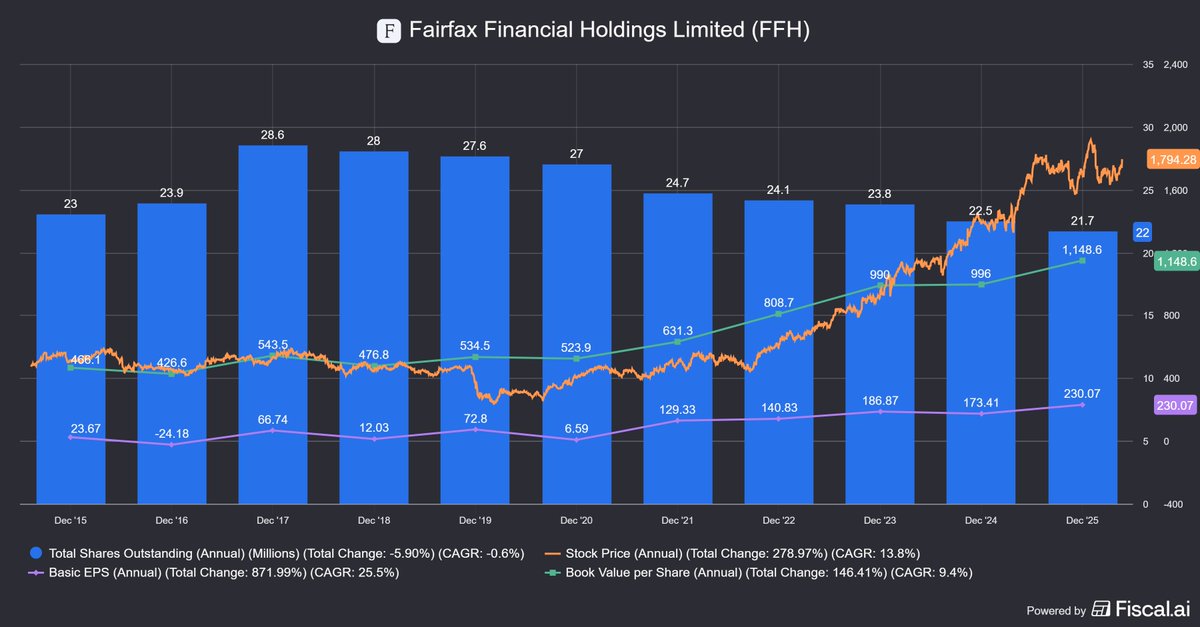

A study on Fairfax Financial - the $55 Billion company no one knows anything about. ↓↓↓

With a stock price that has surged ~700% from COVID lows, here are some key metrics:

- P/B: 1.5x

- Consolidated combined ratio (2025): 93%

- ROE: 17.8%

$FFH since 2015 has:

- revenue growth at a 15.7% CAGR

- grown total gross premiums written EVERY year at a 14.4% CAGR

- profit margin growth of 13% since 2017 (high of 106.6%)

- grown total investments amount to $73 billion at a CAGR of 10.10%

- grown total cash & equivalents to $11.7 billion at a CAGR of 3.98%

Not to mention an aggressive share buyback program (25% less shares outstanding now than in 2017 when they began, at a CAGR of -3.4%), and rapidly growing earnings per share (25.5% since 2015) and book value per share (9.4% CAGR since 2015).

Where exactly does this money come from?

Well they own things. A lot of them.

To start, their core insurance business which generates most of their revenue and their combined ratio's for 2025:

(89%) Northbridge

(95%) Crum & Forster

(102%) Zenith

(94%) Odyssey Group

(89%) Allied World

(93%) Brit

(96%) Ki

(94%) International Re/Insurers

(96%) Gulf Insurance

For a consolidated combined ratio of 93%, or 88% excluding catastrophe losses. Very profitable.

They also own major stakes in a basket of non-insurance businesses such as:

- Recipe Unlimited (i.e. Swiss Chalet, Harvey's etc)

- Under Armour

- Sleep Country

- Sporting Life

- Golf Town

- CVS

- The Keg

- among many others

Fairfax stands for "fair and friendly acquisitions".

From day one, they’ve operated as value investors:

- Buy undervalued assets

- Fix what’s broken

- Let great operators run the business

They began by buying troubled insurance company's and turning them profitable, albeit through a decentralized structure which makes them very unique.

With over 60,000 employees at its subsidiaries and just a fraction working at the actual holding company, Fairfax allows the company's it buys a certain degree of autonomy and self-governance, aside from major decisions where consulting with Fairfax takes place.

This generates the float with which Fairfax so successfully invests and earns additional returns.

Though they had and continue to have many successful investments, they are most well know for shorting the housing market in 2008, and making in excess of $4.5 US Billion. For reference, Michael Burry made ~ $700 million.

What set Fairfax apart and will continues to in the future is their attitude in business.

They believe in fair and friendly business activities and acquisitions, where day to day operators and employees take ownership and therefore think like owners.

They believe in honesty. Prem was always very open about financial results even during many of their bleak periods, to the contrary would often actually highlight poor performance.

And they believe in giving back. Recently they committed to doubling their pre-tax donations from 1% to 2%, supporting various charitable causes and scholarships, covered in an annual corporate responsibility report.

"Doing good by doing well."

It is not hard to see how $FFH got to where it was after 40 years of honest, fair and patient business.

6

3

40

8,952

OmxBerry retweeted

Regeringen har skattebefriat de första 300 000 kr man sparar på ISK. MP & V vill sänka det till 50 000 kr och S vill höja skatten på ISK för dem som sparar mycket. Låt oss hålla vänstergänget borta från makten och stoppa deras planer på att ta mer av andra människors besparingar.

82

396

3,104

99,413

OmxBerry retweeted

Apr 14

Sverige ska vara ett skatteparadis för företagare och vanliga arbetare. Det vill vi från MUF att Moderaterna ger i vallöfte.

Det innehåller 5000kr sänkt skatt i månaden för vanliga arbetare, avskaffad statlig inkomstskatt och sänkt bolagsskatt!

di.se/mobil/debatt/muf-vi-kr…

37

12

189

7,699

BREAKING: Iran’s President Pezeshkian releases a statement threatening to back out of the ceasefire agreement:

“The repeated aggression by [Israel] against Lebanon is a flagrant violation of the initial ceasefire agreement and a dangerous indicator of deceit and lack of commitment to potential accords. The continuation of these aggressions will render negotiations meaningless; our hands will remain on the trigger, and Iran will never abandon its Lebanese brothers and sisters,” he says.

84

OmxBerry retweeted

Apr 8

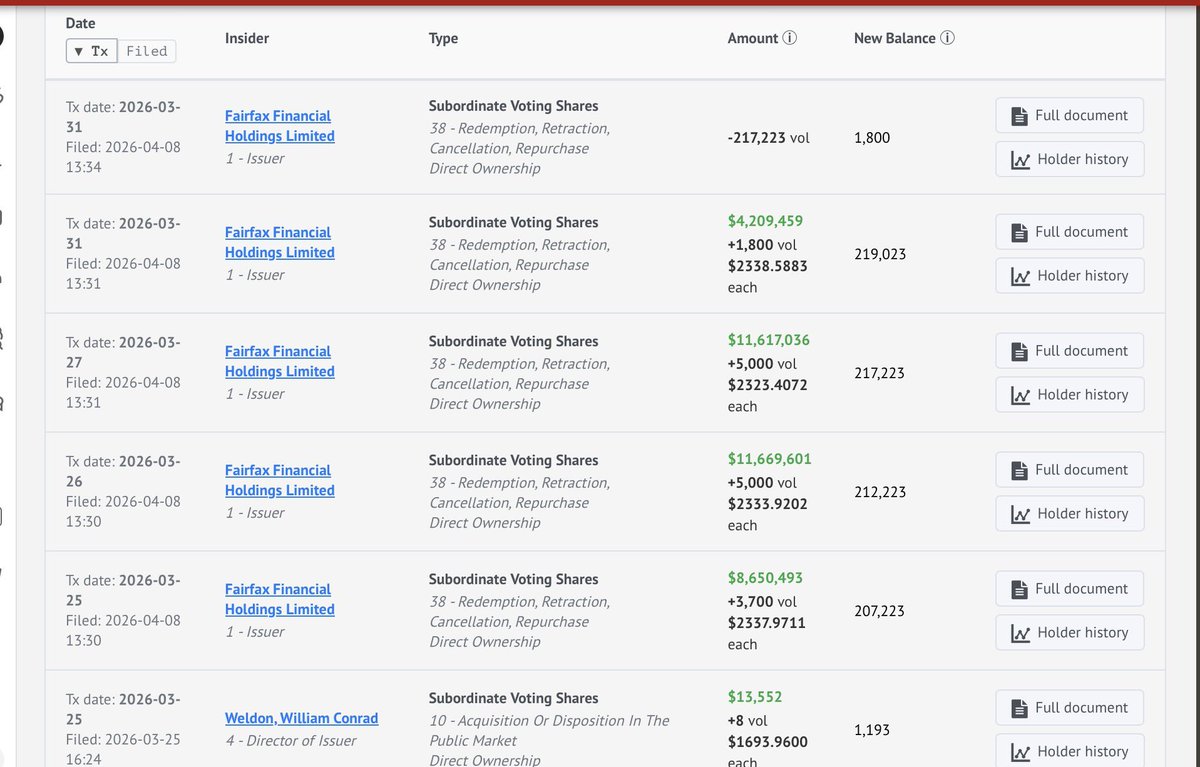

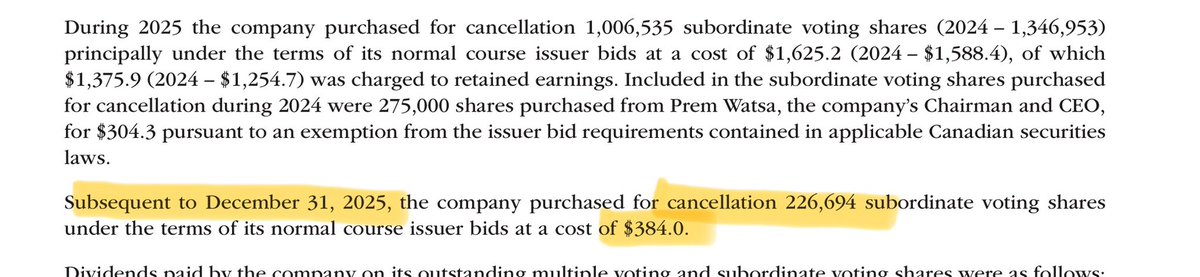

$FFH.TO bought and cancelled more shares in March than January and February combined. Over 1% of shares outstanding.

Mar 9

$FFH.TO disclosed in the AR that it bought back ~227k shares in 2026 so far, meaning that it bought almost 60k shares in the first week of March as Jan and Feb have been filed already.

Hat tip to @CroweTarn for catching it and sharing it on CoBF.

11

7

90

15,679

OmxBerry retweeted

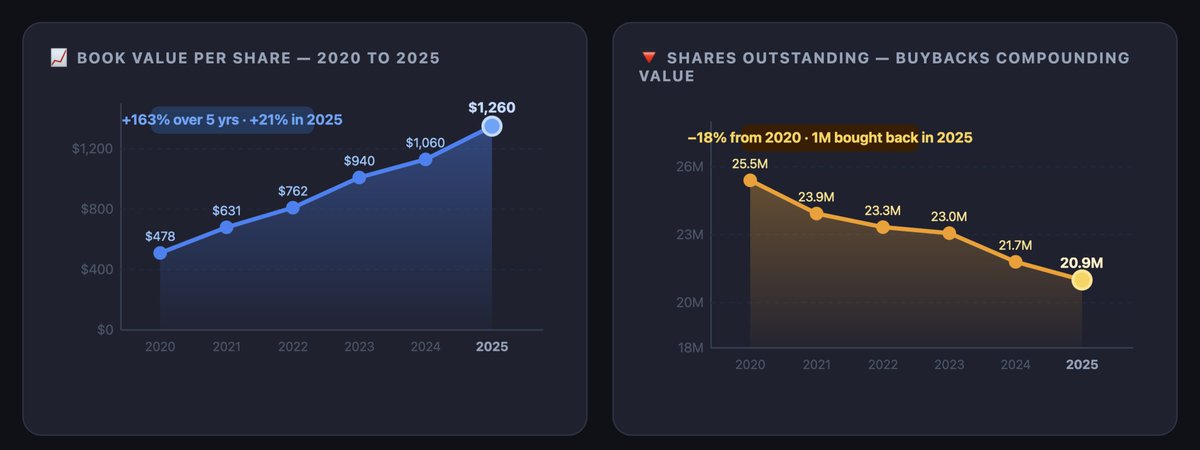

Apr 6

Fairfax Financial in two graphs:

160% BVPS Growth while 20% less shares outstanding. $FFH.TO

2

8

42

7,918

OmxBerry retweeted

Apr 2

Europe is on a path to destroying itself.

Unchecked immigration of millions of immigrants that burden their welfare states, bring violence and terrorism to their shores, and take over local governance, one city at a time.

Anti-capitalist policies that make it difficult for businesses to adapt their workforces to a rapidly changing competitive environment now accelerating due to AI.

A business environment and tax regime that is antithetical to startups.

The absence of any progress or innovation in AI and limited access to the compute necessary to compete.

Energy dependence due to the green movement at a moment when energy demands are rapidly increasing.

And now, the abandonment of the U.S. when we have asked for limited assistance — base access and flyover rights — in the midst of our efforts to eliminate Iran’s nuclear and ballistic threat which is already within striking range of Europe, after we have invested nearly $200 billion in helping Ukraine.

NATO is about to be toast. Europe’s defense burden is about to rise massively while their economies continue to fall further and further behind.

In short, Europe needs to wake up before it is too late, and it may very well be too late.

Apr 2

An important read on Europe and NATO.

2,311

3,337

19,595

2,327,820

OmxBerry retweeted

Mar 31

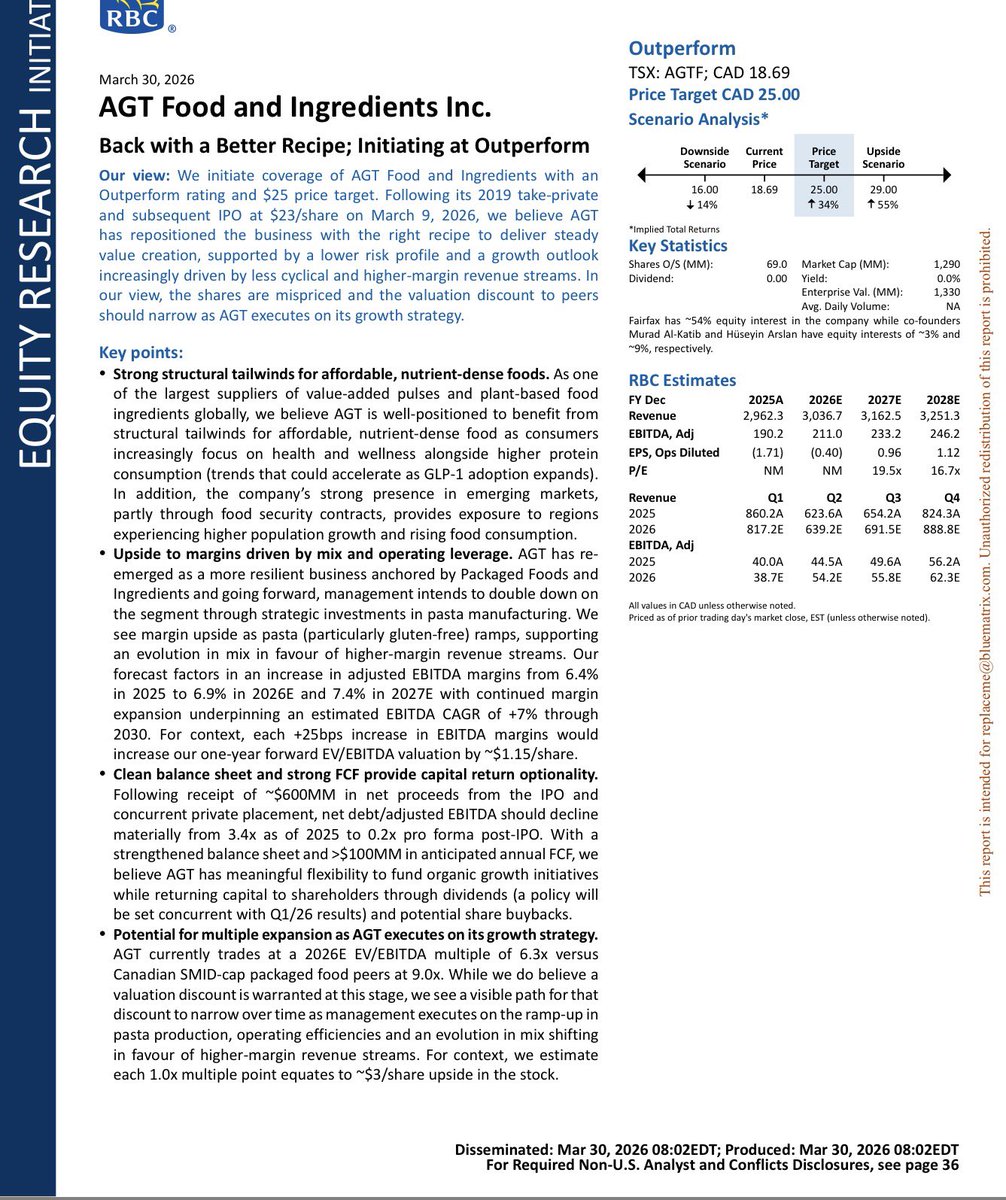

RBC initiates on $AGTF.TO with an Outperform and C$25 price target.

1

1

3

706

OmxBerry retweeted

Mar 15

Ät på Max i Gävle om ni har vägarna förbi, bra gjort av Maria Lindstedt, alla kan begå misstag. @maxburgers_se hoppas ni tar hand om folket som får utstå denna ovärdiga rapportering.

Förväntar mig att SVT reportern Rikard Berglin får sparken och folket bakom får sig en varning.

124

314

3,767

181,929