Oneassure simplifies decision making while buying an #insurance policy. Consult our advisors for 100% unbiased recommendations

Joined April 2020

- Tweets 438

- Following 12

- Followers 452

- Likes 213

175 Photos and videos

OneAssure retweeted

Even if you have health insurance, there’s a high chance you’re underinsured.

Comment below and I’ll review your policy for free!

6

3

13

3,634

OneAssure retweeted

Hi Twitter!

Thought of introducing myself here.

I’ve helped 2k families secure their future @OneAssure. Most people are overpaying for the wrong cover, I’m here to fix that.

Expect:

- Unbiased, no BS advice

- Industry truths

- How to actually get your claims paid

1

4

2,388

Jan 14

Our founder, @ruchirkanakia is speaking at one of the biggest personal finance summits in the country. NFP National.

Very proud to be the only insurance platform in the room.

Let’s build what actually moves the ecosystem forward.

1

3

1,762

OneAssure retweeted

1 Dec 2025

If you could ask only one question to your insurance agent, you should ask

"What is the single most common reason claims are denied on this specific policy?”

This question is your ultimate test.

If the agent gives a straight answer, great.

If they avoid the question, or worse go silent then walk away. Never pay for a policy that won't pay you back.

3

11

1,409

OneAssure retweeted

19 Nov 2025

Why most life insurance policies don’t actually protect families?

Term insurance is often sold as peace of mind.

But for most Indian families, it ends up being a false sense of security.

Here are the 3 reasons why:

1. Most people are underinsured.

They take a ₹25–50 lakh cover when their family actually needs ₹1 crore or more to replace income and sustain expenses for years.

2. Investment-linked plans are mistaken for protection.

Endowment and money-back policies sound attractive because they offer returns but they dilute the real purpose of insurance: income replacement.

3. Advice is rarely data-driven.

Policies are sold emotionally, not scientifically. Very few people calculate how much cover their dependents truly need.

The result? When something happens, the payout is far too little to secure the family’s lifestyle or goals.

The truth is that over 90% of life insurance in India doesn’t serve its real purpose, protecting the family’s financial future.

So what’s the fix?

1. Start with a needs-based calculation at least 10–15× your annual income.

2. Choose pure term insurance (no investment component).

3. Review your cover every few years as your income and responsibilities grow.

1

7

985

OneAssure retweeted

9 Sep 2025

The best way to judge an insurance advisor isn’t by how smoothly they sell you a policy because that’s just paperwork. The real test is how they show up during a claim, when stress is highest and support matters most. I’m proud that most of Google reviews on @OneAssure talk about claim settlement, not just the buying experience because that’s where real value is delivered.

1

6

1,102

OneAssure retweeted

12 Aug 2025

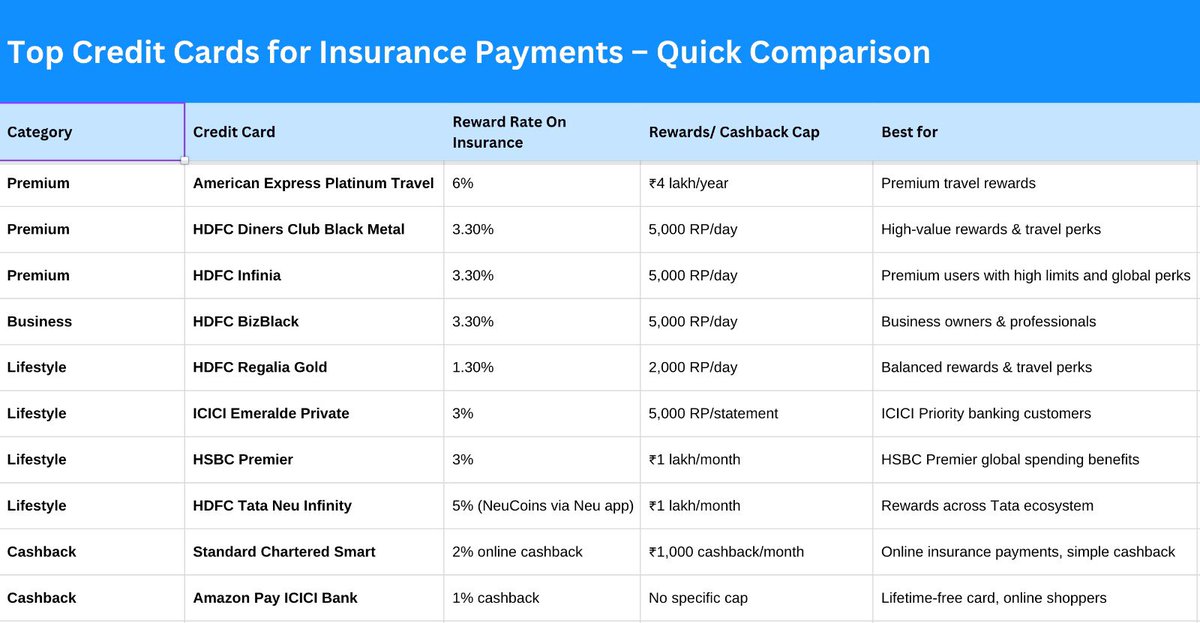

Not all #creditcard give reward points on insurance premium payments.

A few exceptions are as follows, something you should look out for:

1

2

8

922

OneAssure retweeted

2 Aug 2025

Medical Insurance - CASE SOLVED

Last week, I posted a bitter post on the opaqueness of Medical Insurance (India) and how my family's premiums shot up by 50-70% reasons for bizarre reasons.

That post is here

lnkd.in/dcxBURQC

As magical as LinkedIn is (hint - always stay active on LI), lots of good advice came pouring in.

What hurt me was that while the advice seemed to be 'common knowledge', neither my Insurance agent nor the issuing company had ever updated me on newer policies, the ability to buy "super top-ups", etc.

Among the angels who helped, @ruchirkanakia of @OneAssure became my ROCKSTA!

He analysed my problem and then advised me on solid solutions to not just optimise my costs but also get MORE than what I am being offered.

The Insurance Company seemed shell-shocked at the counterpoints I provided and in the end, yielded to all my demands :)

Lessons:

GET A CONSULTANT for any long-term investment, insurance or wealth planning you do.

Why?

25 years ago, "mediclaim" was a novelty, the market choices were limited, and I was young. Just signing up for a 'good brand' seemed logical. Today, with multiple providers and deep differentiators, you need experts like Ruchir Kanakia, not an amateur like Alok.

The same applies to all other fields you are NOT a master in.

Also, remember, this is PURE #dhandhekibaat.

The payer (you) wants the best value for the least cost.

Also, the issuer (Insurance, MF) wants to get the best value for the least cost. It's never a win-win until you have an expert on your side.

(To date, the Insurance company @BajajAllianz has never connected with me, despite messages reaching the CEO downwards. That's proof of how closeted and close-minded they are.)

8

3

8

1,964

OneAssure retweeted

21 Jul 2025

Hiring 🎥

Looking for a social media intern, someone who gets the algo like its second nature.

📍Indirangar, Bangalore- on site role (trust me you will want to work from here) , 3-month internship, convertible to full time.

1

2

8

833

OneAssure retweeted

18 Jul 2025

We're hiring @OneAssure for the SDE Intern role!

If you're a final-year student or fresher who wants to work on real-world products, this is your chance to learn and ship fast 🚀

🔍 Familiarity with Golang and gRPC gives you an edge!

📌 Apply here: oneassure.in/careers

#Hiring #SDEIntern #Golang #FresherJobs #TechJobs

2

1

5

567

OneAssure retweeted

9 Jul 2025

Have you ever had a cashless health insurance claim denied?

Trying to understand real issues people face so can help others avoid them.

Vote & share your experience

64%

Yes

9%

No

18%

Faced delays

9%

Never used cashless claim

11 votes • Final results

1

1

4

534

OneAssure retweeted

4 Jul 2025

Wrapped up our monthly townhall with updates, wins, and big plans ahead.

Grateful for a team that builds, questions, and shows up every time😊

1

8

417

OneAssure retweeted

28 Jun 2025

On insurance awareness day, let’s remember that most people in India don’t skip health insurance because they don’t care, but because they don’t understand it. Jargon, exclusions, and fine print create fear and confusion. As experts say, it’s time to simplify, not just sell. Real awareness starts with clarity.

1

4

347

OneAssure retweeted

23 Jun 2025

Looking to hire video editor, open to freelancers too! If you’re someone who truly visualises storytelling, and can turn insurance content into engaging, scroll-stopping videos, I’d love to see your work. DM me or email @ founders@oneassure.in

31

1

38

4,569

OneAssure retweeted

19 Jun 2025

Bajaj State Leadership Team visited our office with big news!!!

They’ve launched India’s 1st region-specific health policy that’s curated state-wise, priced for the masses.

✅ OPD Modern Treatment AYUSH Daycare

✅ Pre/post hosp: 30/60 days

✅ Room: Pvt AC

✅ Premium: Low & flexible

✅ Add-on Restore 10% NCB

A smart, affordable option for first-time buyers.

1

1

16

592

OneAssure retweeted

16 Jun 2025

When we started building, we were a tech-first company. But always sales-first when it came to product decisions. It’s easy to get lost in research and roadmaps. But real validation?

“Can you sell it?”

If someone pays for your product and comes back, that’s true validation. At OneAssure, we listened to what our advisors hear in the field and what customers actually buy, not just what looks good in a prototype.

Sales isn’t the end of product but the beginning as it gives us proof, direction, and focus.

Too many startups wait for “perfect.” But in reality nothing validates faster than a paying customer’s yes.

How do you bring sales into your product process?

1

11

364

OneAssure retweeted

9 Jun 2025

Messages like this are the reason we show up every day. This is what we do and exactly why we do it. 😊

1

8

351

OneAssure retweeted

24 May 2025

The pure joy of making a difference! Saw a tweet about a cashless claim issue with HDFC ergo (first claim in 10 years on a super top-up policy!), reached out, and we're thrilled the claim is now settled. This is exactly why we built @OneAssure to cut through the complexity and ensure everyone gets the support they deserve! 😊

Guys happy to share that hdfc ergo has passed the claim :). Never give up on the fight @money_theory @ruchirkanakia

1

7

577

16 May 2025

What did you do with your first salary?

If you had invested just ₹500, compounding could’ve turned it into lakhs. 📈

Savings are step one. Investing is what builds wealth.

Watch this:youtu.be/cuMMzinF00c

1

743