Evidence-based financial education and fun stats. Part research, part ramblings. Tweets ≠ advice. YouTube vids at youtube.com/optimizedportfol…

Joined September 2020

- Tweets 7,469

- Following 60

- Followers 2,826

- Likes 6,778

1,192 Photos and videos

Pinned Tweet

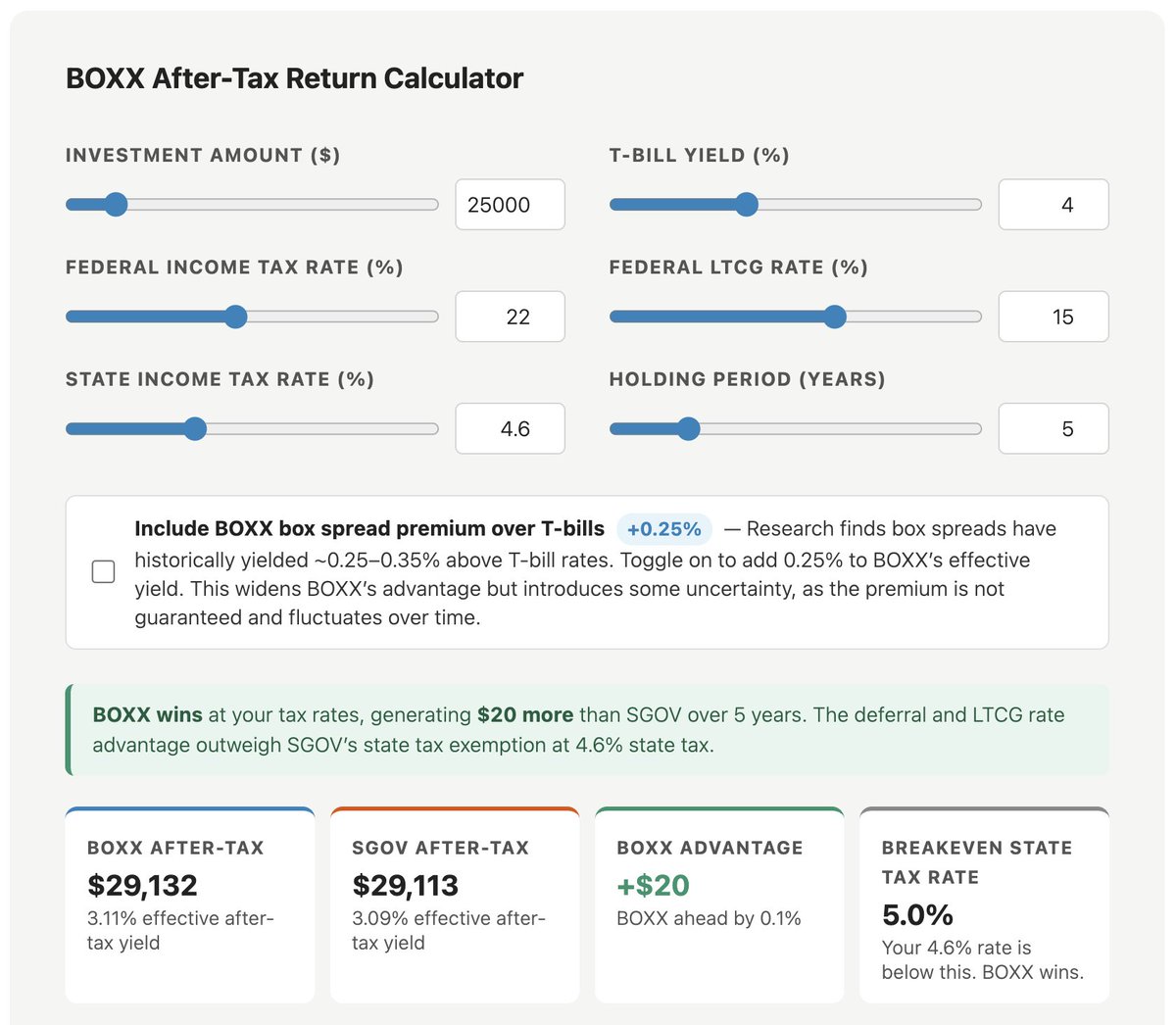

$BOXX after-tax return calculator is live to compare against a plain T-bills fund like $SGOV for specific tax rates.

Obvious disclaimer: Rough estimate. Hypothetical results. Not tax advice or investment advice. Consult your CPA and CFP®.

optimizedportfolio.com/boxx-…

4

43

11,211

Reminder: For the average person, a taxable brokerage account is NOT the most important account, and most of the claims in this video are patently false and/or strawman nonsense.

Jun 11

The most important account in your personal finances is your taxable brokerage account, here’s why..

1

7

598

Optimized Portfolio | John Williamson, APMA® retweeted

Jun 12

The dangerous retirement dividend myth I keep hearing:

“If my portfolio yields 4–5%, I’m set for life. I can just live off the dividends/interest.”

Let me explain why this is NOT the right way to think about generating income from your portfolio

Dividend yield and bond yield have almost nothing to do with how much you can safely spend in retirement.

Safe Withdrawal Rate (the amount you can pull out every year for 30 years without running out of money) is driven by TOTAL RETURN, not yield.

We’ve watched this play out in real time:

- YieldMax / covered-call ETFs advertising 12–15% “yields” → share prices get crushed, total return ends up low or negative

- High-dividend “aristocrats” or REITs that pay 6–8% → price drops 30–50% in a bear market and never fully recovers

Even if the dividend check hits your account every month like clockwork, your principal can (and often does) evaporate underneath you, leading to a shortfall in your retirement income needs

What actually determines how much income you can generate for the rest of your life:

1. Asset allocation (stocks vs bonds vs cash)

2. Sequence-of-returns risk & volatility

3. Your spending flexibility in bad years

4. Time horizon/longevity

5. Total return (price appreciation dividends/interest), not just the yield

A portfolio can have:

- 0% yield (pure growth stocks or zero-coupon bonds) → perfectly safe 4% withdrawal

- 8% yield (high-dividend or option strategies) → still blows up at 4% withdrawal

Yield feels safe.

Total return is safe.

Stop chasing yield.

Start focusing on sustainable total return and withdrawal rules (3–4% rule, guardrails, bucket strategy, etc.).

Your future self will thank you.

16

4

37

5,898

My reaction to the SpaceX IPO - $SPCX - since I already own total market index funds:

6

317

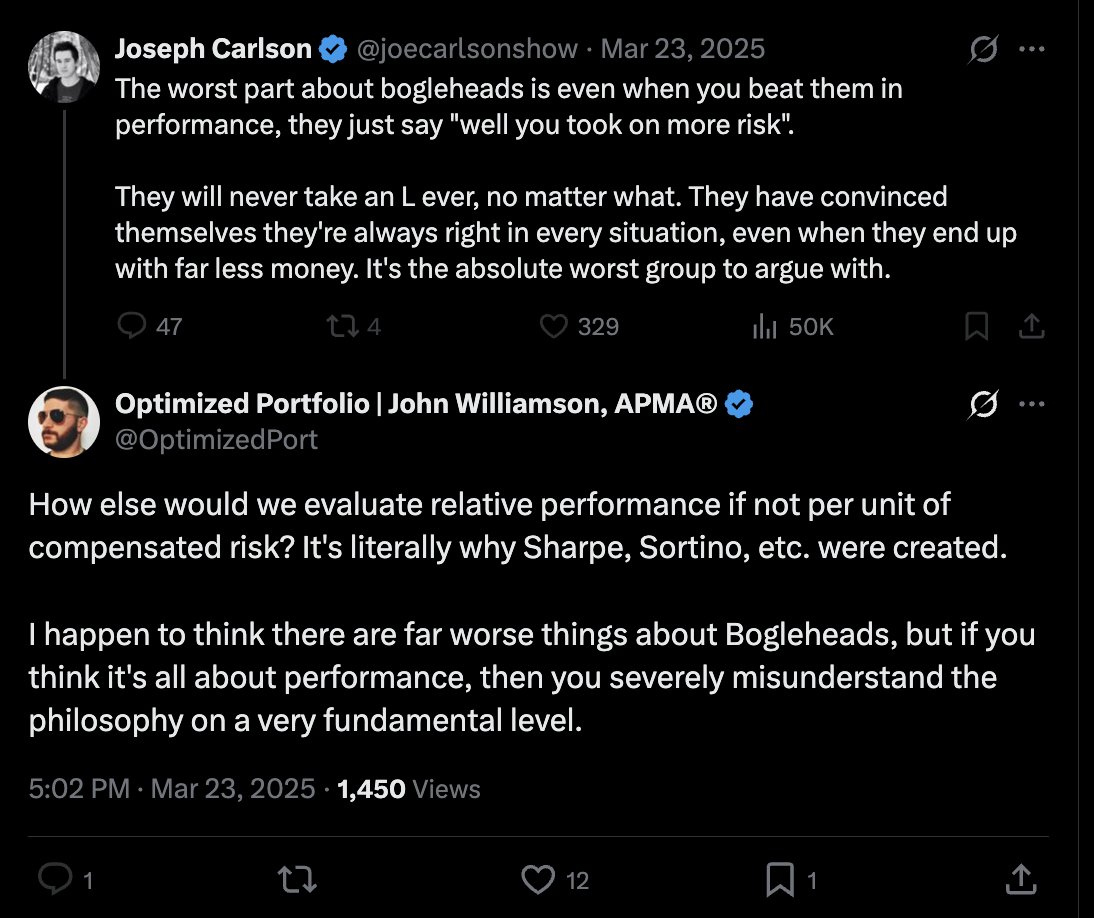

His "...and get a little lucky" is doing the heavy lifting here.

At a 7% annualized return, $3 would need 66 years to turn into $300.

I think like this in terms of future value too, but it's also important to remember inflation. At 3% inflation, that $300 is about $43 today.

Investor Chris Camillo reveals a $3 coffee from Starbucks is actually worth $300 if invested aggressively with a little luck

“Are you willing to skip the coffee at Starbucks for $300?”

1

5

599

Once again, no it isn't.

You clearly do not understand what that phrase does and does not mean.

Jun 9

Past performance is not indicative of future results..for individual stocks. For diversified index funds and ETFs it absolutely is.

Entire companies (Vanguard), all our nation’s retirement plans, and every bit of advice for the margin in your budget have been built on this concept.

3

9

841

To the people who say 401k's are a "scam."

If you say 401k's are a scam, I'm immediately ignoring everything else you say.

4

409

Reminder that paying less in taxes is better than paying more money than paying more in taxes, and most plan to live past age 60. This should be axiomatic.

Jun 9

The only account you need to become financially independent before 60 years old is a taxable brokerage account.

Any other recommendation, like 401ks, IRAs, and mega giga sigma backdoor Roth IRAs are extreme cope and will negatively impact your personal finances.

4

13

3,543

Despite seeing amateur finfluencers' claims to the contrary, covered call options do not provide improved efficiency or diversification for an equities portfolio.

1

1

8

669

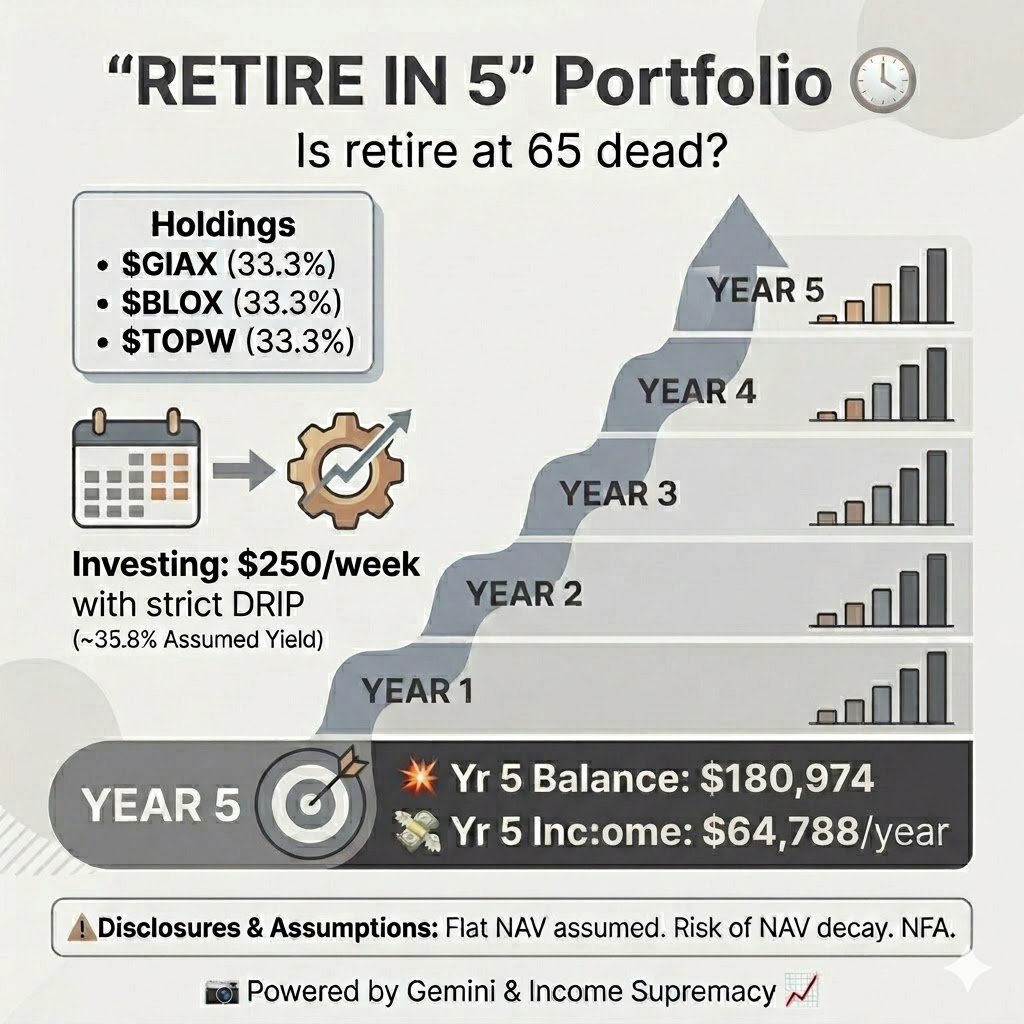

Faulty, dangerous assumptions, inferences, and implications here.

Plainly, the idea that complex, high-fee, high-yield products expedite retirement is false.

I think OP knows this. I wish people would stop perpetuating this nonsense. Novices take it at face value.

"Retire In 5" Portfolio🏖️

Is retire at 65 dead?

$GIAX (33.3%)

$BLOX (33.3%)

$TOPW (33.3%)

Investing $250/wk with DRIP (~35.8% yield):

💥Yr 5 Balance: $180,974

💸Yr 5 Income: $64,788/yr

⚠️Flat NAV assumed. Risk of NAV decay. NFA

📷Powered by High Yield📈

results by Gemini

1

7

3,531

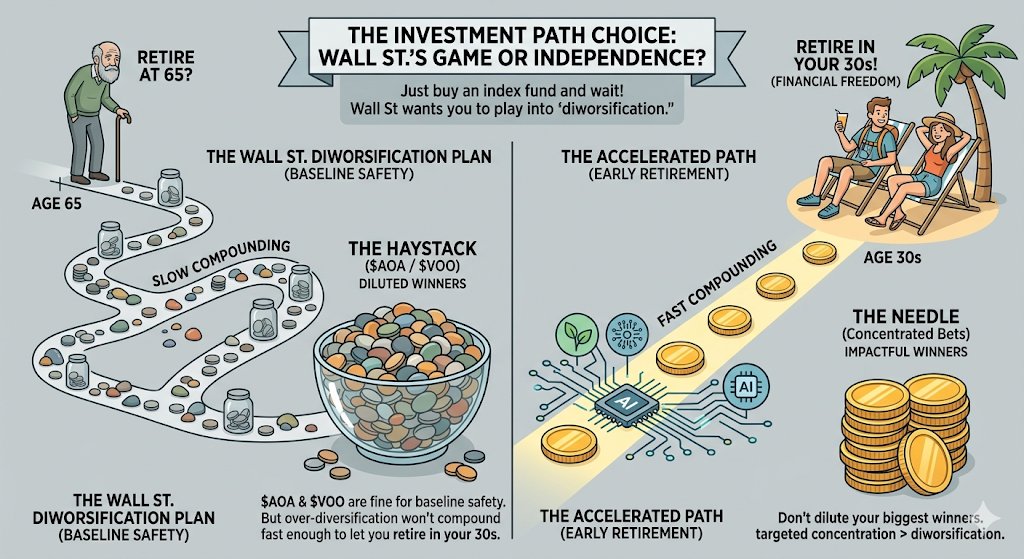

This is objectively terrible advice.

Reminders:

1. Stocks are not "safe."

2. Total mkt index funds are not "diworsification." You'll outperform most investors.

3. Nearly impossible to consistently identify "winners."

4. Single company risk is idiosyncratic. Buy the haystack.

"Buy an index fund and wait!"

Funds like $AOA & $VOO are safe, but having hundreds of holdings is "diworsification."

Alone, it won't compound fast enough for the average person. Buy the haystack, dilute the winners.

Target some needles, not just the haystack.

9

1,103

No it's not.

May 31

1

8

1,049

Interest from a savings account.

May 30

1

11

2,293

Love when you reply to some random topic and it blows up and you see the interesting characters who come out of the woodwork whom you've avoided inside your FinTwit bubble.

2

926

What happened to cracking down on bots?

3

341

This is actually quite negotiable.

News flash: Most people don't want to own a business or have a side hustle.

"Hustle culture" à la grifters like Alex Hormozi and Grant Cardone is so annoying.

May 31

This is non-negotiable if you work a W2 corporate job: you need a side hustle or business and an investment portfolio of stocks, real estate, and private businesses.

3

10

806

Take a drink every time you see a dividend bro mention "NAV erosion" when discussing a covered call fund.

I think they don't even understand what they're talking about or the broader context or implications of that term.

1

7

747