Searching for uncommon returns in small-caps and mid-caps. Written by @joe_oa

Joined August 2022

- Tweets 4,063

- Following 473

- Followers 4,413

- Likes 1,190

756 Photos and videos

Overlooked Alpha retweeted

Jun 12

With SpaceX IPOing today, I'll never forget this Warren Buffett quote about valuations:

"It’s far better to buy a really cool rocket company at an astronomical price than a boring company at a wonderful price."

48

78

2,736

300,487

Jun 10

so cool

307

Overlooked Alpha retweeted

Jun 8

Sandisk's market cap is $260 billion. It's trailing 12-month free cash flow is $2 billion.

100

65

1,746

378,943

Today's market is creating a generation of investors with no regard for fundamentals.

The longer it goes on, the better the opportunity will be for serious investors.

251

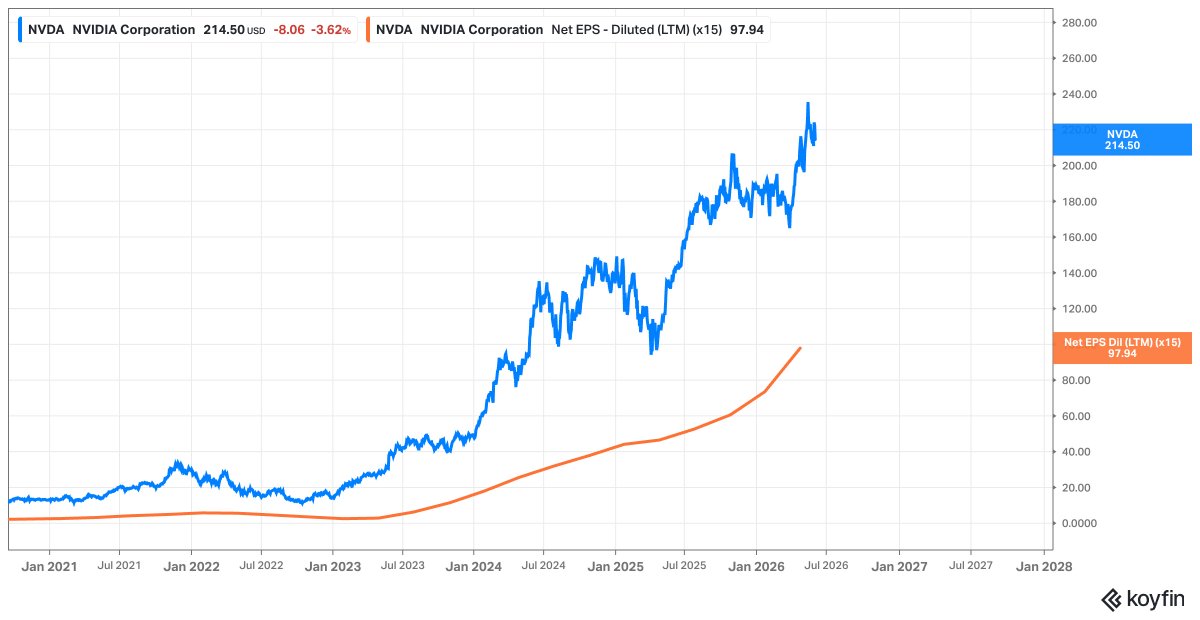

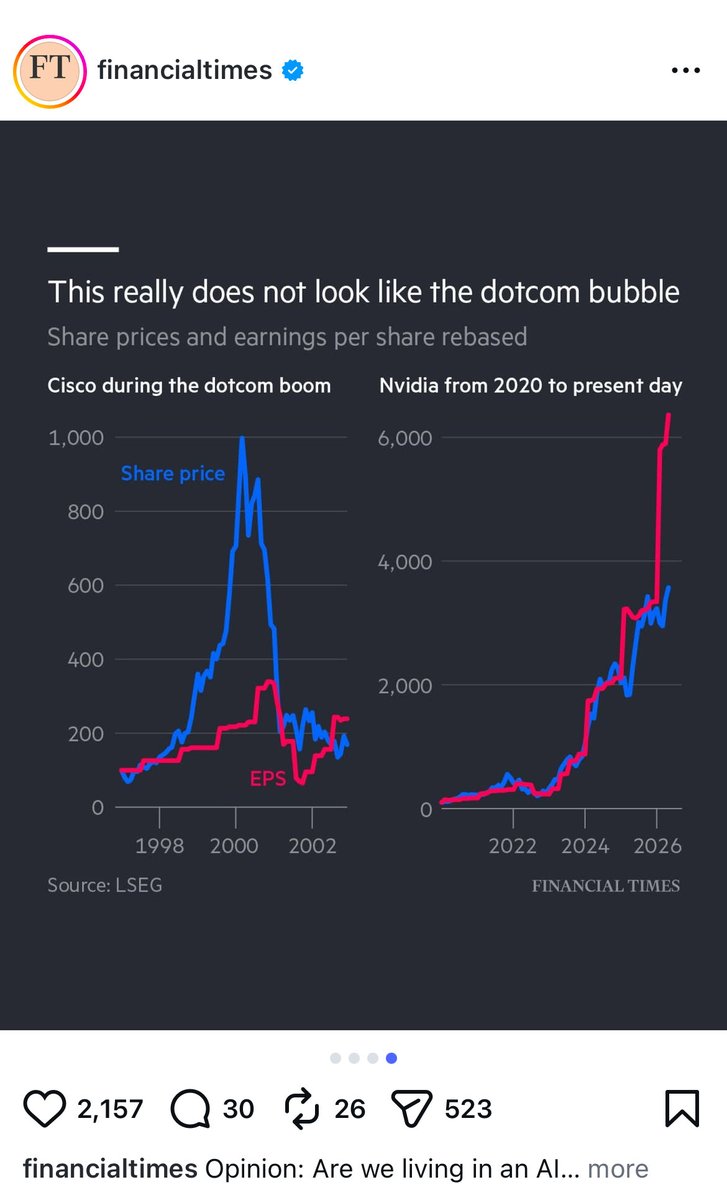

Here is a better way to plot the earnings of Nvidia. EPS is given a multiplier of 15 and plotted against NVDA share price. The line represents the value of the stock at a 15x PE.

258

May 28

👋 New idea just dropped

- £370 million consumer tech biz with 3 growing brands

- Scaled revenues 7x since 2020

- Gross margins up ~600 basis points yoy

- Highly cash generative and attractive valuation

Check it out in the usual place:

open.substack.com/pub/overlo…

1

231

May 28

Ok who the heck is Leopold Aschenbrenner? I never heard of him before

2

431

May 28

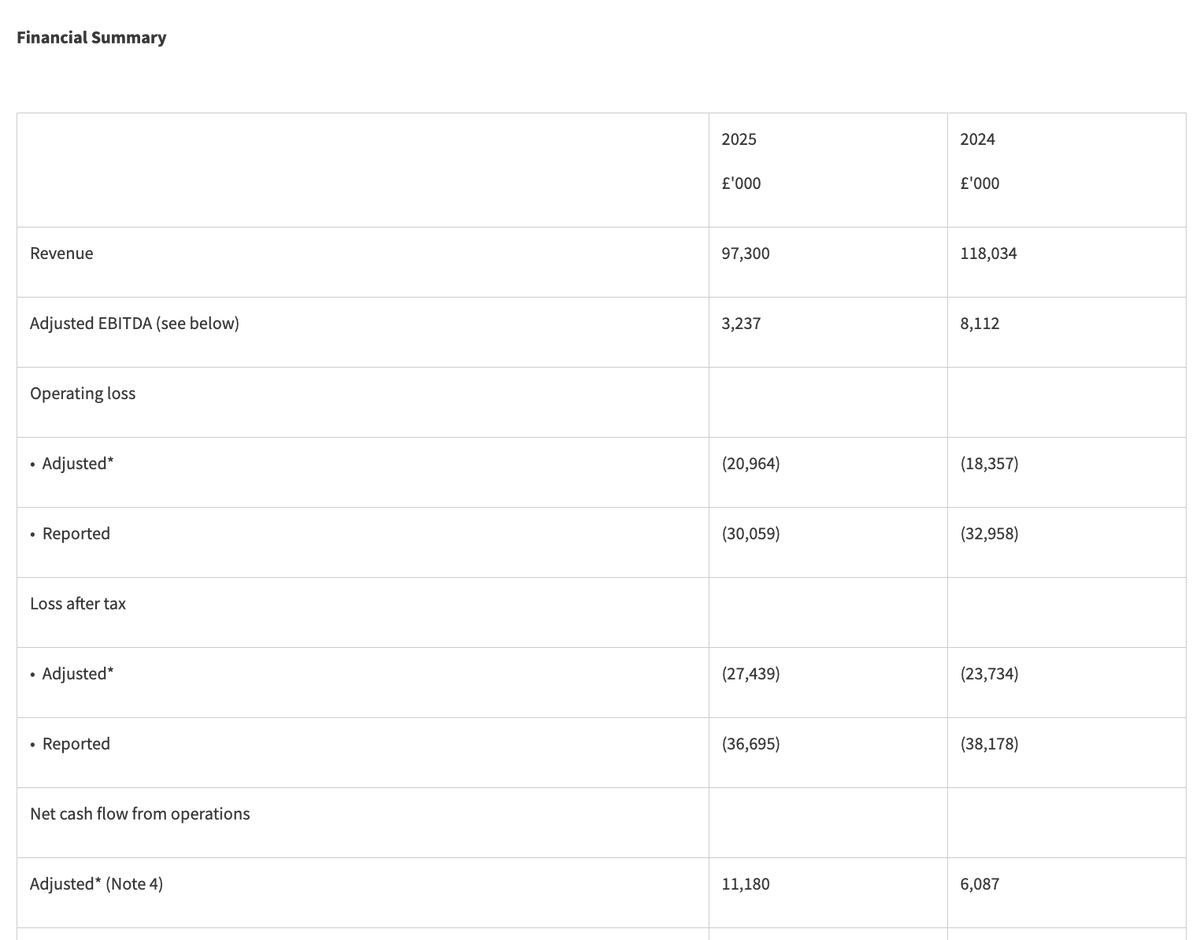

lol... AI meme stock $IQE which is up 800% YTD and has its headquarters in Cardiff, Wales just reported a 17% revenue decline and £30 million operating loss.

Guidance is for high-single digit to low double-digit adjusted EBITDA. This against a £450 million market cap. You really can't make it up.

726

May 13

Making a profit seems to be a negative in this market

3

375

May 12

I didn't believe this when I first heard it.

Y Combinator bought a 6% stake in Stripe for $17,000

1

513

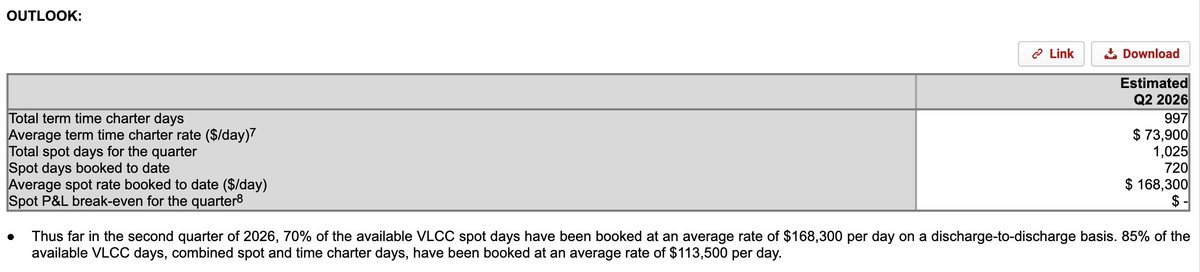

$DHT put up a strong earnings report today.

The company operates a fleet of VLCC crude oil tankers and is benefiting from geopolitical disruption, especially around Iran and the Strait of Hormuz, which has pushed charter rates to extreme levels.

In Q1, DHT generated $164.5m in profit after tax with average spot rates of $91.7k/day. But the average spot rate booked for Q2 has exploded to $168 k/day.

Co. has also sold some vessels and MC looks to be around $3 bn so potentially less than 6x earnings?

The bull thesis is that sanctions, the shadow fleet, longer oil shipping routes, and limited new tanker supply could keep the market tight for years.

DHT is also modernising its fleet and paying out huge dividends tied to earnings.

However, resolution in the Middle East, lifting of sanctions and typical shipping cycles will eventually see some normalisation in rates.

Not an expert here but the scale of the increase in spot rates seems worthy of investigation, especially if Iran peace deal falls through.

1

565

The market does not seem to understand Backblaze $BLZE.

I first wrote about this stock around $6 a share. Since then it’s been up to $11 and down to under $4. And now the stock is rallying once again; jumping 45% after another earnings beat.

Fundamentally though, the business hasn’t changed. Its backup business is mature and slow growing. Its cloud business is exciting and fast growing albeit partly commoditised.

Altogether it’s not a terrible business but probably not worth paying a premium.

Based on guidance, valuation looks to be around 9.3x adjusted ebitda.

But SBC is running at $27 million a year (about 17% of sales) which makes the case much less appealing.

2

3

1,897

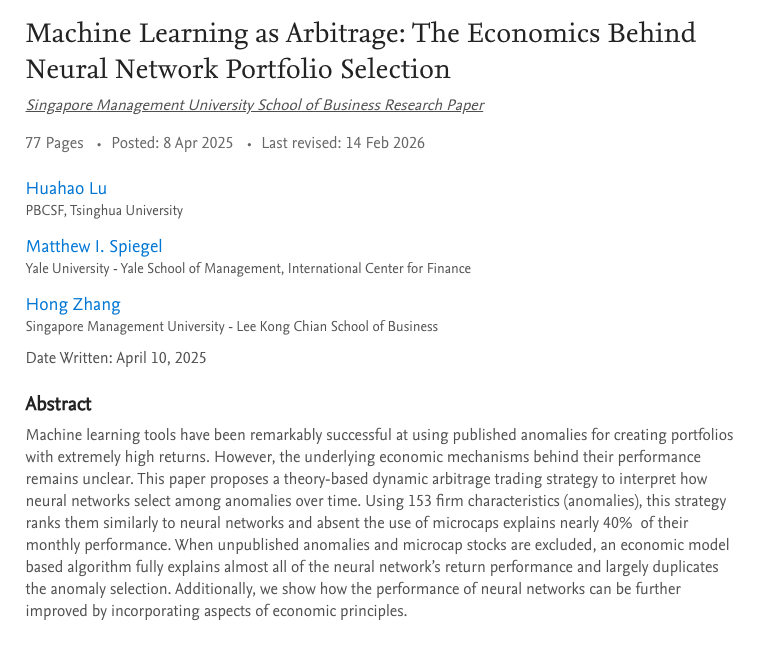

An SSRN paper called 'Machine Learning as Arbitrage' found that neural-network alpha tends to disappear when both unpublished anomalies and microcaps are excluded (SSRN).

Capacity-constrained microcap investing, not generic AI modeling, is still where the most edge lives.

1

405

Plans to move Wise primary listing to US approved by High Court judge. The company plans to list on the Nasdaq on May 11.

Wise said the plans would bring "greater visibility in the US, the biggest market opportunity for our products today", $WISE

2

545