Daily insights on institutional algorithmic trading | CEO @robuxio_com

Joined September 2021

- Tweets 8,518

- Following 287

- Followers 11,952

- Likes 6,362

2,114 Photos and videos

Pinned Tweet

Jun 3

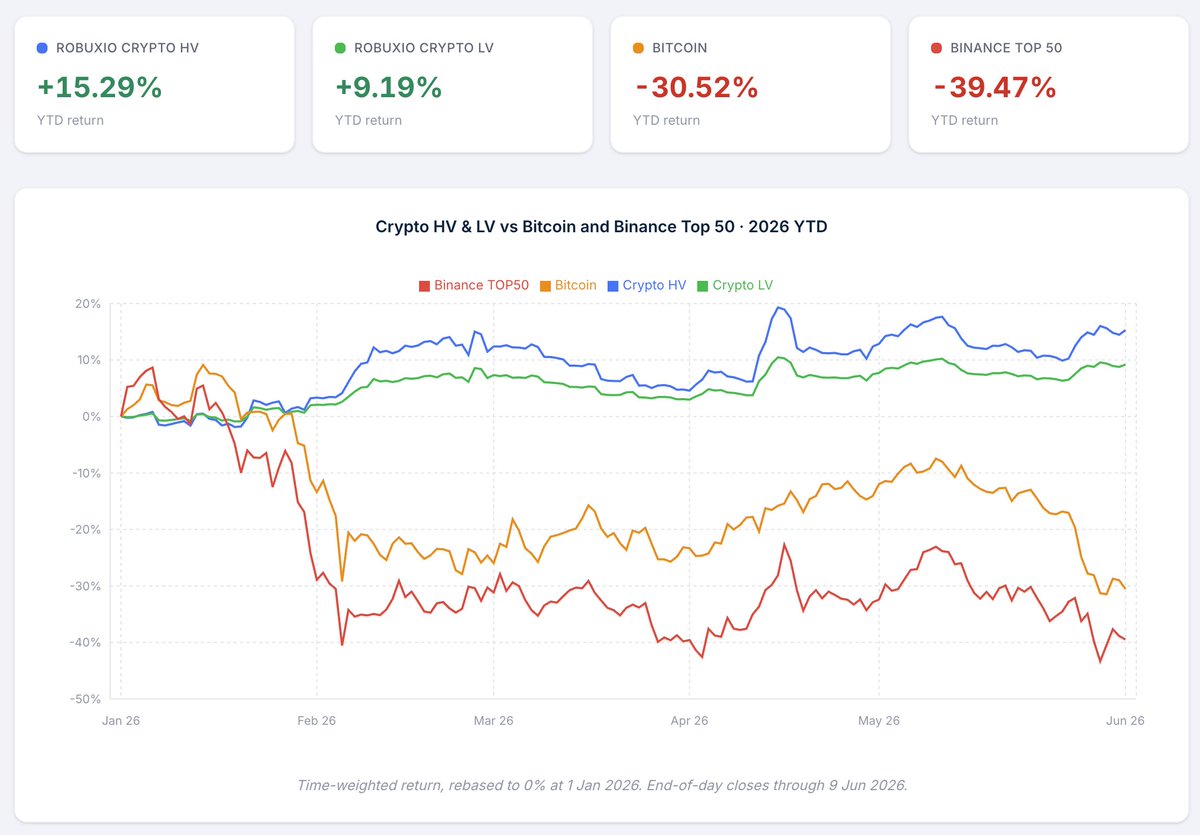

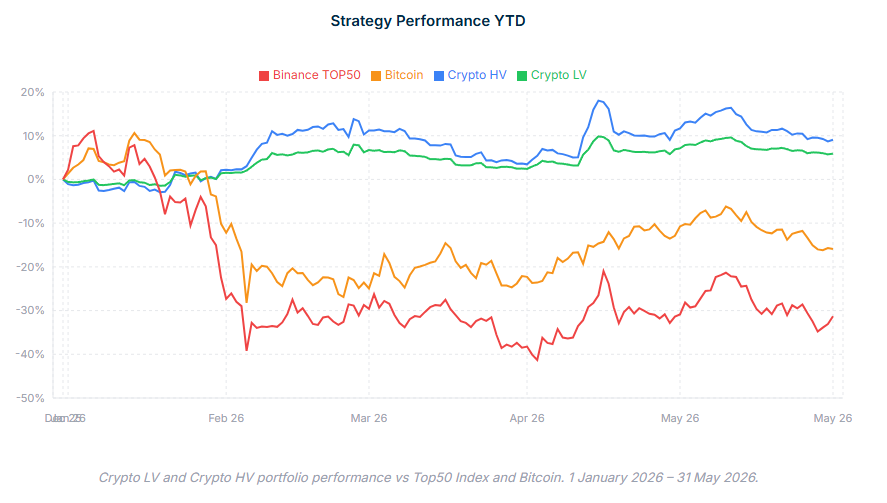

2. Performance YTD:

YTD return of Crypto HV portfolio is 9.1% with a −9.1% max drawdown.

Crypto LV portfolio returned 6.9% with a −5.2% max drawdown.

Bitcoin performance: -15.9%

Top50 performance: -31.3%

1

3

787

Crypto's defining feature isn't long-term trendiness.

It's volatility.

That's also the reason why you need an active approach if you want to profit from the crypto market.

1

6

531

Jun 12

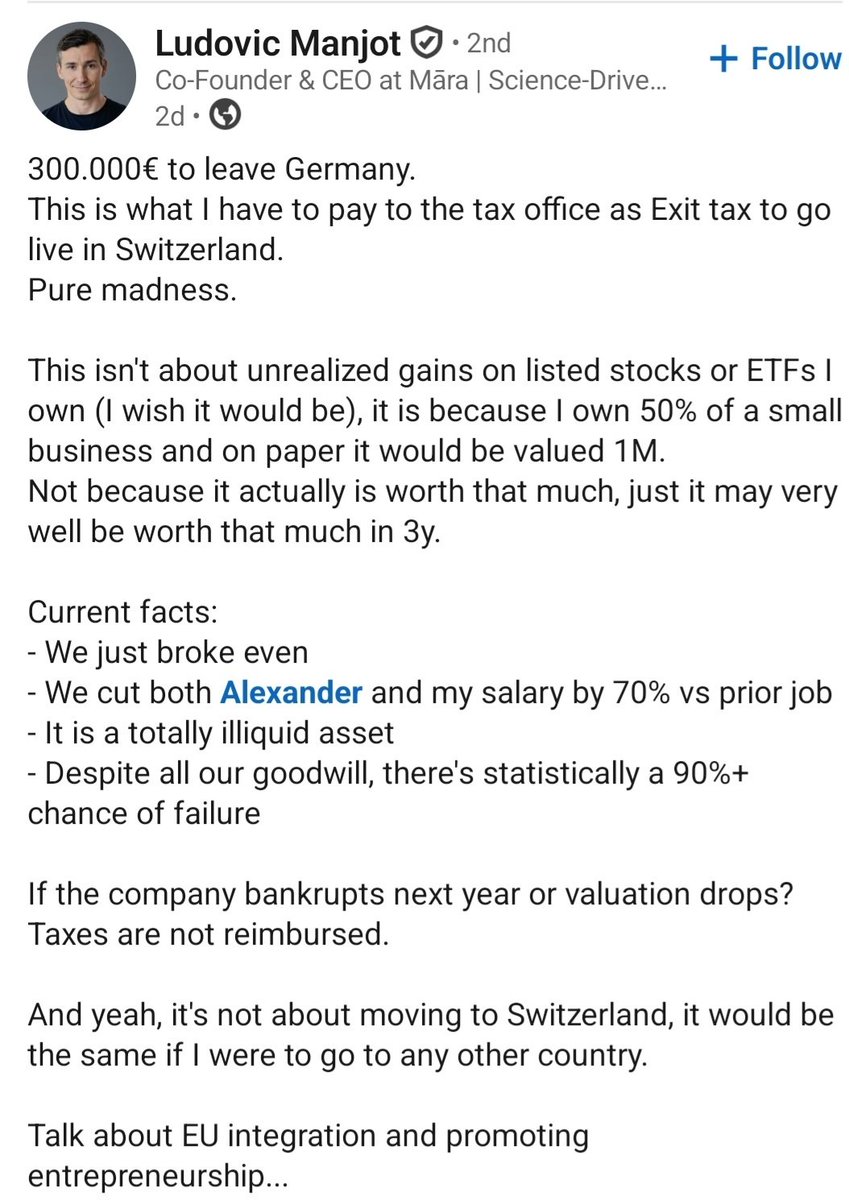

The moment my country introduces even the possibility of an exit tax, I’m packing up my family and leaving. Exit tax is just another form of imprisonment.

4

19

2,588

Jun 12

Boring period!

...was one of our client's comment on the 2026 ytd performance.

I took it like a big compliment in a period when BTC 30D vol went up to 80%. And BTC is down -30% ytd.

But he was right, both portfolios are under the long-term volatility target.

Most of the crypto price action in last 6 months was sideways. In this environment, directional approaches tend to do the best if they are more selective/sizing down.

2

1

13

1,004

Jun 12

A passive investor makes money one way: the market goes up.

A systematic long/short approach is built to do something different, to extract returns from movement itself, in either direction.

Let's walk through the three cases:

1. Market up: the long sleeves capture the trend, much like passive.

2. Market down: here they diverge completely. The short sleeves profit from falling prices. Where the passive investor just absorbs the loss, a long/short portfolio has a sleeve that can generate returns from this regime.

3. Market sideways: A range-bound market goes nowhere for the index, but it still swings within the range, and mean reversion strategies harvest those swings. Again passive exposure will end up with nothing, while a mean reversion sleeve will profit.

That's the structural advantage.

Passive needs one specific outcome to win. A multi-sleeve, long/short portfolio has a way to profit from up, down, and sideways.

It will not beat a roaring bull market every year, that's not the goal, and any honest manager will tell you so.

The goal is to not be dependent on the one outcome passive requires.

2

1

19

2,278

Jun 12

Want to discover how you can get systematic equities exposure?

In our 7-day equities playbook series, we share exactly how you can profit in every market regime.

Always 4 minutes (or less) to read.

Join us here:

robuxio.com/playbook/equitie…

1

1,264

Jun 11

My new favourite YT channel: @Tommy_Anytime

The way he goes after trading guru scammers is legendary!

3

560

Jun 11

My 2 cents on SpaceX IPO:

"On average, Retail IPO stocks decline by over 60% from the offer price after one year."

Source: Retail IPO access: High Hopes, Low Returns

Going long on the IPO offering price is against statistics. Let's see if Musk's magic will change it.

2

1

9

1,367

Jun 11

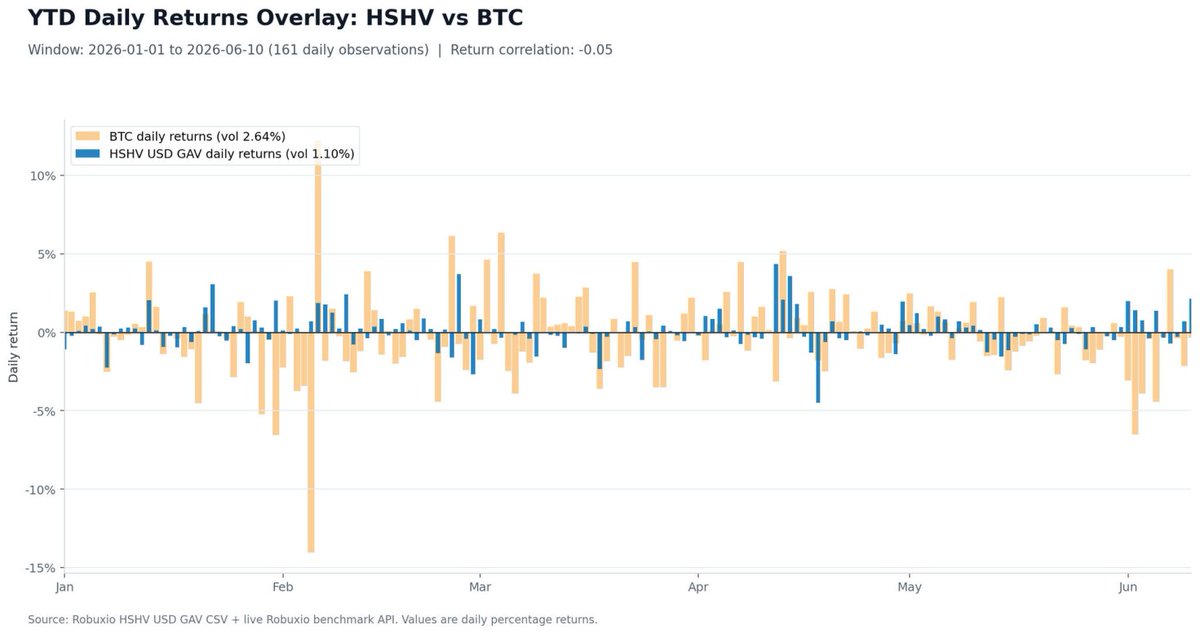

Having a truly all-weather approach to the crypto market has been paying off again this year.

4

572

Jun 10

If you want to buy and hold crypto, there are only one or two coins you should actually own.

Everything else is built for trading and most allocators have only recently learned this expensive lesson.

2

8

692

Jun 9

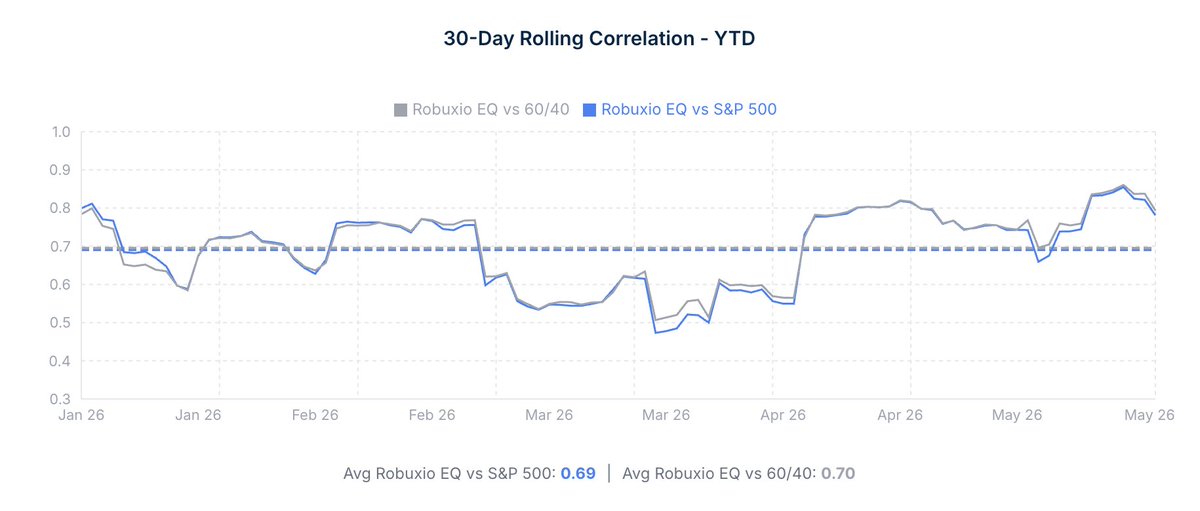

"Buying and holding the S&P 500 is diversified enough."

Not really.

Owning 500 stocks feels diversified. Owning a US index, an international index, some tech, a couple of growth funds, all of these feel diversified.

But then a real stress event hits, and everything falls together. 2008. March 2020. 2022. Suddenly your "diversified" holdings all move with a correlation near one, exactly when you needed them not to.

That's because they were never truly diversified.

All of them are the same bet: long equity beta

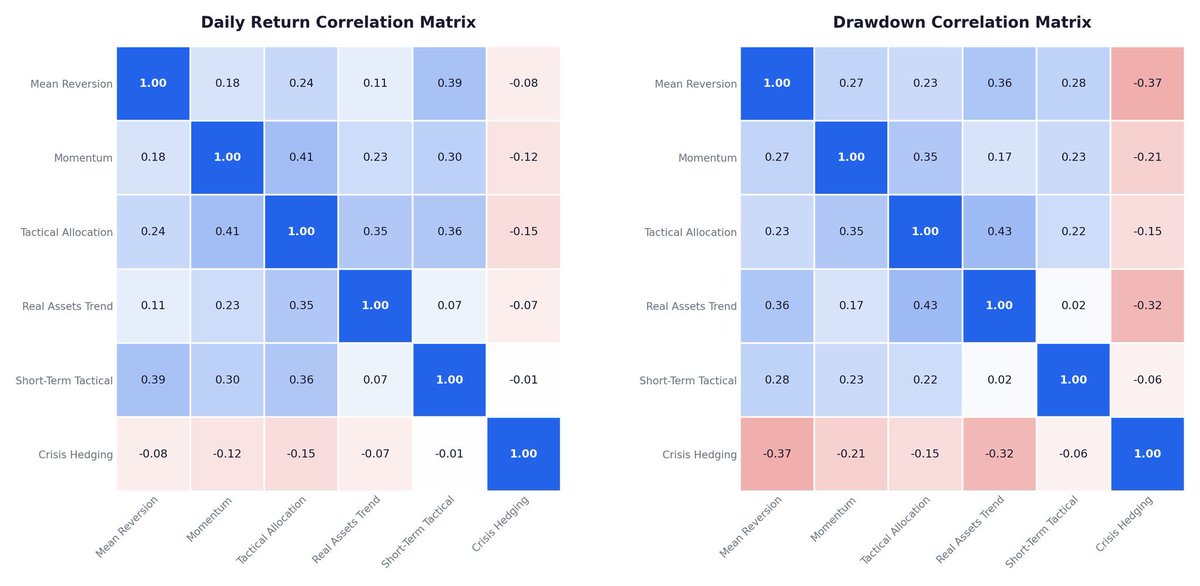

Real diversification isn't about owning more stuff. It's about owning different return drivers. Strategies that make money for genuinely different reasons, so they don't all enter drawdowns at once.

Long equity and short equity. Momentum and mean reversion. Strategies that pay in calm markets and strategies that pay in chaos.

When the return drivers are uncorrelated in returns and drawdowns, you tend to have lower portfolio volatility and feel recover from drawdowns a lot faster.

This is exactly what our Robuxio Equities portfolio is designed to do.

You don't necessarily get higher diversification by owning more things.

You get it by approaching it systematically.

3

4

18

1,668

Jun 9

Want to discover how you can get systematic equities exposure?

In our 7-day equities playbook series, we share exactly how you can profit in every market regime.

Always 4 minutes (or less) to read.

Join us here:

robuxio.com/playbook/equitie…

1

2

795

Jun 6

My very first message to anyone serious about allocating to crypto is don't buy-and-hold.

Do this instead.

1

1

11

1,175

Jun 5

There are 2 ways to get the exposure:

Alternative investment vehicle: robuxio.com/capital

Managed account solution: robuxio.com/crypto/sma

1

360

Jun 5

The S&P 500 is more concentrated now than it was at the dot-com peak.

A passive allocation to the S&P 500 has no mechanism to reduce exposure during deteriorating market conditions, accelerate recovery, or adapt composition.

A systematic approach on the other hand can, by combining uncorrelated return sleeves.

3

2

5

697

Jun 5

Want to discover the benefits of systematic equities exposure?

In our 7-day equities playbook series, we share exactly how you can profit in every market regime.

Always 4 minutes (or less) to read.

Join us here:

robuxio.com/equities-playboo…

1

390

Jun 4

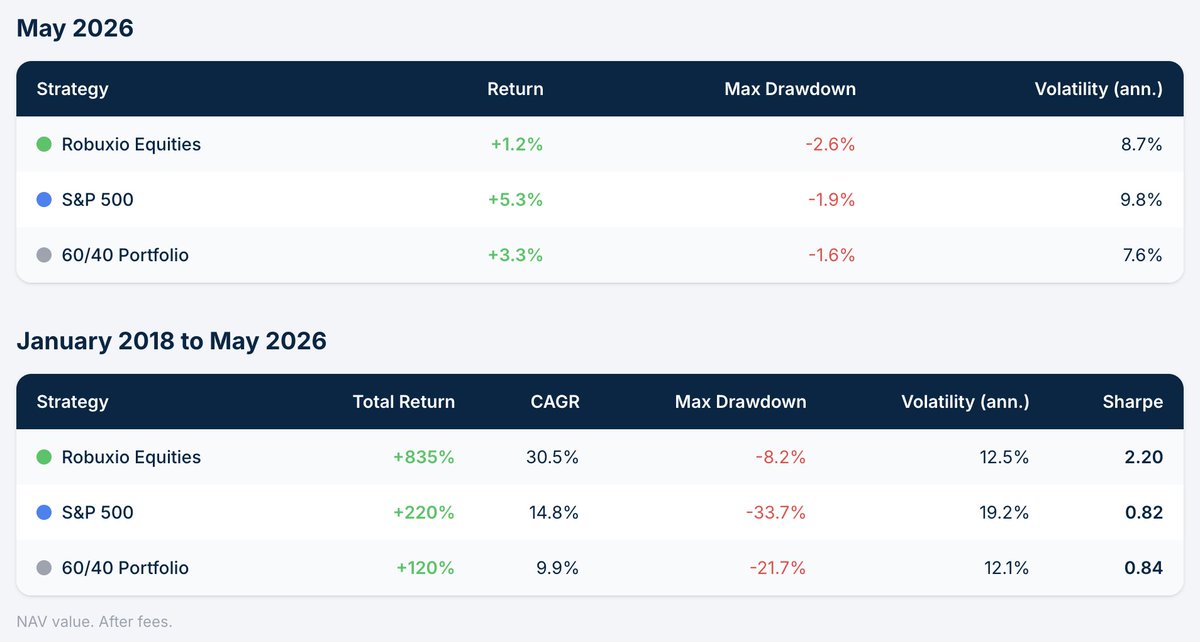

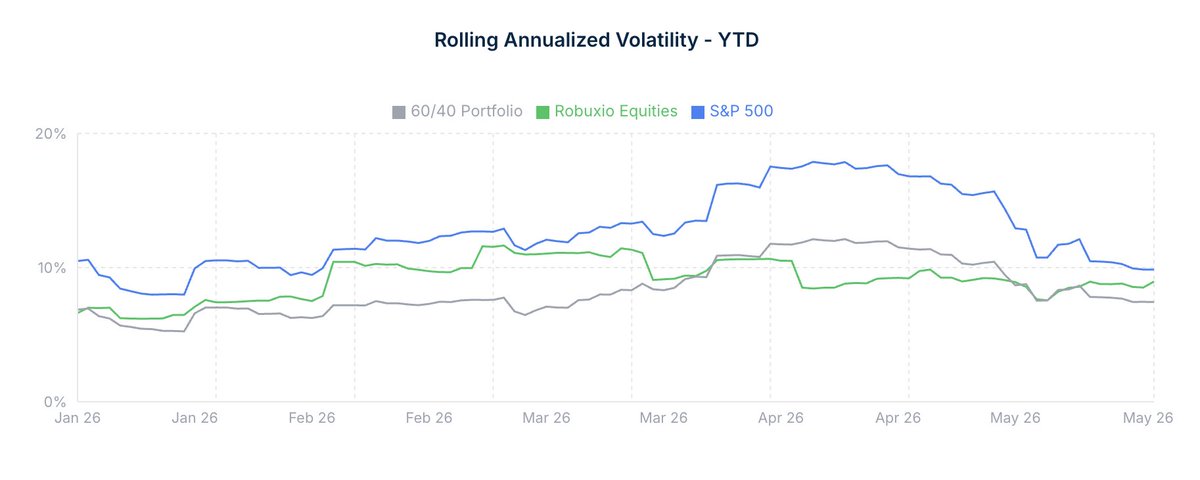

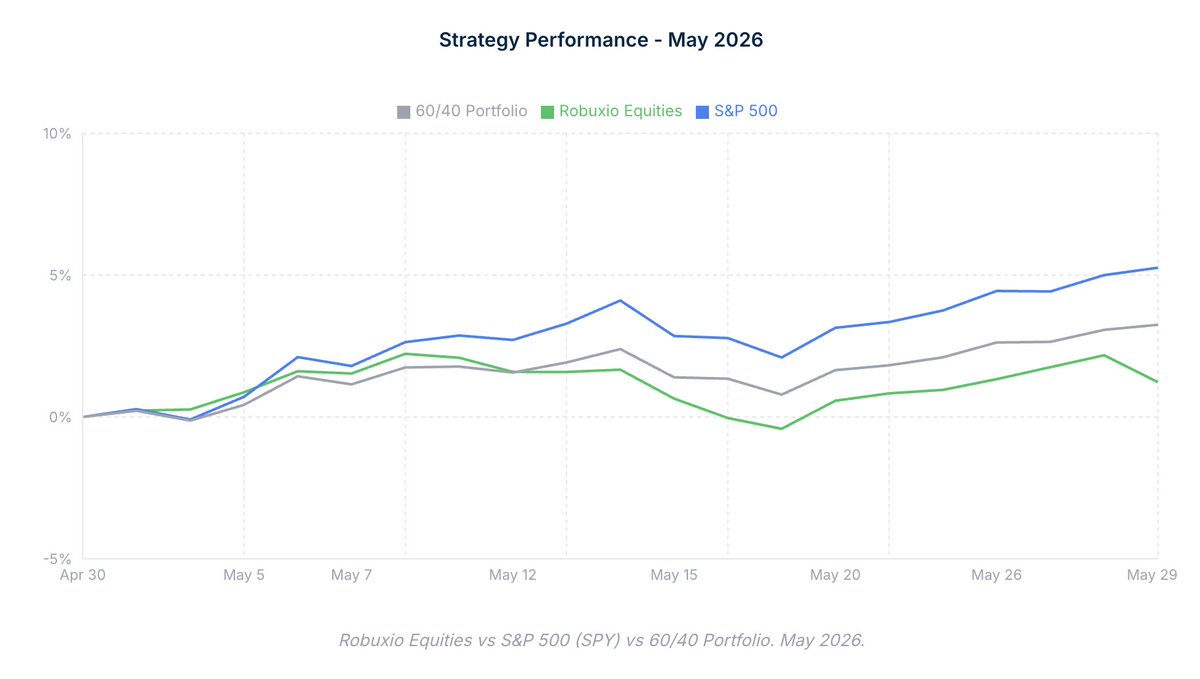

1. May Equities Performance Report:

Robuxio Equities returned 1.2%.

S&P 500 delivered 5.3%.

60/40 delivered -3.5%.

1

3

890