Paycrypt is an onchain utility payment platform for onchain users . Simple, secure crypto payments. Tg channel: t.me/paycrypt_org

Joined September 2025

- Tweets 88

- Following 12

- Followers 30

- Likes 682

12 Photos and videos

Pinned Tweet

10 Sep 2025

Ever feel like your crypto is trapped on a wallet? With Paycrypt, you can finally put it to work for your everyday life😉.

2

4

15

578

Paycrypt retweeted

Jan 20

Welcome Back 😮💨

We would love to sponsor 5 people airtime on Farcaster and Baseapp

Drop screenshot of you opening @Paycrypt_org1 on Farcaster or Baseapp

6

4

9

445

Jan 20

We’re back 🚀

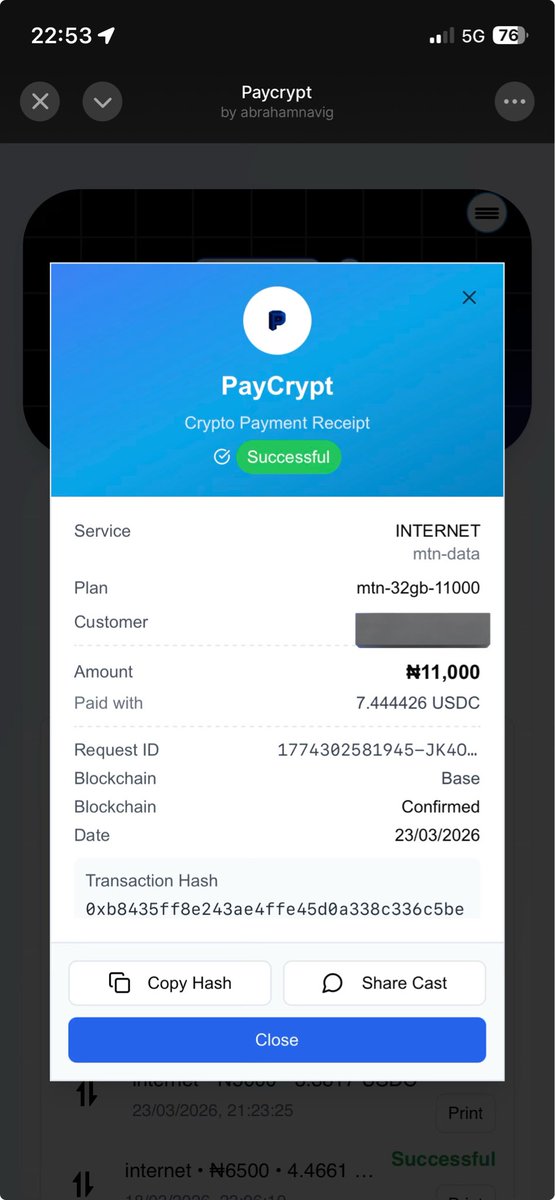

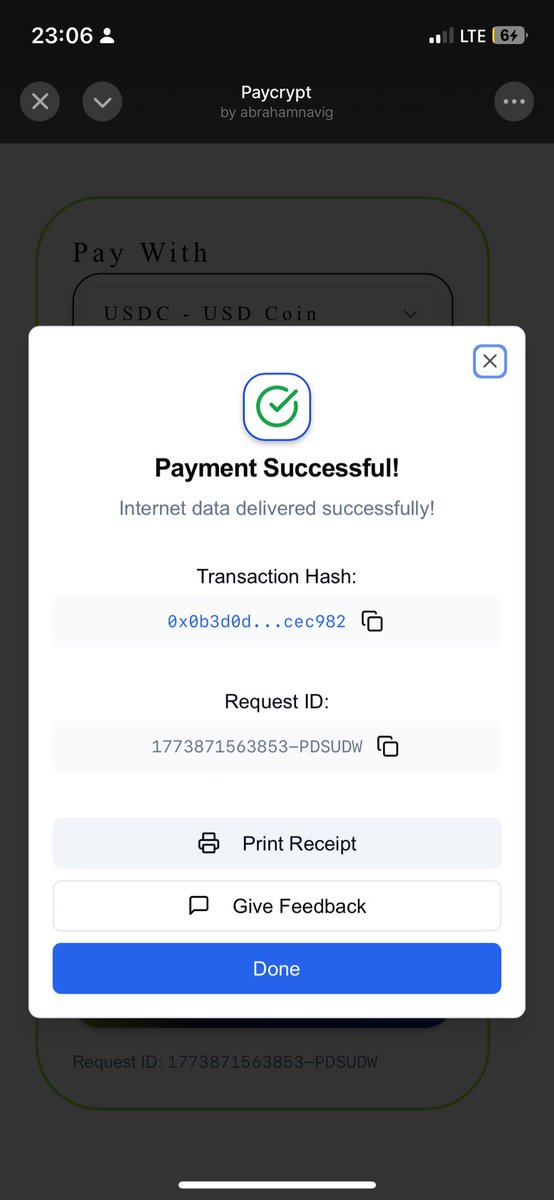

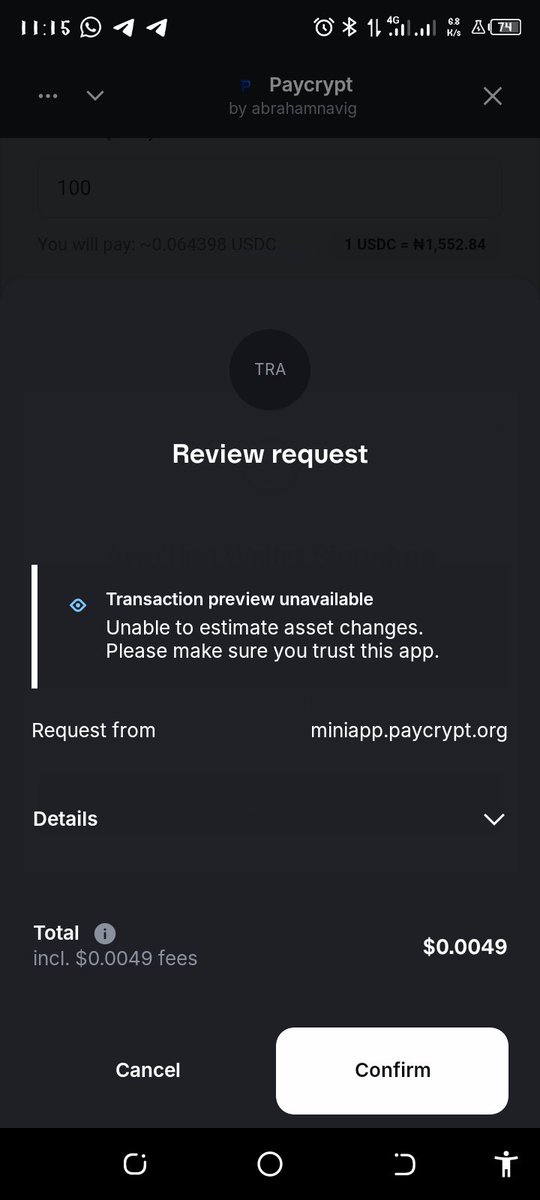

Paycrypt lets you pay for everyday utilities using crypto fast, simple, and practical.

Use it on the web: paycrypt.org, or access it as a mini app on Base & Farcaster.

Crypto, finally made useful. 💙

5

10

22

556

Jan 6

🚨 Important Update! 🚨

Paycrypt is undergoing maintenance.

We'll be back soon! Stay tuned for updates and thank you for your patience.

2

6

148

25 Dec 2025

This Christmas 🎄 , we say thank you 😊 .

To our users, partners, and supporters — you’re the reason we build.

Wishing you peace, joy, and a seamless holiday season with PayCrypt.

2

4

9

176

Paycrypt retweeted

15 Dec 2025

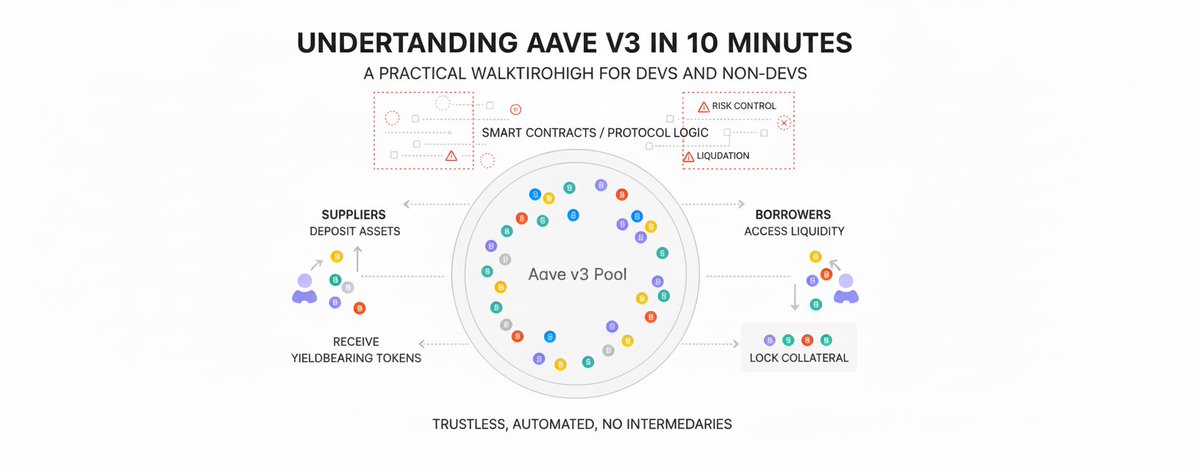

aave v3 in 10mins (part 1)

if you’re a defi developer, you need to understand this. not because you’ll fork it, but because aave is the reference model for onchain lending. most designs in defi either copy it, extend it, or try to fix something it already solved.

and if you’re not a developer, this still matters. aave is one of the clearest examples of how defi actually works.

🔖bookmark this. it’s one you will come back to later.

aave v3 is a non-custodial liquidity protocol. that means no one holds your funds, no one approves your actions, and no one decides if you’re “eligible”. everything runs through a proxy smart contracts.

aave is like the same way you think of uniswap, but instead of swapping tokens, you’re swapping time and risk for yield.

on uniswap, you add liquidity to a pool and earn fees when people trade.

on aave, you supply usdc to a pool and earn interest when people borrow.

so lets say you have usdc just sitting in your wallet. instead of leaving it idle, you supply it to aave. once you do that, your usdc goes into a liquidity pool and you receive ausdc in your wallet. which becomes your living balance. it grows over time as borrowers pay interest..

now someone else wants liquidity.they borrow from the same pool you supplied to. but they must over-collateralize. if they want to borrow usdc, they lock up something worth more than what they’re borrowing, maybe eth or another asset.

this over-collateralization is the foundation of the whole system

as prices move, aave tracks every position with something called a HEALTH FACTOR . it’s a single number that tells you if a position is safe or risky. as long as it stays above 1, everything is fine. once it drops below 1, the position becomes liquidatable

if someone’s position becomes unsafe, a liquidator can step in, repay part of the debt, and receive collateral at a discount. it’s brutal, but it’s what keeps the system solvent without human intervention.

when there’s enough liquidity, borrowing becomes cheap

aave v3 added some important ideas that made the system safer and more efficient.

for example efficiency mode if you’re supplying and borrowing assets that move together in price, like stablecoins or eth-based derivatives, aave lets you borrow more against your collateral. this increases capital efficiency,

isolation mode. new or riskier assets can be listed without endangering the whole protocol. they’re allowed as collateral, but only for limited borrowing and up to a capped amount.

aave v3 also introduced earn vaults. instead of interacting with the protocol directly, users can deposit into vaults that manage supply positions on their behalf. vault shares represent ownership and yield, following the erc-4626 standard. for builders, this makes it easier to create yield products without touching lending logic from scratch.

the key thing to understand is that aave v3 isn’t just an app. it’s infrastructure and defi products all plug into the same smart contracts. aavekit exists so developers don’t need to reinvent supply, borrow, interest models, or liquidation logic.

TLDR :aave shows how money can move without custody, without permission, and without intermediaries, while still managing risk at scale.

this post is intentionally high level. if you understand this flow, you already understand more defi than most people.

on the next one , i’ll go deeper on architecture, hub-and-spoke thinking, how v3 evolved into v4, contract structure, and why these design choices matter for builders.

but for now, if you made it this far, bookmark this. it’s a foundation piece.

3

5

13

713

5 Dec 2025

Utility onchain 🙂

5 Dec 2025

Do we have @base Builder Wrapped 2025?

Quote this with what you built on Base this year and a link to check it out!

2

128

Paycrypt retweeted

29 Nov 2025

Hello 👋 , how is your weekend going?

6

4

24

752

25 Nov 2025

Paycrypt working on a look for its mini app on Farcaster and base app 😁

2

3

12

424

Paycrypt retweeted

12 Nov 2025

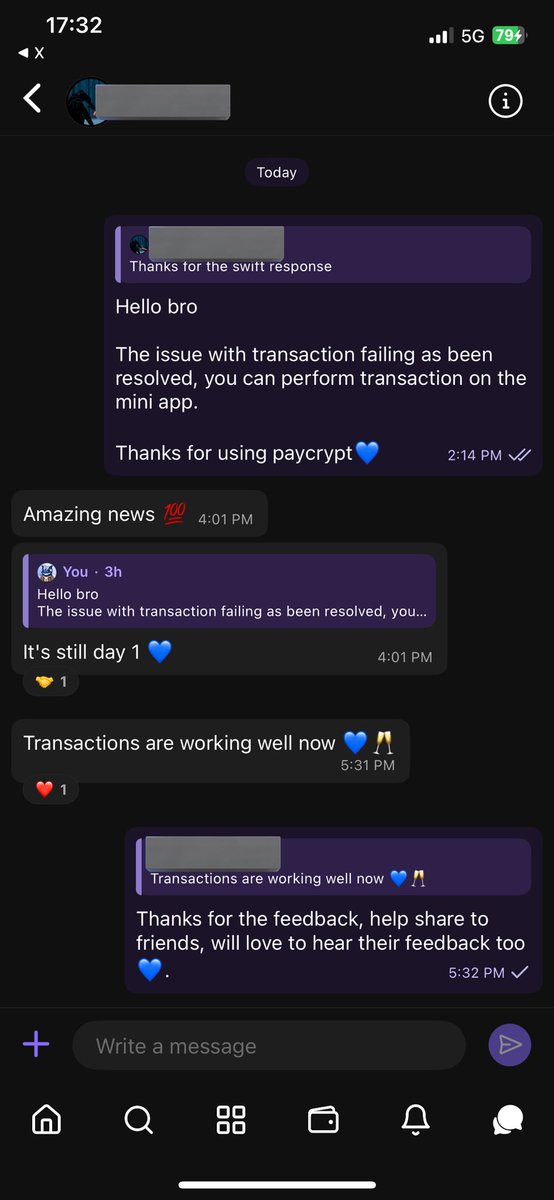

@Paycrypt_org1 is active 24/7 even during technical failure , I am available for feedbacks too

3

6

551

18 Sep 2025

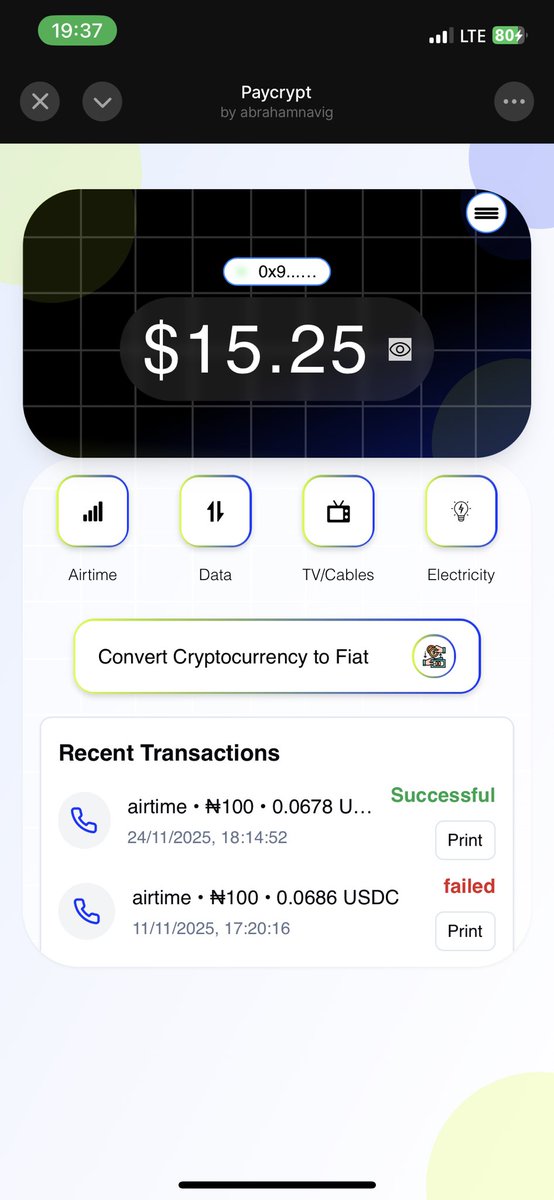

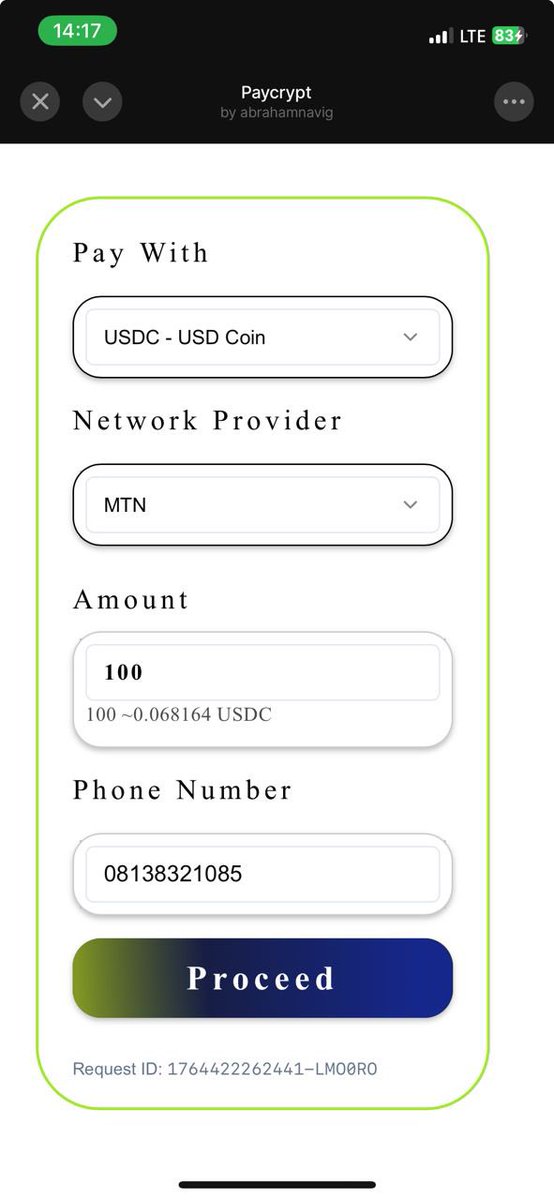

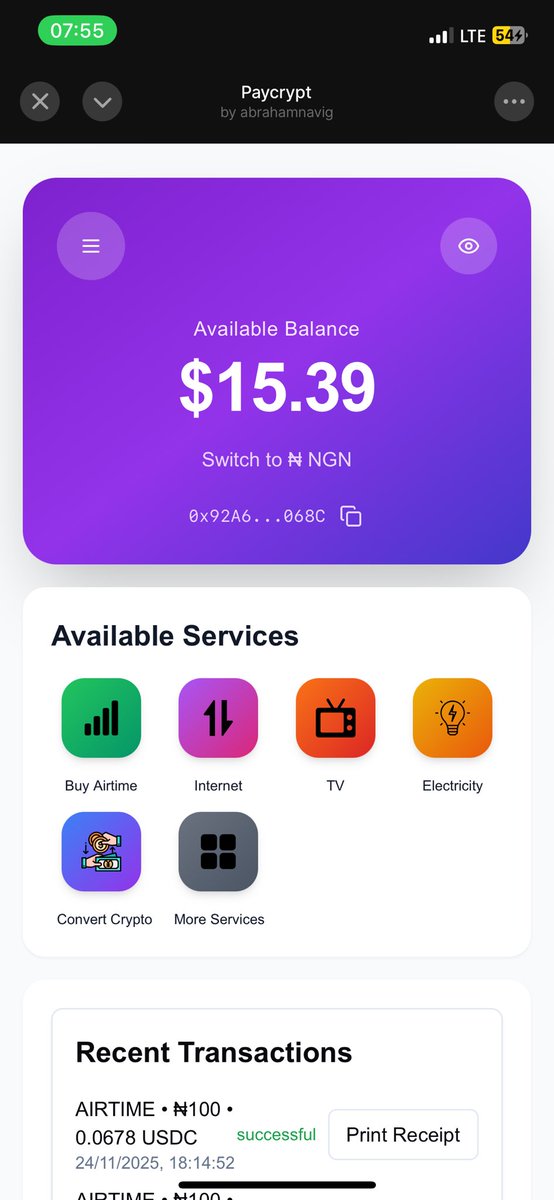

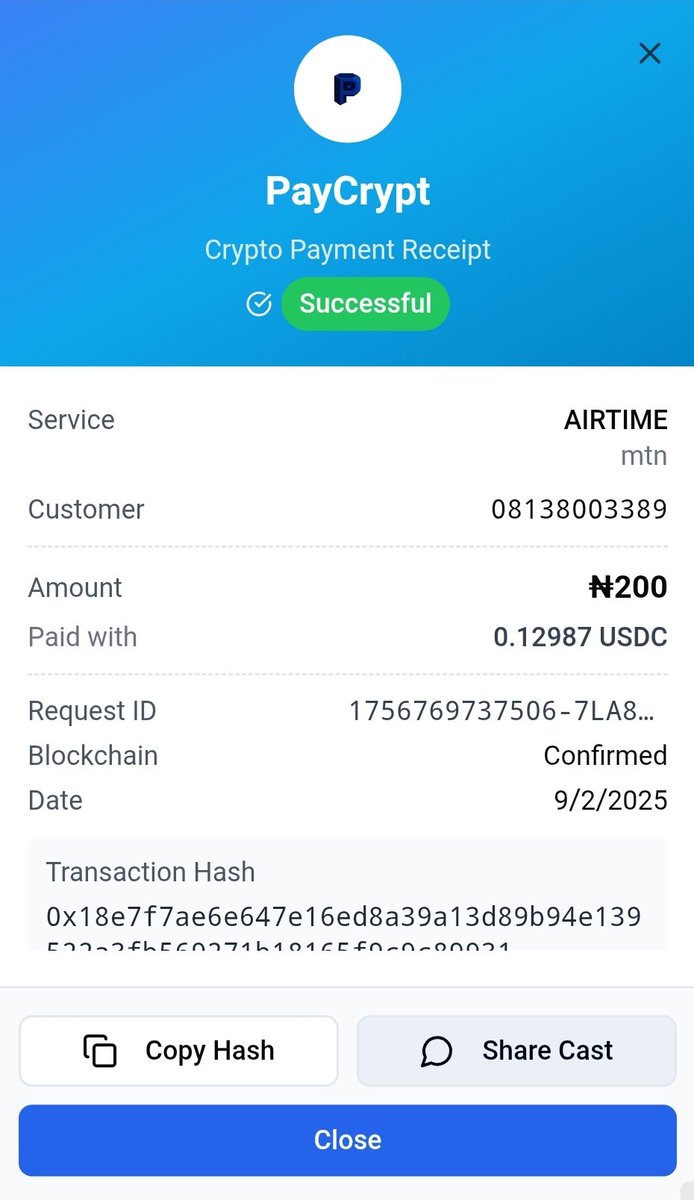

POV: All bills sorted outed without P2P hassel😉.

Pm paycrypt fams🤗.

1

3

6

293

15 Sep 2025

After using cryptocurrency to pay your bills with paycrypt 🌚

2

12

291

Paycrypt retweeted

15 Aug 2025

1

5

285

Paycrypt retweeted

23 Aug 2025

From learning how to Build on Blockchain to Becoming Founders of A Big Startup @paycrypt_org

Founding Team of Paycrypt ⚡️

Pay for all your Utilities with Crypto!

11 Jul 2025

We learnt about @storyprotocol and it importance in Blockchain

We looked at products we can collaborate with artists and creatives to build on @storyprotocol IP

@gardo_martinez @jacobmtucker

4

12

65

4,033

Paycrypt retweeted

25 Aug 2025

Throwback to when we were building @Memevibe_fun .

@paycrypt_org is active 🫡 on web , @farcaster_xyz and @baseapp

Gm , have a blessed day fam

farcaster.xyz/miniapps/46N-w…

2

11

289

Paycrypt retweeted

2 Sep 2025

Paycrypt mini-app has been one of the best project i have worked on

1

7

233