Helping foreign investors navigate the Warsaw Stock Exchange. Sign up for unique insights about Polish companies: polepositioninvesting.com/co…

Joined May 2025

- Tweets 531

- Following 77

- Followers 1,245

- Likes 291

121 Photos and videos

Pinned Tweet

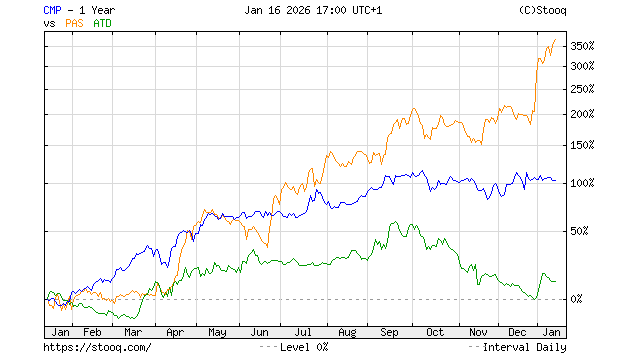

My 2025 result on Polish equities portfolio slightly missed mWIG40 return, significantly missed WIG20 and beat sWIG80.

2025 total return (including dividends and free funds interest) 29.2%

For comparison indices 2025 results:

WIG20: 45%,

mWIG40: 33%,

sWIG80: 25%

#PolishStocks

2

4

1,308

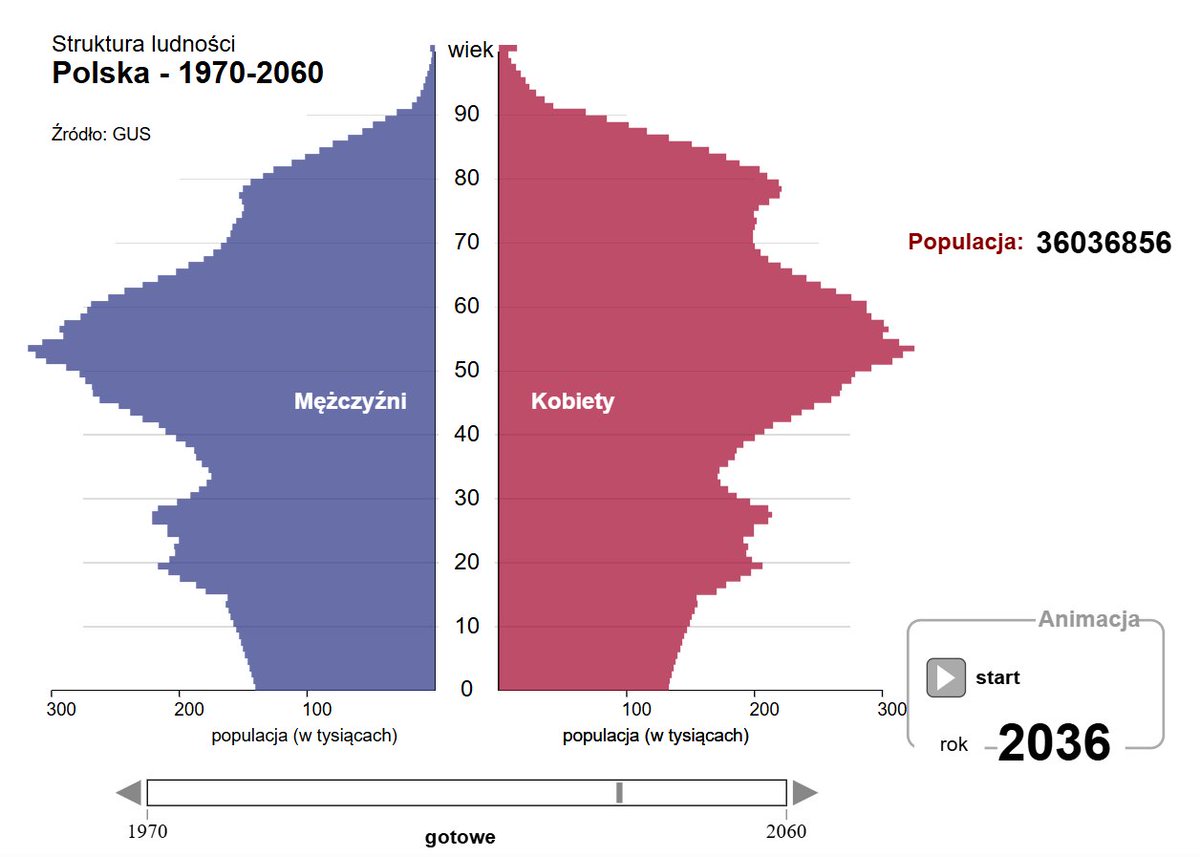

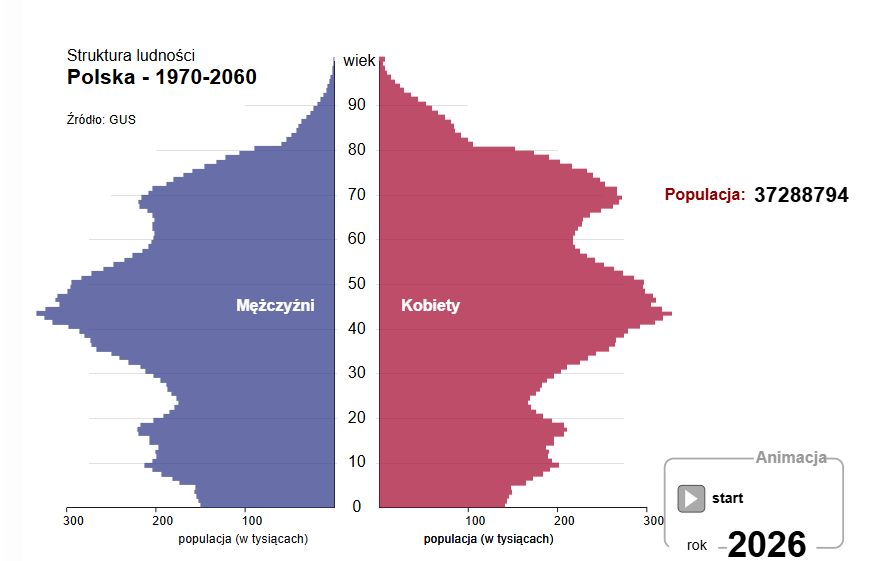

Already more 70 years old people than 20 years old citizens in Poland:

1

1

347

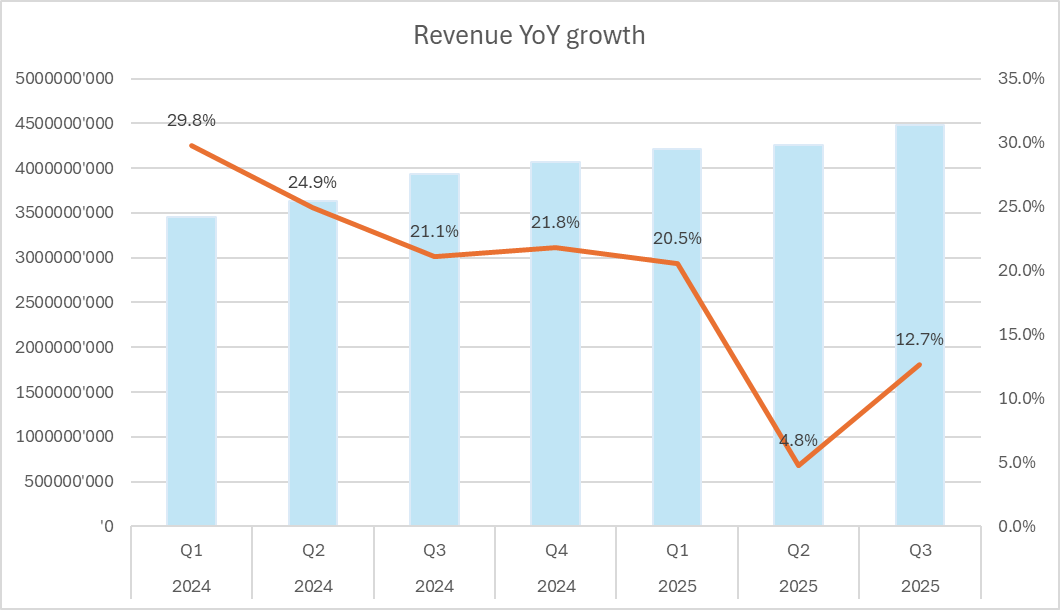

From #LPP Q1 2026 conference call, which has just finished: (fast fashion retailer. Owner of Sinsay, Reserved, Cropp, House, Mohito brands)

LPP’s Q1 2026 conference call delivered a clear message: profitability remains the top priority.

While revenue grew by 10% YoY, management acknowledged that sales performance was below expectations due to unusually unfavorable weather and lingering logistics disruptions following the 2025 fire at its Romanian distribution center. Like-for-like sales declined 2.8% at the group level and 7% at Sinsay.

Despite these headwinds, LPP delivered its fifth consecutive quarter of margin improvement. Gross margin reached a record 58.5%, supported by lower markdown activity, favorable FX rates, and freight costs. EBITDA and net profit grew significantly faster than revenue, demonstrating the strength of the company’s operating model.

The most important strategic announcement was the reduction of Sinsay store openings from 950 to 750 annually. Management emphasized that the goal is not to maximize store count but to maintain attractive returns and protect profitability. New Sinsay stores continue to generate strong economics, with payback periods remaining below 18 months.

Management also openly admitted that Sinsay had become overly focused on low prices at the expense of fashion appeal. The company is now implementing a “Back to Fashion” strategy, aimed at improving product attractiveness, increasing marketing spending, enhancing the in-store experience, and restoring stronger like-for-like growth.

Encouragingly, trading trends improved sharply after the quarter ended. In May and early June, group sales grew approximately 20%, e-commerce sales increased 17%, and like-for-like sales returned to positive territory at around 4%.

1

1

578

My key takeaway: LPP is transitioning from a phase of aggressive expansion to one of disciplined, profitability-focused growth. The company is sacrificing some near-term revenue growth, but maintaining high returns on capital, strong cash generation, and improving margins.

I am also skeptical if weather could have so much negative impact. By cold weather people tend to buy more clothes, especially after mild recent winters people might not have some many warm clothes.

413

#Synektik $SNT.WA 🇵🇱 (#IntuitiveSurgical $ISRG) partner in CEE) FY H1 2025 financial results and notes from the results conference call, which I participated in:

Financial Results and Profitability

H1 FY2025/26 was another record period in terms of both revenue and EBITDA.

Group revenue increased by 35% YoY to PLN 441 million.

EBITDA from continuing operations grew by 46% to PLN 118 million.

The Medical Equipment & IT segment increased revenue by 36% to approximately PLN 414 million, while EBITDA rose by 46%.

The Radiopharmaceuticals segment grew revenue by 17% and also delivered record results.

Profitability has been growing faster than revenue for several consecutive quarters.

Management expects further margin expansion driven by a rising share of recurring revenue.

The improvement in profitability is structural rather than driven by one-off events.

1

4

682

KPO (National Recovery Plan) and Near-Term Demand

Most project settlements are expected between April and September 2026.

The company is seeing accelerating order activity.

Management does not expect a collapse in demand after KPO concludes.

The next EU funding cycle is expected to be even larger.

1

141

Syn2Bio Spin-Off

Short-term effects:

A one-off accounting gain of PLN 261 million.

Changes to equity and balance sheet structure.

Long-term effects:

Synektik will no longer bear the development costs of the cardiac tracer program.

Dividend-paying capacity increases significantly.

Management signaled continued commitment to shareholder distributions

272

Poland's labor market continues to rely increasingly on foreign workers.

According to the latest GUS data, 1.14 million foreigners were working in Poland at the end of 2025, up 7.2% year-over-year and representing 6.9% of all employed persons in the country.

Several interesting treds can be observed:

• Ukrainians remain the dominant group, accounting for 67.6% of all foreign workers (772k people).

• Foreign workers now come from more than 150 countries.

• The fastest-growing groups include workers from Colombia ( 21.3%) and India ( 9.1%).

• Foreign workers are significantly younger than the domestic workforce, with a median age of 37 versus 43 for Polish workers.

• The highest concentration of foreign labor can be found in staffing and support services, where more than one in four workers is a foreign national.

Source: GUS, "Cudzoziemcy wykonujący pracę w Polsce w grudniu 2025 r."

1

203