| @OpenGDP OG Alpha-OGDP socials - Alphasquad | @fortytwonetwork 42💙🤍 @RallyOnChain creator @SentientAGI EarlyAGI 💗

Joined July 2021

- Tweets 29,946

- Following 1,908

- Followers 1,582

- Likes 106,000

1,476 Photos and videos

Pinned Tweet

16 Dec 2025

Exploring the OpenGDP Devnet: testing faucet, token transactions, and stress tests on the Devnet. These intensive tests help evaluate network performance and system stability. Upcoming updates and public access are coming soon!

@OpenGDP

49

9

397

22,861

Prey.gdp retweeted

We do swarm inference across specialized models at @fortytwonetwork. DM if you’re interested in early API access.

22

10

47

391

Prey.gdp retweeted

Open-source AI is entering a different phase.

We’re no longer seeing isolated model launches.

We’re seeing an ecosystem being assembled.

• Frontier open models with million-word context

• Physical AI world models for robotics

• Self-hosted AI workspaces anyone can run

• Memory systems built for long-term agents

• Open infrastructure for AI factories

• Enterprises investing billions into securing open ecosystems

And projects like Sentient are pushing the next layer:

building user-owned AI where agents, tools, and intelligence evolve in the open.

The future of AGI won’t be decided by a single company.

It will be shaped by communities that choose openness over control.

That’s the shift this week’s field notes make impossible to ignore.

@SentientAGI

11

3

60

1,142

Startup idea: Origin Protocol.

The internet is very good at spreading ideas and terrible at remembering where they came from.

A researcher writes a thread.

A developer shares a concept.

A small account discovers a narrative.

A month later the same idea is everywhere and nobody knows who started it.

Origin Protocol would timestamp ideas, connect every remix back to the source, and let AI map how knowledge actually traveled across the internet.

Not copyright.

Not patents.

A public graph of influence where attribution becomes part of your on-chain reputation.

The biggest missing infrastructure in AI is not generation.

It is remembering who created the signal before the noise arrived.

Feels like something @RallyOnChain would appreciate.

Who deserves credit for an idea after a thousand people improve it?

12

1

48

761

Job title that will exist by 2030: Future Waste Collector.

Their job is to clean up the thousands of lives AI helped you almost live.

The business you almost started.

The city you almost moved to.

The career path generated from a different version of you.

Not a coach.

Not a recruiter.

Someone who helps people bury the futures they did not choose, so they can finally build the one they did.

The strange part is that this job will probably exist because machines become too good at imagining possibilities.

@RallyOnChain

10

50

794

Prey.gdp retweeted

Jun 12

Three different AI giants.

Three independent research teams.

One name that keeps showing up.

First Alibaba.

Then Google.

Now Microsoft.

None of them had a reason to promote an open-source project. Yet all of them referenced EvoSkill when discussing self-evolving agents.

Microsoft went even further.

They didn’t just cite it.

They described EvoSkill as the strongest harness-side competitor they evaluated and the closest open-source system to the approach behind Codex </> and Claude Code <>.

That says something important.

Real research doesn’t care about followers.

It doesn’t care about hype.

It cares about results.

You can’t buy your way into academic citations from the world’s biggest AI labs.

You earn them by shipping work that moves the field forward.

At this point, the pattern is impossible to ignore.

3 major labs.

3 separate papers.

1 open-source team.

@SentientAGI isn’t trying to join the frontier conversation anymore.

They’re helping define it.

12

1

66

1,213

Jun 12

The bio I'd never put on LinkedIn:

I ignored a project for three weeks because I thought the logo looked ugly.

I once spent an entire night tracking a wallet that I was sure belonged to a genius trader.

It was an exchange hot wallet.

My most useful skill is reading the replies under a crypto post and guessing who never opened the docs.

I abandoned a thread that was almost finished because I was scared someone smarter than me would point out a mistake.

The best thing that ever happened to me was being wrong in public.

It stopped me from pretending to be an expert and forced me to become a student.

That is why @RallyOnChain makes sense to me.

The version of me that looked confident was mostly performing.

The version that admits mistakes creates better work.

12

65

877

Jun 12

One assumption keeps showing up in discussions about institutional blockchain adoption, and I think it misses the real decision banks are making.

The choice in 2026 is not simply which technology stack to trust.

It is which future counterparties you want to be connected to.

Settlement infrastructure compounds differently from almost every other market. Every new institution does not just add volume, it expands the number of possible financial relationships across the network. Ten institutions create 45 potential settlement corridors. One hundred create nearly 5,000.

That is why history matters here. SWIFT did not become a global standard because messaging was an exciting business. It scaled from 239 institutions to more than 11,000 because every new participant increased the value of joining and the cost of staying outside. Visa followed the same structural path.

The 2026 window exists because the remaining institutional questions are moving from research into production. The GFMA identified the open agenda clearly: interbank interoperability for tokenized deposits, transaction privacy standards, RTGS-equivalent settlement, and governance for digital money.

The first production deployments that solve these problems become more than products. They become coordination points.

This is where @zksync stands out. Live deployments already include Deutsche Bank's Memento platform, ADI Chain with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton, while Cari Network is onboarding five U.S. regional banks representing more than $600 billion in combined deposits.

The architectural approach matters because regulated institutions need multiple properties at the same time: private execution, institution-controlled infrastructure, cryptographic finality through validity proofs, and native interoperability.

JPMorgan Kinexys has already processed more than $1.5 trillion on blockchain rails. The tokenized RWA market is approaching $29 billion. More than 93% of tokenized U.S. assets already settle on Ethereum.

The interesting question for the next decade may not be which network processes the most transactions.

It may be which network becomes the place institutions expect everyone else to already be.

8

1

59

761

Prey.gdp retweeted

Jun 11

Sentient’s Cohort 0 results highlight something many people miss about AI agents:

The goal isn’t to use more compute.

It’s to use compute intelligently.

→ Wrong answers are expensive.

43% of all inference spending in Cohort 0 went toward incorrect outputs because many agents kept generating even after going off track.

The strongest teams didn’t just achieve higher accuracy.

They reached it with lower cost.

→ Reasoning should scale with the problem.

Across 223 tasks, successful trajectories used more reasoning in 166 of them.

But the increase was deliberate:

• ~10% more on easy tasks

• ~25% more on medium tasks

• ~35% more on hard tasks

The best agents invested extra computation only when it improved the outcome.

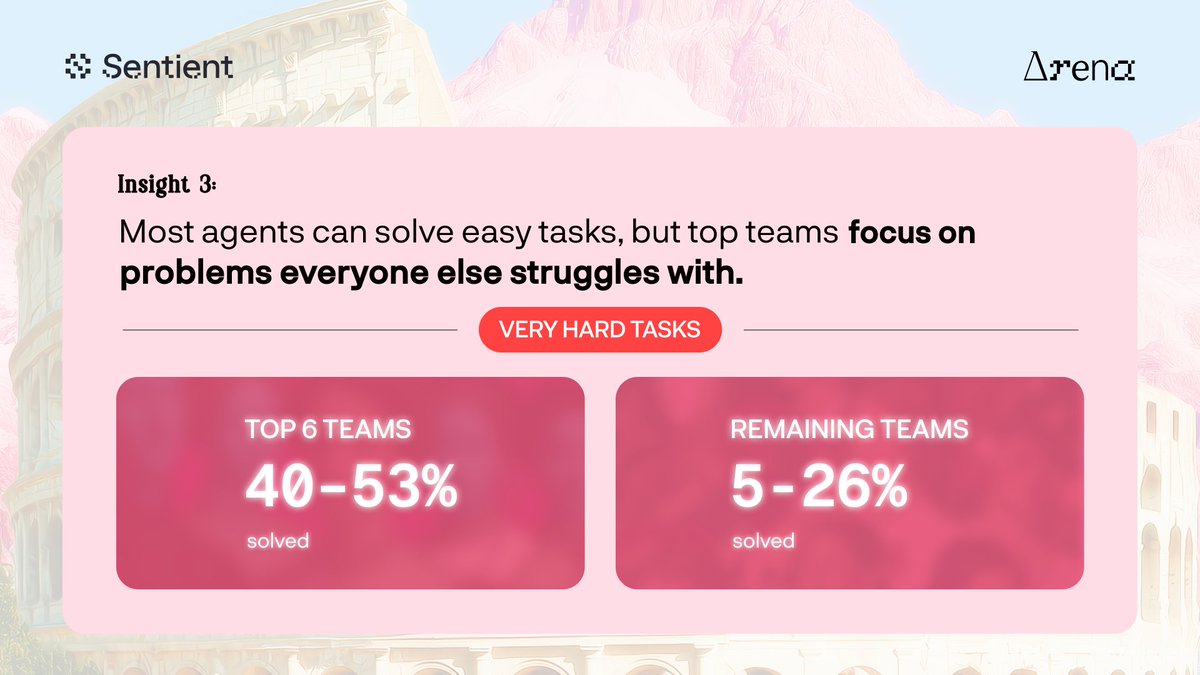

→ The leaderboard is decided by the hardest problems.

The biggest gap between the Top 6 teams and everyone else wasn’t on easy or medium tasks.

It was on hard and very hard ones.

Top 6 teams solved:

• 83–92% of hard tasks

• 40–53% of very hard tasks

Teams ranked 7–15 solved:

• 17–75% of hard tasks

• 5–26% of very hard tasks

Easy problems are crowded. The real advantage comes from solving the long-tail challenges where most agents fail.

Cohort 0 sends a clear message: the next generation of AI agents won’t be defined by bigger reasoning budgets, but by knowing when and where reasoning actually matters.

@SentientAGI

Jun 10

We analyzed data from our first batch of Arena builders to see what separates the top teams from everyone else.

Here are the three open source AI insights that stood out ↓

17

3

71

1,375

Prey.gdp retweeted

Jun 11

The opinion that usually costs me followers: most people calling themselves long term investors are just short term traders who got trapped and renamed the strategy. @RallyOnChain

11

2

53

911

Prey.gdp retweeted

Jun 11

Apparently I won Crypto Person of the Year 2026.

My dad still introduces me as "my son who spends too much time on the computer."

Honestly, I let him.

Trying to explain wallets, rollups, or on-chain reputation never worked.

One day he asked me,

"So... do people actually use the things you talk about?"

That was the first time I realized I wasn't chasing tokens anymore.

I was chasing usefulness.

Thanks, @RallyOnChain, for making that measurable.

10

2

58

1,040

Jun 11

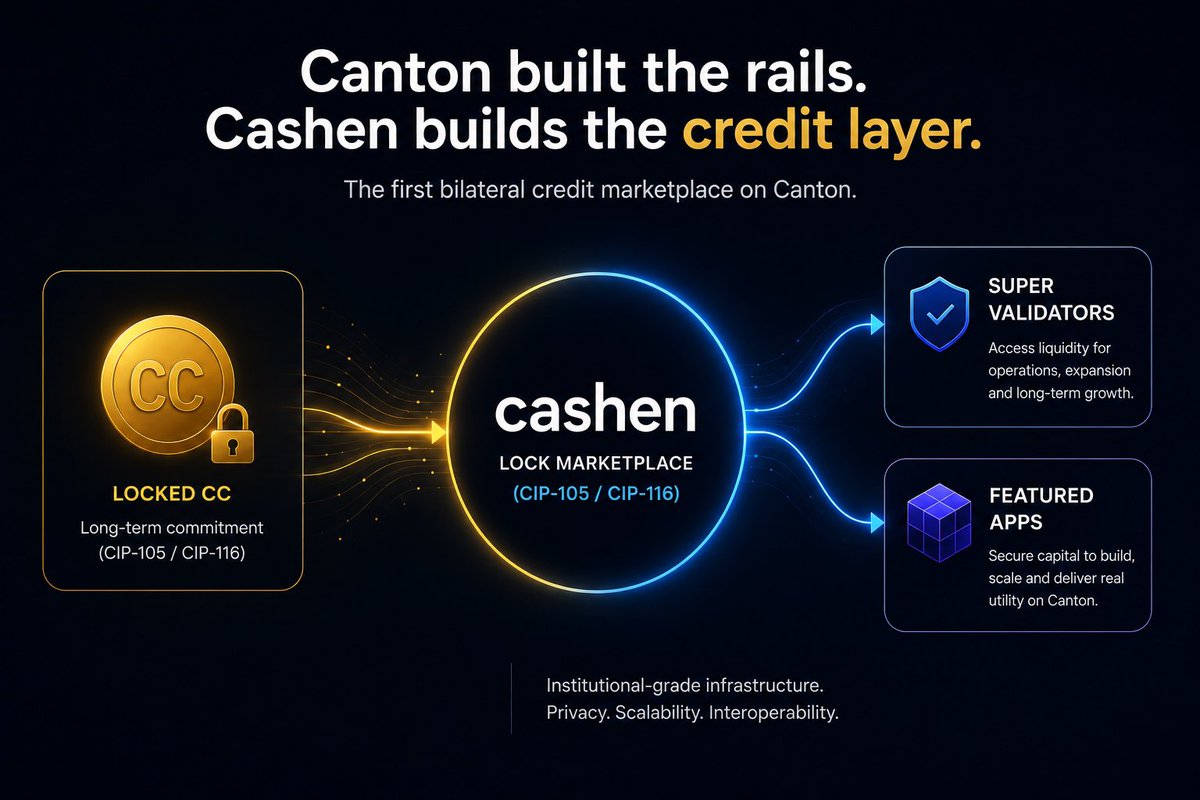

Locked capital doesn’t have to be idle capital.

What I find interesting about @Cashen_cc is that it gives the Canton ecosystem a marketplace for locked positions under CIP-105 / CIP-116, connecting capital providers with Super Validators and Featured Apps that actually need liquidity.

That’s a stronger model than forcing assets to sit unused. It aligns incentives while keeping long-term commitment to Canton.

3

46

700

Prey.gdp retweeted

Jun 11

.@Cashen_cc is live on CCTools.

The bilateral marketplace for Canton locks: suppliers earn yield on their CC with full custody, while Featured Apps and Super Validators get the CC they need to lock for CIP-105 / CIP-116. Backed by Ergonia, a Cumberland DRW company.

> 15,000 CC pool, 40 winners

> Top 10 tweets win 750 CC each, judged on quality

> 30 raffle winners, 250 CC each

Show Canton what Cashen unlocks: cctools.network/earn/cashen-…

314

1,169

1,135

19,533

Jun 11

The waitlist era is over.

Rally is now open to everyone, making it easier than ever to start building your onchain reputation.

Everyone now has instant access.

A brand new profile page helps you track your stats and rewards.

New users receive a 200 RLP welcome bonus.

Signing up with a referral unlocks 400 RLP instead.

The Wingston NFT whitelist is also open for those who stay active.

This is more than a feature update.

It is a step toward a more accessible ecosystem where participation is rewarded from the very beginning.

The best time to build your profile is before the next wave arrives.

@RallyOnChain

rally.fun/r/preywebthree

6

43

868

Jun 11

Watching GenLayer's testnet evolve has been interesting because every stage feels connected to a larger goal.

The objective was never just to distribute points.

It was to stress-test a network where Intelligent Contracts can use AI, interact with real-world information, and still reach decentralized consensus.

Participants have been helping validate infrastructure, explore new execution models, and provide feedback on a system that moves beyond traditional if/else logic.

Most blockchains ask:

"Did this transaction happen?"

@GenLayer is exploring a harder question:

"Can a decentralized network evaluate context and make a reasonable decision?"

That is exactly why I've been paying attention to this testnet from the beginning.

7

40

809