Joined May 2023

- Tweets 1,157

- Following 29

- Followers 656

- Likes 613

5 Photos and videos

Pinned Tweet

Apr 18

secure your handle now 🔥

Apr 17

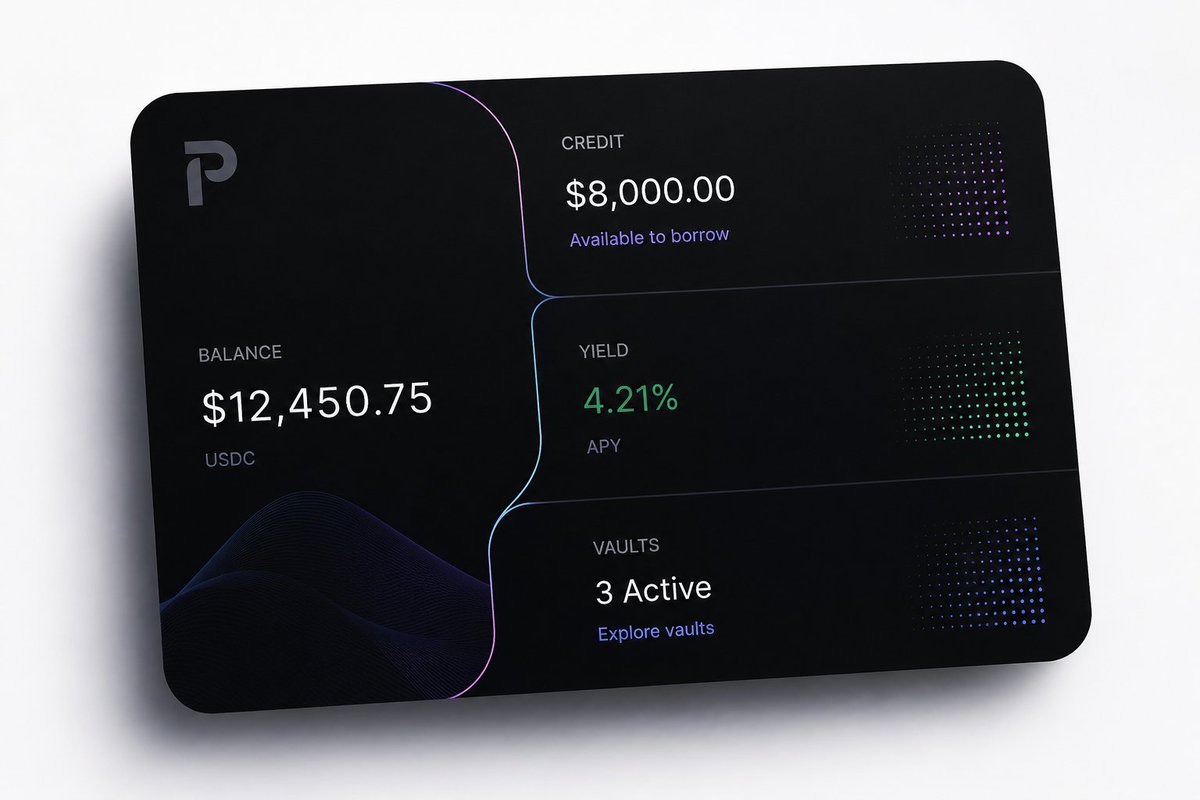

Your [@handle] will be your identity on Pulsar.

The neobank built for how money actually moves today.

RT Reply with your handle for early access before public reservations open on 4/20 ↓

24

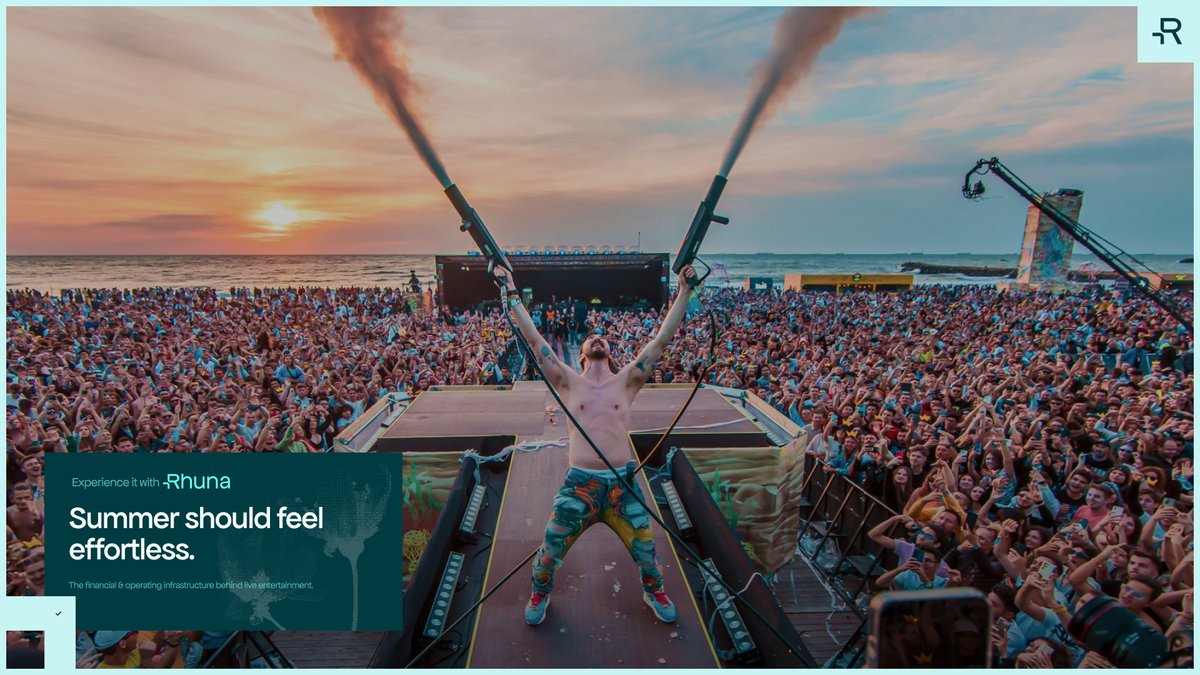

Every summer, millions of people move more money in a weekend than some towns move in a year.

And it all has to feel effortless.

Behind every drink, ticket, top-up, check-in, and vendor payout is a temporary financial system expected to work like a permanent one.

That’s the standard festivals create. And it’s why, through Rhuna, we’re powering the financial & operating infrastructure for live entertainment.

8

11

28

1,596

ᕈulsar on Base retweeted

Jun 4

Money carries more than value.

It carries people’s time, choices, plans, pressure, and freedom.

So the experience around it should help people feel a little more in control of what comes next.

Less weight to carry. More room to move.

3

10

35

1,201

ᕈulsar on Base retweeted

Jun 3

excited about @WalletConnect x @privy_io and @PulsarMoneyApp

stablecoins get more useful when they work across the ways people already pay: card, tap-to-pay, QR, wallet checkout, merchant rails

in simple: with these partnerships plugged in, spend from your non-custodial wallet balance as easily as scanning a QR

Jun 3

The next step for stablecoins is accessibility.

With WCP, Pulsar users will be able to spend directly from their Pulsar account, across wallets and merchants worldwide.

A fintech experience, abstracting the settlement through @privy_io & @WalletConnect.

5

5

43

4,183

ᕈulsar on Base retweeted

Jun 3

The next step for stablecoins is accessibility.

With WCP, Pulsar users will be able to spend directly from their Pulsar account, across wallets and merchants worldwide.

A fintech experience, abstracting the settlement through @privy_io & @WalletConnect.

Jun 3

The WalletConnect Pay ecosystem keeps growing.

Today at Money20/20, we're announcing the next wave of wallet partners going live with WalletConnect Pay.

Here's who's in ↓

4

14

48

6,505

ᕈulsar on Base retweeted

Jun 1

This week, the Pulsar Money team is heading to several events across EU & US.

From Paris to New York, we’ll be on the ground talking about what comes next for money movement, stablecoins, and the infra needed to make the next generation of fintech usable in everyday life.

2

10

31

2,499

ᕈulsar on Base retweeted

May 29

new generation of fintech

the Revolut & Wise generation was incredible. they disrupted a conservative market ruled by dinosaurs by making money movement feel natural. better onboarding, better FX, cleaner cards, faster notifications, a nicer app on top of a very old stack

but the next wave is different because the stack itself has completely changed:

→ stablecoins make settlement global and 24/7

→ self-custody lets the account belong to the user instead of the institution

→ bank rails and cards can sit at the edges of a stablecoin-native balance

→ DeFi protocols can sit underneath the account for swaps, yield, trading and credit

→ agents can start acting on clear rules and limits instead of leaving the user to manually move money between 5 products

the old fintech product was: take the bank, make it mobile

the new fintech product is: rebuild the financial account around money that moves, earns, settles and can be routed

the line I keep coming back to is:

→ everyone earns on your money. except you

banks earn on idle balances. card networks earn on every swipe. FX providers earn on every border. platforms earn on your deposits, transactions and data. the user is usually the last person to benefit from their own financial activity

that's why the next generation of fintech that wins will be the one that inverts that

your money should work for you first. it should earn while it waits, move globally when needed, stay under your control, and connect to the best financial infrastructure without forcing you to become a DeFi power user

Pulsar is our view on the consumer side of this

→ a stablecoin-native money app where your balance can spend, send, earn and eventually route itself more intelligently, while still feeling like a normal everyday app

and it all comes down to executing on that vision with surgical precision, because make no mistake, average consumers will accept nothing less

8

15

93

7,952

ᕈulsar on Base retweeted

May 26

yesterday’s post about credit-backed stablecoin cards brought up a lot of good conversations, especially around one question:

if the first wave of these products was debit-style, what does credit actually change?

with most stablecoin debit cards today, the payment flow is still very similar to a normal fiat account. you hold a balance and you spend from that balance

the infra may be different & the UX may be better, but the basic function is still the same.

credit, however, introduces a second layer:

instead of every transaction being a direct deduction from the balance, the account can start deciding how to use the user’s financial position more intelligently

that’s where the product starts to become more powerful because onchain credit can make a user’s money more flexible

the same $100 can sit in the account, back credit, earn yield, and still support everyday payments without being moved/sold

that matters in 3 practical ways:

first, it makes the account more capital-efficient. the user does not have to interrupt their position every time they spend. the card becomes access to liquidity

second, repayment can become programmable. incoming stablecoin flows, idle balances, or yield can reduce the credit line automatically based on rules the user sets. the experience can still feel like a normal card, but the account underneath can manage repayment much more intelligently than a monthly statement cycle

third, risk can be handled continuously. live LTVs, dynamic limits, top-up rules, repayment triggers, and alerts can sit inside the account instead of being exposed as a DeFi dashboard the user has to manage manually

for this to work, I think there are 2 underestimated challenges:

1/ UX - making DeFi great again by making it understandable to a regular consumer. both in terms of displaying info & managing account settings

2/ account logic - when to spend from balance, when to borrow, when to repay, when to route yield, when to top up collateral (and so on) - these sound like small product decisions, but they actually are the product. the flywheel works if all pieces are aligned

however, I think we're in for an exciting ride and credit on crypto infra can make everyone's dollars more useful once they are truly here

May 25

one thing after watching stablecoin cards lately

in the US, credit is the default. people "put it on the card" and the card almost always means credit. rewards, points, credit score, the whole social contract of how you spend lives there.

in most of europe and a lot of asia, the opposite. the card is debit. you spend what you have. credit is a separate product you opt into.

and i think this is what's actually shaping stablecoin cards right now

because the first wave of stablecoin cards is basically the european version. debit-style, spend crypto through a card. you swipe, your balance drops, you sold an asset to buy a coffee. useful, but it's the smaller version of the product

the next wave is the american version. credit attached to the account. you don't sell when you spend, you borrow against what you hold.

onchain, that architecture can actually be cleaner than the legacy version

collateral is liquid, transparent, programmable and composable. credit lines can sit behind the user experience, while settlement still happens in the format merchants already understand

this is why infra like @sprinter_ux is interesting

one credit line, collateral across chains, USDC drawn to a receiver address. for a card program, that receiver can simply be the settlement layer. user taps, USDC settles, the credit line sits behind the experience, and the user never has to think about chains

@Morpho matters for the same reason

not as the card layer, but as part of the credit and yield layer underneath the account. if stablecoin apps become real financial accounts, they need lending markets, curated vaults and idle-balance yield underneath them

so the cards are the interface people already understand, while the account behind the card is the actual product.

the goal is to make that feel normal to use, just like traditional credit accounts.

of course, still real work to do on risk, LTVs, liquidations, refunds, tax, compliance, chargebacks, but the direction is pretty clear;

and that's a big part of what we’re building at @PulsarMoneyApp

looking deeply in this space so let me know if you have any other ideas and views on these infra protocols we should take a close look at

1

3

12

1,184

ᕈulsar on Base retweeted

May 26

3

7

19

987

ᕈulsar on Base retweeted

May 26

NYC has some of the best coffee shops

will be there in a few days, excited to meet friends and have good chats over some exceptional coffee ☕

planning to try a few from @swang_co’s list below

May 9

best spots to lock in on a drizzly Saturday in NY 🌧️

- conwell coffee hall

- Georgie’s cafe

- haraz coffee house

- stone street

- cafe jalu

- mori coffee

- plantshed

- the lost draft

- toby’s estate in tribeca

- kings street coffee

- the blue bottle on broadway

- moshava

only including the few that are both laptop friendly over the weekend and with ample seating

for founders building/raising, come co-work with me next Sat!

1

3

10

772

ᕈulsar on Base retweeted

May 22

Ready for Pulsar coffee meet-ups in the US?

This summer, we’ll be hosting open spaces to talk fintech, AI, and what’s next - with close friends and new ones. ☕️

5

9

29

1,605

ᕈulsar on Base retweeted

May 25

one thing after watching stablecoin cards lately

in the US, credit is the default. people "put it on the card" and the card almost always means credit. rewards, points, credit score, the whole social contract of how you spend lives there.

in most of europe and a lot of asia, the opposite. the card is debit. you spend what you have. credit is a separate product you opt into.

and i think this is what's actually shaping stablecoin cards right now

because the first wave of stablecoin cards is basically the european version. debit-style, spend crypto through a card. you swipe, your balance drops, you sold an asset to buy a coffee. useful, but it's the smaller version of the product

the next wave is the american version. credit attached to the account. you don't sell when you spend, you borrow against what you hold.

onchain, that architecture can actually be cleaner than the legacy version

collateral is liquid, transparent, programmable and composable. credit lines can sit behind the user experience, while settlement still happens in the format merchants already understand

this is why infra like @sprinter_ux is interesting

one credit line, collateral across chains, USDC drawn to a receiver address. for a card program, that receiver can simply be the settlement layer. user taps, USDC settles, the credit line sits behind the experience, and the user never has to think about chains

@Morpho matters for the same reason

not as the card layer, but as part of the credit and yield layer underneath the account. if stablecoin apps become real financial accounts, they need lending markets, curated vaults and idle-balance yield underneath them

so the cards are the interface people already understand, while the account behind the card is the actual product.

the goal is to make that feel normal to use, just like traditional credit accounts.

of course, still real work to do on risk, LTVs, liquidations, refunds, tax, compliance, chargebacks, but the direction is pretty clear;

and that's a big part of what we’re building at @PulsarMoneyApp

looking deeply in this space so let me know if you have any other ideas and views on these infra protocols we should take a close look at

12

14

111

19,956

ᕈulsar on Base retweeted

May 25

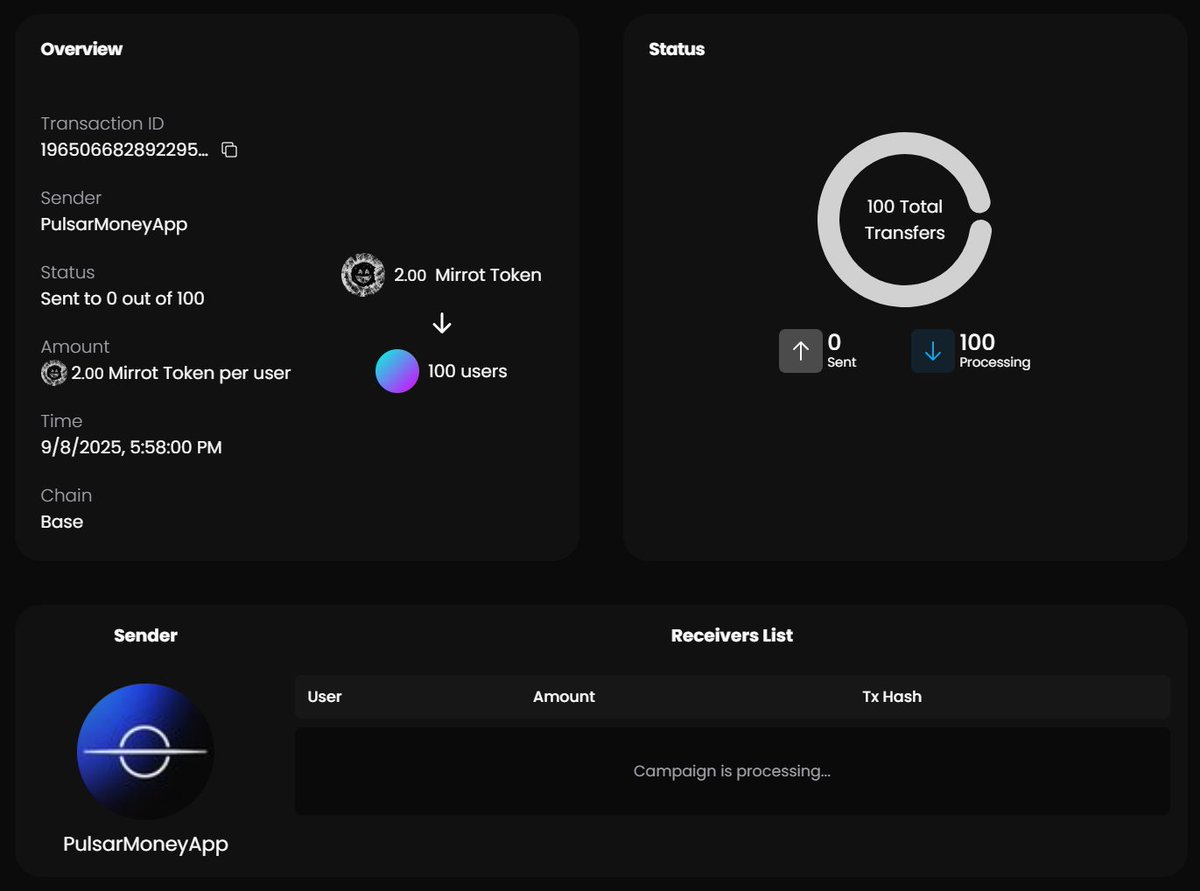

Leaderboard rewards are now live on EthraShip Portal!

🔹 1,500 $USDC prize pool.

🔹 app.ethraship.io

Complete tasks, invite friends, and reach Top 10 to qualify for rewards.

22

32

77

4,974

ᕈulsar on Base retweeted

May 22

Neobanks & payments infra are becoming one of the most important conversations in fintech.

Next Tuesday, we’re hosting an X Space with @xMoney_com to talk about what next-gen of financial products need to get right.

Set a reminder 👇

x.com/i/spaces/1pKkOyklwDXKj

4

16

49

7,618

ᕈulsar on Base retweeted

May 22

Pulsar cafe coming this summer to SF & NY ☕

2

4

19

2,141

ᕈulsar on Base retweeted

May 19

/Pulsar make me breakfast

not really but, you will be able to order breakfast from your favorite restaurants nearby via Pulsar soon

from unsubscribing to ordering things online to managing the portfolio, the Pulsar AI module will be quite a big differentiator

May 19

Just ask & it gets handled.

Building the Pulsar fintech app from the ground-up with AI native capabilities means you can manage your life easier, faster, and with more control.

It's time to lock in.

3

6

21

1,725

ᕈulsar on Base retweeted

May 19

we’re big believers that social profiles will become part of how payments work

from our social media payments module, to the social layer inside the Pulsar Neobank, to what we’re building with @r3vl_xyz, this is a vertical we’re excited to push forward

more on Reveel x Pulsar soon

May 19

You can messages to anyone in the world in seconds. But try sending them $10.

5.5 billion people are connected via messaging.

Yet, we still hear this:

- "Do you have CashApp?" "No, only Venmo"

- "Do you take Dollars?" "No, only Pesos"

- "Can I send you USDC?" "No, only USDT."

That conversation is happening millions of times a day.

We built Reveel to make it disappear.

Reveel is the first global peer-to-peer network that lives inside your messages and works on top of the wallet you already have.

Starting today, we’re opening our APIs to third-party wallets and banks — so they can integrate native, messaging-first P2P payments directly into their own products.

No new app. No complex addresses. Just send.

Hundreds of thousands of users across 100 countries. Millions of transactions. And we’re just getting started.

The financial layer for how the world already communicates. Let’s build it together with @r3vl_xyz.

7

6

30

1,634

May 19

x402 looks good over here

May 19

Just ask & it gets handled.

Building the Pulsar fintech app from the ground-up with AI native capabilities means you can manage your life easier, faster, and with more control.

It's time to lock in.

1

48

May 18

based

May 17

the SF house that helps founders build, raise, cook and go viral

went to @theresidency dinner, met great builders, heard crazy stories and got to chat with @GilboaAmitay after seeing him go viral the day before

one of our portfolio companies is there too, excited to share which soon

founders in locked in mode. the energy there is very much in the spirit of SF, impressed by @theresidency project and people there

1

103

ᕈulsar on Base retweeted

May 17

the SF house that helps founders build, raise, cook and go viral

went to @theresidency dinner, met great builders, heard crazy stories and got to chat with @GilboaAmitay after seeing him go viral the day before

one of our portfolio companies is there too, excited to share which soon

founders in locked in mode. the energy there is very much in the spirit of SF, impressed by @theresidency project and people there

May 11

We got an 8-figure acquisition offer 2 days after launch.

We said no, because the problem we're solving is worth way more than that.

It’s 2026, but teams are only getting lonelier, and context is still the problem.

The issue isn’t intelligence. Your team has plenty of that.

It’s shared memory and context, the thing that makes 10 A-players feel like 1.

That’s what we’ve solved with @playdotfast, while making work more fun.

We're killing traditional SaaS, and believe you me, we're leaving no holds barred.

3

4

21

1,501