nothin, just chillin

Joined July 2010

- Tweets 2,992

- Following 785

- Followers 595

- Likes 7,215

237 Photos and videos

Robert retweeted

There are people with months of recorded activity on dFusion right now.

Queries, ratings, contributions. The network logs all of it at the individual level, on-chain. Operators accrue even faster because activity flows through their infrastructure.

None of it resets when the network goes live.

testnet.dfusion.ai/

10

11

81

1,834

Robert retweeted

The Truth About Cloud Costs

Who Is Paying the Rent in the AI Era?

*On the quiet rise of cloud infrastructure costs*

As the AI industry has accelerated, the thing that has grown fastest is not model performance. It's the price of compute.

In 2023, the average hourly cloud rental cost for an NVIDIA H100 GPU sat around $2 to $3. By mid-2024, that number had climbed to $4 to $6. By 2025, some regions were reporting hourly rates as high as $8 to $10. Same hardware, same usage hours, but the price has doubled or tripled. Meanwhile, AWS, Azure, and GCP have grown their AI workload revenue by more than 50% annually.

These numbers tell a simple story. **Someone is paying more rent every year.**

Who absorbs the rent

Look at the P&L of nearly any AI startup, and the largest line item is, with rare exception, cloud infrastructure. OpenAI runs on a structure that would be impossible without Microsoft's Azure credits. Anthropic depends heavily on AWS. The companies smaller than them have it worse — 30 to 50 percent of their revenue flows directly to cloud providers.

That cost ends up somewhere. Some of it is passed to users through price hikes. Some is absorbed through margin compression and pushed onto investors. And some is paid through closure — companies that simply couldn't sustain the cost and disappeared from the market.

The bigger problem is that the pricing power sits in the hands of three companies. AWS, Azure, Google Cloud. Together they hold more than 65 percent of the global cloud market. Pricing in this space is not the result of competition. It is closer to a cartel.

The economics of distributed infrastructure

This is where distributed infrastructure becomes meaningful. Not because "decentralization is good" as a slogan, but because without distributing pricing power, the cost structure of the AI era is fundamentally unsustainable.

A distributed compute network can run on a different cost structure. A node operator only needs to recover their electricity bill and hardware depreciation. The real estate, marketing, and shareholder dividends that big cloud providers build into their pricing simply don't enter the equation. That's where the math for delivering the same unit of compute at half the price comes from.

Distributed infrastructure isn't a fit for every workload. Ultra-low-latency training and single-shot training of the largest models will continue to live in centralized data centers. But inference, fine-tuning, distributed training, and data storage — these are workloads that can move to distributed infrastructure today. And these workloads, in aggregate, are where most AI spending actually happens.

To summarize

Infrastructure costs in the AI era will keep rising. Models will grow larger. Inference demand will explode. Data center power costs are already approaching their limits. In this trajectory, someone has to pay more rent each year.

The question is whether that rent continues to flow to three companies, or whether it gets distributed to the participants of an actual network. That single choice will define the next decade of AI-era infrastructure.

4

3

18

685

Robert retweeted

The chain I trust most with my project is Abey because _________.

8

24

117

2,995

Robert retweeted

Earn points when your friends use AI.

We bet you can’t name one friend who doesn’t use AI. Everyone uses it. So why not earn rewards from it?

Introducing Subnets: Get rewarded on behalf of other people’s activity.

Get points with real value from every query. Here’s how:

58

55

466

11,786

Robert retweeted

Jun 3

“The mission of Sodax is to enable all users to experience the power of DeFi.”

@real_digidavid, Head of Marketing at @gosodax, sat down with @DavidThaDegen to discuss accessibility, adoption, and the long-term vision for DeFi.

0:27 - Thoughts on @consensus2026

1:23 - What Is Sodax?

2:25 - David's Role at Sodax

3:18 - Who Sodax Is Built For

4:45 - David's Background

6:26 - The Evolution of the Industry

8:55 - The Vision of Sodax

11:04 - Advice for Listeners

Watch the full episode below!

12

22

57

2,561

Robert retweeted

Jun 3

Founder & CEO of @Tokenomist_ai, @apewagmi, joined @DavidThaDegen at @SEABWofficial to talk about onboarding, building in the space, and what they hope to achieve.

0:37 - Diving Into Tokenomist

1:00 - Onboarding New Users

1:52 - Inspiration for the Project

2:52 - Do They Attend Many Events?

3:03 - What They'd Like to Achieve

3:55 - Advice for Builders in Thailand

5:19 - Where to Find Them

Watch the full episode below!

12

34

90

2,725

Robert retweeted

The purchase takes 2 minutes.

The position you're buying into is what matters.

dFusion subnet holders don't use the network. They operate inside it. Data rubrics, verified contributors, knowledge pipelines. All routed through your infrastructure. All tracked on-chain.

Referral code gets you 15% off.

Pay with ETH on Arbitrum.

When the network goes live, every verification event, every data flow, every query runs through an operator's slot.

There are a limited number of slots.

testnet.dfusion.ai/claim-sub…

8

57

249

6,130

Robert retweeted

May 29

.@MehowHacks, CEO & CTO of @Americanfort_io, joined @DavidThaDegen at Consensus Miami 2026 to talk about digital security, user experience, and the problems they’re solving.

0:18 - Thoughts on @consensus2026

2:14 - Diving Into American Fortress

7:13 - The Problem They’re Solving

14:30 - Is There a Difference in User Experience?

16:49 - Keeping the Rollout Simple

17:25 - Mehow’s Motivation

20:13 - Where to Stay Up to Date

Watch the full conversation below!

11

15

76

5,817

Robert retweeted

May 26

“People learn by doing.”

@rjvollono, CCO at @stbl_official, joined @DavidThaDegen to talk about adoption, community feedback, and how users are engaging with crypto around the world.

1:06 - Meet Joe STBL

2:57 - How They’re Driving Adoption

3:40 - Inspiration from Countries Using Crypto Daily

5:47 - The Importance of Community Feedback

6:13 - Where Their User Base Is

8:10 - Joe’s Background

11:36 - Where to Stay Up to Date

Watch the full conversation below!

11

22

93

2,643

Robert retweeted

May 25

Privacy, compliance, and institutional adoption all have to work together.

@ActionCEO sat down with Amanda Martin, COO of @CantonFdn, to talk about the network, developers building on it, and what comes next.

0:25 - What Is Canton

0:41 - Who’s Building on Canton

1:35 - Why Builders Choose Canton

2:14 - Why They Attended @EthereumDenver

4:11 - What Comes Next

5:46 - Privacy KYC

6:39 - What She Wants to See Built

7:10 - Getting More Developers Involved

8:05 - How the Network Works

10:26 - Where They’ll Be This Year

11:18 - How Devs Can Learn to Build on Canton

12:33 - Getting Started

13:03 - What She Wants to See on the Network

Watch the full conversation below!

12

18

119

5,631

Robert retweeted

May 22

.@Jason_Barraza_, Institutional BD Lead at @RedStone_DeFi, joined @DavidThaDegen to talk about onboarding, growth, and what RedStone is building toward.

0:51 - Diving Into RedStone

3:13 - What Excites Jason

4:51 - What RedStone Wants to Achieve

6:10 - Onboarding

7:10 - Where to Find Them

Watch the full clip below!

11

14

111

4,296

Robert retweeted

May 22

Happy Bitcoin Pizza day 🍕

Bitz is giving away 210k $SATS for RT reply on the post below

May 22

10,000 $BTC bought two pizzas in 2010, we're giving away 210 pizzas today! 🍕

To enter:

- Order or make 1 pizza, write "Bitz 2026" on a piece of paper, take a photo, and post it tagging us

21,000 SATS for the first 210 entries will be added to your Bitz balance, no wager.

No AI or stock photos. Real pizzas only

Happy Bitcoin Pizza Day!

60

9

92

2,344

Robert retweeted

May 22

According to @zachxbt, The @Polymarket UMA CTF Adapter contract appears to have been exploited on Polygon.

Users should stay cautious and avoid unnecessary interactions until there is official clarification from or.

Attacker address: 0x8F98075db5d6C620e8D420A8c516E2F2059d9B91

36

3

86

8,797

La primera temporada de trading en @Onchaincc by Bitso, ya está en vivo. 300,000 USDC en premios.

Opera futuros perpetuos y memecoins para subir en el leaderboard. Crea tu cuenta.👇

6

23

64

6,691

Robert retweeted

May 15

12

33

119

4,974

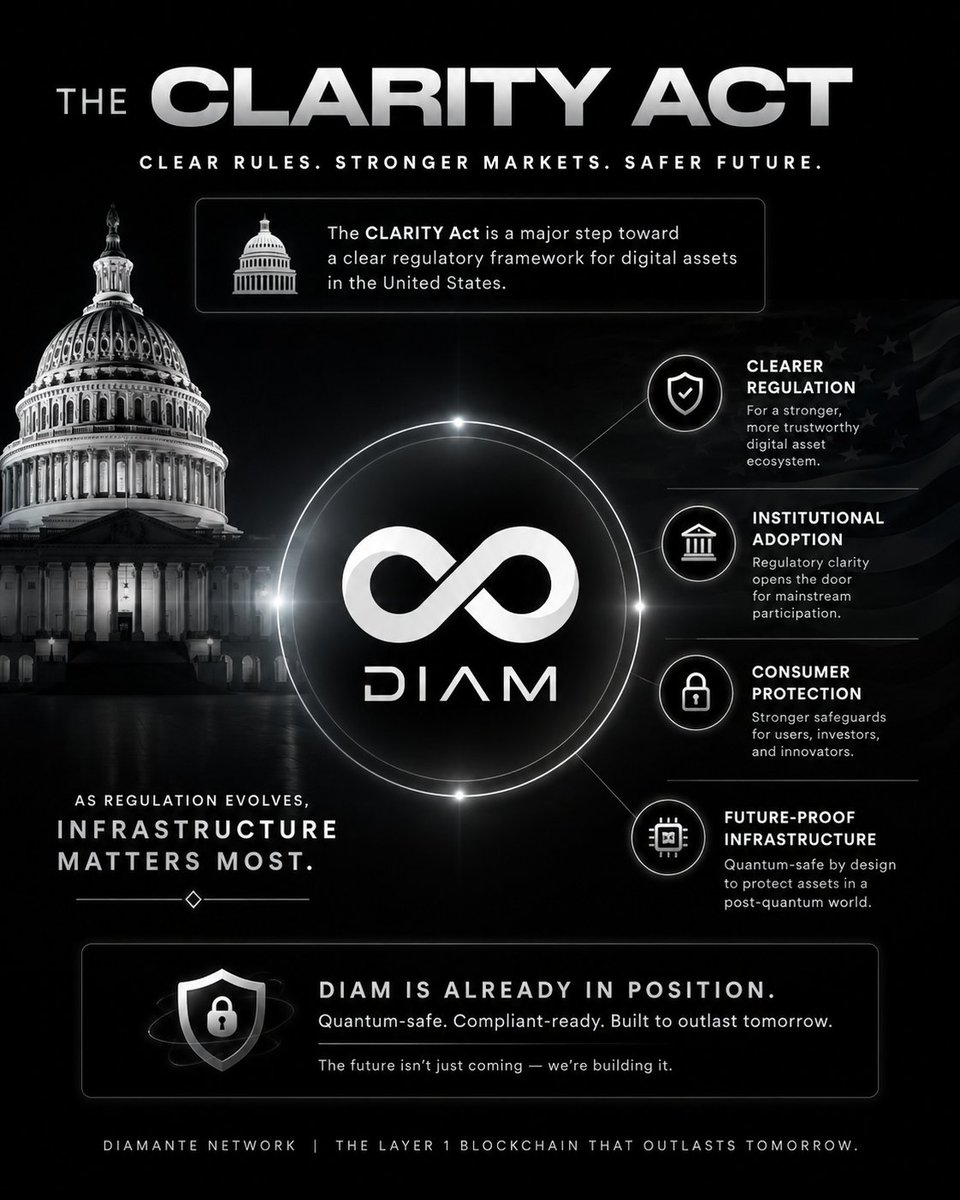

Today’s CLARITY Act markup is bigger than most people realize.

Crypto regulation is moving toward:

• Consumer protection

• Institutional standards

• Infrastructure security

• Long-term resilience

━━━━

Now add quantum computing to that equation.

Most blockchains still need to figure out how they will secure assets against future quantum risk.

Diam already has quantum safeguards built into its infrastructure.

As regulation and institutional adoption accelerate, security will become one of the biggest differentiators.

25

18

80

11,170

Most people still think quantum is a future problem.

• Governments are already preparing.

• Institutions are already positioning.

• Infrastructure is already shifting.

• Scammers are already collecting your data.

The timeline is shorter than most realize.

@diamante_io was built for this reality from day one.

26

12

76

9,324

Great IP makes content easier.

@bearish_af gives creators something fun to build with.

The rest comes down to imagination.

Quality over quantity.

21

9

59

5,867