Head of Global Policy Research at Piper Sandler. Former founding partner of Cornerstone Macro and Federal Reserve senior staff member.

Joined January 2020

- Tweets 2,795

- Following 201

- Followers 11,534

- Likes 1,595

816 Photos and videos

17 Oct 2022

Three things that are wrong with this tweet.

1. There was one error—certainly consequential, but one, not four. The forecast was wrong, and from there everything else followed.

1/3

17 Oct 2022

An independent #FederalReserve is critical to the well-being of the US #economy. Having said that, it is getting harder to justify such independence when four big operational errors (of analysis, forecasts, actions and communication) are accompanied by a lack of accountability.

4

6

57

17 Oct 2022

2. The Fed is not unaccountable. That's why the chair testifies at least twice a year before Congress. Congress is the boss, and Powell was confirmed with 80-19 votes just a few months ago. Not a lot of unhappiness by the boss, apparently.

2/3

2

1

20

17 Oct 2022

3. What is the alternative?? Are we expected to think that the Turkish model is better? If a central bank's independence was questioned every time it makes a forecast error, inflation and a lot of other things would be a lot worse.

3/3

2

2

39

10 Oct 2022

Hard for me to imagine someone more deserving of the Nobel prize in Economics than Ben Bernanke. Congratulations to him and @BrookingsEcon.

10 Oct 2022

Congrats to our Hutchins Center colleague Ben Bernanke! @BrookingsEcon nobelprize.org/

1

1

7

4 Oct 2022

Some more color around @jeannasmialek tweet.

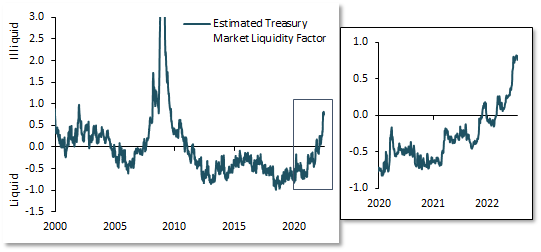

The point was to say that we are not close to Treasury market dysfunction becoming a constraint to #Fed policy. Even if reserves keep declining at recent pace, it will still be at least 7 months before problems arise. 1/3

4 Oct 2022

How far can Fed QT go before the Treasury market goes from illiquid to dysfunctional?

@R_Perli estimates: "reserves may not shrink more than an additional $500-750 billion without inducing a dysfunctional Treasury market."

a.k.a. at least 7 months at the current pace.

1

5

17

4 Oct 2022

But the #Fed can do a few things to slow the shrinking of reserves (lower RRP rate, lower counterparty RRP limit, rise IOR). Banks could also offer more competitive deposits. The peak rate could be reached before 7 months. Any of this would push the limit farther out. 2/3

1

2

6

4 Oct 2022

Bottom line, a lower inflation or a deteriorating labor market are more likely catalysts for a #Fed "pivot" than trouble in the Treasury market. 3/3

2

1

18

22 Sep 2022

It was a pleasure to discuss the September #FOMC meeting, the outlook for #Fed policy, and many other issues with @sobel_mark of @OMFIF today. Thank you Mark for the invitation. Full discussion in the link below.

omfif.org/videos/the-fed-and…

4

10

21 Sep 2022

The #FOMC projections for the unemployment rate are a giveaway that they think a recession is coming. There has never been a situation where the UR increased more than ~0.5% without a recession.

12

65

191

19 Sep 2022

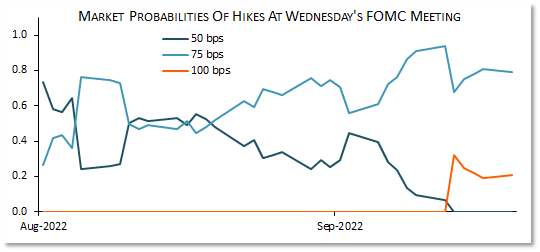

Another hawkish #FOMC meeting this week.

- Odds of 100-bp hike greater than the 20% the mkt prices in and close to 50%

- Dots to show FFR above 4% this year and a bit higher in '23

- Powell will try to sound hawkish, but experience suggests room for mkt misunderstanding. 1/3

5

15

49

19 Sep 2022

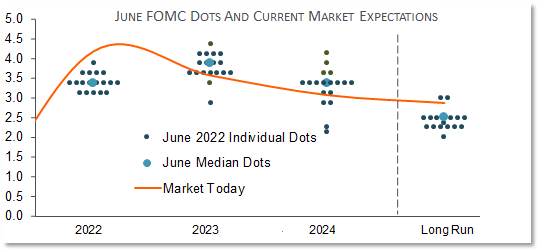

2023 and '24 #FOMC dots will be above current mkt pricing. Still, don't expect the market to fall in line b/c mkt expectations are averages across many scenarios, and there are scenarios in which the Fed will have to cut substantially next year. The mkt needs to price those. 2/3

4

5

15

19 Sep 2022

In any case, dots beyond this year are just guesses and subject to large changes, just like recent sets. What the #Fed will do in 2023, 2024, and 2025 depends on inflation and employment, not on what the dots will show on Wednesday. 3/3

3

22

13 Sep 2022

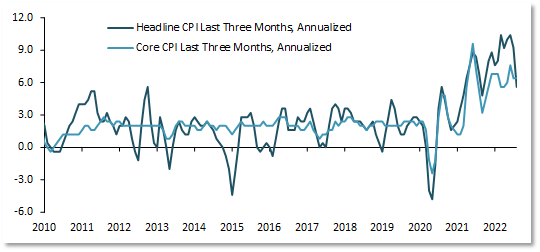

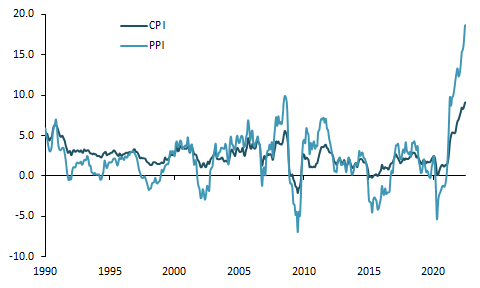

Another bad CPI report, comparable to June or July. A 0.6% MoM core CPI number is just not good.

The #Fed will want to see a series of MoM numbers annualizing to less than 3% before relenting. For now, we are not even remotely close. 1/2

2

12

40

13 Sep 2022

The #Fed will probably still hike by 75 bps next week (as expected before today's CPI report.

But then, for Nomember and December, it will likely be either 75 bps/25 bps or 50 bps/50 bps as equally plausible base cases. Either way, above 4% at year end. 2/2

6

25

1 Sep 2022

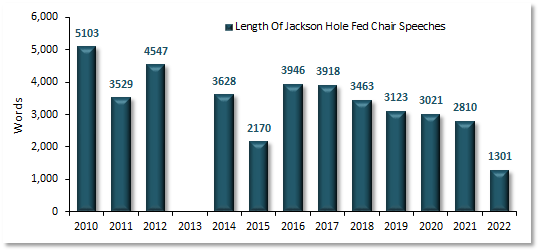

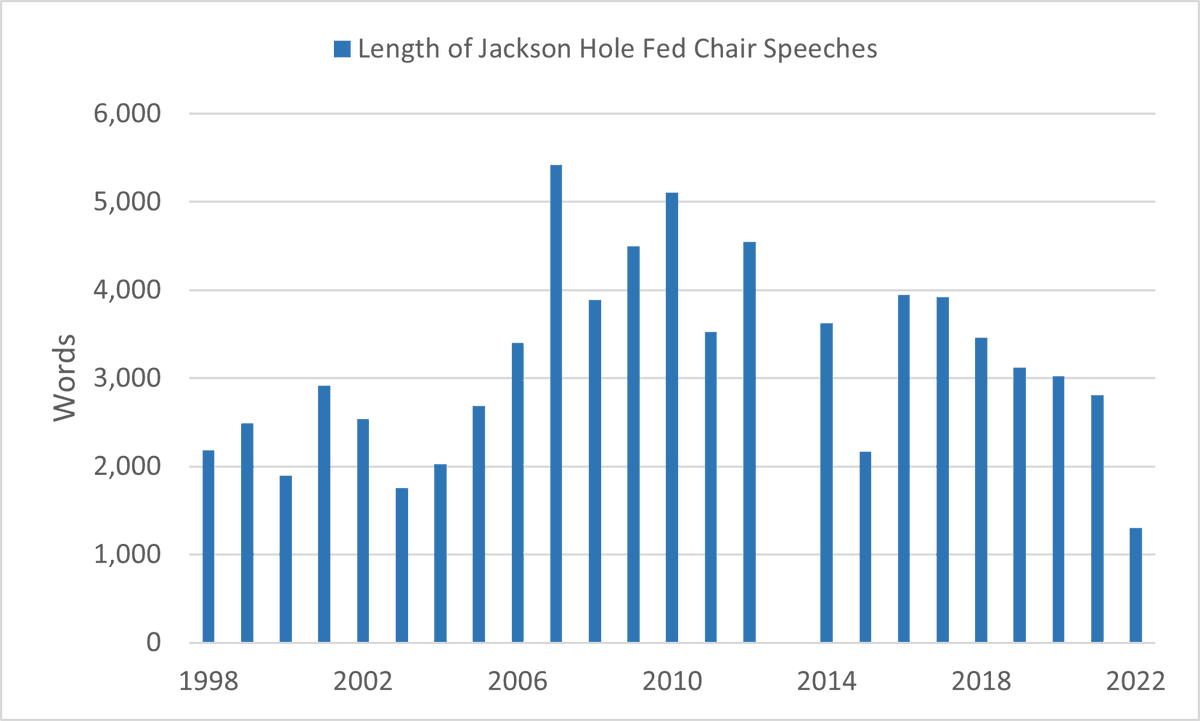

Powell's speech at Jackson Hole was the shortest by a Fed chair there since at least 1998.

Short to the point = good.

31 Aug 2022

Could only go back to 1998 via Fed archive. Unsure where to get 1978-1997

federalreserve.gov/newsevent…

federalreserve.gov/newsevent…

3

17

26 Aug 2022

A very welcome development: Powell's speech today was the shortest speech by a Fed chair (or vice chair) at Jackson Hole since at least 2010 (and probably well before that--I didn't have time to go back more).

Less than half of last year's length, and 1/4 of Bernanke's in 2010.

13

32

132

26 Aug 2022

Powell really didn't say anything shocking today from the point of view of the bond market: Expectations for rate hikes moved up only marginally.

But the stock market might be internalizing that there was no dovish pivot in July and that there won't be one any time soon.

10

41

242

5 Aug 2022

Brief thread on today's employment report.

This strong report *increases* the odds of recession. Aside from the payroll number, two things are distressing for the #Fed:

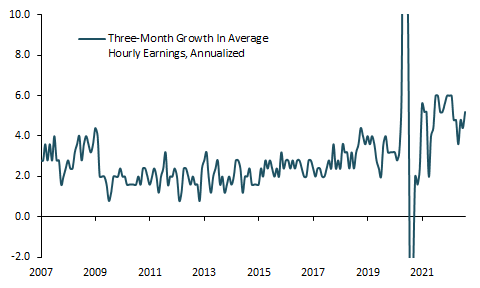

1) Average hourly earnings are annualizing 5.2% for the past 3 months and pointing up-way too high. 1/4

20

81

315

5 Aug 2022

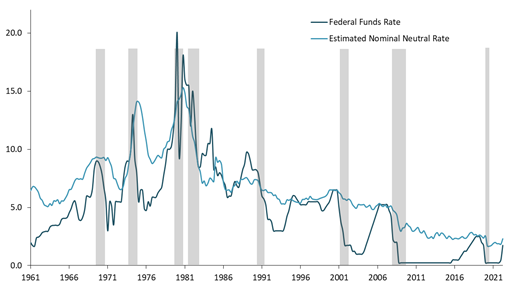

Since 1960, every time the #Fed tightened to or above neutral the economy entered recession. Hard to make a case as to why it should be different this time.

This jobs report was too strong. By incentivizing the Fed to hike even more, it makes recession even more likely. 4/4

7

15

117