Joined November 2020

- Tweets 250

- Following 451

- Followers 18,258

- Likes 1,461

42 Photos and videos

Pinned Tweet

May 12

$ROO is now live on @virtuals_io!

CA: 0xE31700c6BD46638D207991fB5CC5c0daD3D1e3DA

83

152

351

23,725

Jun 11

The Ratehopper LP Agent (v7 model) just flipped from OUT OF POOL → SAFE TO RE-ENTER

• Market stress indicators have cooled

• Volatility is back in normal range

• Flow/funding signals stabilized

• Drawdown risk is contained (-4.49% 7D)

• No active “extreme risk” conditions detected

The v7 model agent is now re-entering LP positions as markets stabilize.

V8 and v9 models still recommend staying out of the pool. Agents keep monitoring the situation.

4

38

47

872

Jun 11

Disclaimer from our agents:

This is not financial advice. LP strategies involve smart contract risk, market volatility, and potential impermanent loss. Backtests and signals reflect historical/model-based performance and do not guarantee future results.

1

2

226

Ratehopper retweeted

Jun 1

Shred Security🤝@RatehopperAI

Proud to announce the security partnership between Shred Security and @RatehopperAI — an innovative AI-powered platform that enables self-repaying loans by autonomously borrowing against your crypto assets, deploying capital into yield strategies, and repaying debt through intelligent rate optimization and refinancing.

This marks our third engagement with the Ratehopper team. As the protocol rapidly grows, security remains their top priority.🫡

2

2

16

1,031

May 28

We’ve already started integrating Base MCP. Soon, you’ll be able to create and manage Ratehopper agents directly via Base MCP.

Introducing Base MCP

Your agent's new gateway to Base

→ Connect an agent to your Base Account

→ Enable it to swap, trade, and manage your portfolio

→ Use plugins from leading apps on Base

The next stage of the agentic onchain economy

16

157

210

3,322

May 26

We're in good company.

Excited to see @bigwil's @pantheonvaults Creator Index go live today.

As a founding launch partner:

Support $BWIL by holding $ROO.

Support $ROO by holding $BWIL.

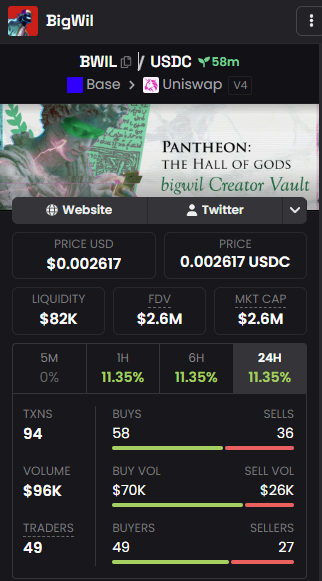

Okay... My creator index on @pantheonvaults on @base is officially live for public trading!

$BWIL ca: 0xd830cAb9F54618a111aa1197d480885e8AA9f289

Enjoy!

1

3

17

965

Ratehopper retweeted

May 21

u know whats gonna happen next

I'm excited and very pleased to announce that I'll be partnering with the @RatehopperAI team on @virtuals_io through 2026 and beyond as they become the fifth team to join my @pantheonvaults creator index, which is set to launch early next week!

I've known the Ratehopper team for over six months and watched them build to this point. They align perfectly with my own vision, and the vision I have for my creator index, which is long-term!

They've built for many months prior to launching the $ROO token in recent weeks. Their product, which is the first agentic self-repaying loan protocol, has all of the potential in the world in my opinion!

Give them a follow and stay tuned for more details on how you can gain exposure to their project via my creator index!

13

4

53

4,989

May 21

Excited to be partnering with @bigwil, a longtime @virtuals_io supporter, as he launches his creator index through @pantheonvaults.

We believe this is a more transparent and mutually beneficial model for ambassador relationships. Instead of one-sided promotion deals, creator index participants can gain exposure to the same deal flow and projects creators themselves are backing.

@bigwil has supported Ratehopper long before launch, and we couldn’t have asked for a better partner to build alongside.

I'm excited and very pleased to announce that I'll be partnering with the @RatehopperAI team on @virtuals_io through 2026 and beyond as they become the fifth team to join my @pantheonvaults creator index, which is set to launch early next week!

I've known the Ratehopper team for over six months and watched them build to this point. They align perfectly with my own vision, and the vision I have for my creator index, which is long-term!

They've built for many months prior to launching the $ROO token in recent weeks. Their product, which is the first agentic self-repaying loan protocol, has all of the potential in the world in my opinion!

Give them a follow and stay tuned for more details on how you can gain exposure to their project via my creator index!

8

29

64

2,863

May 14

Agents will eat the world.

4

1

38

1,988

Congrats to the @RatehopperAI team for a successful launch on @virtuals_io

~$6.5m ATH on launch for $ROO pulls in some healthy capital through ACF.

The team detailed all of their plans yesterday on @VirtualsWeekly Episode 102, and I've had them at A Tier for a while now so this result isn't a surprise!

Using capital to borrow against, and then deploying it to make a healthy margin, sounds simple, but an end to end agentic solution is more complex than you might think.

Ratehopper has solved for this, and there's a big blue ocean of opportunity ahead!

Despite the lack of quantity on the Virtuals launchpad (it's changing soon btw), we've still got quality!

8

12

68

105,253

May 12

Thanks to our community for making us aware of this, we have completed the process to get the correct information updated on @dexscreener ASAP

May 12

Check the Dexscenner profile, the scammers have updated it.

2

1

18

2,365

May 12

We're pleased to announce we've submitted our @CoinGecko application.

Request ID: CL1205260049

geckoterminal.com/base/pools…

8

3

29

1,657

May 12

How Ratehopper's LP Agent Works ⚡️ ⤵️

A simple example: $1,000 in $ETH collateral

Say you deposit $1,000 worth of ETH as collateral on @Base.

At 50% LTV, the agent can borrow $500 USDC against it. If the borrow rate is around 5% APY, that comes out to roughly $25 per year in interest, or about $0.07 per day.

When conditions are favorable, the agent deploys the borrowed USDC into a concentrated ETH/USDC @Uniswap LP position to capture trading fees.

Based on our live data, active concentrated LP positions in this pair can generate 25-80% APY in trading fees depending on range, volatility, and market conditions.

Using a 35% APY example, the $500 LP position would generate about $175 per year in fees, or roughly $0.48 per day.

That creates a simple spread:

$0.48 earned per day - $0.07 owed per day = $0.41 profit per day flowing back toward the debt.

In this example, the $500 loan could be repaid in just over 3 years, while your $1,000 ETH collateral remains yours the whole time, with full upside if ETH appreciates.

Your agent is not just sitting still the entire time either.

It monitors borrow rates across @Aave, @Morpho, @Compound_xyz, and other lending markets in real time. If a materially better rate appears, the agent can refinance the debt in a single transaction, moving your loan to the cheaper protocol without you doing anything manually.

Before the agent starts, you choose your risk profile.

You can borrow more conservatively with a lower LTV, or deploy more capital with a higher LTV. You can also choose tighter or wider LP ranges depending on how much fee concentration and market flexibility you want.

The agent is also built to respond when market conditions change.

A sharp ETH move can push an LP position out of range, fees can stop, and the position can take on more risk while debt remains open. Ratehopper agents handle this through an exit signal engine that monitors volatility, onchain sentiment, options markets, futures markets, and broader regime changes.

The agent also runs continuous z-score monitoring across key protocol metrics, including utilisation rates, liquidity depth, and onchain activity. If any of these deviate significantly from historical norms, it can be an early signal that something is wrong. A sudden spike in utilisation, for example, can be one of the first onchain signs of a protocol exploit, liquidity crisis, or counterparty stress.

When the agent detects an anomaly like that, it can exit the LP position, repay outstanding debt, and move to safety before the damage spreads.

When conditions stabilize, it can re-enter.

You keep the ETH exposure and generate positive cash flow while the loan manages itself. And when the market gets dangerous, the agent gets out.

10

30

79

7,236