Event Driven, Deep Value w/ Catalyst, Real Assets, EM. 中文/Eng

Joined June 2021

- Tweets 12,755

- Following 5,056

- Followers 3,008

- Likes 18,367

630 Photos and videos

11 Nov 2025

Spectacular news for $CSR shareholders. Which mid-cap REIT is next?

ir.centerspacehomes.com/corp…

11 Nov 2025

🏢 Centerspace Reportedly Weighs a Potential Sale

Centerspace $CSR — a multifamily REIT focused on apartment communities across the U.S. Midwest and Mountain West — is exploring strategic options, including a possible sale, according to sources familiar with the matter.

💼 Key Details

* Exploring strategic options: The company is working with advisers to review takeover interest.

* No final decision yet: Talks are in the early stages, and Centerspace could still decide to remain independent.

* Market reaction: Shares rose 2.5% to $60.22 on Tuesday following the report.

🏘️ Portfolio Snapshot

* 13,000 apartment units across 85 properties.

* Core markets: Minneapolis, Denver, and Salt Lake City.

* Secondary markets: Grand Forks (ND), Billings (MT), Rapid City (SD), and other smaller Western cities.

* Strategy: Focused on stable, workforce-oriented housing in mid-sized and overlooked growth markets.

* Market cap: Roughly $1 billion.

📉 Recent Performance

* Shares are down 9% year-to-date, underperforming the broader apartment REIT sector.

* Faces similar headwinds as other multifamily REITs — rising financing costs, soft rent growth, and limited transaction liquidity.

🧭 Why It Matters

* A sale would mark one of the first major mid-cap apartment REIT takeovers since interest rates surged in 2022.

* Centerspace’s Midwest and Mountain West footprint could appeal to private equity or larger REITs seeking diversification outside high-cost coastal markets.

* As capital markets stabilize, multifamily M&A is expected to pick up — positioning Centerspace as a possible early mover.

investing.businessweek.com/n…

1

5

3,389

11 Nov 2025

Theoretically $CSR should be sold at up to $90/sh (high 5s), but given recent precedents, I would expect a valuation closer to $75-80/sh (low to mid 6s) reflecting a 25-33% deal premium.

2

2

946

Huge disappointment with $CSR strategic review, tiny deal, cap rate not disclosed (suggestive of FFO dilutive deal). Seems like institutional appetite for multi-family is possibly tapped out.

1

1

329

PE bros at Jardine are back to acquiring random assets. NAV discount should widen to historical levels to reflect empire building. I’ve rotated my Jardine / HK Land positions into Swire B class shares, which offer much better value.

1

237

$IMAX finally up for sale, its China sub $1970.HK accounts for ~50% of group NPAT, nearly 100% of historical cumulative FCF, trades at low single digit EBITDA mul vs. Parentco trading at a mid-teens mul. Chain rule applies to HKSE companies making the situation highly asymmetric.

2

2

544

29 Jun 2023

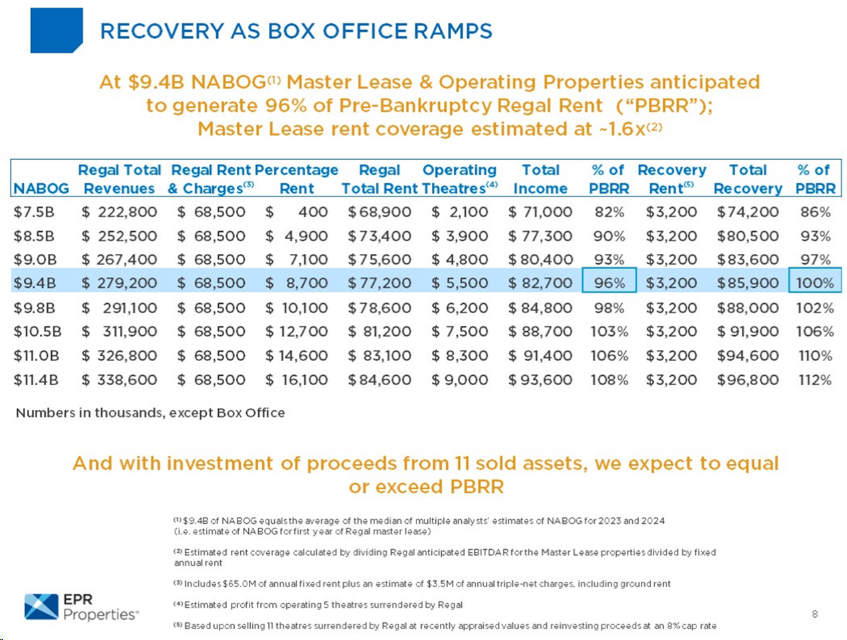

$EPR restructuring of theatre leases with Regal, estimated to generate 96% of pre-bankruptcy rent, and 100% or pre-bankruptcy rent after reinvestment of asset sale proceeds.

2

5

2,259

25 Sep 2025

$EPR selling its casino ground lease to Genting for $200mn at undisclosed "highly attractive cap rate". Transaction deleverages $EPR to sub 5x ND/EBITDA and funds growth for 2026, ATM tap no longer on the horizon. asgam.com/2025/09/17/genting…

1

2

996

$EPR quietly hikes its dividend by 5%, still trades at an 8 cap.

1

1

1

424

Maybe this will be the year for $VRE liquidation, hard to believe that activism started in 2018, when $CLI traded at $18-20/sh. Nearly 8 years later, a realistic exit value is $18-24/sh.

🚨 Erez Asset Management Encouraging $VRE Veris Residential to Explore Options 🚨

Reuters out with a story that Bruce Schanzer is urging the company to put itself up for sale, arguing a transaction could reward shareholders with a 70% premium to the real estate investment trust's current share price.

Erez Asset Management wants the company to begin a formal review of strategic alternatives and to publicly announce and fully market the process as it is pressing management and the board to act quickly and boldly now that its three main competitors have announced similar reviews.

reuters.com/legal/transactio…

1

5

1,363

Good riddance to $VRE, takeout valuation of $19/sh at the low-end of expectations, but takes out a serial underperformer from my portfolio. Veris Residential to be taken private in $3.4 billion all-cash deal - reuters.com/legal/transactio…

281

25 Jun 2025

Mr Market is offering a rare opportunity to buy Airports of Thailand $AOT.TB at a 50% discount.

20

17

190

39,446

It turns out that Airports of Thailand $AOT.TB is still the monopoly airport of Thailand, and Mr. Market was wrong last year.

3

5

682

I remain long Airports of Thailand $AOT.TB x.com/justmikemckay/status/2…

395

5 Aug 2025

$AHH trading at nearly an 11 cap rate, noticing that 2Q results and stabilized NOI look much better vs 1Q. New mgmt conveniently negotiated a new share based comp package at the all-time low (after cutting the dividend and raising new equity).

2

14

2,642

Major $AHH portfolio repositioning announced: (1) planned sale of majority of multi-family portfolio, (2) disposition construction segment, (3) exit of pref equity portfolio, (4) $50m retail acquisitions at attractive cap (5) deleveraging to 5.5x ND/EBITDA.

1

1

394

29 Oct 2025

Multi-family REIT $UDR trading back to covd-19 and 2023 lows. Markets are totally efficient.

2

8

1,464

$UDR shares modestly re-rating with management announcing $700m of asset sales to fund share repurchases.

238

19 Dec 2025

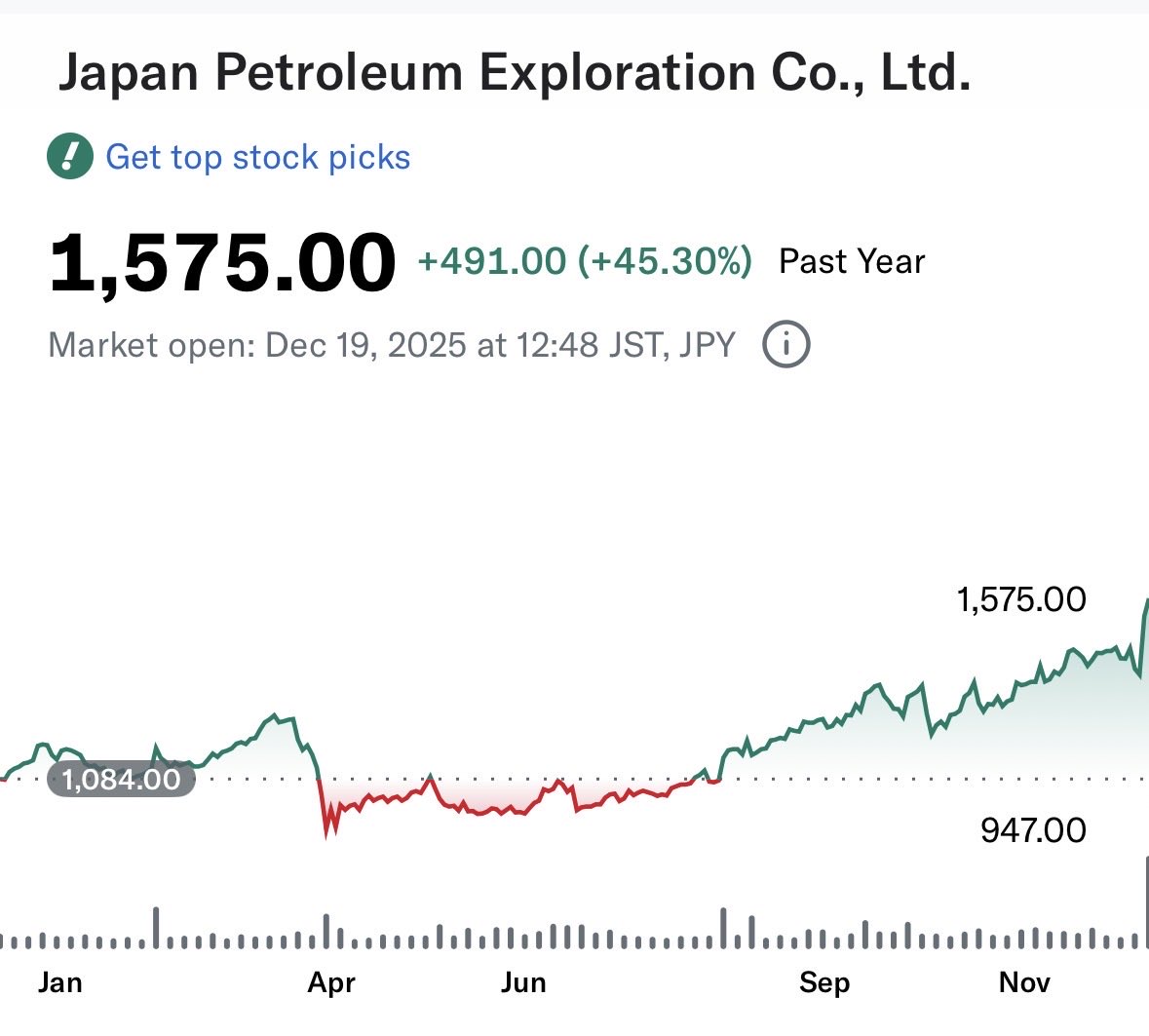

My favorite energy stock 1662.T is up >1.5x during a weak oil price environment, and still trades below net cash and securities.

2

1

10

1,354

JAPEX 1662.T could double again from here and would be valued at around 6x EBITDA, great balance sheet with zero debt.

1

2

444

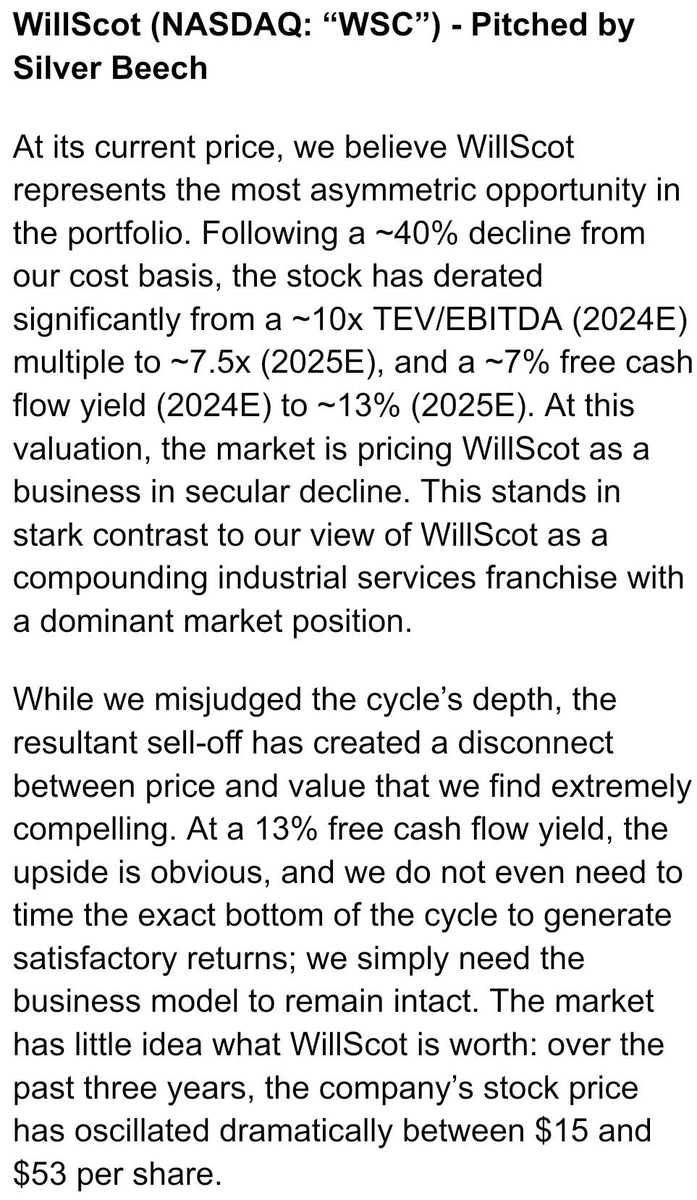

Interesting pitch on $WSC .. I have been wondering about both $WSC and $MGRC, which has received bid from $WSC in 2024 and also was rumored to have PE interest.

Potential 100% in $WSC from Silver Beech

- Dominant industrial services franchise priced as if in secular decline

- Meanwhile, the industry is consolidating as private comps liquidate

- Distress is clearly temporary

- At 13% FCF yield, timing the cycle turn isn’t even required

3

1,644

6 Sep 2025

Anyone have views on $COLD? Trading at sub 10x AFFO, 6.6% divvy yield, 65% payout. ND is 6x Adj. EBITDA, cap rate is >12. I've been lucky enough to stay clear. At these levels, can't deny that it looks attractive.

34

9

204

49,483

30 Dec 2025

$COLD exploring PE interest. I built a small position as a low conviction trade. While contentious among public investors, its seems intuitive that infra fund investors could gravitate to this situation. semafor.com/article/12/29/20…

3

6

983

Attractive set-up for $COLD with a reasonably well covered 7% dividend and catalysts including PE interest and short-covering. Not a large position, but wouldn't want to be short.

1

3

527

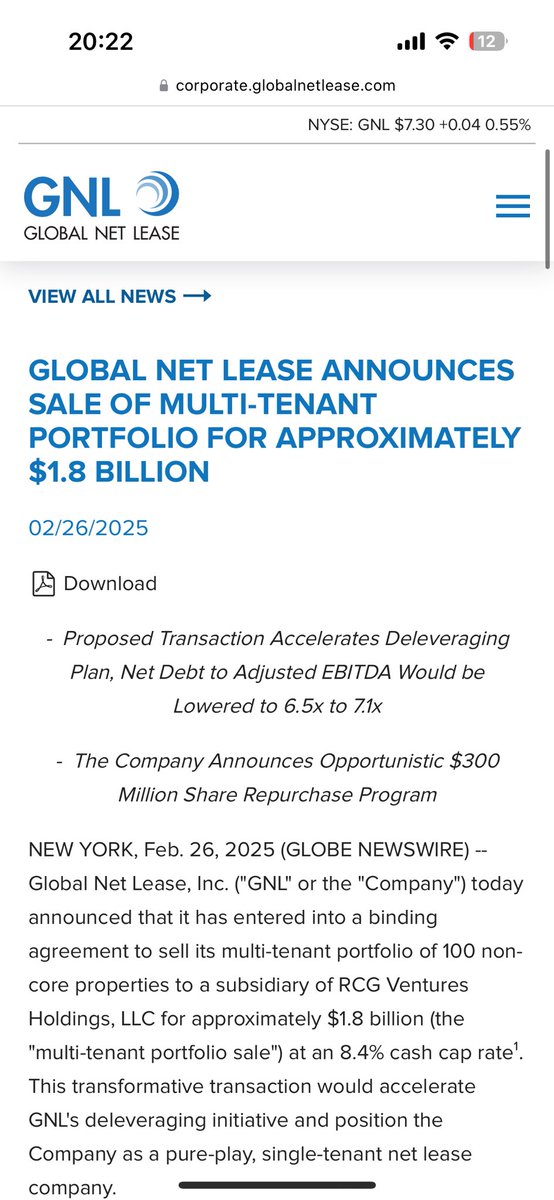

26 Feb 2025

Wow, transformational asset sale announced by $GNL …will catalyze a significant deleveraging and share repurchases.

4

6

2,184

Predicting inflection in $GNL for 2026, with deleveraging towards ~6x ND/EBITDA, more office sales, reducing office exposure towards negligible ~15% of NOI, and more share repurchases. Nearly 1.5x one year upside, using an exit 8 cap assumption.

1

324