Joined August 2025

- Tweets 734

- Following 24

- Followers 131

- Likes 105

220 Photos and videos

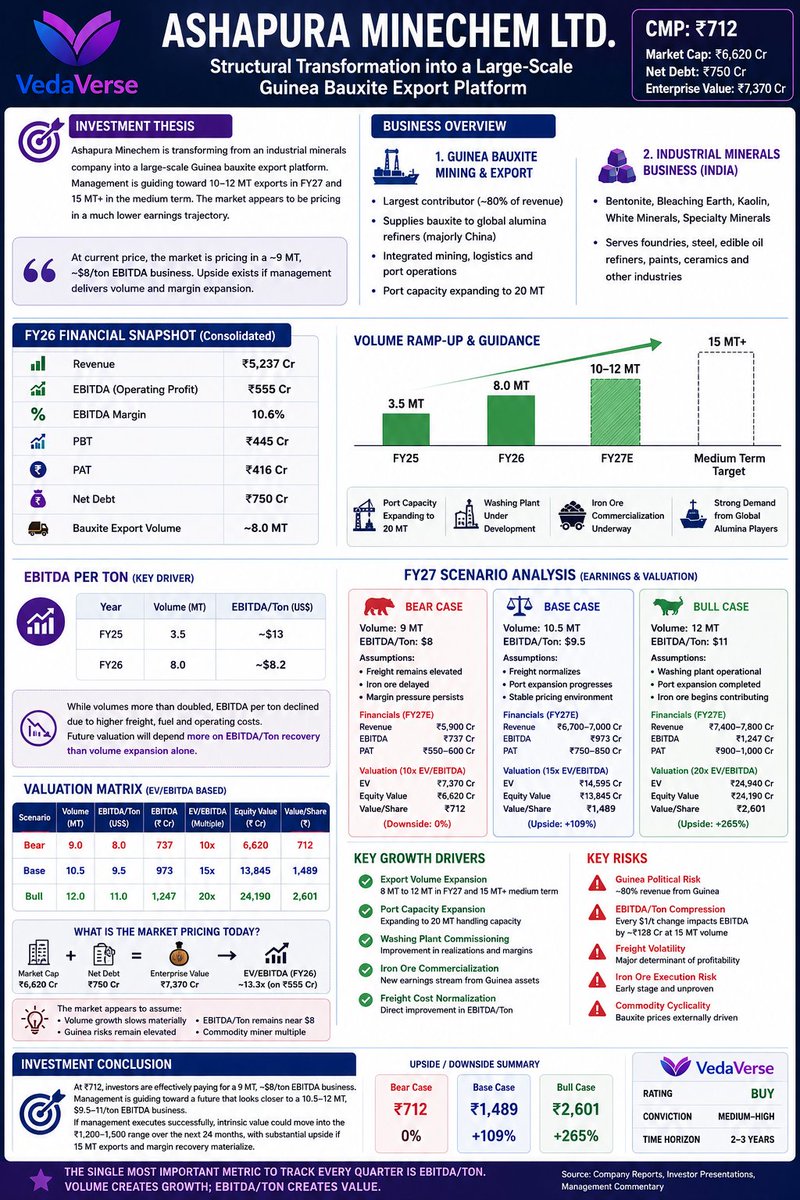

🚀 Ashapura Minechem is no longer just a bentonite company.

From 3.5 MT → 8 MT bauxite exports in just one year, with management targeting 10–12 MT in FY27 and 15 MT ahead.

💡 The market sees a commodity miner. The opportunity may be a rapidly scaling African mining platform.

2

57

Multi-Beggar Series Continues...

3rd Name in the series of "Multi-Beggar from My PF."

Bharti Airtel a Duopoly Business with a Strong Cash Flow Visibility.

Still Holding Partial Profit Booked.

No Buy/Sell Recommended

DYDD

#Bharti #Telecome #infra #ARPU #CashFLow #Duopoly

Jun 5

Another Multi bagger from My Portfolio.

KPIT TECH

One of the Great Company I like the Management a lot.going through a Headwinds Right now.

No buy/sell recommended

Only to motivate you guys.

1

111

Made a Post way Back about This Infra Company. It shines Today.

No Buy/sell Recommended.

Apr 9

Ashoka Buildcon an EPC Player

Trades at TTM PE OF JUST 3.3x

has an order book of over 15000 Cr with a Market cap of 3450 Cr.

TTM REVENUE 8260 Cr

TTM ADJ. PAT 926 Cr

Book value of 150

CMP IS 123

Undervalued ?

1

26

Most investors see a holding company

I see exposure to Brakes India, Turbo Energy, Axles India, Wheels India & TVS Holdings through a single stock

📊 Portfolio Value ₹7,621 Cr

🏦 Market Cap ₹8,660 Cr

🎯 CMP ₹390

Sometimes the real value is hidden beneath the reported No.

1

57

Jun 12

🚨 New Video Out

The Compounder Architecture:

My complete framework for finding high-quality businesses and avoiding value traps.

🎥 Watch here: 🎥youtu.be/8PqlNa0zWEY

#ValueInvesting #StockMarket #CompounderStocks

1

51

Jun 12

Made a Business Analysis Report on Hexagon Nutrition Ltd.

What a Listing a Good Business at A Decent Valuation.

Locked In UC in Just 5 Minutes of Listing.

#IPO #Hexagon #Vedaverse

Jun 9

Hexagon Nutrition Ltd

IPO DEEP DIVE

What the DRHP Says, What the Numbers Reveal, and What Investors Must Know.

No Buy/Sell/Apply Recommended.

#HexagonNutrition #HexagonNutritionIPO #HexagonNutrition #EquityResearch #InvestingIndia

2

219

Jun 11

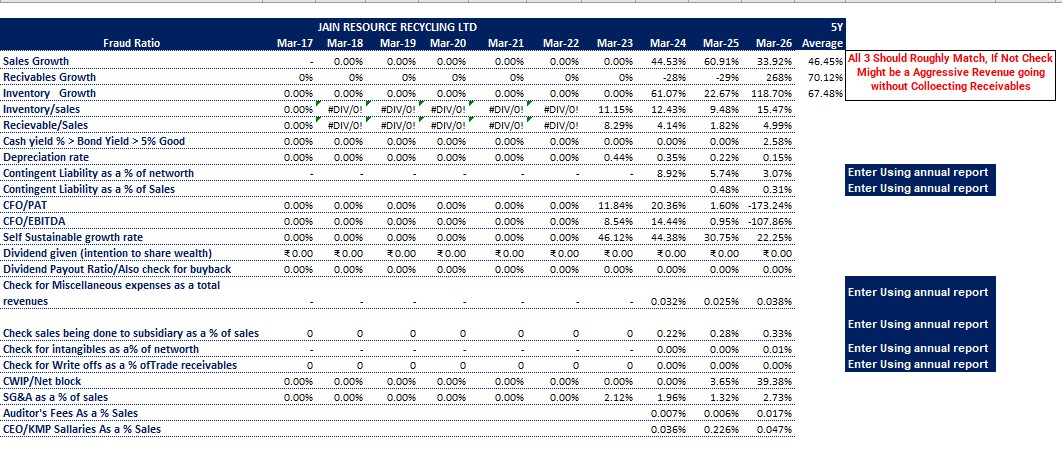

Jain Resource Recycling Ltd

Bull, Base and Bear Scenarios for Jain resources in Bear cases when Your Return CAGR is decent Mostly You Have a Good Risk to Reward Ratio.

I have Done it For Both Methods P/E and EV/EBIDTA.

No Buy/Sell Recommended.

Only For Education Purpose Only.

Jun 11

While Analyzing Companies Do You Do Forensic Analysis if Not Start Doing It.

Here is My Forensic Analysis Sheet. If You need My DCF Sheet where I have done A 2 Z Analysis of Companies DCF, Ratio Analysis, Forensic Analysis.

If You Need Any Help Do Drop a Message.

#DCF #Forensic

1

3

447

Jun 11

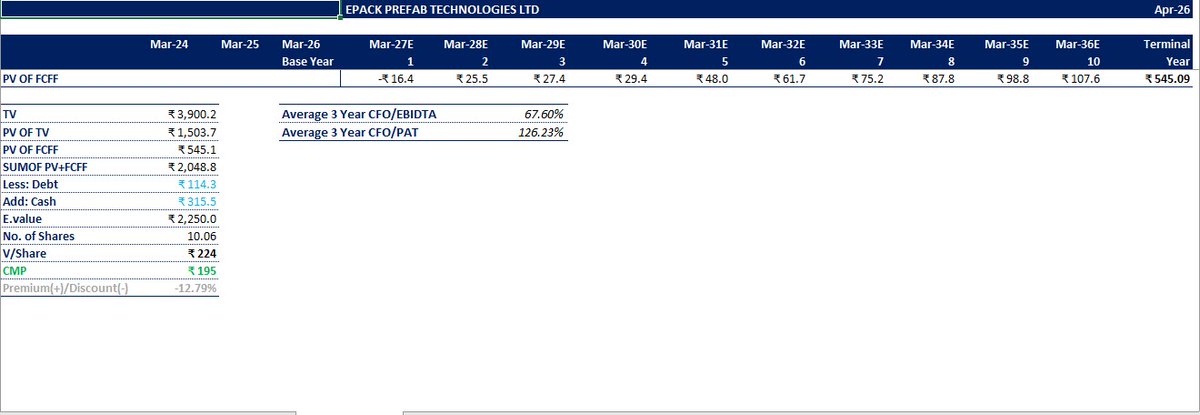

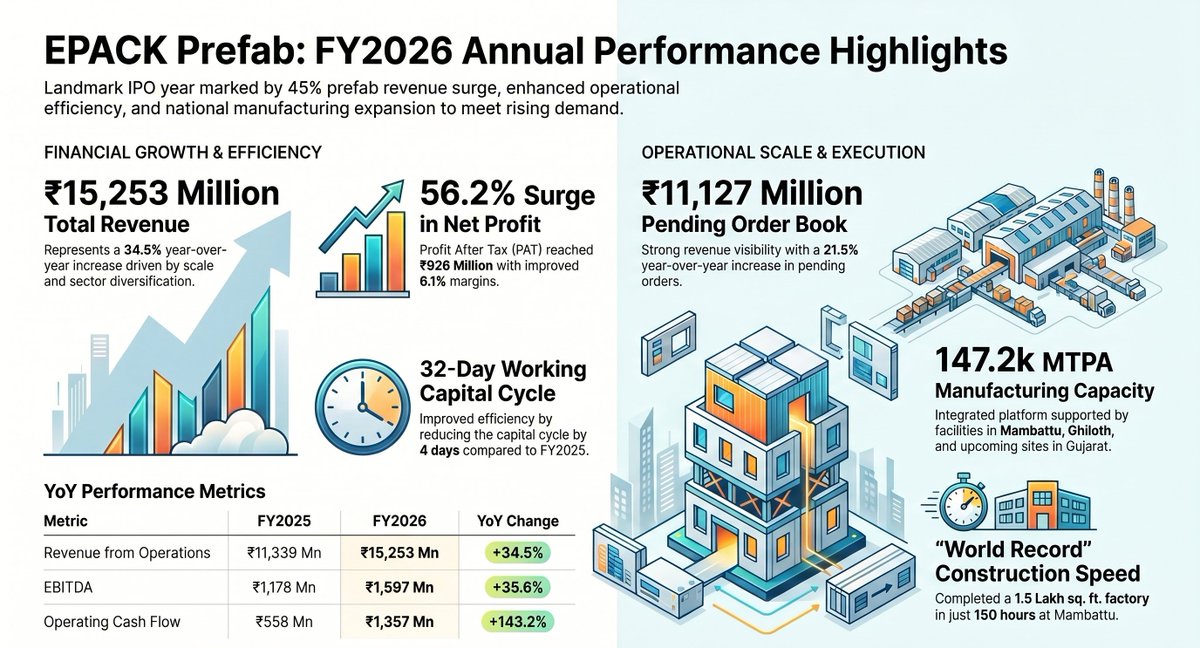

I am bullish on PEB sector as My top Pick is Epack PEB it rewarded The Patience.

It is Up 75% in 2 Months.

It is Reached My DCF Fair Value Today I am Still Bullish on This Sector/Company as Management is guiding 25% Revenue Growth in FY27.

Disc. Holding

No Buy/sell Recommended

May 19

EPack Prefab.

FY27 Guidance.

Revenue: ₹1,925 crore to ₹1,950 Cr.

EBITDA Margin: 10.5% and 11.5%

PAT Margin: 6.5%

Working Capital: 35–38 days

Capex: ₹150 crore

PEB Capacity: 220,000 MTPA

Sandwich Panel Capacity: 2.11 million SQM

Utilization: 75-80%

#EPACKPREFEB #PEB

3

172

Jun 10

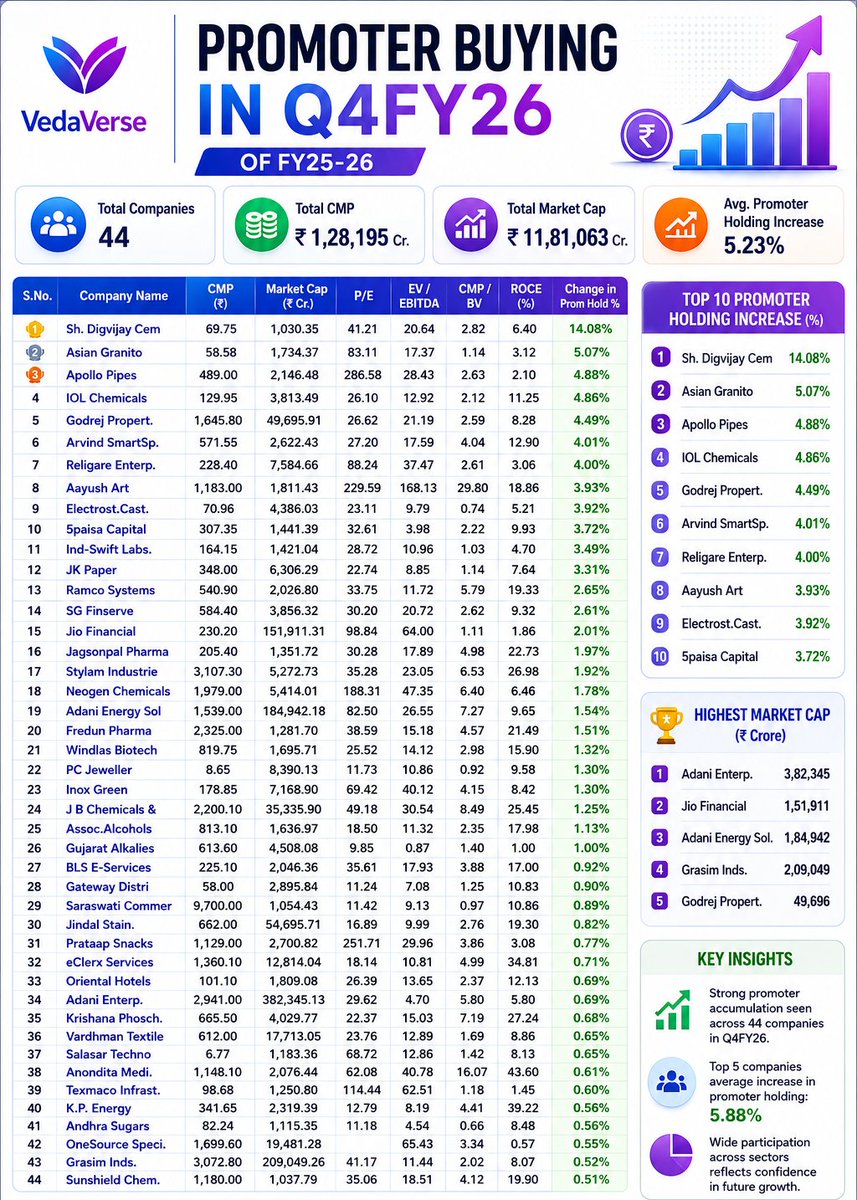

PROMOTERS BUYING IN Q4 FY26.

44 Stocks Where Promoters Increased Their Stake — Tracking the Smart Money

#PromoterBuying #PromoterHolding #ShareholdingPattern #SmartMoney #InsiderBuying #StockMarketIndia #IndianStocks

1

37

Jun 10

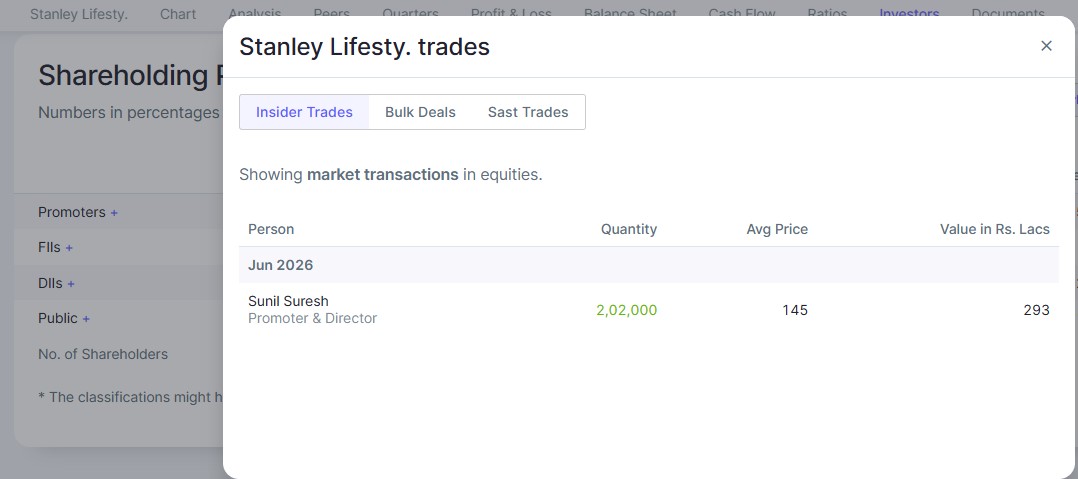

Stanley Lifestyles Ltd.

Promoter Sunil Suresh acquired 2,02,000 shares at Rs.145 in the June Month.

Is it a Bullish Sign for Stanley?

at some point of time Mr. Mukul Agrawal also used to hold 1.58% stake in it.

1

42

Jun 10

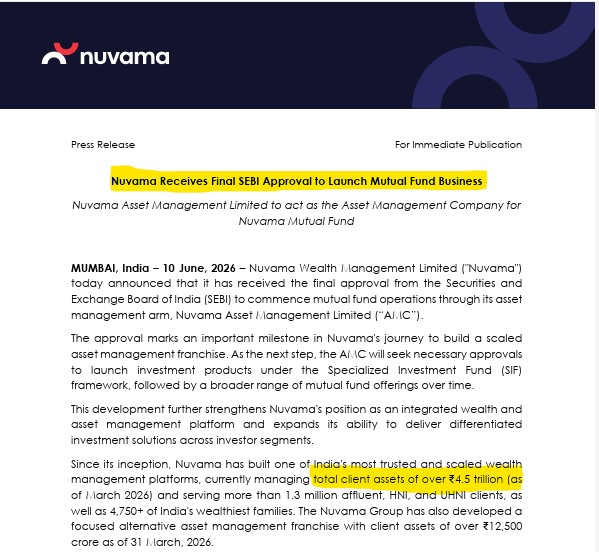

Nuvama receives approval to launch its Mutual Fund business.

The AMC foray adds a recurring revenue stream, strengthens client stickiness, and further diversifies Nuvama's wealth management platform.

#Nuvama #AMC #MutualFund #WealthManagemnet

1

85

Jun 10

Caplin Point Laboratories Ltd.

Made a business explainer in Mid-March Looked Promising as they were expanding their market from LATAM To US.

In Just 3 Months Company rewarded their shareholders well as it Moved 40% from Last we Discussed.

#Caplinpoint #Pharma #LATAM #US

205

Jun 9

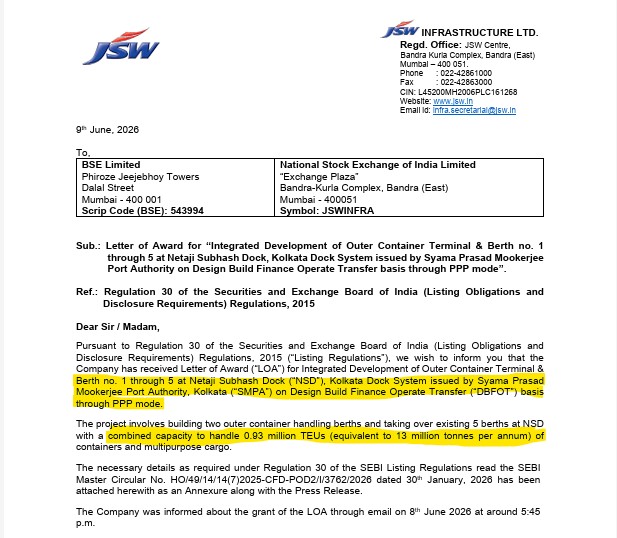

JSW Infra wins a 30-year concession for Kolkata's Outer Container Terminal.

📦 0.93 Mn TEUs capacity

📦 Total Kolkata capacity: ~1.4 Mn TEUs

Another step towards building a larger, diversified port and logistics platform.

#JSWInfra #Ports #Infrastructure #IndianStockMarket

2

156

Jun 9

Hexagon Nutrition Ltd

IPO DEEP DIVE

What the DRHP Says, What the Numbers Reveal, and What Investors Must Know.

No Buy/Sell/Apply Recommended.

#HexagonNutrition #HexagonNutritionIPO #HexagonNutrition #EquityResearch #InvestingIndia

2

811

Jun 9

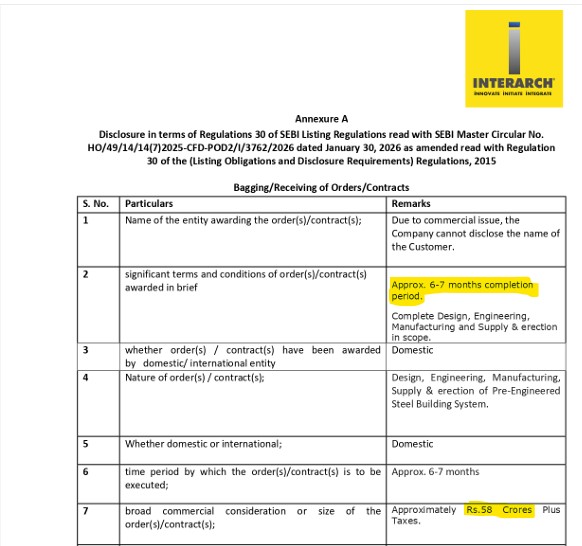

Interarch Building Solutions Ltd.

Quick Update.

Received an Order Worth Rs.58 Cr. For Domestic Pre-Engineered Building. Completion To be in 6-7 Months.

1

60

Jun 9

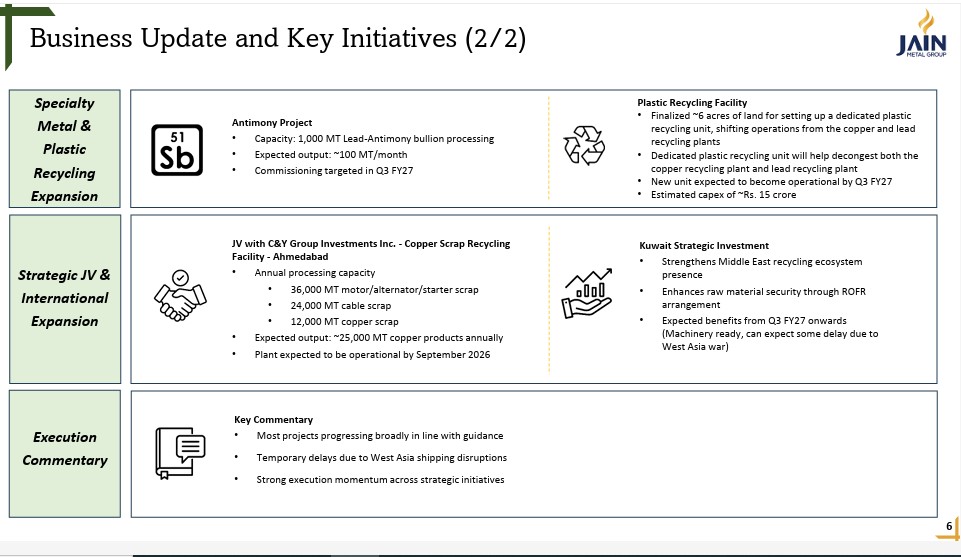

Jain Metal is aggressively expanding across the copper value chain with new capacities in Copper Anode, Cathode, Wire Rods, and Busbars, while strengthening its recycling ecosystem through specialty metals, plastic recycling, and global scrap sourcing partnerships.

#Recycling

1

55

Jun 8

NACL Industries Ltd.

1/8

In 2020, Murugappa Group bought CG Power at ₹8/share — a fraud-ridden, debt-laden wreck.

Today it trades at ₹900 . That's a 100x return in 5 years.

Now they're running the exact same playbook on NACL Industries. Here's what you need to know. 🧵

1

6

309

Jun 8

7/8

— 52-week range: ₹48–₹220. Re-rating may already be partially priced in — Open offer exit by retail = near-term overhang, NACL is NOT the next CG Power. It's a strategic acquisition, not a rescue mission

1

1

91

Jun 8

8/8

My view:

NACL could be the next Shanthi Gears — a quiet 5–10x compounder over a decade, not a 100x moonshot. Watch for: EBITDA margins crossing 12%, D/E below 60%, any new CDMO contract announcement. The Murugappa playbook is rare. When they run it, pay attention.

1

76