SOIC Intelligent Research LLP | SEBI Registered Research Analyst (Reg. No: INH000012582) | Views are personal & for education purposes | Not Investment Advice

Joined September 2025

- Tweets 380

- Following 34

- Followers 11,896

- Likes 88

246 Photos and videos

Pinned Tweet

May 6

We have been running a series called 20 Unique Businesses on this page.

The filter is simple :-

→ High barriers to entry

→ Cannot be replicated just via blank cheque

→ Good return ratios

→ Limited competitors

→ Doing something cutting edge or structurally different

Not stocks to buy. Not targets to chase. Just businesses worth understanding, the kind where the moat is not a number on a screener but something you feel once you study the value chain.

If you missed any of them, this thread is your single window. Every business we have covered so far, in one place -

5

61

391

41,433

May 6

We have been running a series called 20 Unique Businesses on this page.

The filter is simple :-

→ High barriers to entry

→ Cannot be replicated just via blank cheque

→ Good return ratios

→ Limited competitors

→ Doing something cutting edge or structurally different

Not stocks to buy. Not targets to chase. Just businesses worth understanding, the kind where the moat is not a number on a screener but something you feel once you study the value chain.

If you missed any of them, this thread is your single window. Every business we have covered so far, in one place -

5

61

391

41,433

May 6

Sai life sciences

x.com/ResearchSOIC/status/20…

Apr 22

Here is the 5th business of the 20 unique businesses. This one is from the world of pharma. It is a company which truly stands by the complete Integrated facility across the entirety of the CRDMO cycle , along with unique CDMO molecule pipeline which does not have a single molecule dependency unlike most others.

One of the only CRDMO companies in the country that is able to execute well and grow at a faster pace at the same time...

Most Indian companies do ONE of these. Sai Life Sciences does ALL THREE.

This is the story of India's most integrated CRDMO and why it could be a structural story.

Let's understand the why behind it!

2

2

28

9,962

Jun 1

Rategain Travel Technologies

x.com/ResearchSOIC/status/20…

Jun 1

Today, let's talk about a SaaS business that most people would dismiss at first glance.

An IT company. A software business. In 2025-26, the automatic reaction is, "AI will eat these guys alive."

And honestly? For most SaaS companies, that fear is valid.

But this one is different.

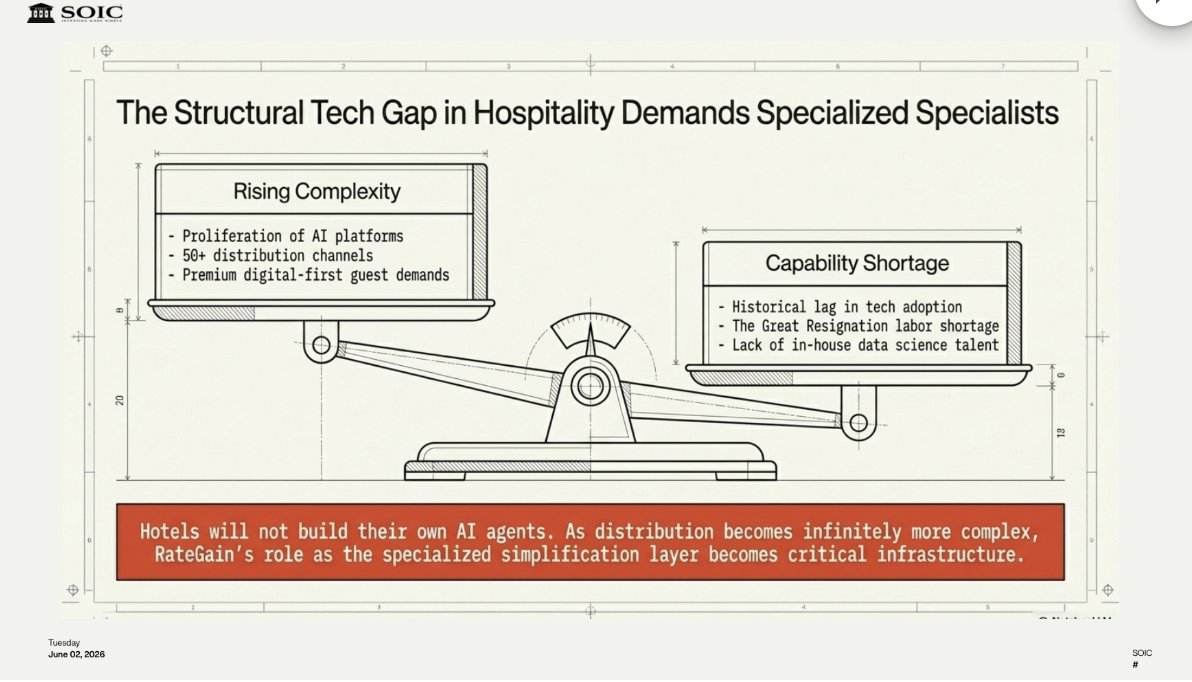

This isn't a generic software vendor selling dashboards or CRM tools. This business has quietly built itself into the invisible infrastructure of a $1.5 trillion global travel industry.

Every time you book a hotel on Booking. com, every time an airline adjusts its fare, every time a hotel decides how much to spend on Google ads there's a high chance this company's technology is running in the background, making that decision happen.

And here's the contrarian thesis that we'll break down in this thread:

AI doesn't disrupt this business. AI makes its moat deeper.

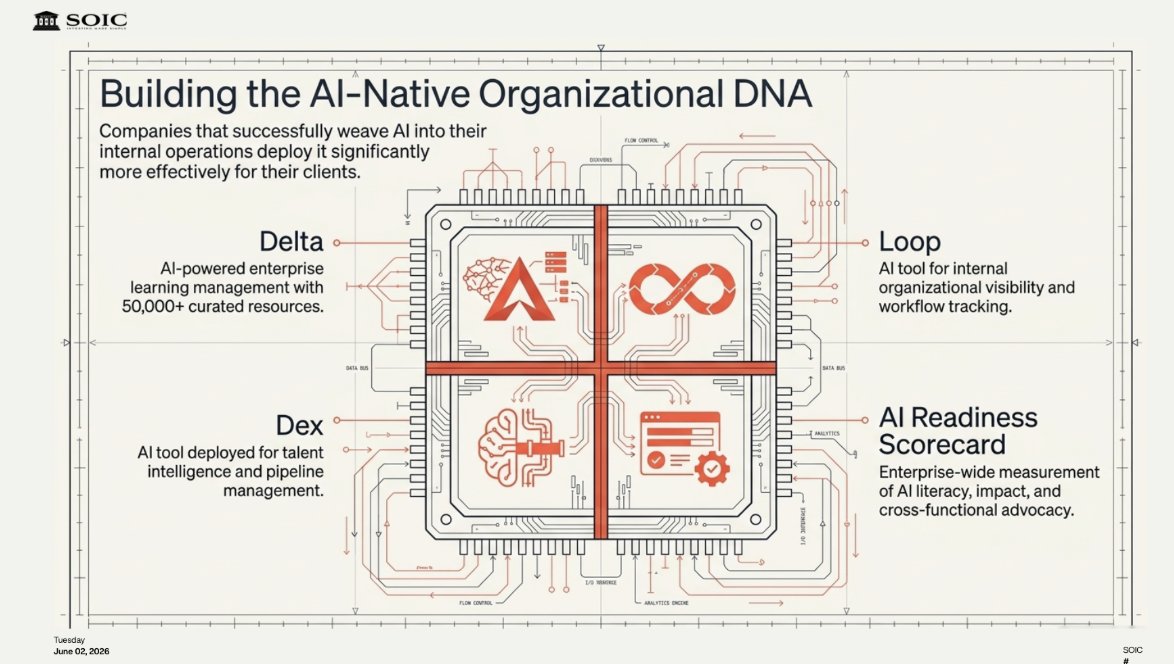

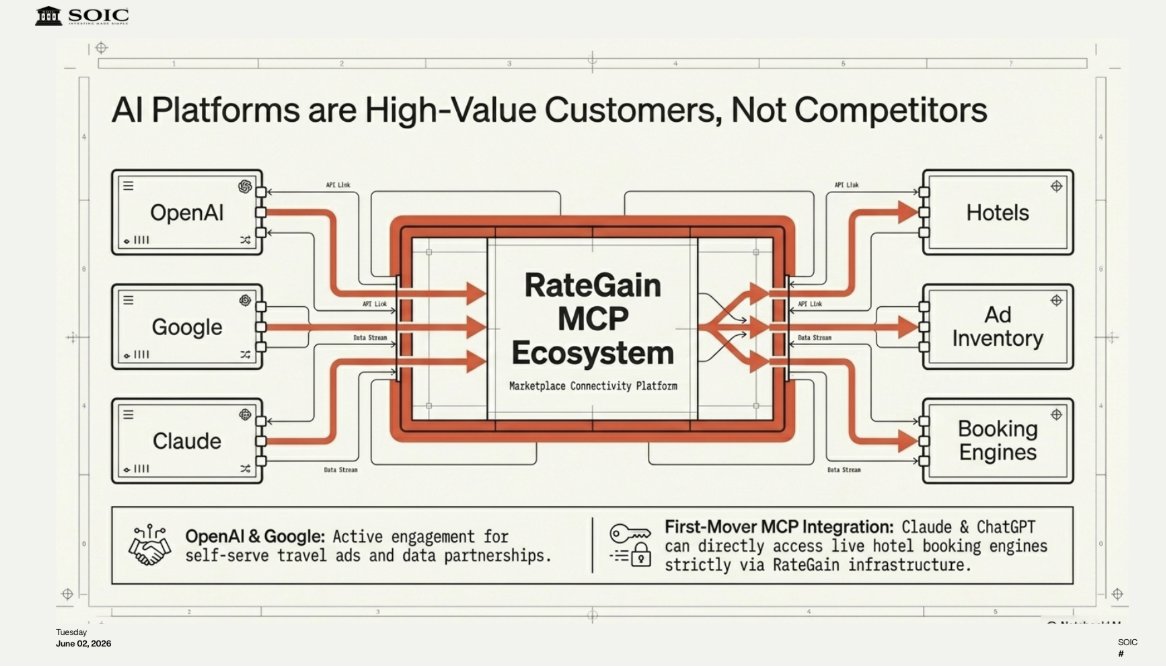

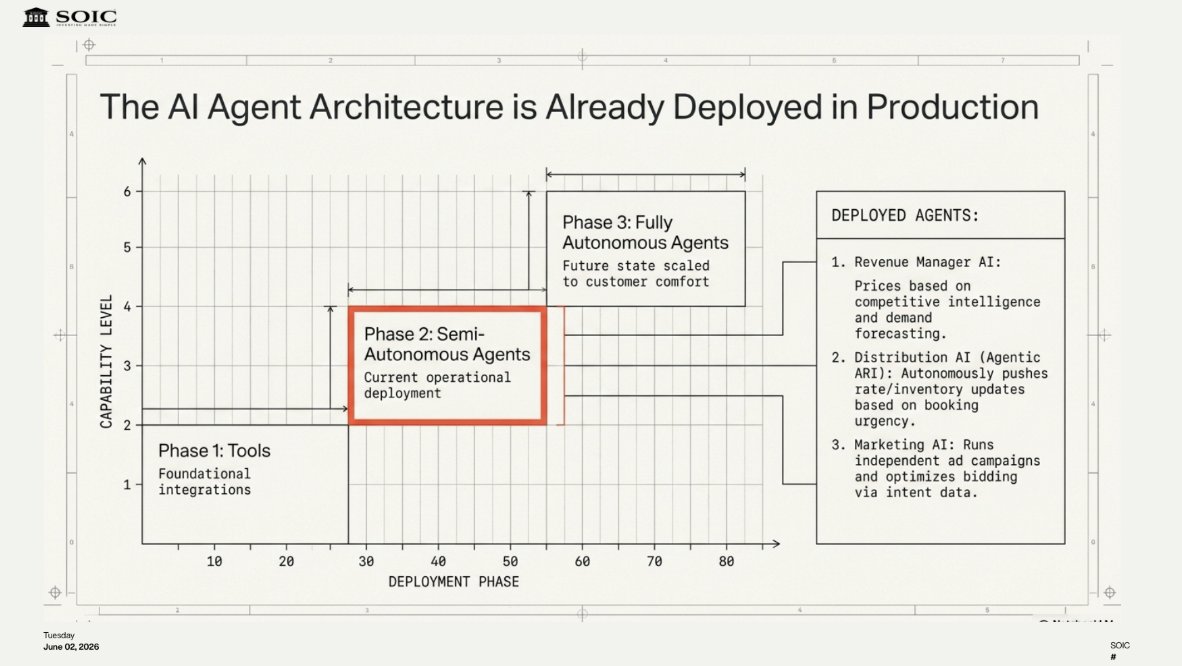

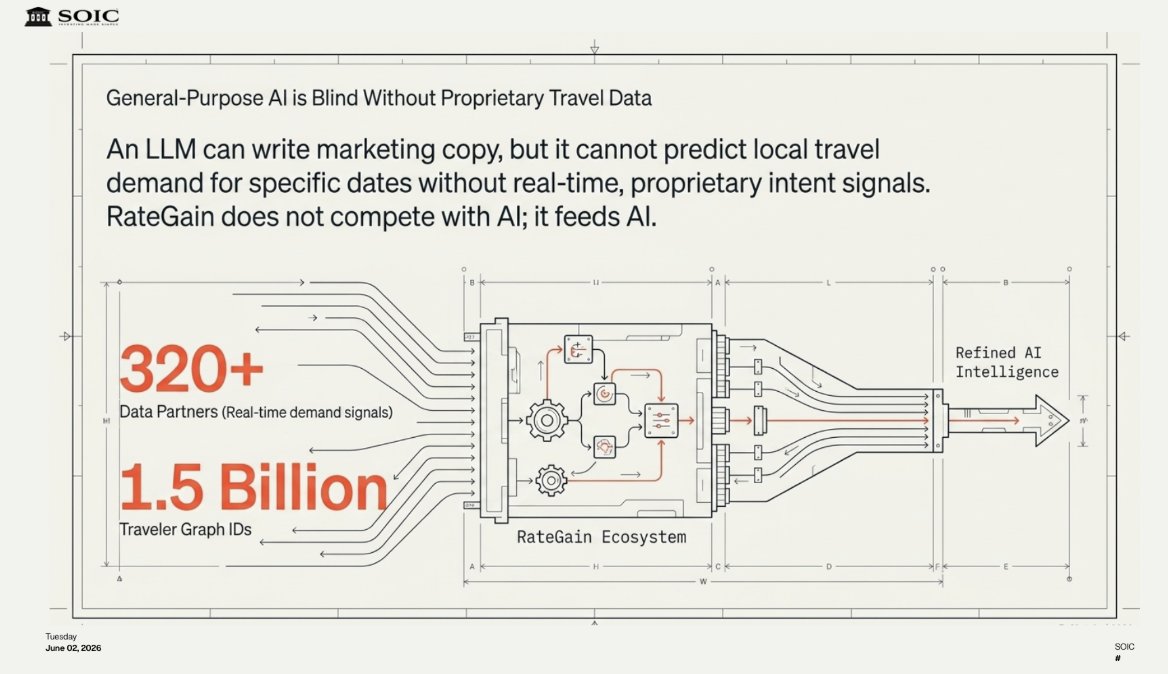

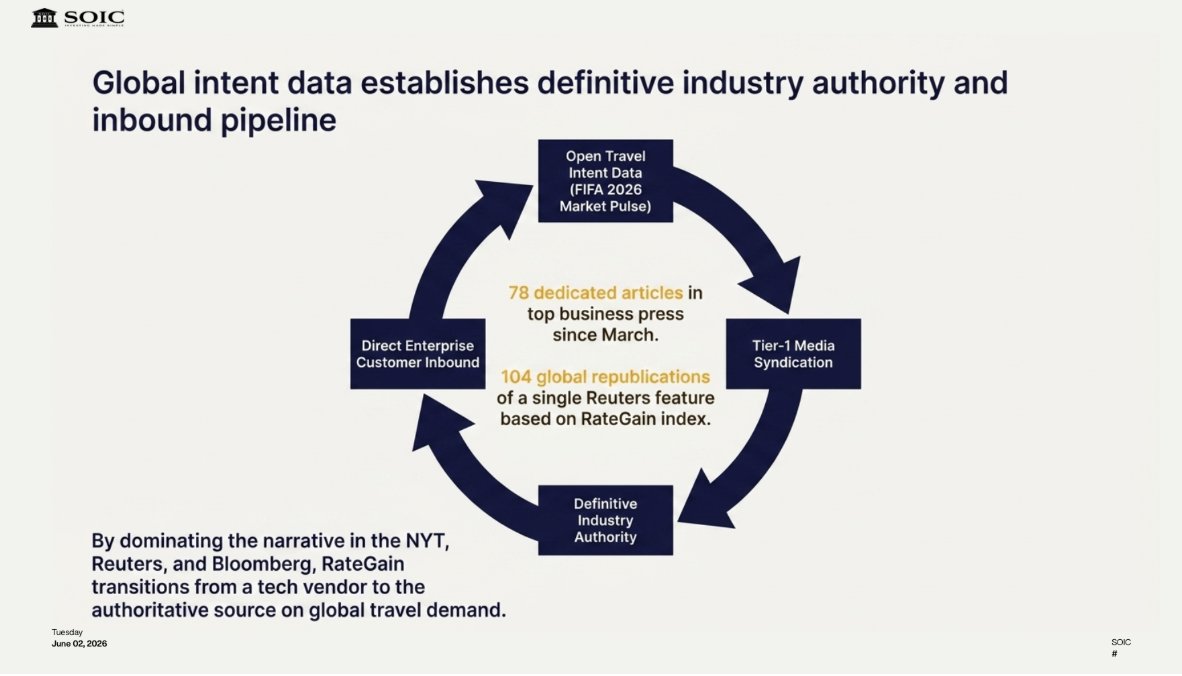

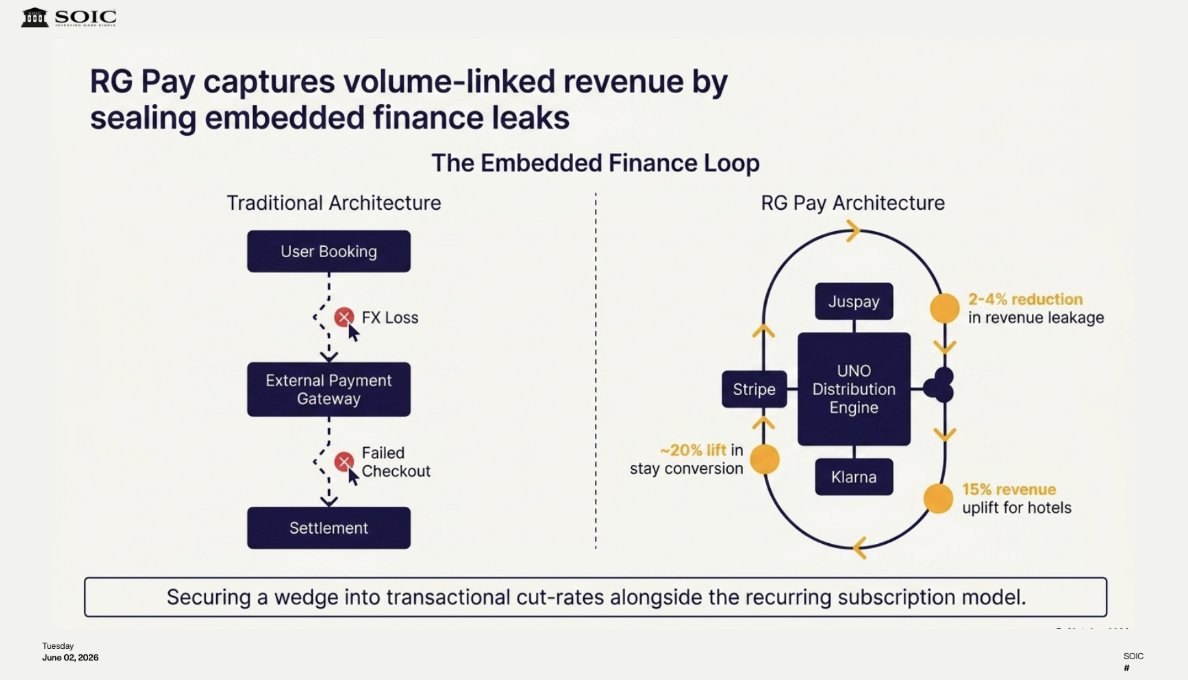

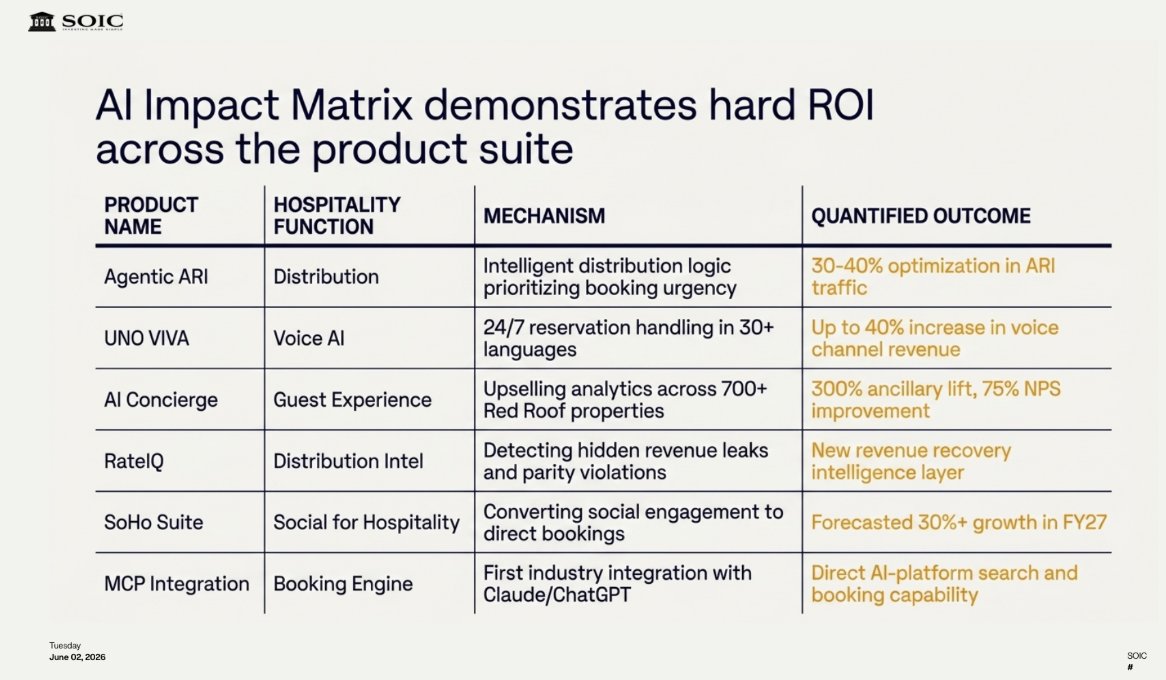

While the market debates whether SaaS companies will survive the AI wave, this one is already deploying AI agents that deliver 300% revenue lifts for customers, has built the world's largest travel intent data platform with 1.5 billion data points, and is in active conversations with OpenAI and Google to become the advertising infrastructure layer for AI-powered travel.

So in this thread, we're going to break it all down for you in simple terms:

→ What the business actually does (and why it can't be replicated)

→ Why financial metrics of this company are among the best in Indian SaaS

→ What's going to drive the next phase of growth

→ The real risks that you should watch

→ And the big question, is AI a threat or the biggest tailwind this business has ever had?

2

12

2,999

SOIC Research retweeted

Jun 1

Today, let's talk about a SaaS business that most people would dismiss at first glance.

An IT company. A software business. In 2025-26, the automatic reaction is, "AI will eat these guys alive."

And honestly? For most SaaS companies, that fear is valid.

But this one is different.

This isn't a generic software vendor selling dashboards or CRM tools. This business has quietly built itself into the invisible infrastructure of a $1.5 trillion global travel industry.

Every time you book a hotel on Booking. com, every time an airline adjusts its fare, every time a hotel decides how much to spend on Google ads there's a high chance this company's technology is running in the background, making that decision happen.

And here's the contrarian thesis that we'll break down in this thread:

AI doesn't disrupt this business. AI makes its moat deeper.

While the market debates whether SaaS companies will survive the AI wave, this one is already deploying AI agents that deliver 300% revenue lifts for customers, has built the world's largest travel intent data platform with 1.5 billion data points, and is in active conversations with OpenAI and Google to become the advertising infrastructure layer for AI-powered travel.

So in this thread, we're going to break it all down for you in simple terms:

→ What the business actually does (and why it can't be replicated)

→ Why financial metrics of this company are among the best in Indian SaaS

→ What's going to drive the next phase of growth

→ The real risks that you should watch

→ And the big question, is AI a threat or the biggest tailwind this business has ever had?

7

38

274

45,538

Jun 1

Today, let's talk about a SaaS business that most people would dismiss at first glance.

An IT company. A software business. In 2025-26, the automatic reaction is, "AI will eat these guys alive."

And honestly? For most SaaS companies, that fear is valid.

But this one is different.

This isn't a generic software vendor selling dashboards or CRM tools. This business has quietly built itself into the invisible infrastructure of a $1.5 trillion global travel industry.

Every time you book a hotel on Booking. com, every time an airline adjusts its fare, every time a hotel decides how much to spend on Google ads there's a high chance this company's technology is running in the background, making that decision happen.

And here's the contrarian thesis that we'll break down in this thread:

AI doesn't disrupt this business. AI makes its moat deeper.

While the market debates whether SaaS companies will survive the AI wave, this one is already deploying AI agents that deliver 300% revenue lifts for customers, has built the world's largest travel intent data platform with 1.5 billion data points, and is in active conversations with OpenAI and Google to become the advertising infrastructure layer for AI-powered travel.

So in this thread, we're going to break it all down for you in simple terms:

→ What the business actually does (and why it can't be replicated)

→ Why financial metrics of this company are among the best in Indian SaaS

→ What's going to drive the next phase of growth

→ The real risks that you should watch

→ And the big question, is AI a threat or the biggest tailwind this business has ever had?

7

38

274

45,538

Jun 1

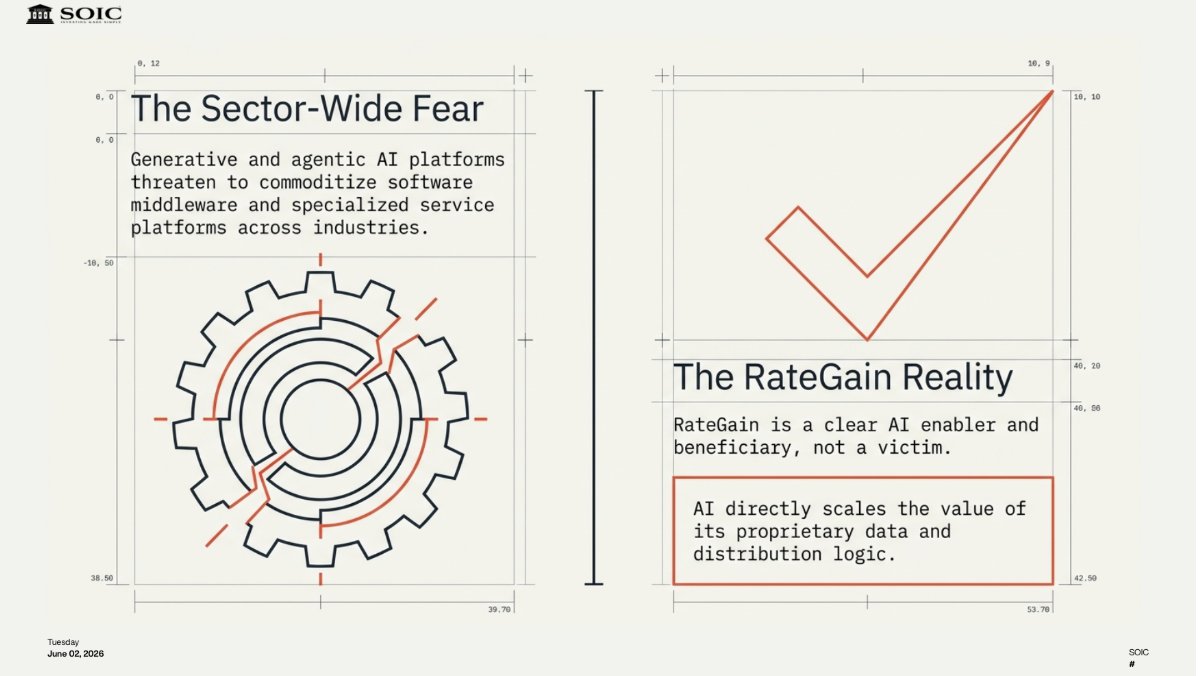

To be intellectually honest, there are two scenarios where AI could pressure RateGain:

Scenario 1 — Large hotel chains build in-house AI: If Marriott or Hilton decides to build its own AI-powered revenue management and distribution optimization stack, they could reduce dependency on third-party vendors like RateGain. However, this is a "build vs. buy" trade-off that large enterprises face in every technology category, and the track record suggests most prefer to buy specialized solutions rather than divert engineering resources from their core hospitality business.

Scenario 2 — A well-funded AI-native competitor emerges: A startup combining frontier AI capability with travel domain expertise could theoretically build a competing platform. Lighthouse is the closest example in the DaaS space. However, the data moat (320 partnerships, 1.5B graph IDs) and distribution network effects (OTA certifications, channel integrations) cannot be replicated by AI alone they require relationships, contracts, and time.

1

4

1,845

Jun 1

We started this thread with a simple question in a world where everyone thinks AI will eat SaaS companies alive, can a travel technology business actually survive and thrive?

After going through the concalls, the investor decks, the expert transcripts, and the numbers here's what we found:

This isn't a company that's waiting around hoping AI doesn't disrupt them. This is a company that has already become the data layer, the distribution backbone, and the marketing engine for global travel — and is now embedding AI into every single one of those layers.

The moat isn't one thing. It's the compounding of six things stacked together 1.5 billion travel intent signals that took 17 years to build, OTA certifications that require years of trust, an integrated stack no competitor has replicated, 97-99% recurring revenue, 13,000 customers across 100 countries, and greenfield products with 90% gross margins.

A blank cheque doesn't buy you this. Only time does.

And the numbers tell the story:

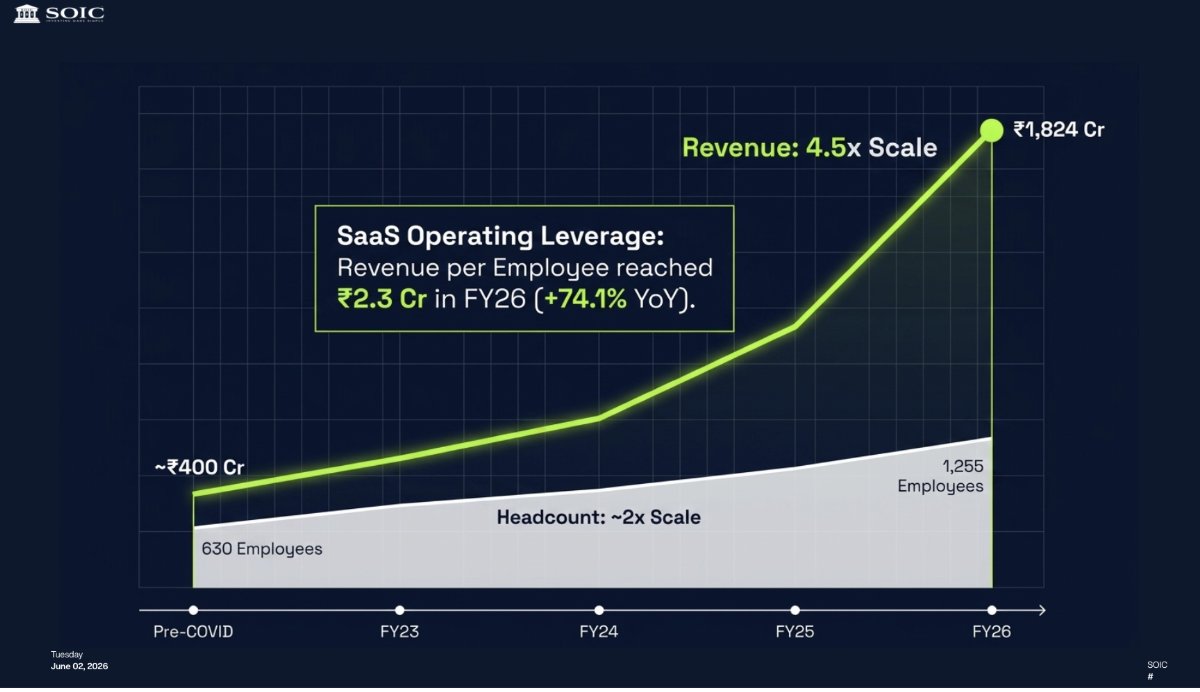

₹367 Cr → ₹1,824 Cr revenue in 4 years EBITDA margins: 8% → 23.5% (Q4 exit) Free cash flow: ₹230 Cr LTV to CAC: 12.8x (benchmark is 3-5x) Target: $1 billion revenue by FY31

Is it perfect? No. The NRR decline is a genuine watch item. The Sojern integration is the biggest bet they've ever made. Debt exists. Competition from Lighthouse in DaaS is real.

But here's the thing about great businesses they don't need to be perfect. They need to be structurally positioned in a way that time works in their favour, not against them.

And when the founder of this company says on an earnings call "We entered FY26 as a travel technology platform. We are exiting it as the AI-powered operating system for travel revenue growth" that's not a marketing line. That's backed by deployed AI agents, measurable outcomes, and conversations with OpenAI and Google.

We started this thread saying most SaaS companies should be worried about AI.

This one should be excited.

That's RateGain. The invisible toll booth of global travel.

1

7

1,741

Jun 1

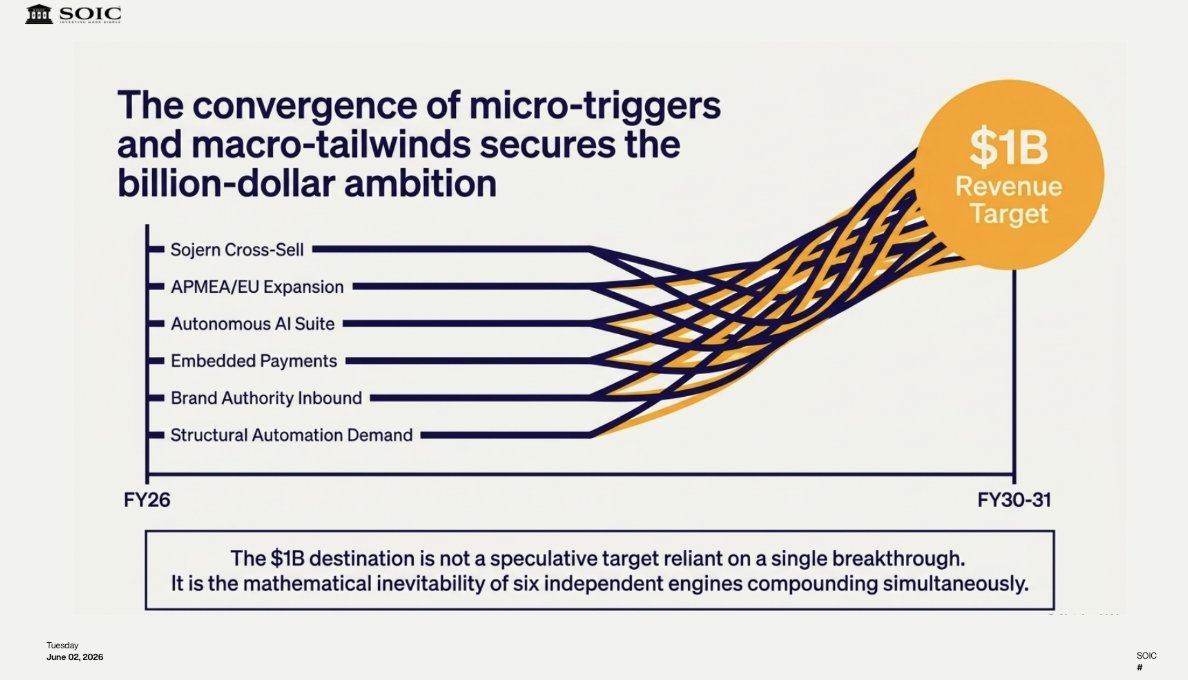

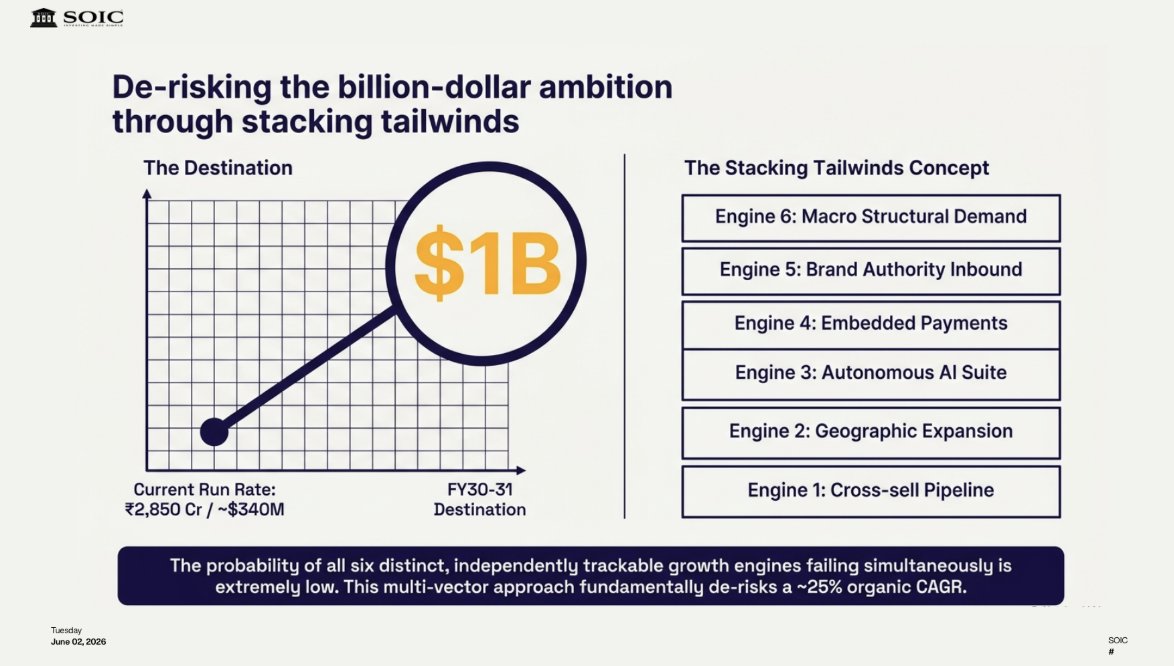

Trigger 6: The $1 Billion Revenue Ambition by FY30-31

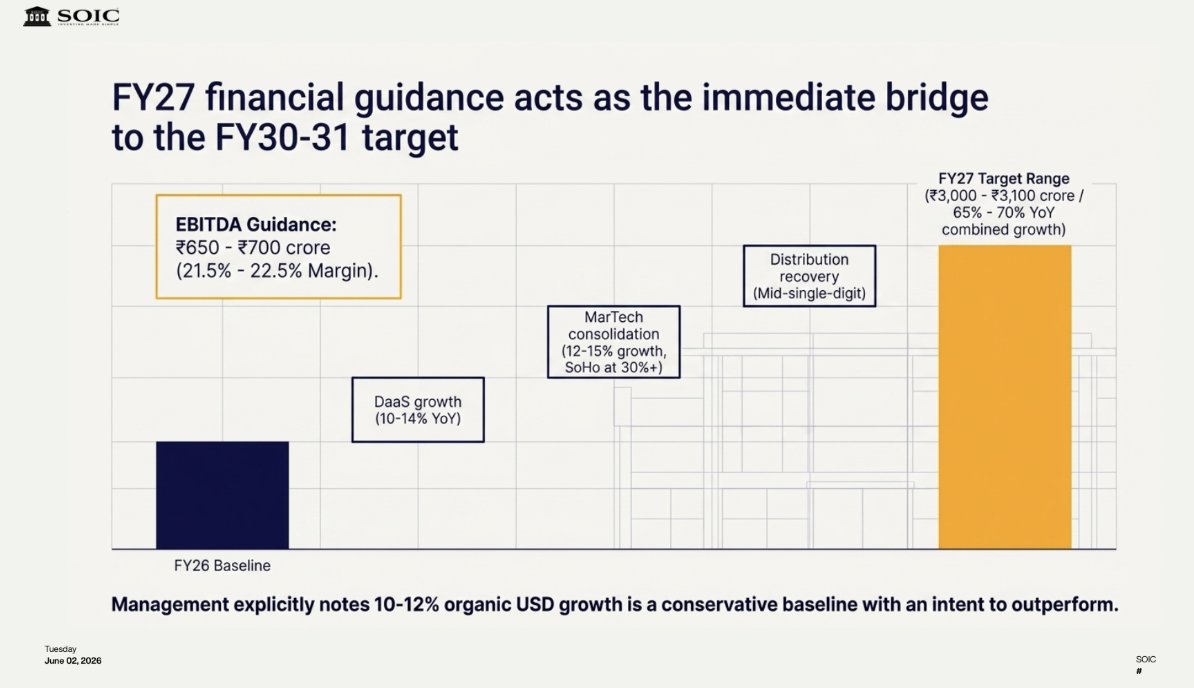

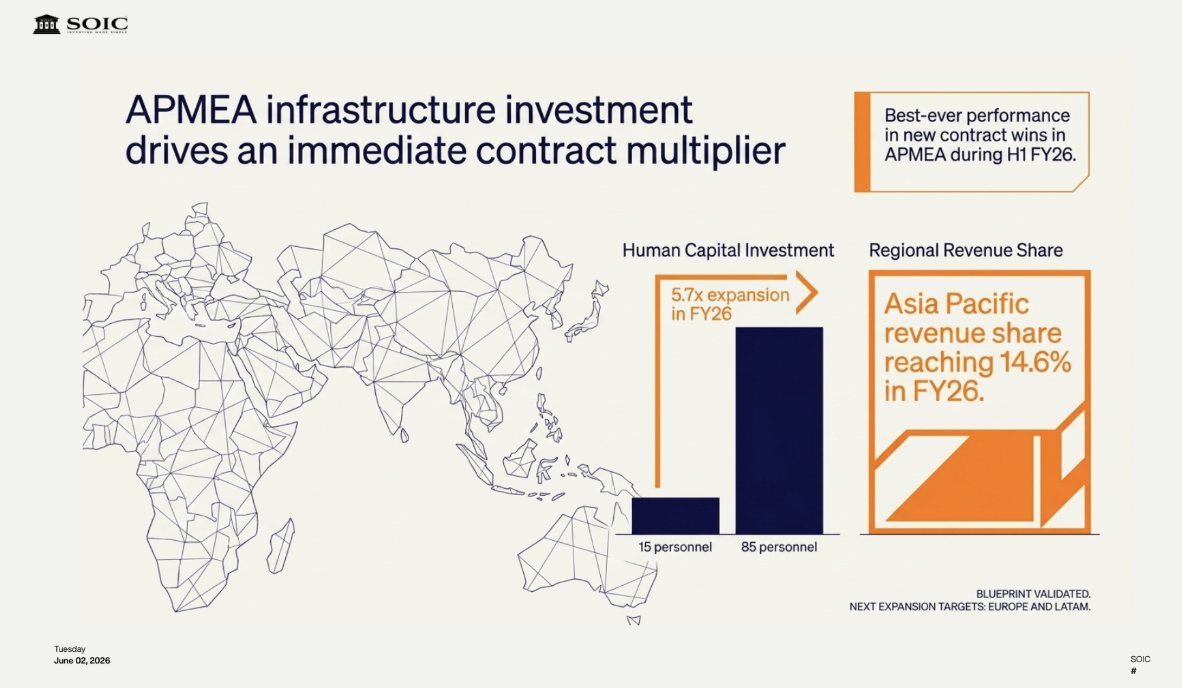

Management has explicitly stated a target of $1 billion in revenue by FY30-31. At the current annualized run rate of ₹2,850 crore (~$340M), this implies roughly a 3x growth over 4-5 years, or a ~25% organic CAGR supplemented by selective M&A.

Segment-wise FY27 growth outlook:

- DaaS: 10-14% growth (low double-digit)

- Distribution: Mid-single-digit recovery from the soft FY26

- MarTech (consolidated): 12-15% growth, with properties on the higher side and SoHo at 30%

- In USD terms: 10-12% overall organic growth

652