Account for following Traders.

Joined October 2023

- Tweets 2,552

- Following 34

- Followers 1,000

- Likes 7,949

391 Photos and videos

Pinned Tweet

16 Sep 2025

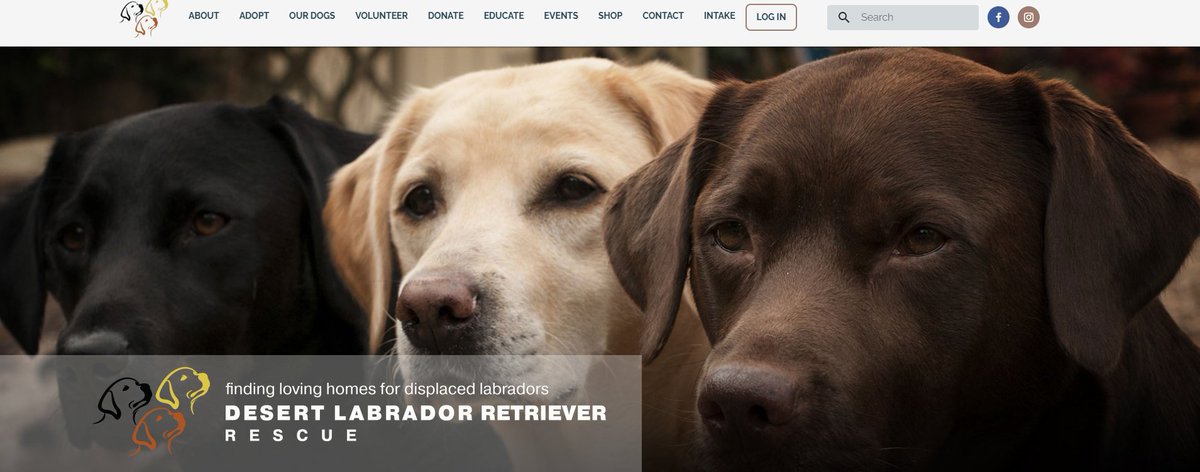

I am not interested in followers, subs, or your money. If anything I post ever helps you become a better trader, please donate to one of my favorite rescues. @DLRR @LabRescueLRCP

6

1

55

8,881

I don't know what I was expecting with the new Market Wizards book, but honestly, I think it kind of sucks so far. I'm glad I got the audio version so I can list it at 1.5x speed.

1

170

What coincidental timing did Howard Lutnick's firm announced the most bullish target for $SNDK right before there was an announcement that in apache helicopter got shot down and the stock cratered.

1

173

Local hay is selling for $350 /ton. That is 2x normal. A ripple effect from increased diesel and fertilizer costs. The ripple will continue into beef prices this winter. It might not sound like much, but my neighbor puts up 500 tons for his small herd. That is an extra $87,500.

1

1

6

389

Retired Trader 🇺🇸 retweeted

May 31

I will never waste another minute voting again. I was involved with state politics years back. It's ALL scripted down to the fake legislature meetings and politician votes. It's ALL controlled by money. Voting is an illusion to make citizens FEEL like they have say.

3

3

30

392

May 29

I never buy anything with an advertisement and wear nothing with a label or brand name. If they need to convince me that I need to buy it then I don't need it. Not being a lemming has never made my life worse.

1

4

150

May 27

Me waiting for the dip to buy...

May 26

Naturally mummified remains were discovered along the arid Atacama desert coast in Chile, dating to around 7000 BC

Community note

The mummified remains shown were long-buried, not discovered sitting exposed along the coast as implied; Chinchorro mummies were always found in extended positions and this image depicts exhumed remains. en.wikipedia.org/wiki/Chinchorr… snopes.com/fact-check/700…

2

243

May 18

There are so many things far more important than money.

May 18

1

6

591

May 18

We're there...

Koreans have now maxed out margin on KOSPI and are directly going to banks for loans. People that are 60 have never owned trading accounts and now it’s the fastest growing age group entering to buy leveraged semiconductors. Just one article of many describing the madness.

$soxx $dram

koreatimes.co.kr/amp/economy…

3

397

May 14

Regardless of the market, and propaganda, I FEEL like I did in 2022 during the recession with costs of everything going up faster than the ability to keep up with them. Every breath is monetized and trades charging $150-200 /hr. Everything feels like we are being gouged.

226

I remember during the dotcom bubble when I had friends Cash, advancing credit cards and taking out home equity loans to put into the stock market because nothing ever went down. None of them retired rich and most of them lost everything.

1

8

403

Not a bubble at all...

1

1

295

Definitely not a bubble...

Trade NVIDIA with up to 20x leverage. No expiry. More control, more upside.

2

159

AI was only released to the public to fool them into thinking it will enhance jobs and for videos and memes to justify building giant data centers out in the open for government surveillance and digital ID.

1

186

Apr 30

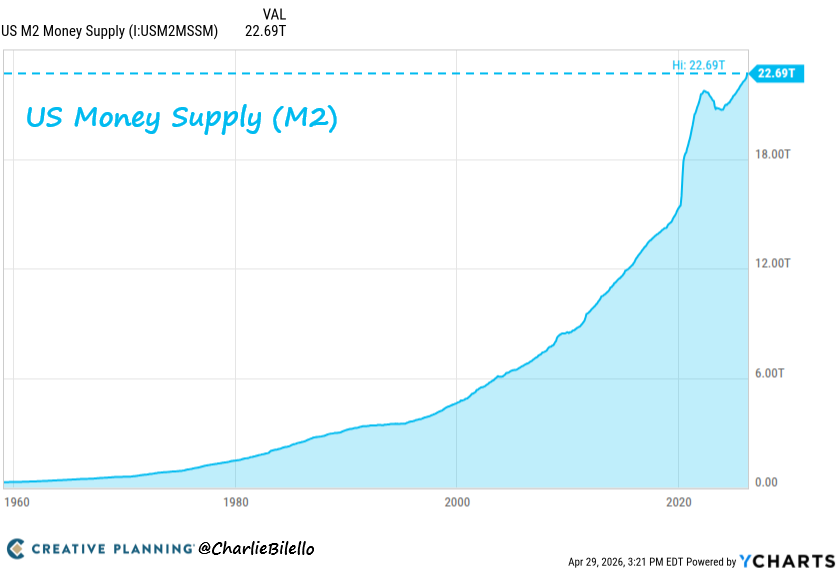

How can I invest my money in an ETF tied to the M2 money supply?

Apr 30

The Fed expanded the money supply by nearly $9 trillion under Powell.

Inflation has averaged >4% per year over the past 6 years.

Powell's explanation? It was nearly all due to rolling “supply shocks" over which the Fed has no control.

The truth: this inflation was made in Washington as it always is - from too much government borrowing/spending and too much government creation of money.

1

282

Retired Trader 🇺🇸 retweeted

Apr 28

Paul Tudor Jones just said something the market really doesn't want to hear.

"We're clearly so leveraged in equities in this country. We're 252% of stock market cap to GDP. In 1929, we were at 65%. In 1987, about 85%. In 2000, we got to 170%. And now we're at 252."

Every number he listed, 1929, 1987, 2000 ended the same way.

"If you think about the periodicity of significant bear markets since 1970, we get a mean reversion about every ten years. That would be a 30 to 35% decline. Well, 35% on 250% of GDP is 89% of GDP. The reverse wealth effect, oh my gosh. 10% of our tax revenues are capital gains; they go to zero."

This isn't a perma bear making noise but Paul Tudor Jones called the 1987 crash before it happened and made 200% that year.

When he talks about mean reversion, he's speaking from a track record that almost nobody in finance can match and then he said this:

"If you buy the S&P at this current valuation, the 10-year forward returns are negative when you buy with the S&P P/E of 22. That's what history shows."

He's right, every major study on long-term equity returns shows that starting valuation is the single most predictive variable for 10-year forward performance.

At a P/E of 22, history doesn't give you a great answer.

"The real problem is, if you look at private equity in 2007 and 2008, that was about 7% of institutional portfolios. Now it's about 16%. Real estate's gone up. Infrastructure bets have gone up. We're so much more illiquid than we were in 2008."

In 2008, the crisis was bad because the system was leveraged.

Today the system is leveraged and illiquid, pension funds, endowments, and sovereign wealth funds can't hit a sell button on private equity.

They can't exit real estate in a week, when forced deleveraging starts in a system this illiquid, the exit doors are half the size they were last time.

Jones didn't say a crash is coming tomorrow.

He said the conditions that produce the worst outcomes in financial history are more present right now than at any prior peak he's seen in 50 years of trading.

He said buying the S&P at these levels and expecting the same returns as the past 100 years is math that doesn't work because those 100-year averages include decades when stocks were priced at 6 or 7 times earnings, not 22.

"Valuation matters a lot, and the stock market's really high, and it's going to be really hard to make money from here."

80

291

1,810

284,106

Apr 25

I have been all over Italy for 9 days. I have seen zero chemtrails, real contrails, zero illegal immigrants, and only a few homeless only at the Vatican. America is in severe decline and is ruled by evil and greed.

2

9

309

Apr 25

I believe that 75% of all jobs are fake and produce nothing of value. Just circular money flow to keep taxing to keep the ponzi scheme going. 99% for government jobs.

1

9

267

Apr 24

If you believe this "war" is meant to be won while they are simultaneously blowing up refineries, you should ride the short bus. It is a planned energy shortage for global control of movement. The world's long shot savior turned out to be a supervillian.

1

3

171