Joined June 2022

- Tweets 1,081

- Following 822

- Followers 700

- Likes 18,580

49 Photos and videos

Asset Battle —Post #3

The Hyper-Growth Faceoff: $QQQM vs $SCHG

For investors under 40 seeking to maximize their core growth pillar, the debate often narrows down to these two aggressive capital vehicles. Let’s look at the underlying financial plumbing to distinguish them:

⚡ Gladiator 1: $QQQM (Invesco NASDAQ 100 ETF)

• Expense Ratio: 0.15%

• Index Strategy: Tracks the 100 largest non-financial companies on the Nasdaq. It uses a strict modified market-cap weighting system.

• Key Metric: Highly concentrated. The top 10 holdings routinely control over 45% of the fund. It represents a direct, unfiltered bet on secular technological dominance and artificial intelligence infrastructure.

🚀 Gladiator 2: $SCHG (Schwab U.S. Large-Cap Growth ETF)

• Expense Ratio: 0.04% (Significantly lower cost drag)

• Index Strategy: Selects companies from the Dow Jones U.S. Large-Cap Total Stock Market Index based on four growth factors: forward earnings-to-price, historical revenue growth, multi-year asset growth, and internal cash flow velocity.

• Key Metric: Broader diversification. It contains over 240 stocks, spreading risk beyond just pure-play tech into consumer discretionary and healthcare innovators.

The Allocation Rule: Choose QQQM if you want a pure, unhedged exposure to tech-heavy operational monopolies and accept higher peak-to-trough volatility. Choose SCHG if you want a highly efficient, mathematically screened growth bucket with lower sector concentration risk.

25

The Dividend Math — Post #1

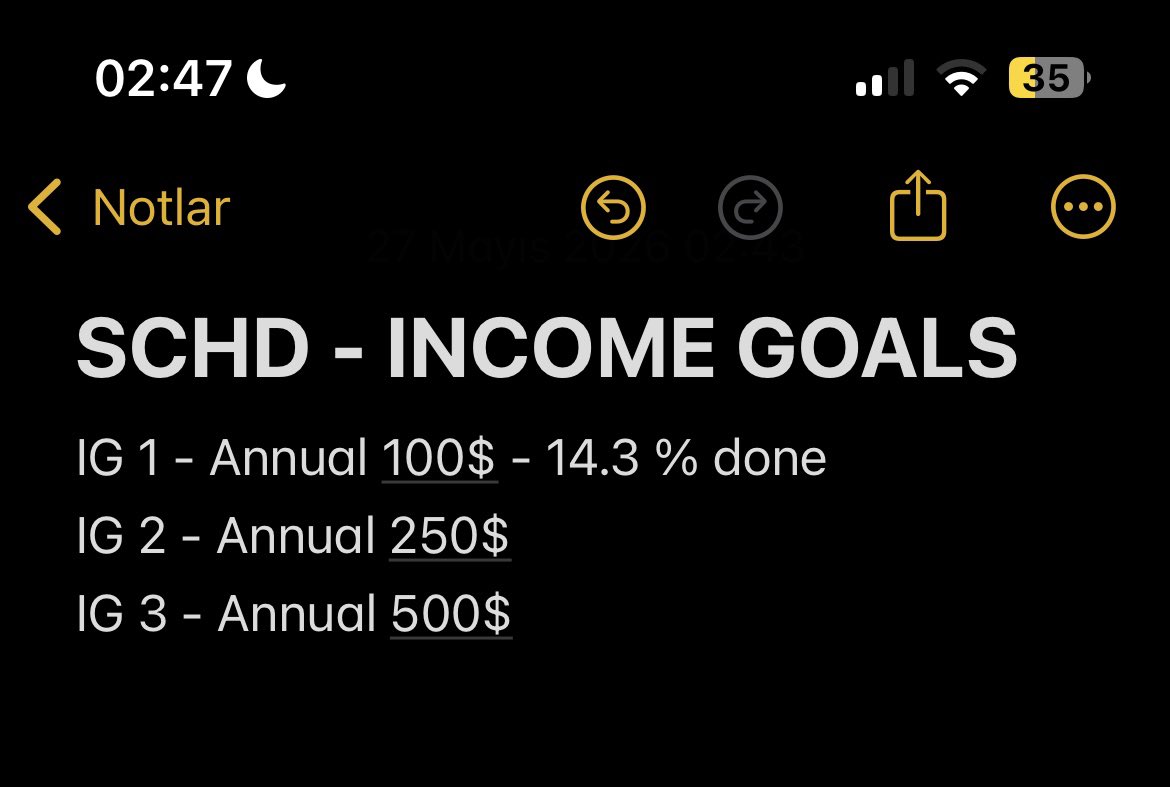

The 10-Year Dividend Snowball: Why $SCHD is the ultimate engine for patient money.

Amateurs look at SCHD's current starting dividend yield of roughly 3.4% and say, "That's too low, I can get 5% in a basic cash account." They are completely blind to a metric called the *Dividend Growth Rate (DGR)*.

Over the last decade, SCHD has maintained an average annual dividend growth rate of approximately 11%. Let’s look at what that exact percentage does to your real wealth over a 10-year accumulation phase:

Imagine you deploy $50,000 into SCHD today.

• Year 1: You receive a solid but modest ~$1,700 in annual dividends.

• Year 5: Because the corporations inside the fund are growing and raising their payouts, your annual cash flow climbs past $2,600 without you adding a single extra dollar.

• Year 10: Your annual dividend check crosses a massive $4,800.

Your personal "Yield on Cost" has more than doubled from 3.4% to nearly 10% on your original money. And this doesn't even factor in the fact that your initial $50,000 principal has significantly appreciated in market value.

Stop chasing high static yields that never grow. Invest in dividend growth velocity.

6

7

269

The Portfolio Blueprints — Post #1

The Ultimate 3-ETF Long-Term Portfolio:

A 10 year blueprint for hands-off wealth creation.

Imagine building a financial engine that doesn't just grow your capital over the next decade, but also drops real, withdrawable cash into your account every single month. Here is the ultimate 3-pillar "set-and-forget" portfolio designed for long-term compounding:

1. 🚀 The Core Growth Engine: $VOO or $SCHG

• Allocation: 50%

• The Play: Capture the unstoppable expansion of the US economy. VOO gives you the gold-standard S&P 500, while SCHG tilts heavily into hyper-growth tech giants like Apple, Microsoft, and Nvidia. This builds your massive tower of core wealth.

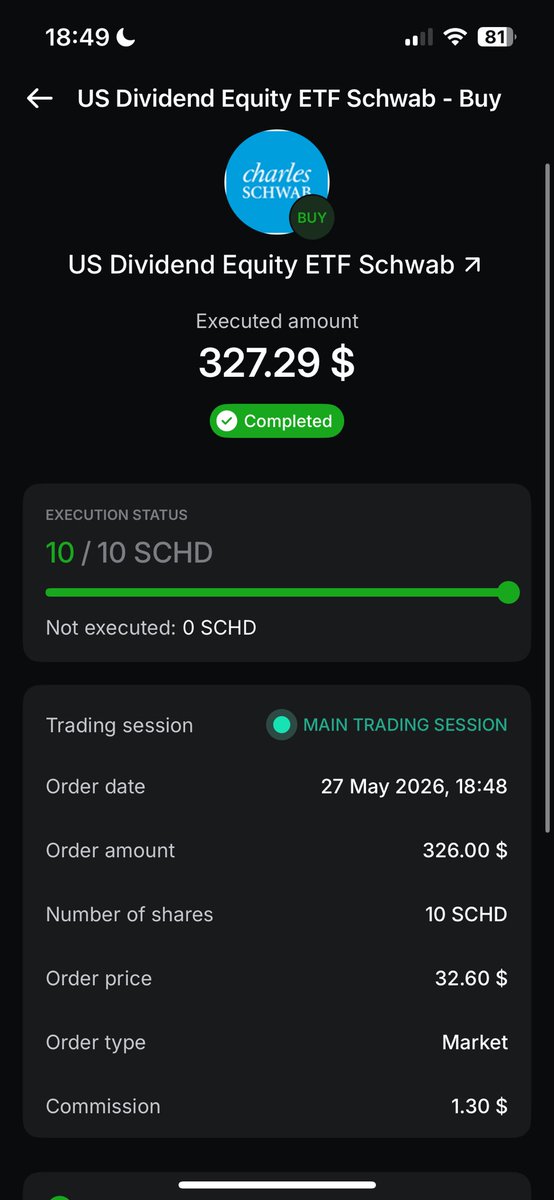

2. ☃️ The Compounding Machine: $SCHD

• Allocation: 30%

• The Play: Schwab U.S. Dividend Equity ETF doesn't just hunt yield; it selects 100 financially bulletproof companies that raise their payouts like clockwork. Over 10 years, this dividend growth behaves like an un-killable snowball.

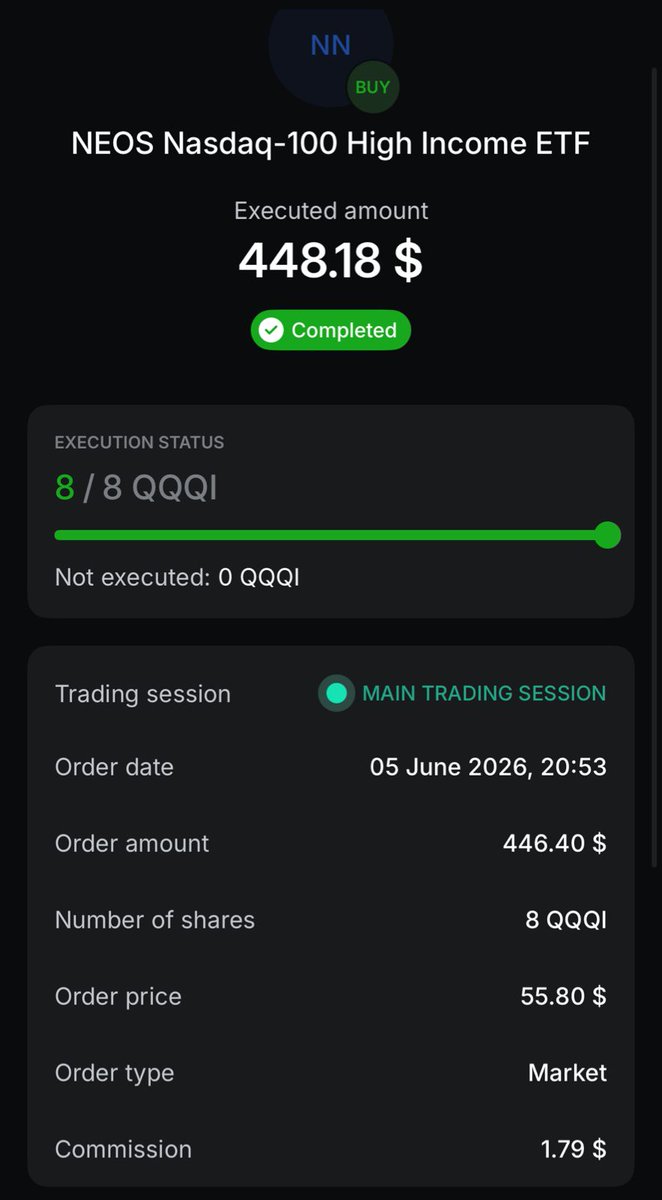

3. 💸 The Cash Booster: $QQQI

• Allocation: 20%

• The Play: NEOS Nasdaq 100 High Income ETF uses advanced covered call options mechanics to extract an incredible ~14% annual yield, paid out in monthly cash checks.

The Strategic Loop: During your accumulation phase, you don't spend the QQQI monthly cash. Instead, you instantly route those distributions back into VOO and SCHD.

You are using Wall Street option premiums to fundamentally fund your core shares for free.

4

75

The Alternative ETF Guide — Post #16

Asset Profile: QQQ (Invesco QQQ Trust) — The Innovation Concentration

Let's look at the absolute gold standard of technology accumulation. Launched on March 10, 1999, right at the peak of the Dot-Com bubble, QQQ tracks the 100 largest non-financial companies listed on the NASDAQ exchange.

Let's look at the hard historical data of what happens when you buy human innovation over a 25-year window:

📊 The Historical Simulation:

If you had invested a lump sum of $10,000 into QQQ on January 1, 2010—right as the modern smartphone and cloud ecosystem began to scale out:

• By 2015: Your $10,000 was worth $22,500.

• By 2020: Your capital exploded to roughly $48,000.

• By today in 2026: That single $10,000 check has snowballed into an estimated $115,000.

Expense Ratio: 0.20% (Highly efficient for the raw firepower it provides).

Warning: QQQ is heavily concentrated in mega-cap tech (Apple, Microsoft, Nvidia, Amazon). You are not buying a balanced economy; you are betting that tech monopolies will continue to consume global corporate margins. If that is your thesis, buy it, hold it, and never look back.

5

84

The Brutal Truth — Post #16

The "Safe Cash" Delusion: The mathematical reality of your emergency fund.

Let’s look at the exact numbers over a 20-year timeline to see what holding "safe cash" actually costs you.

Imagine you keep a permanent $40,000 "emergency fund" sitting in a standard, traditional bank account because it makes you feel secure. You want to know it's there, untouched.

Let’s run the real data based on historical inflation vs. market compounding:

• After 20 years of a standard 3% average inflation wave, your $40,000 cash reserve still reads "$40,000" on your screen. But its actual physical purchasing power has been quietly slashed to roughly $22,000. You lost half your wealth without spending a single dime.

• Now imagine you kept just $10,000 in cash for true emergencies, and deployed the other $30,000 into a broad US index fund (VOO). Over those same 20 years, at the historical 10% average return, that $30,000 compounds into roughly $201,800.

Holding massive cash reserves isn't "risk management"—it is a guaranteed, slow-motion liquidation of your lifetime labor. Minimize your cash drag, maximize your asset velocity.

1

9

125

Jun 12

The Fee Autopsy — Post #1

The Silent Bank Robbery: How a tiny 1.5% wealth management fee steals 40% of your total lifetime wealth.

When you hire a traditional financial advisor or buy an actively managed bank fund, they tell you: "We only charge a tiny 1.5% management fee to handle your portfolio. It's practically nothing."

Your brain thinks: "Great, if the market returns 10%, I keep 8.5%. That's a fair deal."

Let’s run the exact 35-year simulation out to a standard retirement timeline with a $100,000 starting portfolio:

• Scenario A (Self-Invested): You buy a cheap index fund with a 0.03% fee. At a 10% market return, your money grows to $2,780,000.

• Scenario B (Managed Fund): You pay that "tiny" 1.5% fee. Your effective return drops to 8.5%. Your money grows to $1,740,000.

Where did the missing $1,040,000 go?

It went straight to the bank advisor’s bonuses.

Because of compounding math, that tiny 1.5% fee didn't take 1.5% of your money; it took **nearly 40% of your total lifetime wealth**. Fire your expensive advisor and buy the index yourself.

2

6

132

Jun 12

The Monopoly Engine — Post #1

The Greatest Corporate Theft in History: The math behind Mark Zuckerberg buying Instagram.

In April 2012, Mark Zuckerberg looked at a tiny photo-sharing app with only 13 employees and zero dollars in revenue called Instagram.

Wall Street laughed when Zuckerberg aggressively offered to buy it for exactly $1 Billion in cash and stock. Pundits called it the peak of Silikon Valley insanity.

Let's look at the data today, 14 years later:

Instagram doesn't just make revenue now; it generates over $50 Billion a year in ad sales alone.

Zuckerberg didn't just buy an app; he bought a structural global monopoly that choked out his competitors. He bought a cash machine for a price that represents less than two weeks of Meta's current profit margins.

When analyzing elite tech companies, stop looking at their current price. Look at their ability to use their cash to swallow future monopolies before they even emerge.

2

6

132

Jun 12

The Brutal Truth — Post #15

The "Apple Reality Check": Why saving for a luxury item is a mathematical disaster.

Let’s run the exact numbers on consumer hype versus investment power over a 25-year window:

Imagine it’s May 2001. Apple releases the very first iPod. It costs exactly $399.

• Consumer A is thrilled. They buy the iPod, listen to music, and 5 years later throw it in the trash when the battery dies. Value today: $0.

• Investor A decides to skip the tech hype. They take that exact same $399 and buy Apple stock ($AAPL) instead.

Let’s let the math run through every single stock split and dividend payout until today, 2026:

That single, boring $399 investment has snowballed into roughly $190,000.

One hundred and ninety thousand dollars. From the price of a single music player.

The brutal truth? You aren't broke because you don't earn enough money. You are broke because you keep buying the products instead of buying the companies that make them. Switch sides.

1

9

157

Jun 11

Asset Battle — Post #2

The Battle of Income vs Growth: JEPI vs QQQM

Let’s run an intense 15-year simulation with $50,000 to see what happens when you prioritize immediate monthly cash flow over raw technology growth.

🛡️ Gladiator 1: JEPI (JPMorgan Equity Premium Income ETF)

• Strategy: Uses stock options (covered calls) to pay out a massive ~8% to 10% cash dividend split into monthly checks.

• The Result: Your mailbox is flooded with cash every 30 days. It feels amazing. But because the fund caps your upside to pay that income, your initial $50,000 capital barely grows. In a booming market, you are running in place while heavily taxed on those monthly payouts.

🚀 Gladiator 2: QQQM (Invesco NASDAQ 100 ETF)

• Strategy: Tracks the top 100 tech giants (Apple, Microsoft, Nvidia) with a tiny 0.15% fee.

• The Result: It pays almost zero current income. But over a long horizon, the exponential earnings power of corporate tech turns that $50,000 into a massive tower of capital.

The Verdict: If you are 25 years old, buying JEPI is financial self-sabotage because you are trading decades of exponential growth for pocket change today. Buy growth (QQQM) when you are young; buy income (JEPI) only when you are ready to retire and live off the machine.

1

6

137

Jun 11

The Alternative ETF Guide — Post #15

Asset Profile: AVUV (Avantis U.S. Small Cap Value ETF) — The Factor Experiment

Let's look at one of the most famous long-term data studies in academic finance: The Fama-French Five-Factor Model. The numbers prove that over rolling 20-year periods, small-cap companies that are deeply undervalued (Small-Cap Value) historically outperform large, flashy tech monopolies.

Why? Because small companies have room to grow 1,000%, while multi-trillion-dollar giants physically cannot double their size overnight without consuming the entire global GDP.

AVUV is an institutional-grade ETF built specifically to capture this exact mathematical anomaly.

📊 The Quick Numbers:

• Expense Ratio: 0.25% (Slightly higher because it uses active factor screening)

• Core Metric: Filters out small-cap companies with weak cash flows or bad debts.

⚠️ The Reality:

For the last decade, large-cap tech (like Apple and Nvidia) has crushed everything, making small-cap value look boring. But if you look at a 50-year horizon, the math shifts heavily back to small-cap value. If you want a non-correlated asset to balance out your heavy tech holdings, look into AVUV.

3

107

Jun 10

On the surface, trading $24 for land that now holds Wall Street, Empire State, and Central Park looks like an absolute steal.

But imagine if those Native Americans didn't keep the trinkets. Imagine if they had a global brokerage account and invested that $24 into a compound interest vehicle returning a steady 7% annually.

1

1

90

Jun 10

$7.5 Trillion. That is enough money to buy the entire physical island of Manhattan back today, wipe out all its corporate debts, and still have trillions of dollars left over to buy the rest of New York state.

The land values grew massively, but they couldn't keep pace with the exponential growth of unchecked compounding math.

1

1

32

Jun 10

The lesson of 1626? Never underestimate the power of a tiny amount of money paired with a long horizon of time.

You don’t need a million dollars to start investing today; you just need a few dollars and the patience to let the exponential curve do its work. Hit follow for more fascinating financial breakdowns!

29

Jun 10

Financial History Chronicles — Post #9

In 1626, a Dutch explorer named Peter Minuit made what financial textbooks call the "greatest real estate deal in history." He purchased the entire island of Manhattan from Native Americans for a small bundle of beads and trinkets worth exactly $24.

Today, Manhattan real estate is worth over $2 Trillion.

But if you run the actual mathematical calculation, the Dutch explorer actually lost the deal. Here is the mind-blowing math of compounding interest: 🧵

1

1

78

Jun 10

The Brutal Truth — Post #14

The "Waiting for a Crash" Paradox: How your caution is quietly keeping you broke.

Let's look at exact historical data:

In 2015, Investor A decided to invest $500 every month into the S&P 500 immediately.

Investor B decided the market was "too high" and kept their $500 a month in cash, waiting for a massive 20% crash to buy the absolute bottom.

By the time a major market drop finally happened in March 2020:

• Investor A’s portfolio had already grown by over 60%, creating a massive financial cushion.

• Even after the 2020 crash cut the market by 30%, Investor A was STILL wealthier than Investor B.

• Investor B bought the "bottom," but they bought it at a price that was higher than the market's 2015 starting point.

Market corrections don't happen often enough to compensate for the gains you miss while sitting on the sidelines in cash.

Stop waiting for the perfect red day. Time beats timing. Every single time.

1

1

6

153

Jun 10

The Asset Battle — Post #1

Let’s settle the ultimate financial debate with raw historical returns over the last 30 years:

S&P 500 vs. Gold

If you had invested $10,000 into both assets in 1996, here is what the exact numbers look like today:

🏆 Gold:

Your $10,000 turned into roughly $68,000.

It acted as a solid, safe shield against inflation and economic crises. It did its job.

🚀 The S&P 500 (with dividends reinvested):

Your $10,000 exploded into approximately $174,000.

Why the massive gap? Because Gold is a static metal that just sits in a vault looking pretty. It doesn't create new products, it doesn't hire geniuses, and it doesn't pay you dividends.

The stock market is an engine of human productivity.

Buy the engine, not the metal.

3

6

159