🔗 $SLINK 🔗 | Institutional Upside. Retail Access. Exposure to Securitize private equity & other RWAs. On path to regulated asset-backed token. NFA DYOR

Joined February 2026

- Tweets 3,357

- Following 154

- Followers 792

- Likes 2,212

170 Photos and videos

1/ Deep dive thread: Why $SLINK offers one of the most compelling asymmetric plays in the tokenized Real World Assets space right now.

If you understand where RWAs are heading and the infrastructure powering that shift, this story gets very interesting.

Let us walk you through it👇

14

10

53

4,525

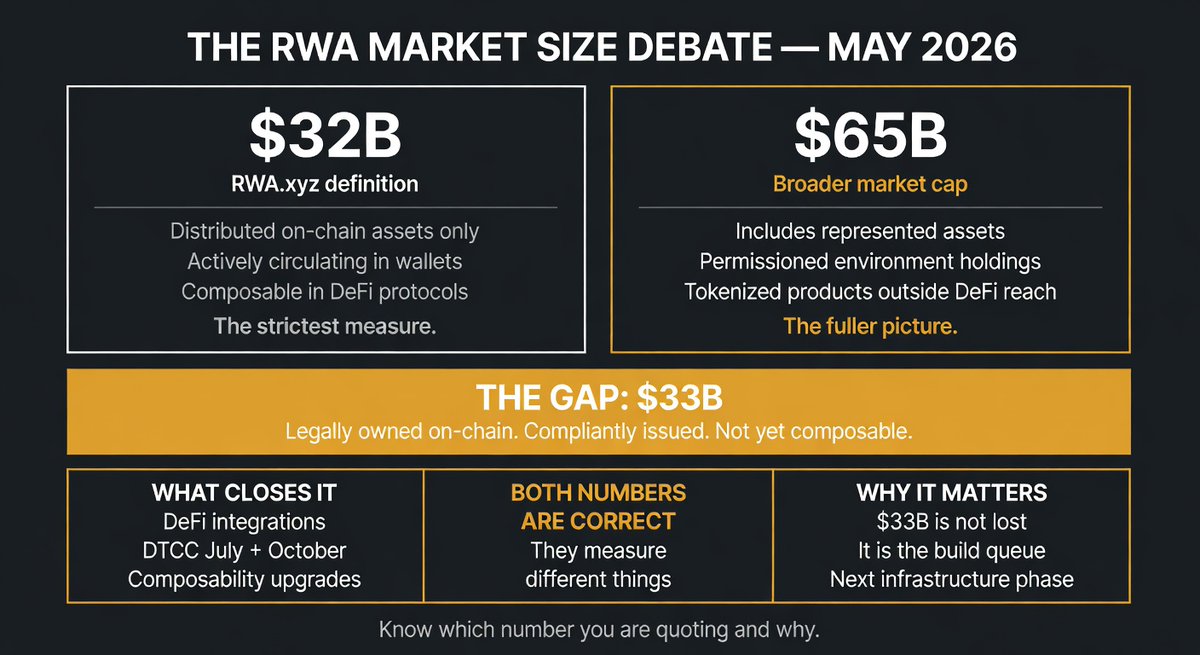

Two numbers are floating around for the RWA market right now.

$32 billion. And $65 billion.

Both are correct. They measure different things. Nobody is explaining the gap.

$32 billion is the RWA.xyz figure. Distributed on-chain assets only. Actively circulating. Usable in protocols. The strictest definition.

$65 billion is the broader figure. Represented assets, permissioned environments, tokenized products sitting outside DeFi reach. All counted.

The $33 billion between them is not a data error.

It's the composability gap made visible as a dollar figure. Legally owned onchain. Compliantly issued. Not circulating. Not composable. Not in the smaller number.

When people debate whether RWA is a $32B or $65B market they are accidentally having the most important conversation in the sector.

The answer is both.

The distance between them is the next infrastructure problem being solved.

Know which number you are quoting and why.

1

2

157

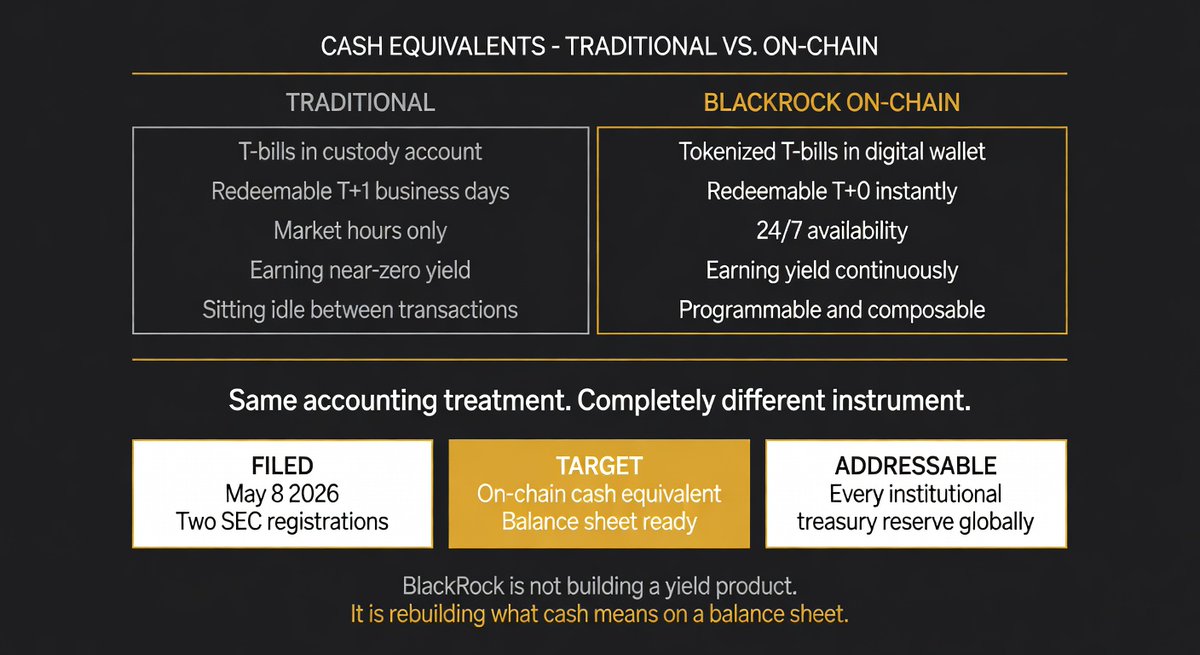

"Cash equivalent" is a specific accounting term.

It doesn't mean liquid. It doesn't mean safe. It means so liquid and stable it can be treated as cash on a balance sheet. T 0 settlement. Near-zero price risk. Immediate redemption.

BlackRock is engineering tokenized Treasuries to meet that definition onchain.

The two new SEC filings are a deliberate step toward turning short term Treasuries and money market funds into onchain cash equivalents, designed to hold cash, short term U.S. Treasuries, and overnight repo agreements backed by Treasuries.

That's not a yield product. That's not an investment.

That's cash in programmable form.

The implication for institutional treasury management is significant.

Every corporation, fund, and institution that holds cash equivalents on a balance sheet, for liquidity, for operational reserves, for margin requirements, can now hold that position onchain.

Earning yield. Moving instantly. Available 24/7.

The question was never whether institutions would hold tokenized assets.

It was whether tokenized assets could replace the most fundamental instrument on every institutional balance sheet.

BlackRock just filed the answer.

1

1

110

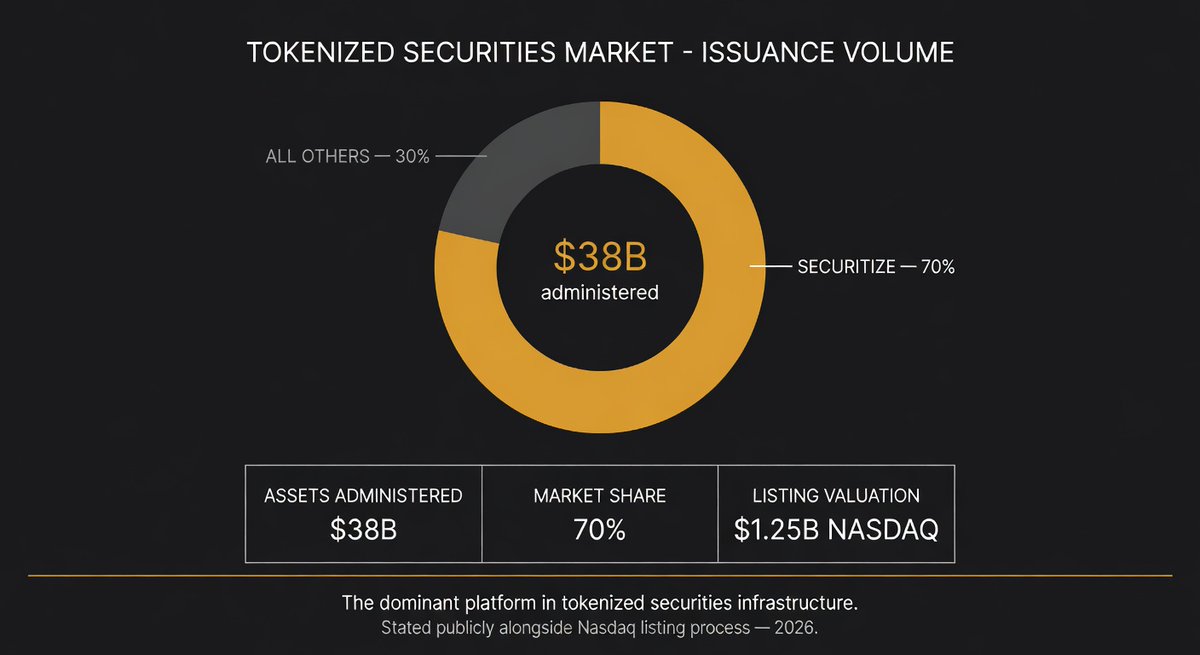

Most people anchor $SLINK to one data point.

The 17,000 seed shares. The 2018 entry. The pre listing window.

Those are real. But there's a number Securitize has stated publicly alongside its Nasdaq listing process that nobody is using.

70%.

Securitize claims 70% of the tokenized securities market by issuance volume. $38 billion administered. Not fund AUM, total tokenized assets processed through the platform.

That's not a promotional tweet. It's a figure stated publicly alongside a $1.25B Nasdaq listing process.

The community token built around the RWA infrastructure thesis isn't anchored to a challenger or a contender.

It's anchored to the platform that processes 7 out of every 10 tokenized securities issued.

No affiliation claimed. No returns promised. No structural connection between $SLINK and Securitize revenue.

Just an honest read on what 70% market share means as a credibility anchor for a community token built around exactly this infrastructure.

The founder didn't build $SLINK around an interesting company.

They built it around the dominant one.

1

1

103

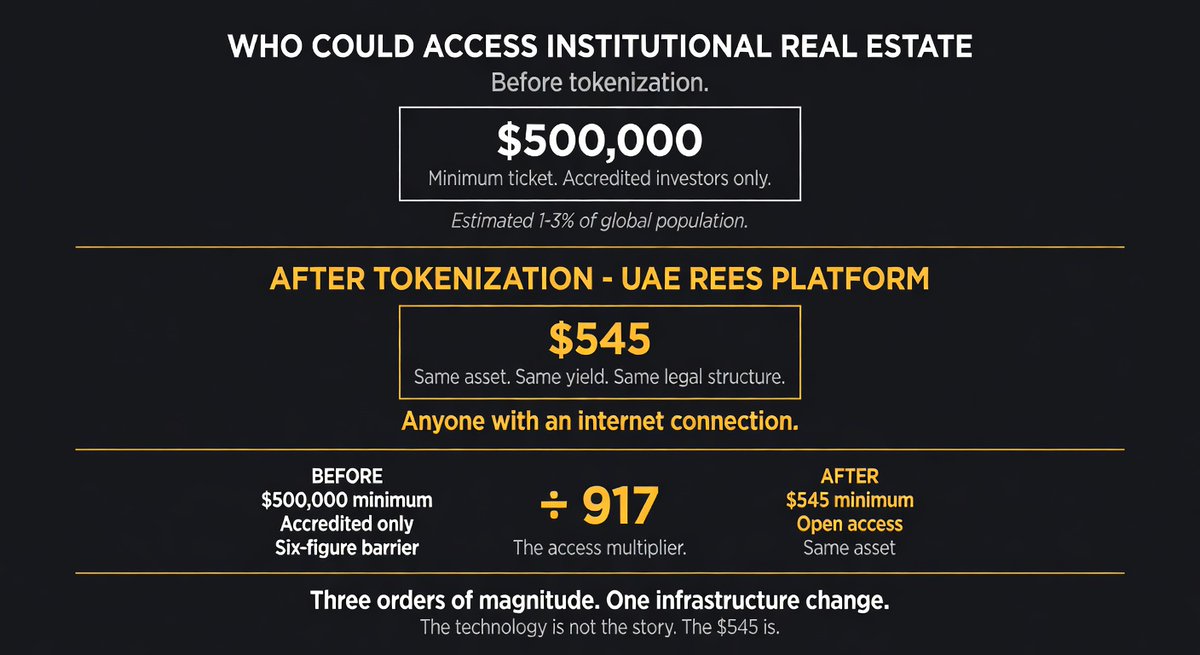

Traditional real estate investment vehicles: $500,000 minimum.

UAE's tokenized real estate platform: $545 minimum.

That's not a marginal improvement in access.

It's three orders of magnitude.

The democratization argument for RWA tokenization is usually stated abstractly - "fractional ownership," "broader access," "financial inclusion."

Those phrases don't land because they don't have a number attached.

$545 does.

For $545 you get exposure to institutional grade real estate in one of the world's fastest growing property markets. Same underlying asset. Same yield profile. Same legal structure.

The only thing that changed is the minimum ticket size.

That change matters more than any technology discussion about which chain it runs on or which protocol handles settlement. The access structure is what determines who can build a diversified real asset portfolio.

Previously: accredited investors with six figure minimums.

Now: anyone with $545 and an internet connection.

The infrastructure made that possible. The $545 is the proof it worked.

2

1

93

ShareLink retweeted

May 22

The world is about to change.

Trillions will be tokenized.

175

523

3,289

151,840

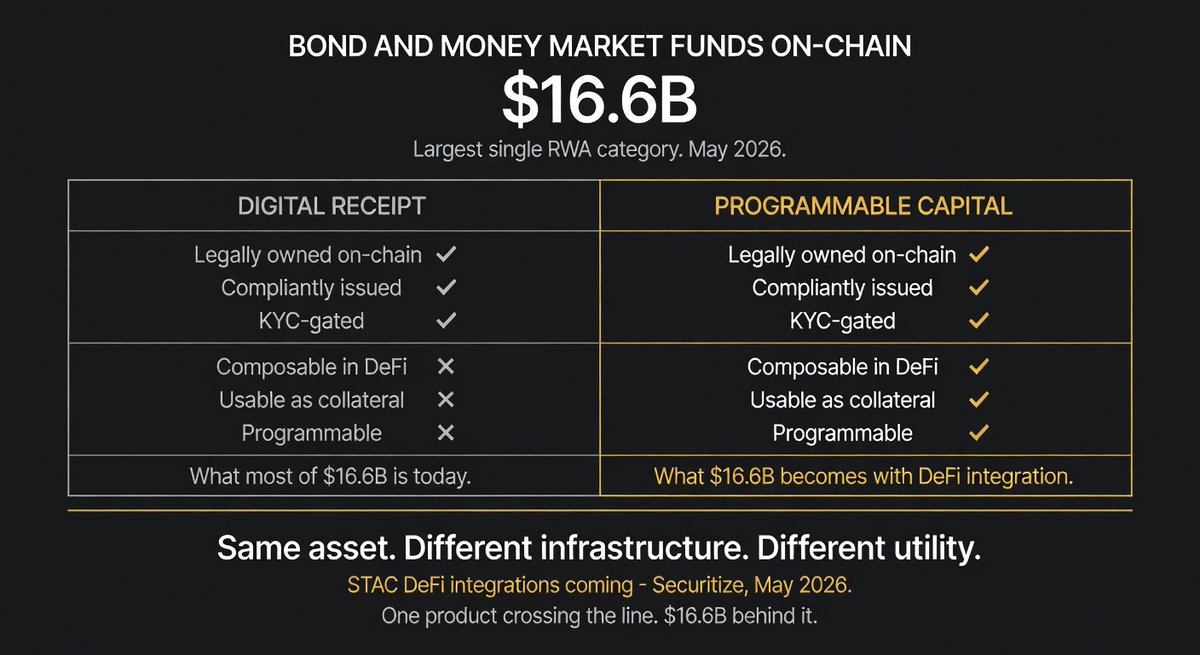

The largest RWA category barely touches DeFi.

Bond and money market funds: $16.6 billion onchain.

Active in DeFi protocols: minimal.

That's the single largest untapped composability gap in the entire tokenized asset market.

$16.6 billion in fixed income, legally owned onchain, compliantly issued, KYC gated, sitting outside the lending markets and collateral vaults that make it actually useful.

A tokenized bond that can't be posted as collateral is a digital receipt.

A tokenized bond that can be posted as collateral, borrowed against, used in yield strategies, and moved across protocols is programmable capital.

Same asset. Completely different utility profile.

The infrastructure connecting the two is being built right now. Securitize's STAC - AAA CLO fund, 4.38% April yield, announced DeFi integrations coming.

That's one product moving from digital receipt to programmable capital.

$16.6 billion in the same category is sitting behind that same gate.

When fixed income composability unlocks at scale, that $2.47B active in DeFi number doesn't grow gradually.

2

3

131

Securitize will not issue a token.

For a regulated entity courting BlackRock, Apollo, KKR, that's the right call.

A platform token would compromise the institutional posture they've spent years building. RIA registration, transfer agent license, broker dealer status. None of that survives a token sale aimed at retail.

So they walked away from the easiest fundraise in crypto. On purpose.

That choice is exactly why the narrative around Securitize has nowhere to express itself onchain.

BUIDL is gated. ACRED is gated. Every flagship product sits behind KYC walls built for institutional flow, not for the community that's been watching this thesis develop since 2023.

The vacuum is real. And vacuums get filled.

$SLINK fills it without pretending to be something it isn't. No claim on platform revenue. No structural tie. No fake integration story.

Just a liquid proxy for people who want to stay positioned around the thesis while the institutions trade it privately.

The honest framing is what makes it credible.

Anything else would collapse the moment someone read the disclosures.

1

1

2

135

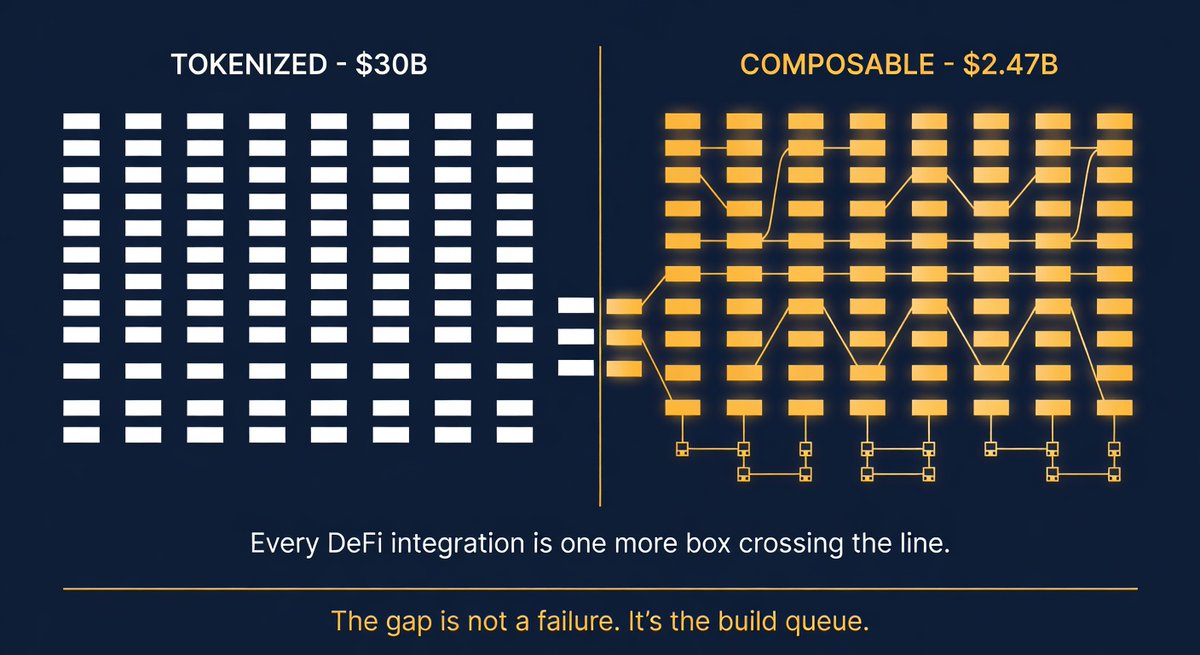

$30 billion tokenized onchain.

$2.47 billion active in DeFi.

That's 8.2% utilization. The other 91.8% sits in permissioned environments, legally owned onchain, compliantly issued, KYC gated. But not composable.

Not moving through lending markets. Not serving as collateral in open protocols.

Most people read that as a failure of the RWA thesis.

It's the opposite.

$27B in tokenized assets sitting outside DeFi is not stranded capital. It's the next infrastructure problem being solved in real time.

Securitize just posted STAC's April yield - 4.38% on a tokenized AAA CLO fund, with "DeFi integrations coming" at the end of the announcement.

That's one product moving from the 91.8% into the 8.2%.

Every DeFi integration announcement is the same move. A permissioned asset crossing into composable infrastructure. A digital receipt becoming programmable capital.

The gap between $30B tokenized and $2.47B composable is not a ceiling.

It's the build queue.

5

5

117

ShareLink retweeted

May 19

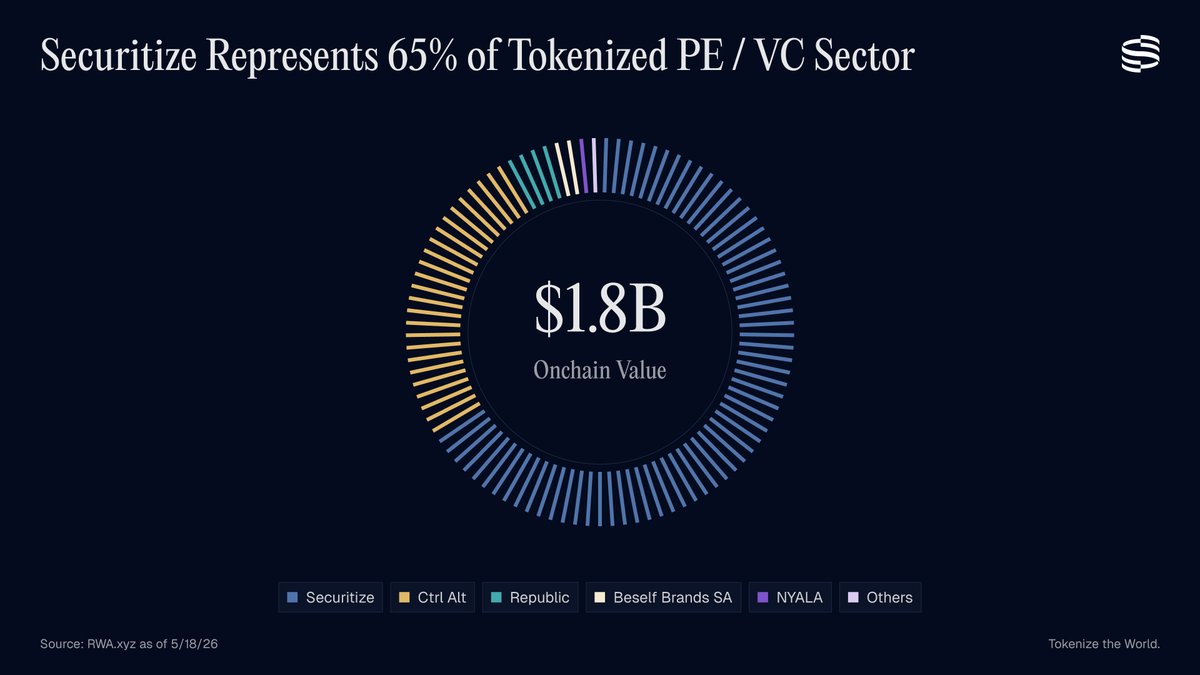

Securitize is the leading platform for tokenized private equity and venture capital funds.

20

21

171

9,240

The newest Ethereum wallets have no DeFi history.

No Uniswap. No Aave. No farming, no airdrops, no governance votes.

Just BUIDL. Or OUSG. Or ACRED.

Chainalysis flagged the pattern, wallets opened in late 2025 and early 2026 specifically to hold tokenized treasuries and private credit. Single purpose. Single asset. First action onchain, only action onchain.

Every prior adoption wave arrived for speculation and stayed for utility.

This one arrived for utility and skipped speculation entirely.

DeFi protocols got built for the previous user. The new user doesn't trade, doesn't farm, doesn't compose. They allocate and they hold.

Onchain quietly grew a second floor that doesn't visit the first one.

2

3

86

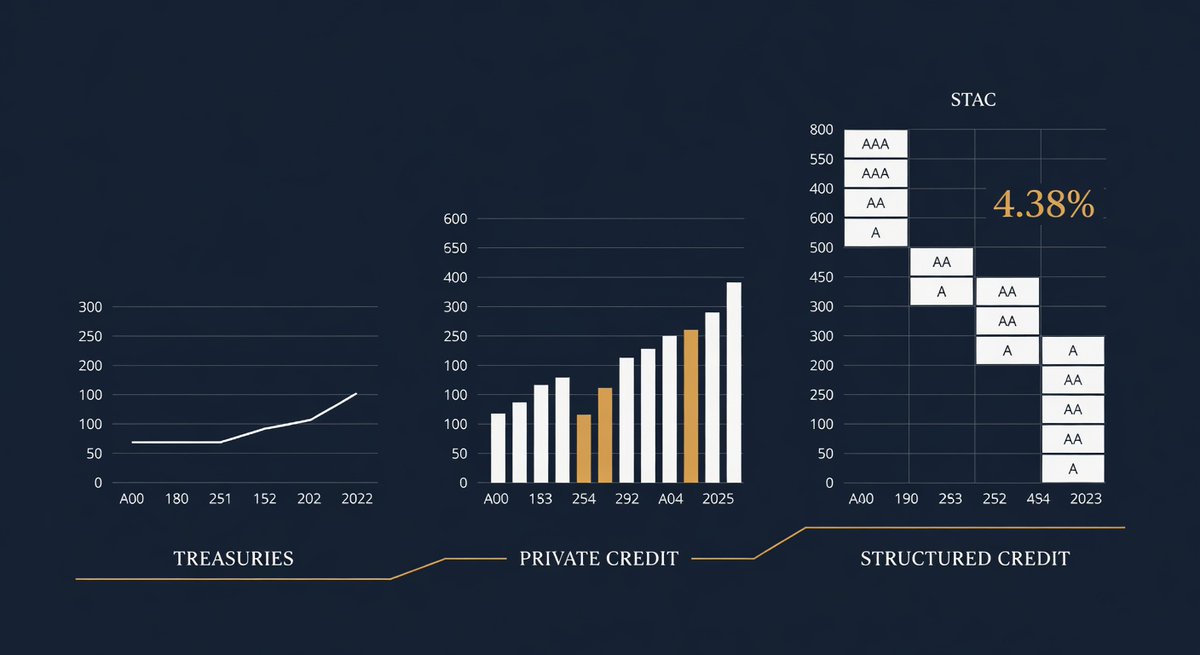

Treasuries first.

Treasuries first.

Private credit next.

Structured credit now.

Each step climbs further up the complexity curve TradFi rails couldn't distribute at retail speed.

BUIDL taught DeFi to hold yield bearing collateral. ACRED extended that into private credit.

STAC now brings AAA structured credit into the same envelope, 4.38%, 24/7, on an asset class that historically trades by appointment.

The "DeFi integrations coming soon" line is where this stops reading like a fund and starts reading like collateral infrastructure.

$SLINK sits adjacent to that arc. Narrative exposure to the platform quietly stocking the onchain balance sheet one asset class at a time.

3

9

178

ShareLink retweeted

May 18

The Securitize Tokenized AAA CLO Fund (STAC) achieved a 4.38% 30-day yield from April 1, 2026 through April 30, 2026.

STAC gives investors onchain access to fixed income.

DeFi integrations coming soon.

38

10

98

7,716

The CLARITY Act isn't enabling new products.

It's releasing products that already exist.

Bernstein Research estimates more than 40 institutional tokenized fund products are currently in SEC preregistration or registration review, representing a $15 to $25 billion pipeline of new on-chain RWA assets.

These aren't ideas. They're products that completed internal approval, cleared legal review, passed compliance sign off, and are sitting in holding patterns waiting for regulatory classification to settle.

The CLARITY Act is a gate, not a starting line.

When it passes, 40 products don't launch gradually. They launch into a market that already has $33B in distributed assets, 792,000 holders, and infrastructure that didn't exist 18 months ago.

The current $33B figure represents what launched without regulatory certainty.

The $15 - 25B pipeline represents what was built specifically for the moment that certainty arrived.

That moment is Q3 2026.

The queue is longer than the current market suggests.

3

97

ShareLink retweeted

May 18

It's a good week to Tokenize the World.

51

52

465

14,280

Why is RWA adoption exploding right now, and not 5 years ago?

Three structural forces are converging simultaneously:

-Blockchain scalability has reached institutional grade (sub second finality, <$0.01 fees, 65k TPS on Solana)

-Regulatory frameworks like MiCA and the CLARITY Act are providing legal certainty for tokenized securities

-Institutions face persistent low real yields in traditional markets, driving demand for onchain structured credit and Treasuries yielding 5-12%

This combination is moving tokenization from experimental pilots to production grade institutional deployment.

The infrastructure layer is maturing, capital is incentivized, and regulatory risk is dropping.

The window is wide open, and it won’t stay this favorable forever

2

5

170

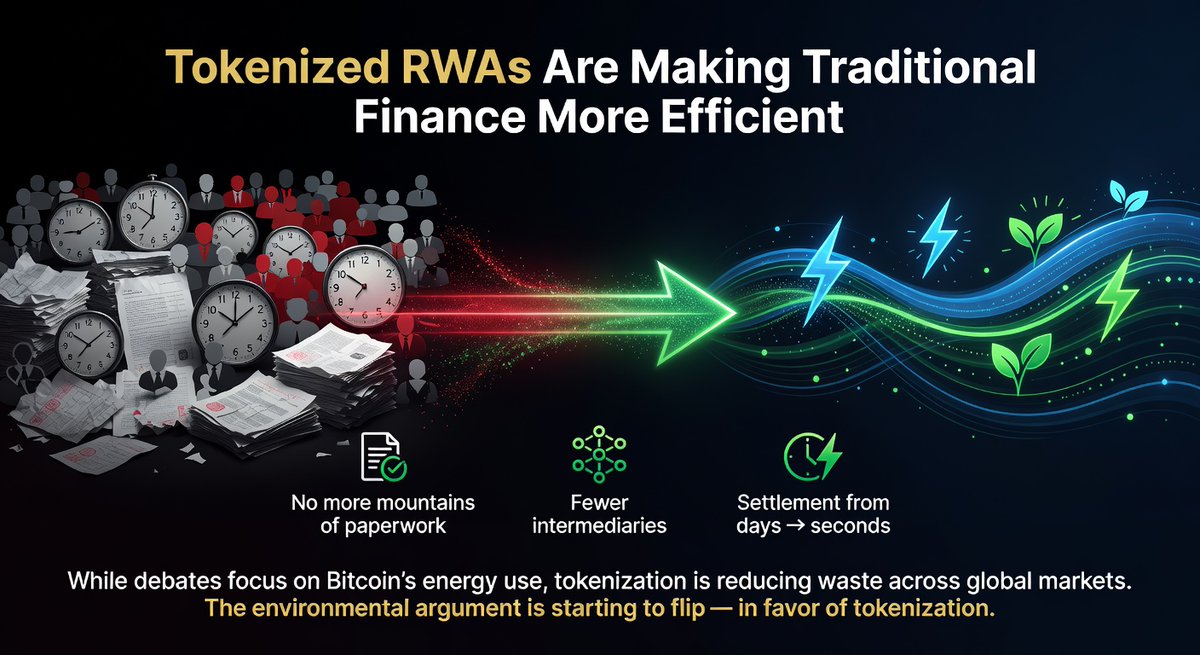

Tokenized RWAs are quietly making traditional finance dramatically more efficient.

No more mountains of paperwork.

Fewer intermediaries.

Settlement times cut from days to seconds.

While debates rage about Bitcoin’s energy use, tokenization is reducing waste across global markets, one asset at a time.

Every tokenized transaction removes friction and unnecessary bureaucracy from the old system.

Over time, this efficiency gain could become one of the strongest environmental cases for blockchain technology.

The argument is starting to flip.

In favor of tokenization.

3

2

7

136

In a market full of loud promises and complicated tokenomics…

$SLINK does one thing only.

It gives you clean, liquid, fair launched exposure to the Securitize narrative, the leading institutional tokenization platform.

No yield farming. No fake utility. No team dumps.

The point?

While most tokens chase hype, $SLINK was created as pure community conviction in the growth of institutional tokenization and the companies building it, without the noise or overpromises.

Simple. Honest. Positioned for the long game.

2

1

5

92

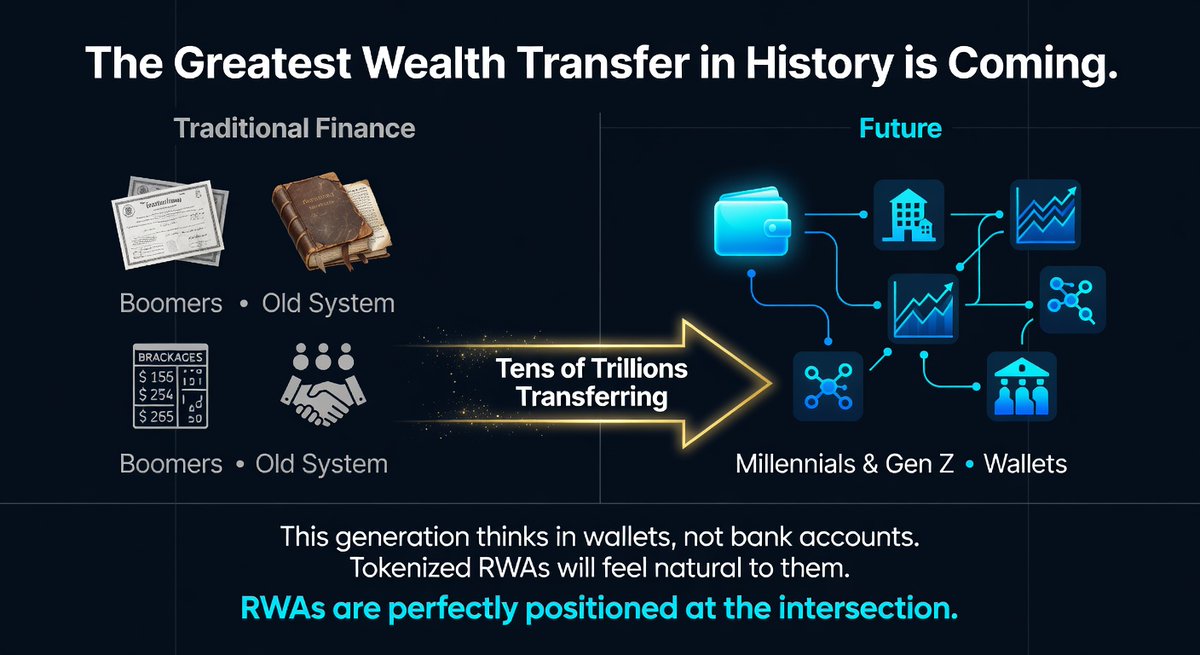

The Greatest Wealth Transfer in History is Coming.

Boomers are about to pass down tens of trillions to Millennials and Gen Z.

This new generation doesn’t think in bank accounts or dusty brokerage statements.

They think in wallets.

They want ownership they can see, move, and control 24/7.

This is why tokenized real estate, stocks, private credit, and funds will feel completely natural to them.

The biggest wealth transfer ever is about to meet the biggest technology shift in finance.

And RWAs are perfectly positioned at the intersection.

The handover is going to be massive.

1

5

7

140