SPML Infra is one of India’s oldest and largest urban infrastructure developers of water, wastewater, solid waste management and clean energy assets.

Joined March 2011

- Tweets 1,955

- Following 191

- Followers 554

- Likes 2,652

1,345 Photos and videos

Pinned Tweet

Jun 13

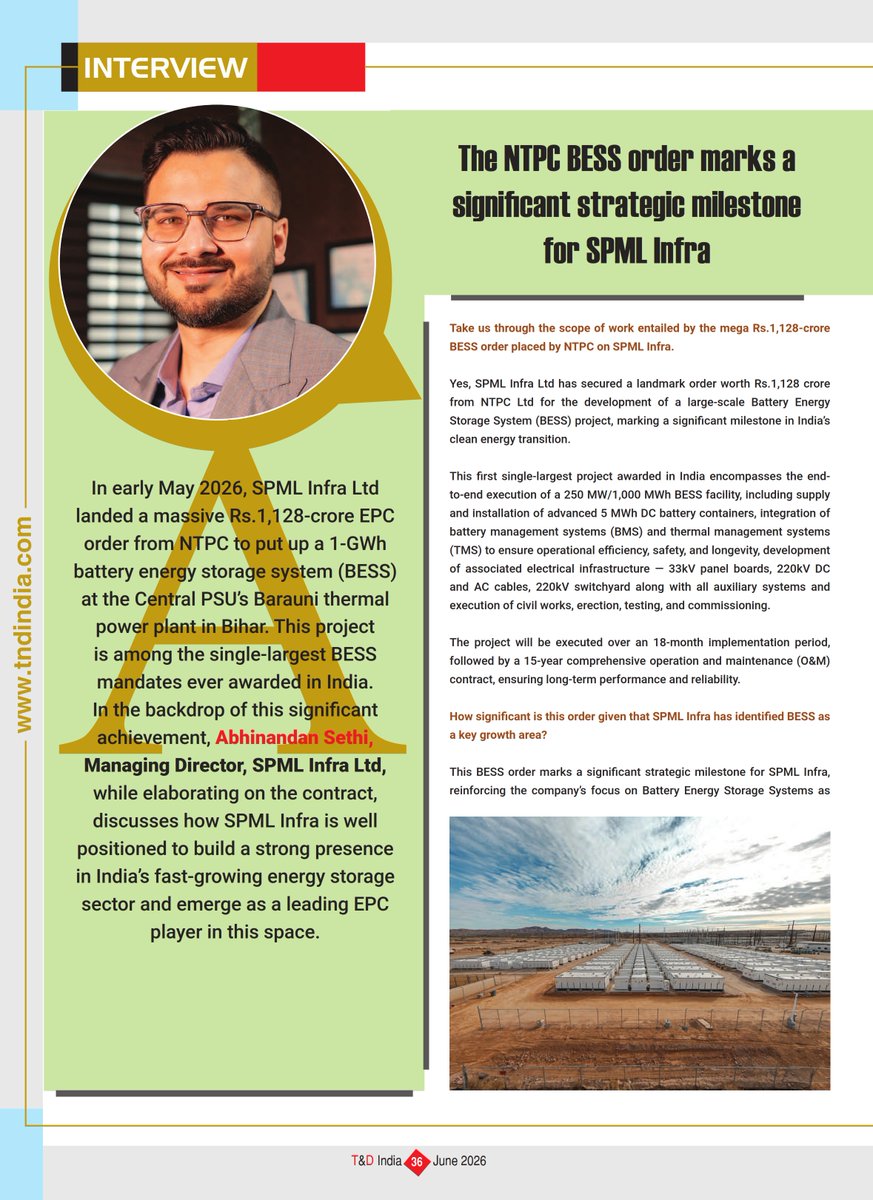

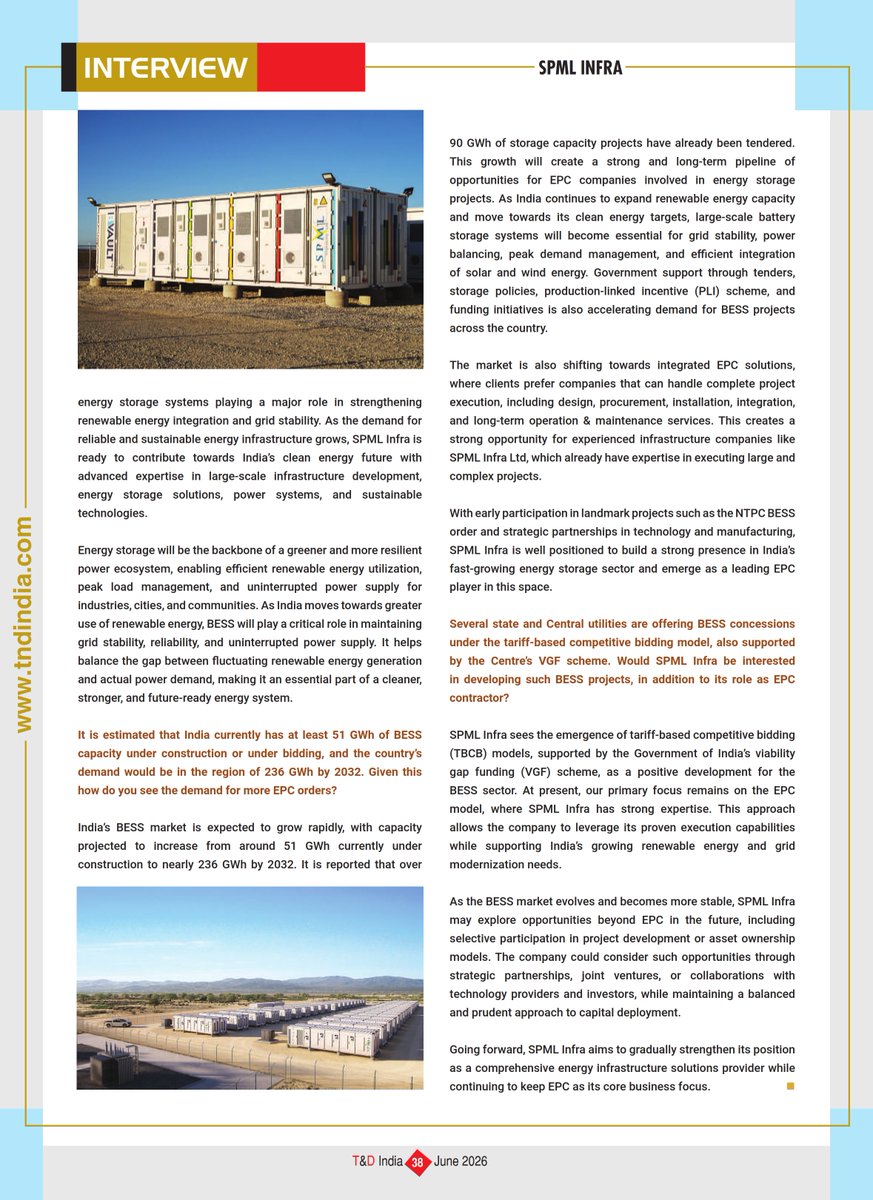

T&D India publishes insightful interview of Abhinandan Sethi, MD, @SPMLInfra

#SPMLInfra #AbhinandanSethi #BESS #BatteryEnergyStorage #BatteryEnergyStorageSystem #EnergyStorage #RenewableEnergy #CleanEnergy #PowerSector #EnergyTransition #GridStability #SustainableEnergy #EPC

1

2

38

May 27

T&D India interview of Abhinandan Sethi, MD, @SPMLInfra highlighting company’s landmark ₹1,128 Cr BESS project order. tndindia.com/the-ntpc-bess-o…

#SPMLInfra #AbhinandanSethi #BESS #BatteryEnergyStorage #BatteryEnergyStorageSystem #EnergyStorage #RenewableEnergy #CleanEnergy #Power

177

SPML Infra Limited retweeted

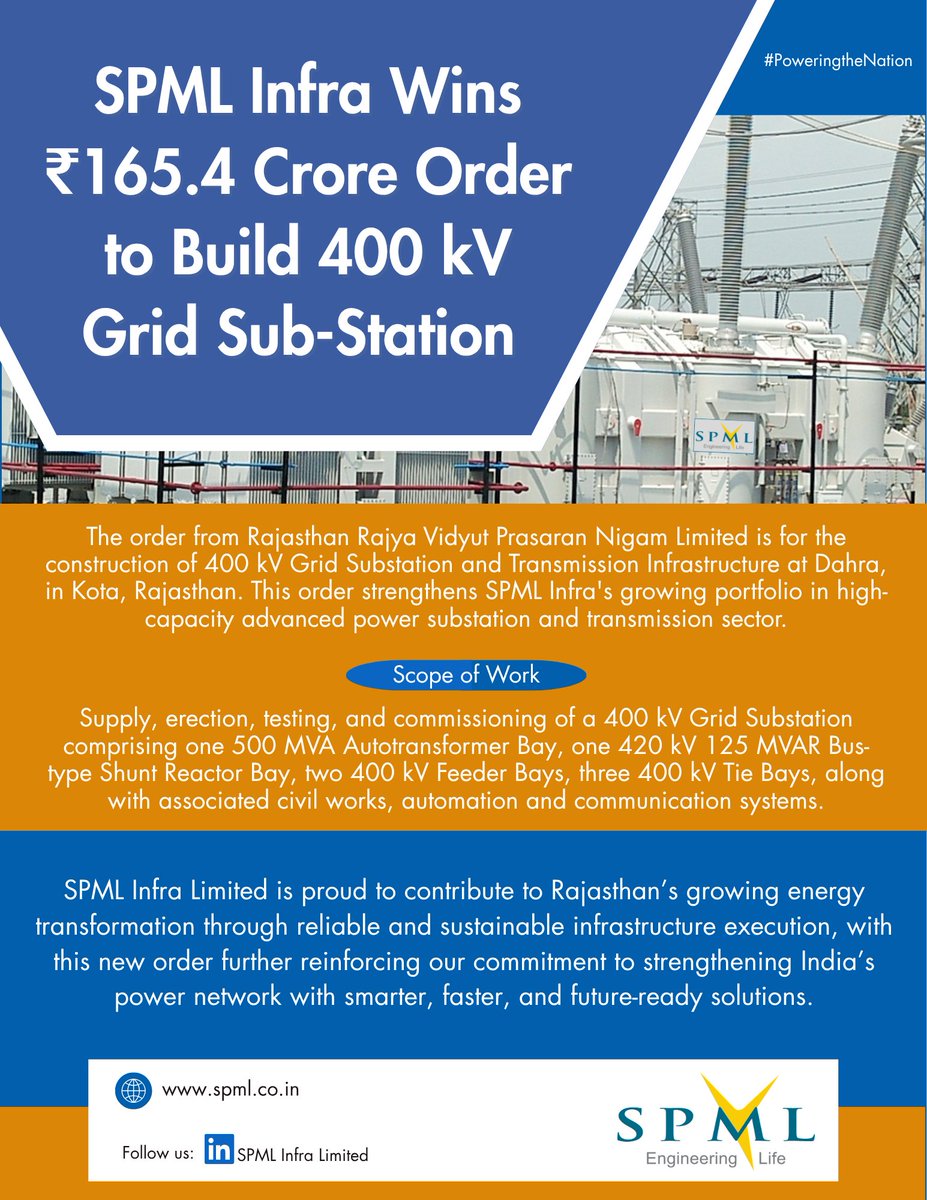

@SPMLINFRA Secures ₹165.41 Crore Rajasthan Grid Infrastructure Contract

#SPMLInfra Limited has secured a major contract worth ₹165.41 crore from Rajasthan Rajya Vidyut Prasaran Nigam Limited. Read the full article on

themachinemaker.com/news/spm…

1

1

135

May 22

@SPMLInfra wins order ₹165.41 Cr from Rajasthan Rajya Vidyut Prasaran Nigam Limited for construction of 400 kV Grid Substation.

#SPMLInfra #RRVPNL #PowerInfrastructure #PowerProject #Transmission #Substation #GridSubstation #EnergyInfrastructure #PowerSector #ReliablePower

2

77

May 20

Happy International HR Day! @SPMLINFRA celebrate invaluable contribution of HR team in building a strong, inclusive, and people-centric workplace.

#InternationalHRDay #HRDay #HumanResources #PeopleFirst #EmployeeEngagement #WorkplaceCulture #TeamSPML #SPMLInfra

59

SPML Infra Limited retweeted

Apr 28

SPML Infra: A Quiet Turnaround — And the Promoter Is Buying (Our IR client)

From ₹1,657 cr in borrowings and a ₹117 cr loss in FY21 to ₹60 cr TTM profit —The board of SPML Infra Limited (NSE: SPMLINFRA) approved a ₹190 cr capital infusion on April 23, 2026 — combining preferential equity & warrants. The headline is the BESS capex, but the bigger story sitting underneath is a textbook financial turnaround that's been quietly compounding for four years — and a promoter group that's now putting its own capital in to back what comes next.

1. The financial turnaround is here and verifiable - This is the foundation everything else rests on. Borrowings have come down from ₹1,657 cr (FY21) to ₹380 cr (Dec 2025) — an 81% reduction in four years. Net profit went from ₹(117) cr in FY21 to ₹48 cr in FY25 to ₹60 cr TTM. Reserves built from ₹254 cr to ₹788 cr. ROCE has climbed from 1% (FY22) to 9%; ROE 7.78%. 5-year profit CAGR is 49%, 3-year CAGR is 431%, TTM growth is 134% — compounding off a low base, but real and accelerating. None of this is forward-looking; it's already in the financials. Q3 FY26 (Dec 2025) is the inflection quarter: revenue ₹230 cr at 11% operating margin — well above the 5-6% range of the previous five quarters, and the highest since the recovery began. New orders of ₹4,324 cr (including a ₹1,128 cr NTPC Thermal Power Stations BESS order) provide FY27-28 visibility.

2. The promoter group is showing real conviction — Promoter holding has trended: 34.80% (Dec 2024) → 35.21% (Mar 2025) → 37.79% (Dec 2025) → 40.96% (April 2026) — a 5.4 ppt increase in 16 months through active warrant exercises. The conversion cadence in early 2026 alone is striking: 3.25 lakh shares allotted on 2 Mar, 6.65 lakh on 12 Mar, 8.5 lakh on 10 Apr — about 18.4 lakh shares exercised in six weeks. Niral Enterprises is the standout — its stake more than doubled from 3.43% (Sep 2025) to 7.16% (April 2026). In this fresh ₹190 cr round, ~45 lakh of the 95.39 lakh warrants — roughly 47% — go to promoter-group entities: Zoom Industrial Services (20.16 lakh), Niral Enterprises (20.16 lakh), and Rishabh Homes (5.38 lakh). Post-conversion, promoter holding could move into the 41-42% range. Promoters don't put fresh capital in at warrant prices when they don't believe in the business — and SPML's family has been doing exactly that, repeatedly, at premiums to the FY24-25 lows. The signal is hard to misread.

Beyond the promoter group, Manju Vijay Kedia — wife of well-known investor Vijay Kedia, whose Kedia Securities Pvt Ltd had already bought ~15 lakh SPML shares at ₹167 via a January 2026 bulk deal — has been allotted 13.45 lakh warrants, committing another ~₹25 cr at ₹186. She is the single largest non-promoter individual subscriber and accounts for ~13% of the fundraise. Kedias now own ~3% stake in the company.

Caveat: 25.3% of promoter holding remains pledged — a legacy issue from the FY21-22 distress period. The pledge has come down materially as the balance sheet deleveraged but isn't gone, and is worth tracking.

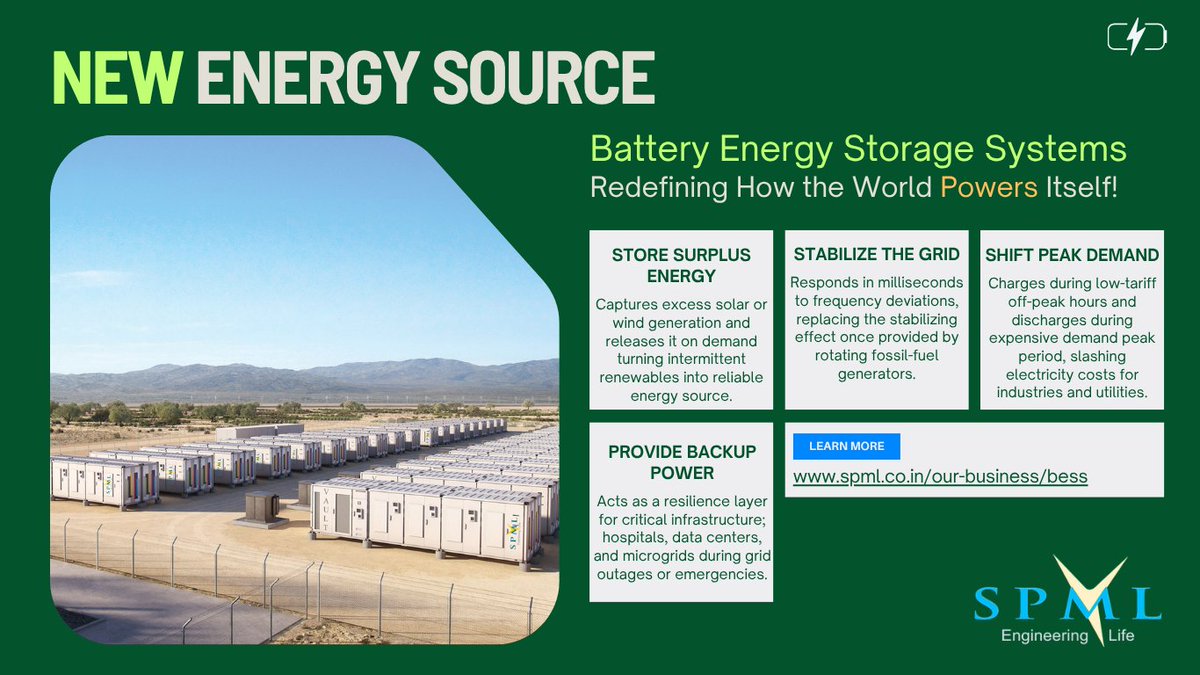

3. The BESS pivot is the next leg of growth, built on a stabilised base - With the debt sorted and profitability returning, management is deploying the new capital into battery energy storage manufacturing. The board hiked capex from ₹176.44 cr to ₹238.43 cr ( 35%) to fund 2.5 GWh → 5 GWh BESS expansion at a 99,000 sqm plot at Supa-Parner MIDC, Maharashtra — plus a 600-unit-per-year container manufacturing line. Phase 1 (2.5 GWh) is targeted for Q1 FY27, full 5 GWh by FY28. Capex being revised upward 14 months into the program signals the order book is materializing. The strategic logic: BESS integration runs 12-18% margins vs 5-8% for water EPC, working capital cycles are shorter (PSU clients like NTPC pay faster than state governments), and the container line should create recurring revenue beyond project EPC. SPML is going manufacturer integrator EPC.

4. The Energy Vault partnership is a structural support, not a marketing line - In April 2025, SPML signed an exclusive 10-year licensing and royalty agreement with Energy Vault Holdings (NYSE: NRGV) to manufacture and deploy B-VAULT BESS technology and VaultOS EMS software in India. The deal specifies 30–40 GWh cumulative volume over 10 years, with 500 MWh minimum in Year 1. Energy Vault has already deployed 1.5 GWh globally (USA, Australia, Italy, China). For SPML, this means proven grid-scale tech and software access without R&D risk. India's BESS market is projected at 236 GWh by 2031-32 (~$57 bn cumulative) — a structural tailwind that benefits the company.

5. Valuation reflects the stabilised business - The stock trades at ~ ₹219, market cap ~₹1,840 cr, EV ~₹2,150 cr. EV/EBITDA ~21x, P/E TTM ~30x, P/B ~2.1x — broadly in line with mid-cap construction peers. The trailing multiples reflect a business that's only just turned profitable; they don't yet reflect what BESS execution might deliver if Phase 1 commissions on schedule and orders continue at recent run rates. What the trailing numbers DO reflect, fairly, is that this is a real company again — earning a real ROCE of 9%, generating real cash flow. That's a meaningful change from where SPML was three years ago.

Risks worth being honest about: (a) Execution risk on BESS is non-trivial — limited prior battery-systems track record, and the Energy Vault tech localisation assumes smooth transfer; however, BESS represents a backward integration into their existing Power EPC business, providing a degree of operational familiarity and sectoral continuity; (b) Promoter pledge of 25.3% is a legacy overhang; however, the pledge is due to NARCL and will be released upon NARCL's exit; (c) Working capital days at 131 are still high — typical of the legacy water/government-receivables business; however, largely the receivables are due to arbitration awards and claims, but this creates cash flow lumpiness; (d) 5-year sales CAGR of -15% — TTM sales are still below FY24 levels, so the BESS revenue ramp has to actually deliver, not just the order book; (e) Stock has rallied 60% in 12 months (₹136 low to ₹219) — easy money is gone, the next leg requires actual capacity commissioning.

-----------

Disclosure - SPML Infra is our IR Client

Informational only. Not investment advice. Investments subject to market risk. GoIndia Advisors LLP | SEBI Registered Research Analyst Reg. No. INH000020040 | SEBI (RA) Regulations, 2014.

More research & tools → goindiastocks.com

Follow us for more insights.

2

22

4,184

@SPMLInfra wins a landmark ₹1,128 cr project to develop 1 GWh #BatteryEnergyStorage #BESS at NTPC Barauni Thermal Power Station in Bihar.

#SPMLInfra #EnergyStorage #BatteryEnergyStorageSystem #PowerSector #NTPC #Bihar #EnergyTransition #GridStability #FutureReady #BESSOrder

3

135

SPML Infra Limited retweeted

May 6

#StockInNews | SPML Infra secures contract worth ₹1,128 cr for 1 GWh Battery Energy Storage System (BESS) project from NTPC

@ntpclimited @SPMLINFRA #StockMarket

1

8

1,196

Apr 28

@SPMLInfra is advancing future of energy through Battery Energy Storage Systems (BESS), strengthening grid reliability, enabling seamless integration of renewable energy, supporting a cleaner, more resilient power ecosystem for India.

#SPMLInfra #EnergyStorage #BESS #CleanEnergy

1

188

SPML Infra Limited retweeted

Apr 27

Vijay Kedia just placed his 2026 bets. The pattern is unmistakable.

The Market Master made fresh moves across the December 2025 and March 2026 quarters, with one clear theme cutting through every trade: Infrastructure and Energy Transition.

Q4 FY26 fresh entries (March 2026 quarter):

SPML Infra: 1.88% stake, 14.98 lakh shares

Acquired through a bulk deal at Rs 167 per share. Roughly Rs 25 crore deployed. Water and power infra play with 700 completed projects.

Webel Solar Energy Systems: 1.02% stake

Smallcap solar play. Stock hit consecutive upper circuits the moment his name surfaced.

Precision Camshafts (PRECAM): 1.05% stake

Re-entry into the auto component name he previously held.

TAC Infosec: stake re-emerged at 3.64%

The cybersecurity SME he originally backed, after the stock corrected nearly 48% in Q4 FY26.

Q3 FY26 entries (December 2025 quarter):

Patel Engineering: 1.01% stake (re-entry after 5 quarters)

1 crore shares, valued around Rs 28.8 crore. Civil construction and hydro infra.

Advait Energy Transitions: 1.14% stake

Through Kedia Securities. 1.25 lakh shares, Rs 18.4 cr. Power transmission plus renewable energy with an order book exceeding Rs 1,000 crore.

Mangalam Drugs and Organics: 1.37 lakh shares at Rs 24

A bombed-out API maker down 80% from its peak. The classic Kedia turnaround bet on a 50-year-old WHO-GMP approved manufacturer.

The trim that completes the picture:

Atul Auto cut from 20.91% to 18.20%. His largest holding, partially booked.

What stands out:

Five of seven new positions sit in power, water, civil infra, or renewables

Zero financials. Zero FMCG. Zero IT services

Average ticket modest. Conviction concentrated, not sprayed

Buying happened during one of the worst small cap quarters in years (his book down up to 48%)

The MEETS-style read on Kedia's positioning:

He is treating the FY26 small cap drawdown as opportunity, not threat. The thematic pivot to Power, Water and Renewables is now explicit, not implied. SMILE is doing what SMILE does. Buying small, ambitious, scalable businesses while the screen looks ugly.

His own line on the carnage on March 26: "Loss is not real, until you sell."

Worth watching whether SPML Infra and Webel Solar can compound the way Atul Auto did over the last decade.

Disclaimer: For educational purposes only. Not investment advice. Securities markets are subject to market risk.

4

33

162

25,750

Apr 27

Battery Energy Storage Systems transforming energy landscape, enhancing reliability, enabling renewable integration & powering a cleaner, more resilient future.

#EnergyStorage #BESS #BatteryEnergyStorage #CleanEnergy #RenewableEnergy #Sustainability #EnergyTransition #SPMLInfra

1

71

Apr 22

#EarthDay is reminder to cherish and protect our only home. @SPMLInfra committed to advancing energy storage technologies that reduce environmental footprint. Together, we can build a greener, healthier, & sustainable planet for generations.

#Sustainability #GreenEnergy #BESS

1

63

Apr 19

May this day bring prosperity, positivity, and new beginnings into your life. @SPMLInfra we renew our commitment towards building a sustainable future with clean water, green energy and responsible use of resources.

#AkshayaTritiya #Prosperity #CleanWater #GreenFuture

71

Apr 16

Driving India’s energy transition, @SPMLInfra is delivering Battery Energy Storage Systems (BESS) to build secure & sustainable energy future for India

#SPMLInfra #EnergyStorage #BESS #CleanEnergy #SustainableIndia #EnergyTransition #RenewableEnergy #PoweringIndia #GreenFuture

1

147