Not Financial Advice. This account is for entertainment purposes only.

Joined September 2018

- Tweets 905

- Following 825

- Followers 94

- Likes 1,728

92 Photos and videos

Hyperliquid, meet Ripple Prime: on.ripple.com/4ke7TzL

We’re now enabling institutions to access onchain derivatives liquidity through @HyperliquidX in a streamlined and secure way. Customers can also efficiently cross-margin crypto with all asset classes supported by our prime brokerage platform.

Institutions, welcome to the onchain economy.

469

1,594

6,129

1,076,415

Big News: @AMINABankGlobal is the first European bank to go live with Ripple Payments: on.ripple.com/4pGovSI

This partnership provides a crucial, compliant bridge between traditional fiat and blockchain rails, solving a major friction point for crypto-native clients who need efficient cross-border transactions.

This is the next step in our expanding relationship with AMINA Bank, building on their earlier adoption of RLUSD.

Our commitment to delivering secure, compliant, and resilient digital asset technology continues to advance the wider adoption of crypto in Europe and beyond!

302

1,686

6,437

760,618

G retweeted

12 Dec 2025

HUGE news! @Ripple just received conditional approval from the @USOCC to charter Ripple National Trust Bank. This is a massive step forward - first for $RLUSD, setting the highest standard for stablecoin compliance with both federal (OCC) & state (NYDFS) oversight.

To the banking lobbyists – your anti-competitive tactics are transparent. You’ve complained that crypto isn’t playing by the same rules, but here’s the crypto industry – directly under the OCC's supervision and standards – prioritizing compliance, trust and innovation to the benefit of consumers. What are you so afraid of?

2,367

7,874

27,686

3,363,397

Banking, bonds, currency and markets: the entire financial landscape is evolving.

Blockchain is a powerful engine that creates groundbreaking opportunities for global businesses.

Learn how we're making it happen with solutions for payments, custody, stablecoins, and more: on.ripple.com/4h1y0In

392

2,628

8,989

904,235

G retweeted

27 Jan 2024

DID YOU KNOW?

UK does not have finance, the City of London does, but it's not part of the UK.

16

58

223

14,778

The Republic of Palau is partnering with Ripple to pilot a USD-backed Stablecoin on the #XRPLedger.

Learn about the benefits for citizens and merchants and how the Ripple #CBDC Platform will be implemented in this next phase of the Palau #Stablecoin pilot.

131

941

3,037

376,055

“As more countries develop regulatory frameworks for crypto, many are looking to Singapore’s early leadership in developing a clear taxonomy and licensing framework," says Ripple's @s_alderoty.🇸🇬

Learn more about Ripple's deepening roots in Asia. bit.ly/3qcHU46

67

545

2,035

198,670

If your company seeks simpler, optimized treasury operations, our payments solution is key 🔑 to achieving superior liquidity and faster, more affordable settlements.

Check out our guide to start streamlining corporate treasury flows. bit.ly/3KkTvoy

66

664

2,405

320,597

🚨WHY #XRP IS NEEDED MORE THAN EVER ?🚨 THE BEST THREAD WILL SEE ON TWITTER THIS WEEKEND! RETWEET, COMMENT AND LIKE ❤️

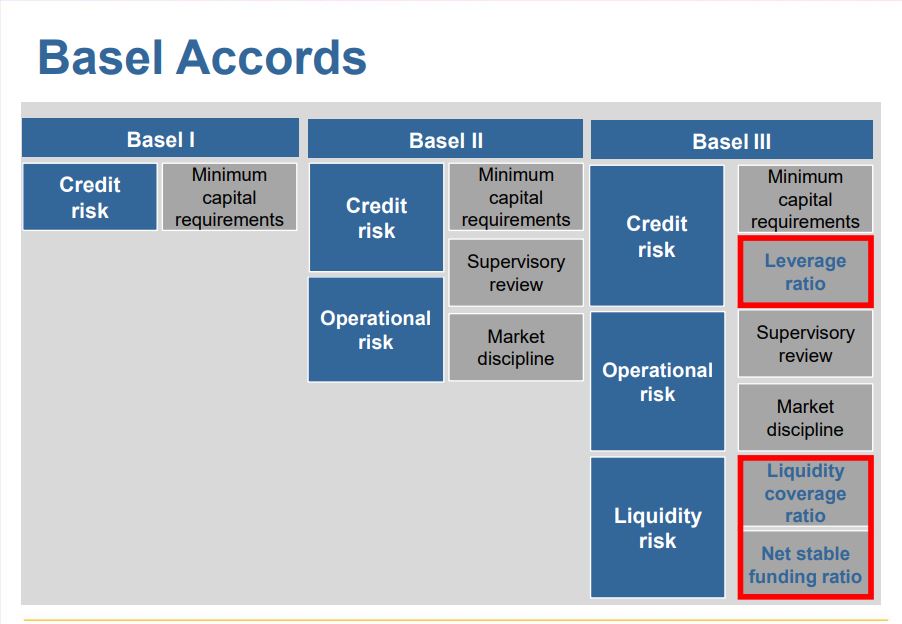

January 25, 2023 - EU Parliament passes Basel III rules, including crypto assets clause ledgerinsights.com/eu-basel-…

The European Parliament’s Economics and Monetary Affairs Committee approved a draft law to implement the Basel III rules on banking capital and liquidity requirements. Included in the draft legislation is a single clause relating to crypto assets

#BASEL III - Rules on banking capital and liquidity requirements for banks in the world. The #Basel III reform is one of the initiatives taken by the Financial Stability Board and the G20, in the wake of the 2007 financial crisis, to strengthen the financial system, guarantee a minimum level of capital and reinforce the financial solidity of banks.

The severity of the crisis was largely due to excessive growth in banks' balance sheets and off-balance sheet items, while at the same time the level and quality of capital to cover risks deteriorated. What's more, many institutions also lacked sufficient reserves to cope with a liquidity crisis. Against this backdrop, the banking system proved incapable of absorbing the losses incurred first on structured securitization products, and then of re-intermediating part of its off-balance sheet exposures. At the height of the crisis, uncertainties over the quality of balance sheets, the solvency of banks and the risks associated with their interdependence (the default of one institution could lead to that of another) triggered a widespread crisis of mistrust and liquidity.

July 21, 2023 - U.S. Federal Reserve confirms July 27 meeting on #Basel III endgame capital proposals for banks marketwatch.com/story/u-s-fe…

#Basel III endgame proposal goes to full vote by the Federal Reserve Board as regulators look to strengthen the financial system. The Federal Reserve Board has scheduled a July 27 open meeting to air proposed rules to implement the #Basel III endgame agreement for large banks, as well as capital surcharges for the largest and most complex banks.

Who is the vice president of the Federal Reserve - Michael Barr (Former employee at #Ripple) and he spoked yesterday at the open board meeting about #BASELL III

youtube.com/watch?v=oWx2QIdO…

December 2010 - #Basel III: International framework for liquidity risk measurement, standards and monitoring bis.org/publ/bcbs188.pdf

During the early “liquidity phase” of the financial crisis that began in 2007, many banks – despite adequate capital levels – still experienced difficulties because they did not manage their liquidity in a prudent manner. The crisis again drove home the importance of liquidity to the proper functioning of financial markets and the banking sector. Prior to the crisis, asset markets were buoyant and funding was readily available at low cost. The rapid reversal in market conditions illustrated how quickly liquidity can evaporate and that illiquidity can last for an extended period of time. The banking system came under severe stress, which necessitated central bank action to support both the functioning of money markets and, in some cases, individual institutions.

January 2, 2018 - THE FUTURE OF CROSS-BOARDER PAYMENTS A LOOK INTO RIPPLE’S DISTRIBUTED LEDGER TECHNOLOGY run.unl.pt/bitstream/10362/3…

According to the ECB (2015) payments systems is the prevailing method for settling in-country transactions involving different financial institutions due to their superior form of transmission, processing and settling. This approach is preferred to correspondent bank arrangements, because it solves the liquidity problem and reduce the exchange rate and counterparty risk. In order to be in place correspondent bank arrangements require that a considerable amount of money is held in NOSTRO VOSTRO ACCOUNTS. This method is operationally inefficient as the money could be used in revenue generating activities, also banks must accounts for the restrictions arising from liquidity requirements under Basel III and the risk of counterparty default. Furthermore, this method exposes the bank to FX risk in volatile currency situations as in countries with unpredictable inflation and political stability. Moreover, costs to the payer and/or payee include charges from several parties, such as FX rate spread and SWIFT fees. Ultimately, as a result of predominantly non-aligned development, there is a shortfall of 9 standardization and automation in inter-bank networks which concurs in making settlement time vary from three to five working days.

March 13, 2020 - Ms. Carolyn Rogers Secretary General #Basel Committee on Banking Supervision Bank for International Settlements CH-4002 #Basel Switzerland ripple.com/files/ripplelabs_…

#Ripple welcomes the opportunity to comment on the Basel Committee on Banking Supervision (BCBS) discussion paper “Designing a prudential treatment for crypto-assets.”

As BCBS recognizes, different types of crypto-assets can serve different functions in the banking system. #Ripple’s use of #XRP in conjunction with its software products allows financial institutions to settle cross-border transactions globally, on a real-time basis, at a fraction of the cost of traditional services available to market participants. Historically, remittance providers enable payments by PRE-FUNDING (NOSTRO VOSTRO) correspondent accounts. This not only traps enormous amounts of capital, but also creates foreign exchange and foreign counterparty risks that often must be hedged. The trapped capital also creates compliance costs and large lost opportunity costs. This process limits the reach of efficient payment solutions to high-volume currency pairs and is a major driver of the high fees being charged to customers sending smaller amounts to friends and families overseas. Payments between less frequently-traded currencies can be even more expensive and cumbersome. Crypto-assets specifically designed for payments -- like #XRP -- have the potential to reduce these limitations by enabling payments without the need to pre-fund overseas. #Ripple’s software leverages #XRP as a bridge between currencies. This allows financial institutions to access liquidity on demand through digital asset exchanges without having to pre-fund accounts in the destination country. The payer and payee continue to use fiat currency for their payment, with #XRP used as a bridge between the regulated financial institutions that are facilitating the remittance transaction. This is particularly useful for smaller institutions with limited capital; using Ripple products, they can achieve broad global payment reach without additional capital needs. #Ripple’s aim is not to replace fiat currencies, but rather enable a faster, less expensive, and more transparent method of making payments that is in the public’s best interest. Ripple’s solution can also serve as bridge between crypto and crypto and crypto and fiat. For example, a Central Bank Digital Coin can be bridged to another store of value using #Ripple’s products.

#XRP: this solution avoids the need for banks and other financial institutions to open and fund a NOSTRO VOSTRO ACCOUNTS in a foreign country, Thanks to #XRP, which operates on the #XRPLedger and therefore uses #XRP, the liquidity costs associated with opening and managing the corresponding account(s) required for these international transactions are avoided. In other words, Bank A in the USA, wishing to transfer $10 million to Bank B in France, will send the equivalent amount in XRP. The transaction takes less than 3 seconds and costs less than $0.004. All the French bank has to do is convert this sum into the desired currency, or keep its #XRP for future transfers.

CONCLUSION

The world is preparing to implement #BASEL III, which requires global banks to hold more capital, more liquidity and more reserves.

How are banks going to do this if they pay a lot of fees for cross-border payments? How are banks going to do this if they have a lot of capital locked up in NOSTRO VOSTRO accounts?

The only solution for BASEL III to be respected is for the banks to use #Ripple = #XRP technology to eliminate pre-funding and save money on every cross-border payment. By doing so, they'll be able to take back the money that's been blocked all this time and use it to their advantage.

27,000 Trillions currently held in NOSTRO/VOSTRO accounts

#XRP has the potential to reduce the overall cost of cross-border payments for banks by up to 90%, reaching a target cost of $1-2 per transaction or a total cost reduction for banks of up to $140 billion, or nearly 50% of current cross-border payments revenues.

That's why #XRP was created that's why #Ripple has access to the world's banking system because #Ripple is there to provide a new infrastructure that will allow them to follow the laws.

Without #XRP there's nothing! and the timing is perfect! we had the summary judgment while they are talking about BASEL III. #XRP is not a security so the banks are going to use #XRP to comply with BASEL III.

@JoelKatz once said, instead of prefunding in every market, customers can prefund in just one account and make payments to any On-Demand Liquidity (ODL) destination market.

One Love ❤️

@Fame21Moore @digitalassetbuy @IOV_OWL @Leerzeit @MrFreshTime @sentosumosaba

35

302

762

120,973

G retweeted

27 Jul 2023

The Republic of Palau Partners with Ripple to Pilot a US Dollar-Backed Stablecoin on the XRP Ledger ripple.com/insights/the-repu…

23

237

966

87,814

The future of money is digital.

Learn why customers trust our groundbreaking technology for minting, managing, and transacting #CBDCs and stablecoins. bit.ly/3XZFjqw

272

2,464

6,831

893,607

After nearly 3 years, the Court’s July 13 decision delivered a landmark win for Ripple and the entire U.S. crypto industry: XRP is not a security.

Progress is worth fighting for.

ripple.com/insights/xrp-is-n…

287

2,570

8,335

1,302,054

G retweeted

15 Jul 2023

Hoping yesterday’s decision is the wake-up call that Congress needs. This ruling directly undercuts the SEC’s claims that nearly all tokens are inherently securities – likely to set a positive precedent for other digital tokens in the US.

14 Jul 2023

Ripple Labs CEO Brad Garlinghouse says that a federal court's decision means that its crypto token XRP “is not a security,” giving the digital-payments company more freedom to pursue various business opportunities trib.al/SjiawoB

279

1,956

7,784

739,060

XRP is not a security.

This victory for @Ripple is a win for the entire industry and a step toward regulatory clarity in the U.S.

A huge thank you to @bgarlinghouse, @chrislarsensf, and @s_alderoty for their leadership and the #XRPCommunity for their continued support.

11,851

12,422

33,217

3,402,960

G retweeted

13 Jul 2023

#XRPCommunity #SECGov v. #Ripple #XRP BREAKING: Judge Torres has issued her Ruling on the Parties Motions for Summary Judgment.

dropbox.com/scl/fi/bk1n1qn1t…

319

2,058

5,997

1,705,809

G retweeted

13 Jul 2023

Seeing some confusion on what the Court's decision means -- here's a recap from our legal eagle @s_alderoty

13 Jul 2023

A huge win today – as a matter of law - XRP is not a security. Also a matter of law - sales on exchanges are not securities. Sales by executives are not securities. Other XRP distributions – to developers, to charities, to employees are not securities.

352

2,539

9,247

647,315

G retweeted

13 Jul 2023

The most important part of this ruling:

“XRP, as a digital token, is not in and of itself a “contract, transaction[,] or scheme” that embodies the Howey requirements of an investment contract.”

This is a now a matter of law (not up for trial.)

1,383

8,535

28,678

3,649,739

G retweeted

16 Jun 2023

Trying something new – some thoughts from me on the events (specifically the release of the Hinman documents) of this week. For me, this has all had a personal bent to it - and felt like it warranted some personal comments.

2,240

8,168

22,290

4,231,314