Crypto Enthusiast | Full-Time Yapper | Talking tokens, testing protocols, and yapping about the next big thing.

Joined June 2025

- Tweets 4,224

- Following 731

- Followers 713

- Likes 4,745

281 Photos and videos

Pinned Tweet

6 Aug 2025

Deep dive on @JoinSapien

On Sapien, something pretty remarkable is unfolding: people from every corner of the globe are connecting and building together in Web3, each bringing their passions and talents. Scroll through Sapien’s community channels and it’s easy to spot developers bouncing ideas off artists, teachers collaborating with data scientists, and everyday users sharing the rewards of open, decentralized social networks.

Take, for example, a strategy analyst in Paris who joined Sapien for the transparency and soon found himself leading an international guild, uniting contributors for a community-driven AI project. Or a group of university students in India, who discovered they could build their skills in AI while earning real rewards simply by labelling datasets, something that’s helping power autonomous vehicles and next-gen medical tools. Across Sapien, creators are launching projects, artists are showcasing their work, and casual users are levelling up through games, quests, and community events.

Everyone on Sapien benefits from the platform’s unique structure: it gives regular people a real voice (and stake) through features like DAOs, quests, and transparent reward systems. That makes it more than social media, it’s an ownership economy where your effort and ideas drive both personal growth and platform evolution.

As Sapien keeps rolling out tools for avatars, cross-platform assets, and more ways to contribute, the vibe is clear: this is what happens when a community truly owns its digital future. For anyone curious about how real people are thriving in Web3, Sapien’s story is just getting started, and it’s being written by everyone involved.

94

20

124

3,777

Real CryptoSam retweeted

Apr 24

🎉 Turing Wallet Official Website Officially Launched

turingwallet.xyz/

Download & explore the turingbitchain Ecosystem today!

79

46

56

15,586

Real CryptoSam retweeted

Apr 13

💸 Why Cross-Border Payments Are Still Broken in a 24/7 Financial World

In 2026, major exchanges can talk about 24/7 trading, yet ordinary cross-border payments still feel stuck in another century.

Consider a simple business payment:

A merchant in Hangzhou China wires $50,000 to a U.S. supplier.

The funds arrive three days later.

The recipient gets only $49,780.

Where did the missing $220 go?

Into the familiar black box of traditional cross-border finance:

intermediary bank fees,

telecom charges,

FX spread losses,

and a long list of hidden deductions that users rarely see in real time.

That is the core problem. Cross-border payments are not just slow. They are structurally opaque.

1️⃣ SWIFT Solved Communication, Not Settlement

For decades, SWIFT has been the backbone of international banking coordination.

But SWIFT is primarily a messaging network, not a true value-transfer network.

It tells banks what to do.

It does not eliminate the need for correspondent banks, nostro/vostro accounts, or layered clearing relationships.

So when one bank sends funds to another market, the payment often moves through multiple institutions before it actually settles.

Every extra hop creates three problems:

more fees

more delays

more uncertainty

The result is a system where money can move globally, but only through a chain of toll booths.

2️⃣ Intermediaries Turn Payments into Friction

Traditional cross-border remittance still depends on a relay model.

One bank passes instructions to another.

A correspondent bank processes the liquidity.

Another institution handles local settlement.

Only then does the recipient finally get paid.

This structure may have worked in a pre-digital era.

But in a world that expects real-time commerce, it creates constant operational drag.

For businesses, this means:

delayed supplier payments

unpredictable cash flow timing

reconciliation headaches

reduced trust in the payment process itself

For individuals, it is even worse.

A remittance is often not a financial product. It is rent, tuition, payroll, or family support.

And every percentage point lost matters.

3️⃣ The Hidden Cost Is Not Just the Fee

The most deceptive part of legacy remittance is that the visible fee is often only a fraction of the true cost.

The larger damage often comes from exchange-rate spread.

Users are quoted a rate that looks acceptable on the surface, but sits meaningfully below fair market pricing.

So even when the payment “works,” value is quietly extracted in the background.

That is why the real crisis in cross-border payments is not just inefficiency.

It is asymmetry:

the institutions know where the money is,

while the user waits in the dark.

🌍 The Bigger Point

The old system was built for institutional coordination, not for seamless global value transfer.

And that is exactly why it now feels outdated.

Cross-border commerce today needs something the legacy stack was never designed to offer:

instant settlement,

cost transparency,

and finality without layers of intermediaries.

The question is no longer whether the traditional model is inefficient.

The question is what comes next.

8

18

1,545

Real CryptoSam retweeted

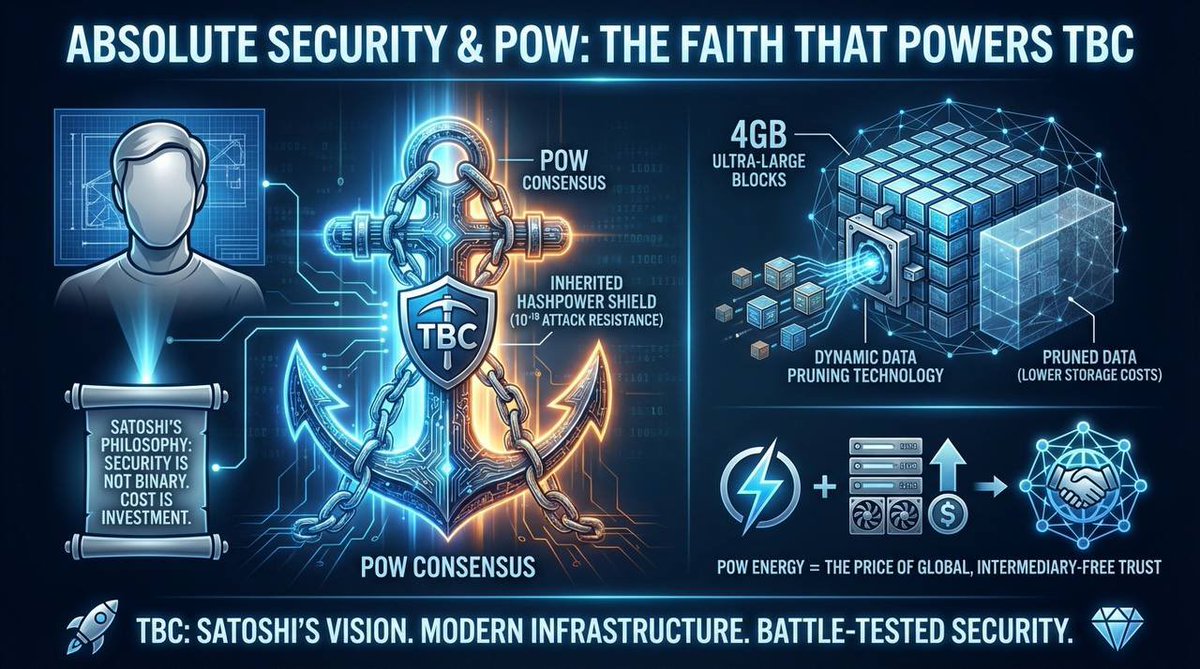

⛏️ Absolute Security & PoW: The Faith That Powers TBC

Satoshi Nakamoto didn't just build a payment system.

He built a philosophy. And TBC is its most faithful evolution. 🧵👇

📜 The Words That Started It All

Satoshi himself drew the boundary on security expectations:

"The system is designed to protect user privacy, but not absolutely. Every transaction is broadcast on the network."

And on the cost of running it:

"The utility of the exchanges made possible by Bitcoin will far exceed the cost of electricity used. Therefore, not having Bitcoin would be the net waste."

These two statements reveal something profound: Satoshi understood that security is not binary, and that cost is not waste—it is investment.

🧠 The "Security-Utility" Balance: Satoshi's Core Insight

Privacy is a relative goal, not an absolute one.

Transparency and PoW consensus costs serve a higher purpose: trustless, intermediary-free transactions.

This is the philosophical foundation TBC builds upon.

Not "maximum privacy at all costs."

Not "zero fees at the expense of security."

But a carefully engineered balance between openness, security, and utility.

🔐 How TBC Translates Philosophy Into Architecture

TBC inherits Bitcoin's PoW consensus mechanism and goes further:

1️⃣ Inherited Hashpower Shield ⚔️

- Shared access to Bitcoin's network of 1.3 million mining machines

- 16,000 full nodes forming a globally distributed verification network

- Long-range attack success rate reduced to 10⁻¹⁸ — effectively zero

2️⃣ Dynamic Data Pruning Technology 🏗️

- Optimized for 4GB ultra-large blocks

- Dramatically lowers storage costs for light nodes

- Maintains full transaction broadcast transparency

- Avoids the regulatory risks of "absolute anonymity"

Security without sacrificing openness.

Scalability without sacrificing decentralization.

⚡ PoW Is Not Waste — It Is the Price of Trust

Critics call PoW energy consumption wasteful.

Satoshi called it necessary.

TBC agrees.

Every kilowatt hour consumed by the PoW network is not an environmental mistake — it is the security premium paid to enable the greatest financial experiment in human history:

Peer-to-peer electronic cash, with no banks, no intermediaries, no single point of failure.

As Satoshi said: "Not having Bitcoin would be the net waste."

The energy isn't the cost of running TBC.

It is the cost of replacing an entire global financial system. 💎

🌐 The Legacy Continues

TBC proves that Satoshi's original vision was not a limitation to overcome — it was a foundation to build upon.

✅ PoW consensus: Battle-tested security since 2009

✅ 10⁻¹⁸ attack resistance: Mathematically unbreakable

✅ Transparent broadcast dynamic pruning: Compliant, scalable, open

✅ No intermediaries: The core value, preserved

The faith in PoW is not nostalgia.

It is the most rational choice for those who take security seriously.

TBC: Where Satoshi's philosophy meets modern infrastructure. 🚀

24

16

29

956

Real CryptoSam retweeted

🏗 Protocols Need Rails: Why UTXO Settlement (and TBC) Matters

x402 defines a powerful payment handshake at the HTTP layer.

But for agent economies to scale, the protocol still needs an underlying settlement substrate that can handle:

- tiny payments (micropayment economics)

- massive frequency (agents don’t transact “sometimes”)

- immediate settlement (no billing cycles)

- programmable conditions (pay only when outcomes are verified)

⚡️ Building Block 2: UTXO Settlement for Machine Throughput

The fundamental mismatch:

Agents generate huge volumes of tiny, frequent transactions. If fees are high or throughput is limited, micropayments become uneconomical.

Why UTXO fits machine payments:

UTXO-style settlement naturally supports:

- parallel validation

- clear ownership and deterministic spend rules

- discrete, atomic transfers that compose cleanly

This is well-aligned with machine-to-machine value transfer where each interaction can be a verifiable output.

⚡️ Building Block 3: Programmable Execution for Autonomous Settlement

Agents don’t just “pay.” They pay based on conditions:

- compute delivered

- data returned

- task completed

- SLA verified

- event triggered

Programmable execution lets payments be coupled to outcomes, enabling atomic “work → verify → pay” flows.

🧱 Where TBC Fits

TBC positions itself as a UTXO-based, high-performance settlement layer with smart-contract capability designed for scalability and low-cost execution—properties that are valuable for always-on agent payments.

🎯 The Combined Stack

1️⃣ Trigger Layer (x402): web-native payment negotiation

2️⃣ Settlement Layer (UTXO / TBC): low-cost, scalable micropayment execution

3️⃣ Execution Layer (Programmability): conditional, outcome-based settlement

When the web can move value as smoothly as it moves information, the machine economy stops being theory—and becomes default.

32

27

42

2,404

Real CryptoSam retweeted

Jan 29

🏗 AI Agents Are Ready. Payments Aren’t.

As AI agents evolve from “assistants” into independent economic actors, the digital economy is shifting fast 🚀

Agents can already:

- retrieve data instantly

- orchestrate tools and APIs

- allocate cloud compute on demand

- execute complex workflows end-to-end

But one bottleneck keeps breaking automation:

Payments. 💳⚠️

Traditional financial rails assume humans—manual onboarding, subscriptions, invoicing, and delayed settlement. That model collapses when software needs:

✅ real-time settlement

✅ high-frequency interactions

✅ micropayments with minimal friction

⚡️ Building Block 1 : x402 — HTTP-Native Payments

The legacy constraint:

Most web services monetize through subscriptions, API keys, quotas, and billing cycles.

That’s slow, rigid, and poorly suited for autonomous agents that want to pay *per action*.

The x402 innovation:

x402 revives HTTP 402 (Payment Required) as a programmable payment handshake.

A typical flow becomes:

1) Client requests a paid resource

2) Server responds with 402 Payment Required payment requirements

3) Client automatically submits a signed payment payload and retries

4) Server verifies and returns the resource

Why this matters:

✅ Payments become part of the request/response flow

✅ Access becomes conditional on payment, not accounts

✅ Enables agentic commerce: pay-per-call, pay-per-result, pay-per-event

This turns “payment” into a native web primitive—exactly what machine-to-machine commerce needs.

60

34

57

4,560

Jan 27

Ethereum isn’t just a chain. It’s the backbone of Web3.

While Bitcoin dominates as a store of value, Ethereum dominates in utility and activity. Every NFT, DeFi protocol, and Layer‑2 solution relies on it.

Why ETH trends on X:

• Layer‑2 expansion: Optimism, Arbitrum, Base, and more

• DeFi growth: lending, borrowing, and trading keep activity high

• NFT and gaming ecosystems: Ethereum remains the hub for collectibles

• Protocol upgrades: continuous EIPs and network improvements

• Developer adoption: tools, smart contracts, and community support

Ethereum is where innovation moves fastest.

BTC may be gold, but ETH is fertile ground for new ideas.

2

48

Jan 27

Bitcoin isn’t flashy. It doesn’t need to be.

It’s still the reference point for crypto, the store of value, the hedge, the baseline for market sentiment.

Why it keeps trending on X:

• ETF and institutional activity shaping flows

• Macro signals like inflation and interest rates

• Network health: hash rate and transaction volume

• Adoption growth: retail wallets, corporate treasuries

• Scarcity narrative: halvings remind everyone supply is capped

Bitcoin may not innovate as fast as Layer‑1s or L2s, but its trust, history, and liquidity keep it central.

1

36

Jan 26

Aptos focuses on one thing most chains still struggle with: consistency.

Not just speed on paper.

Speed under real usage.

Built with the Move language and parallel execution at its core, Aptos is designed to avoid congestion before it happens.

Why that matters:

• Parallel processing instead of sequential bottlenecks

• Move-based contracts reduce unexpected failures

• Designed for high throughput and low latency

• Stable performance for consumer-facing apps

• Strong emphasis on developer experience

Aptos isn’t chasing narratives.

It’s building infrastructure meant to hold up when demand actually shows up.

That kind of reliability is easy to overlook, until you need it.

1

26

Jan 26

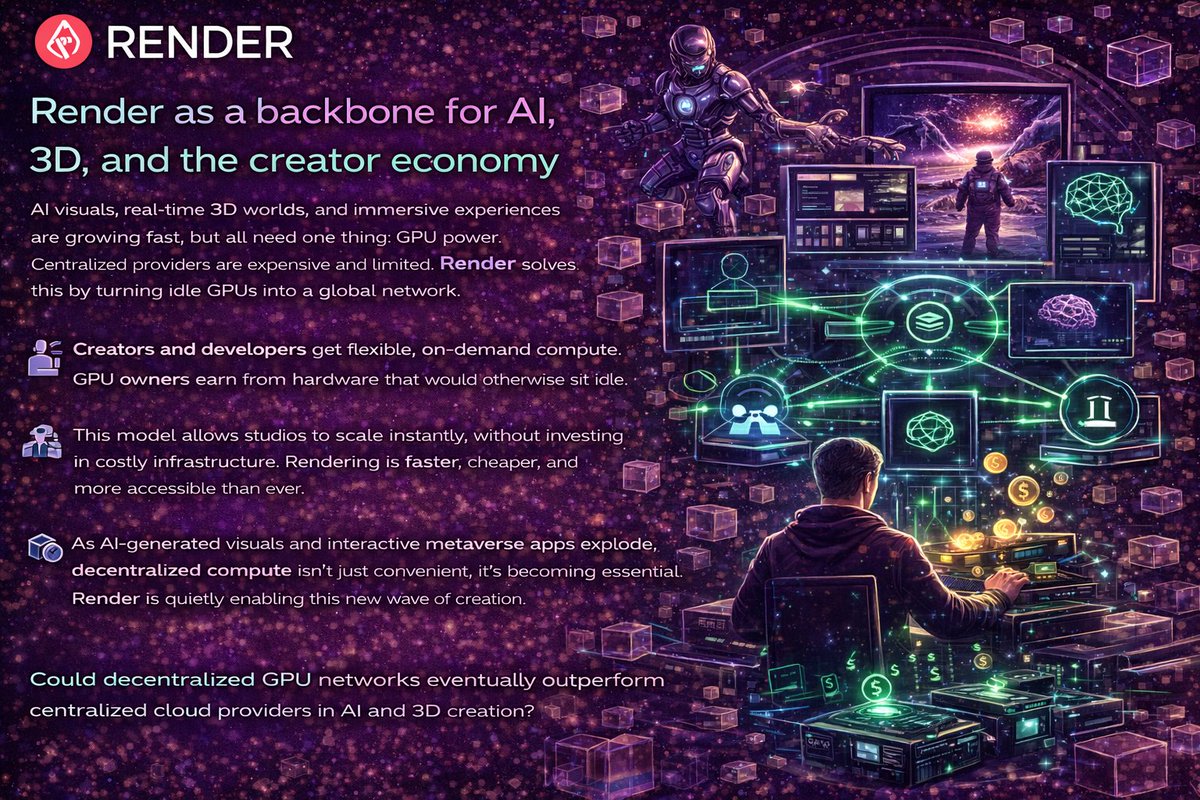

Render is solving a problem most people don’t see yet: compute scarcity.

AI, 3D design, and digital media are all competing for GPU power.

Centralized supply can’t keep up.

Render flips the model by turning idle GPUs into a decentralized compute network.

Why that matters:

• Access to on-demand GPU power without centralized gatekeepers

• Incentives for GPU owners to monetize unused hardware

• Built for rendering, AI, and graphics-heavy workloads

• More flexible and cost-efficient than traditional providers

• Increasing relevance as AI adoption scales globally

Render isn’t about speculation.

It’s about infrastructure for a compute-hungry future.

And that kind of infrastructure tends to age well.

1

38

Real CryptoSam retweeted

6

6

7

225

Jan 23

Injective treats DeFi like a real financial system.

Not an experiment!

Not a workaround!!

Built from the ground up for trading, Injective prioritizes speed, precision, and composability.

Why it keeps attracting serious builders:

• Ultra-fast finality, suited for active markets

• Native orderbook infrastructure on-chain

• Designed for perps, futures, and advanced DeFi

• Cross-chain by default, not bolted on later

• Fully decentralized execution, no custodial layers

Injective sits at the intersection of traditional market structure and on-chain transparency.

As DeFi evolves past simple swaps, chains like Injective become less optional and more necessary.

Image Prompt:

“Futuristic on-chain trading environment powered by Injective, live order books and financial data flowing on blockchain rails, dark professional aesthetic with subtle neon highlights”

1

33

Jan 23

Base is built for usage, not narratives.

While many L2s compete on benchmarks, Base focuses on something simpler: getting people on-chain.

Backed by Coinbase and built on the OP Stack, Base removes friction between users and Ethereum.

What makes Base stand out:

• Direct pipeline to millions of Coinbase users

• Cheap, fast transactions for high-frequency activity

• Full Ethereum security alignment

• Optimized for consumer and social apps

• Part of the wider Superchain vision

Base doesn’t try to replace Ethereum.

It extends it.

If mass adoption happens quietly, it will probably happen somewhere like Base.

30

Jan 22

Why Celestia Is Becoming the Backbone of Modular Blockchains

Most blockchains still try to do everything at once.

Execution, consensus, data, settlement all packed into one chain.

Celestia takes a completely different path, and that’s why builders are paying attention.

At its core, Celestia is not trying to be “another L1.”

It is designed to be the data availability layer for an entire modular ecosystem.

Here’s what makes that powerful:

• Separation of concerns: Celestia handles data availability and consensus only. Execution is left to rollups and app-chains.

• Modular freedom: Developers choose their own execution environments without being locked into a single VM.

• Horizontal scaling: New chains scale independently instead of fighting for shared blockspace.

• Lower launch costs: Teams can deploy sovereign rollups without building security from scratch.

• Faster iteration: Execution layers can upgrade freely without risking the base layer.

The result is a network where innovation moves faster because infrastructure is no longer the bottleneck.

Celestia doesn’t compete with rollups, it empowers them.

It doesn’t replace blockchains, it unbundles them.

That shift from monolithic to modular could define the next phase of Web3.

Do you think modular blockchains will outperform traditional all-in-one chains long term, or will monolithic designs still dominate?

1

2

24

Jan 20

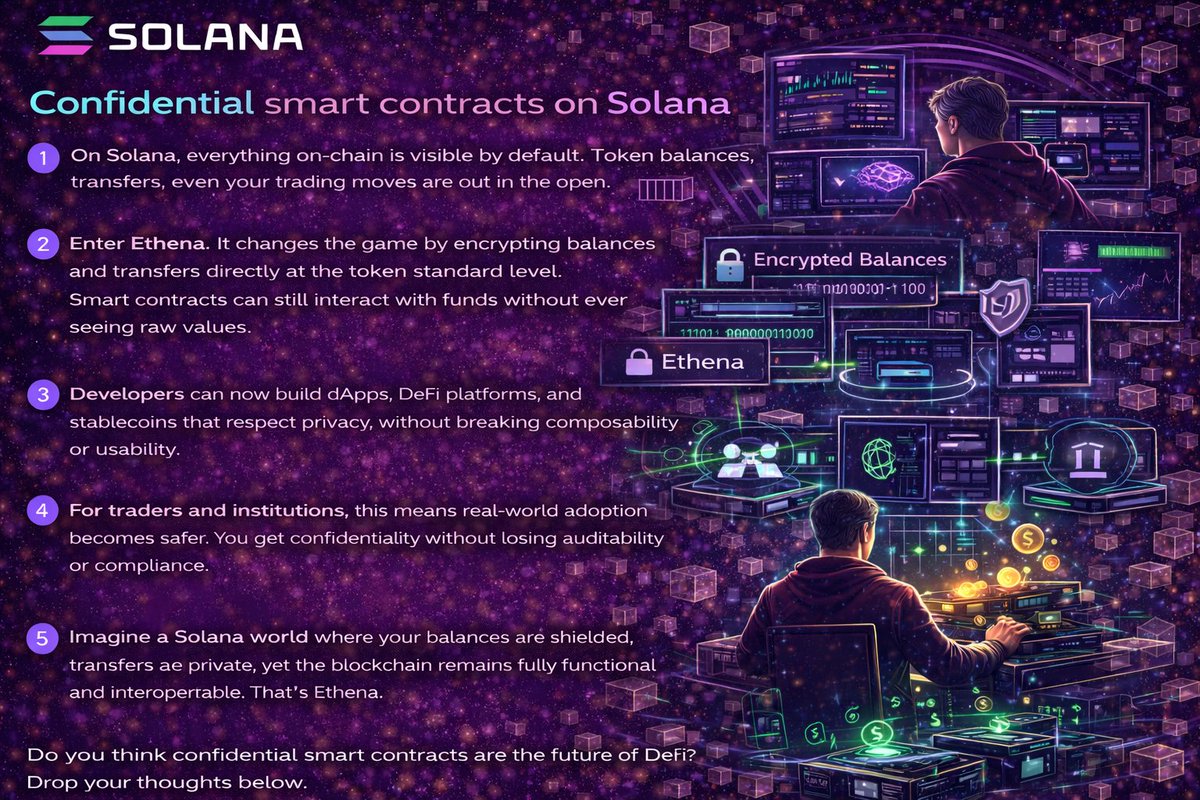

Ethena’s Layered Approach to Privacy and Scalability

Ethena is redefining privacy in DeFi while keeping apps fast and scalable.

Why this matters:

• Encrypted Balances: Transaction amounts remain private, fully secured on-chain.

• Composable Protocols: Developers can build dApps without revealing sensitive data.

• Layered Design: Privacy and scaling are separated, ensuring performance isn’t compromised.

• Seamless UX: Users interact with wallets and apps without complex setups.

• Multi-Chain Potential: Ethena can integrate across chains for wide-ranging private DeFi.

• Compliance Friendly: Auditability and regulation-ready features make it appealing to institutions.

💡 With Ethena, private DeFi isn’t just a concept. Trading, lending, and swapping can happen securely without losing speed or interoperability.

1

3

59

Jan 20

Why Object-Based Blockchains Change How Apps Scale

Sui isn’t just another blockchain, it’s an object-based network designed to rethink how digital assets and apps operate at scale.

Key points to know:

• Objects, Not Accounts: Every asset is an independent object, giving apps clarity in ownership and control.

• Parallel Processing: Multiple transactions can happen at the same time, reducing bottlenecks.

• Instant Settlements: Payments, NFT transfers, and game interactions happen almost instantly.

• Mobile-Optimized: Lightweight objects mean seamless experiences on smartphones and tablets.

• Scalable Architecture: Apps scale horizontally without getting stuck behind sequential queues.

• Developer-Focused: Sui Move empowers developers to design precise, secure asset behaviors.

The outcome? A blockchain ecosystem where high-speed DeFi, NFTs, and gaming are not just possible, they feel natural.

💡 Think of a world where your NFT marketplace updates live without delays, your DeFi trades settle instantly, and mobile blockchain apps feel as smooth as any regular app. Sui makes it happen.

1

36

Jan 19

Hedera: Why Enterprises Quietly Keep Building Here

Hedera doesn’t compete for attention.

It competes on execution.

While most networks optimize for experimentation, Hedera was designed from day one to handle real users, real businesses, and real economic volume.

What makes it different becomes clear when you look under the hood:

• Hashgraph consensus, not a traditional blockchain, enabling faster and fairer ordering

• Near-instant finality, transactions settle in seconds, not minutes

• Consistently low fees, predictable costs even during high demand

• Asynchronous Byzantine Fault Tolerance, enterprise-grade security

• Governing council of global organizations, adding accountability and long-term stability

• Built-in services for tokens, smart contracts, and decentralized storage

Hedera is less about hype cycles and more about reliability at scale.

That’s why it keeps attracting institutions, developers, and public-sector use cases that can’t afford uncertainty.

In a market full of experiments, Hedera positions itself as infrastructure you can actually build on for the next decade.

28

22

92

Jan 17

Where Crypto Meets Real Users

Most Layer-2s compete on tech.

Base competes on distribution.

Built on Ethereum using the OP Stack, Base is Coinbase’s move to push crypto beyond power users and into everyday apps.

Why Base stands out:

• Millions of users one step away; native access to Coinbase’s ecosystem

• Ethereum-aligned; inherits Ethereum’s security and settlement

• Low fees, fast UX; built for frequent, real-world transactions

• App-driven growth; social, DeFi, NFTs, and consumer apps thrive here

• Cultural momentum; Base isn’t just infra, it’s becoming a community

Base isn’t loud.

It’s strategic.

If mass adoption happens through simple apps, seamless onboarding, and familiar platforms, Base is already positioned where users are.

Ethereum is the foundation.

Base is the experience layer.

28

28

94

Jan 17

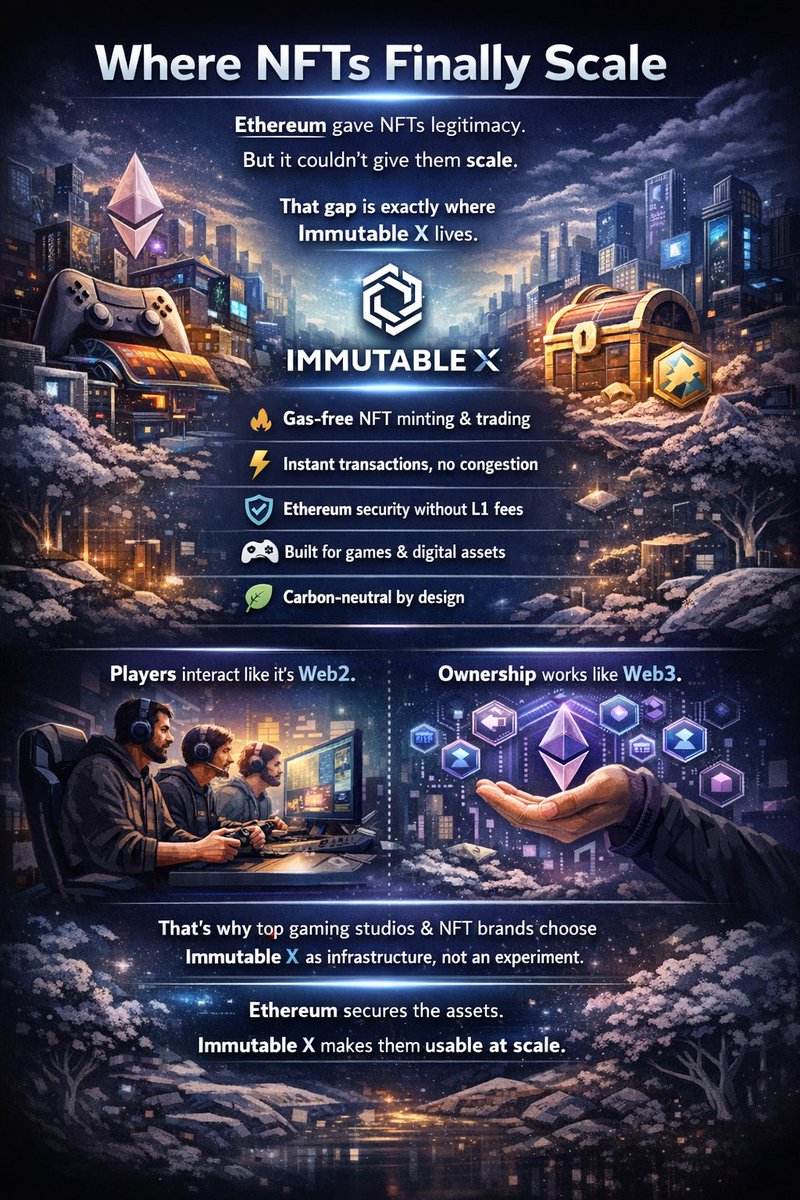

Where NFTs Finally Scale

Ethereum gave NFTs legitimacy.

But it couldn’t give them scale.

That gap is exactly where Immutable X lives.

Instead of forcing creators to choose between security and usability, Immutable X uses zero-knowledge rollups to deliver both.

What stands out:

• Gas-free NFT minting and trading

• Instant transactions with no network congestion

• Ethereum-level security without touching L1 fees

• Built specifically for games and digital assets

• Carbon-neutral by design, not as an afterthought

The result is simple but powerful.

Players interact like it’s Web2.

Ownership still works like Web3.

That’s why serious gaming studios and NFT brands are choosing Immutable X as infrastructure, not an experiment.

Ethereum secures the assets.

Immutable X makes them usable at scale.

25

26

86