Joined June 2009

- Tweets 5,280

- Following 975

- Followers 12,475

- Likes 5,605

1,121 Photos and videos

Pinned Tweet

5 Jul 2022

1/ Introducing the Crypto Banking System, a roadmap to bring DeFi to be a challenger to TradFi

cryptobanking.network/the-cr…

38

159

790

Jun 9

The value of tokenized bank deposits is the compatibility and fungibility with stablecoins.

Ortherwise it is indeed mainly useless.

Jun 9

I wrote about this yesterday. The benefits of tokenized deposits for end customers are very hard to identify.

There may be some internal efficiency benefits for very large banks, which may translate into faster or cheaper experiences for end customers (though that’s likely to be marginal).

Tokenized deposits provide banks with regulatory benefits that they can pass along to end customers because of the restrictions placed on stablecoins (e.g., yield).

And banks may be able to make the limitations of tokenized deposits less painful for end customers if, for example, they create a network to increase interoperability (which is what TCH is working on).

But tokenized deposits still won’t come close, in terms of utility for end customers (above and beyond what regular deposits can do), to stablecoins.

2

972

SebVentures retweeted

Big thanks to @tokenterminal for the detailed Q1 2026 report.

Our north star remains the same: disciplined risk curation and transparent infrastructure our users trust.

Full metrics and team commentary below

2

6

17

3,951

1

3

24

2,554

May 28

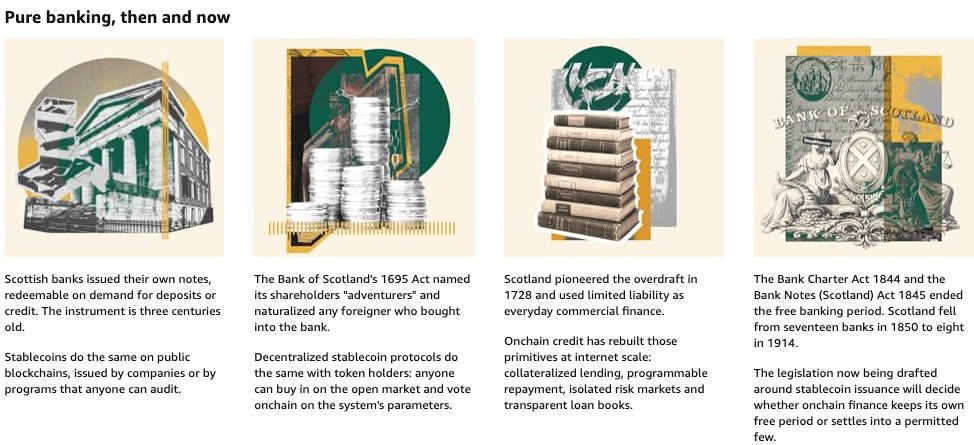

When someone refer to free banking, it is my view that he should start with Scotland.

There is so much to learn.

In 1 month, @SteakhouseFi will tell you why.

🏴🏴🏴

3/ There are no perfect historical analogies for or against stablecoins as private money. Canada did not have crises under free banking for the same reason it had no crisis in 2008: its banking system was national, oligopolistic, and more heavily regulated than in the U.S.

1

3

11

1,272

I'm assuming this is mostly rage-baiting hyperbole, but it's still worth drawing the distinction here, especially given how new onchain vault products are and how few people have actually looked under the hood.

The hedge fund comparison breaks down at the part that actually matters, which is custody. A fund manager holds your assets and moves them around at their own discretion. A Morpho vault curator never touches the deposits at all. The smart contract holds the funds, the protocol enforces the rules, and the curator only sets parameters. We could disappear tomorrow and your money would sit exactly where it is, governed by code anyone can read.

And it goes further than custody. The Guardian role on our @SteakhouseFi vaults isn't us, it's the depositors, all of them in aggregate. If Steakhouse proposes adding a new collateral, any depositor can start a vote to veto it, and we set the quorum deliberately low so it only takes a small fraction of them to block it. Nothing gets slipped in behind your back. New collateral sits behind a timelock, so if you don't like what's coming you can either help vote it down or just withdraw before it ever goes live. You would have to wait until the next investor update to learn about mandate drift in a hedge fund. Here you get a vote and an exit before anything changes.

What curators configure is asset backed lending, with transparent and strongly enforced constraints. Every position is a loan against posted collateral, with a published liquidation loan to value, a named oracle, a defined rate model, and hard supply caps. It's hardly a black box though I concede it can be hard to parse and compare. It is, however, evidently not opaque.

Compare that honestly to a credit hedge fund. There you get a quarterly letter, marks you can't independently verify, concentration you can't see, unilateral discretion, and a manager who is literally holding your money. With a vault you get every loan, every allocation, every realized loss, and every fee, live, queryable by anyone, enforced by code instead of promised in a pitch deck. It's not less transparent than a fund. It's dramatically more.

You are right that the data can be scattered and that nobody has fully packaged it yet. That is absolutely a frontend and user experience problem. We also believe it is eminently fixable and our philosophy is to show our work and maximize the constraints we operate our vaults with.

The reason we build onchain is to put more transparency into a system that has spent decades getting good at the opposite. We're not perfect and there's considerably more that needs to be done to achieve that, but we believe we're on the right trajectory.

May 27

If you really think about it, vaults are effectively hedge funds run by curators

> Users deposit capital -> receive vault shares -> curators allocate funds and charge mgmt fees on AUM and carry on returns...sounds like a fund product to me

> I’m all for simplifying defi, but nuts that protocols present these products on their frontends to users without any of the disclosure you’d expect from a manager stewarding billions: track record, realized losses, methodology, conflicts of interest, etc.

> Fwiw most curators are good actors offering valuable services, but the fact that users need to sleuth on-chain and hunt down scattered info to diligence a product presented as a "vault" feels like a giant landmine hidden in plain sight

6

15

74

11,262

May 28

Can someone show me when T-Bills were illiquid ?

And repo against treasuries illiquid for more than a day?

When did a G-MMF break the buck (trap inside)?

What are those moments @greg_ip ?

5/ A few additional points. I accept that the Genius act limits both the leverage and risk inherent in fractional banking that led to historic crises. But it doesn't eliminate it, because even the safest assets can become illiquid at moments of stress.

1

4

691

SebVentures retweeted

1

4

19

2,291

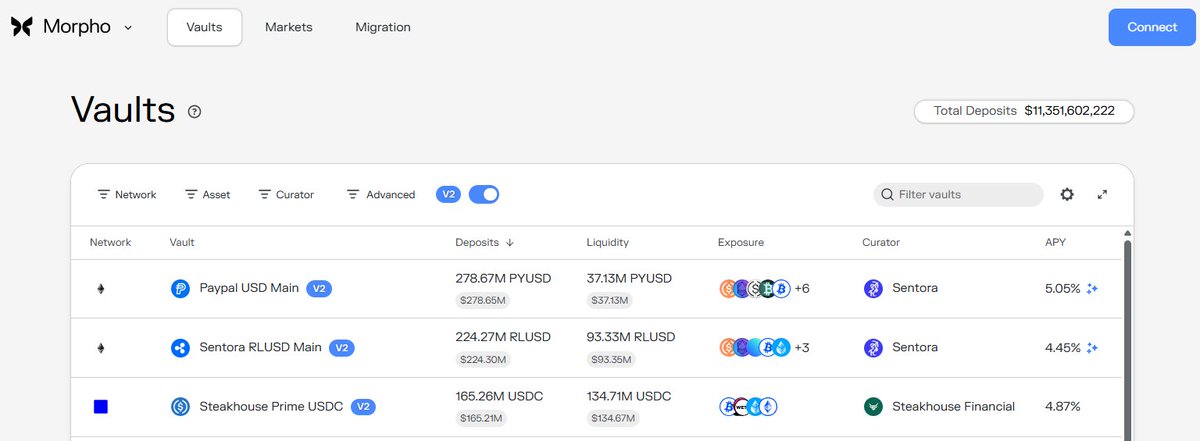

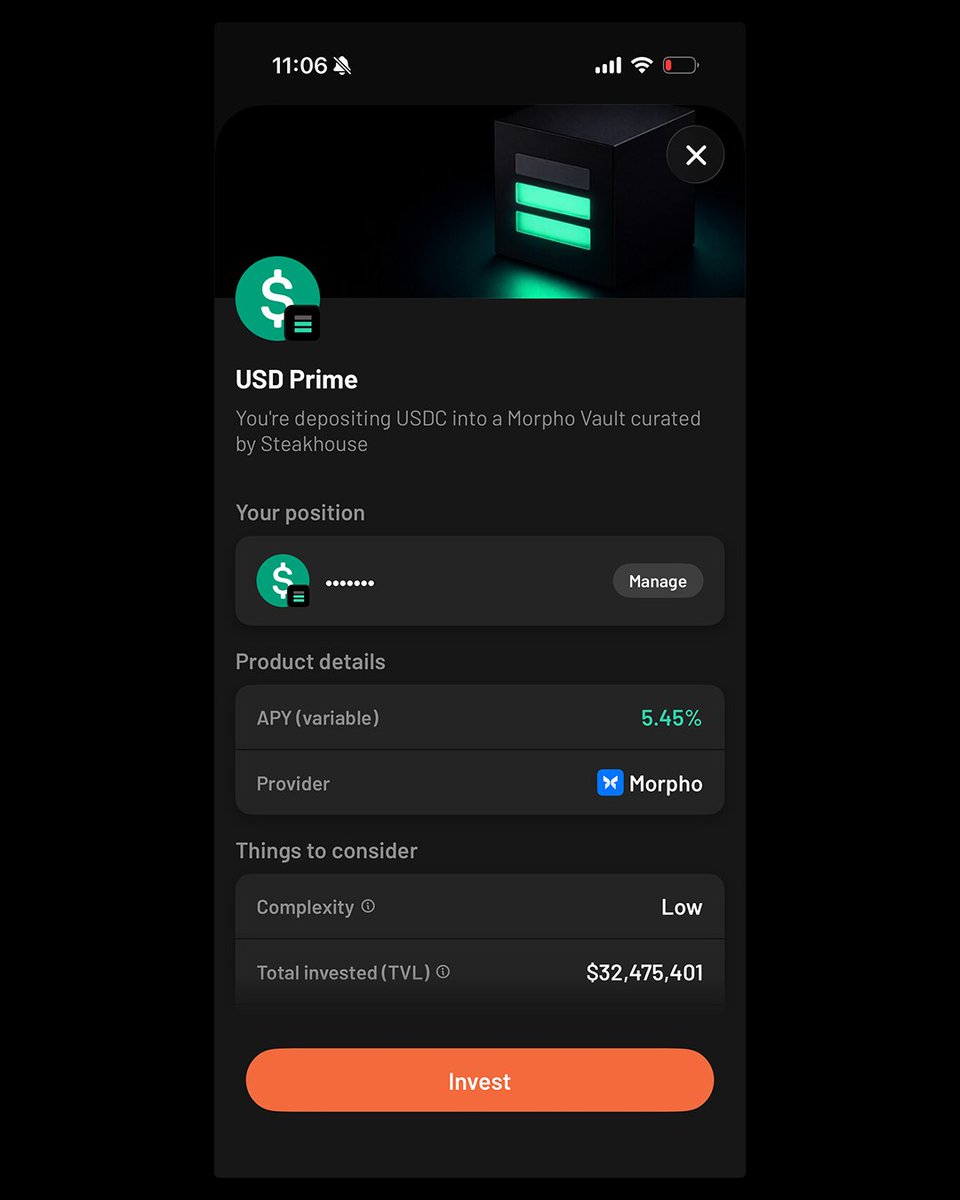

What happens when 3 of Europe's best collab?

USD Prime 💸

USD Prime is built on @morpho, curated by @SteakhouseFi, and available on Ready

35

3

38

6,940

May 20

👀

May 20

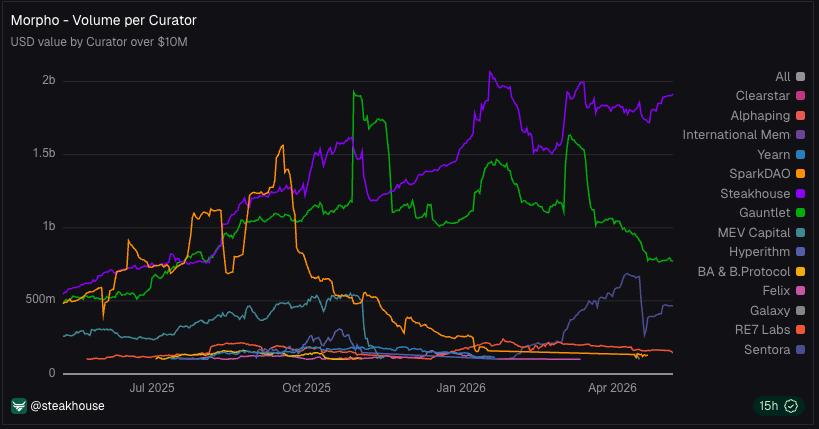

🥩🏡 @SteakhouseFi is pulling away from the pack.

Steakhouse currently holds a ~$1 billion lead over the next largest @Morpho vault curator, up from virtually no lead a year ago.

A curator ecosystem to follow 👇

1

1

7

1,679

SebVentures retweeted

1

4

17

1,553

SebVentures retweeted

May 14

RWAs are about to have their stablecoin moment.

Introducing Grove Basin: programmable credit infrastructure enabling eligible tokenholders instant stablecoin liquidity for approved exits from tokenized offchain assets.

Up to $1 bn in committed daily liquidity.

Tap in 🚰

330

1,775

5,452

1,008,864

May 11

The new @BlackRock tokenized MMF is quite structural shift.

- an actual MMF (2a-7), not a private fund

- still bad for retail and DeFi composability

- 📌strategy to provide singleness of money for GENIUS stablecoins ⚓️

- fees are high but not crazy (20bps)

sec.gov/Archives/edgar/data/…

3

2

19

2,624

SebVentures retweeted

If I were a saboteur trying to destroy the Euro from within while remaining undetected, I would not be doing anything differently than what the ECB is already doing.

May 8

Stablecoins are not an efficient way to strengthen the international role of the euro, says President Christine @Lagarde.

The best solution remains deeper capital market integration through the savings and investment union and a stronger safe asset base ecb.europa.eu/press/key/date…

16

23

200

7,150

May 8

Ulrich Bindseil seems to be on a warpath since leaving the @ecb . Amazing what happens when people can actually say what they think.

blockchain4europe.eu/wp-cont…

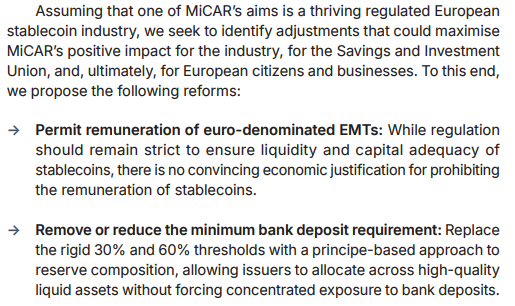

Gems:

"Relying excessively on bank deposits for backing brings an element of fractional backing to EMI-issued EMTs which in times of financial stress could lead to fragility, even with banking regulation and liquidity support for banks"

"remunerated stablecoins would not be expected to offer yields as high as those of short-term, high-quality debt instruments that back them. Rather, their remuneration would likely be lower due to their superiority as moneys – a convenience yield (which mirrors their need to hold only assets of highest liquidity and credit quality)."

"without promoting euro-denominated stablecoins, the euro will continue to underperform relative to the role it could play in international finance."

"Of course, there remains some uncertainty over the impact of remunerated stablecoins on the banking and broader financial systems, but it is vital to move away from knee-jerk claims about stablecoins’ impacts on banks"

"The minimum required deposit share of stablecoin reserves under MiCAR appears to be not only a symptom of the influence of banks on MiCAR, but also of a collective failure to understand flow of funds dynamic which led to the wrong conclusion that stablecoins absorb deposits if they invest their reserves into securities, while they do not if they hold deposits with banks"

4

2

19

1,864

May 8

Once again, framing stablecoins as private liabilities to express it is bad. While forgetting to say that bank deposits are exactly the same (both issuers are private companies and supervised by the central bank).

Funny to use SVB as example of the biggest risk of stablecoins as ... it is showing that banks are the key risk (which MICA forces stablecoins to have outsized exposure for no reasons).

So much energy used to compete against EUR stablecoins to sell their own CBDC, whatever it is. Great use of public funding.

May 8

Stablecoins are not an efficient way to strengthen the international role of the euro, says President Christine @Lagarde.

The best solution remains deeper capital market integration through the savings and investment union and a stronger safe asset base ecb.europa.eu/press/key/date…

8

9

99

7,155

SebVentures retweeted

At our European Policy Reception during @ParisBlockWeek, we caught up with our good friends over at @SteakhouseFi!

Co-Founder, @SebVentures, gave Adriana Ennab a rundown on exactly why they partnered with us!

Watch till the end to find out his views on fighting for your 4%👀

2

4

13

1,480

SebVentures retweeted

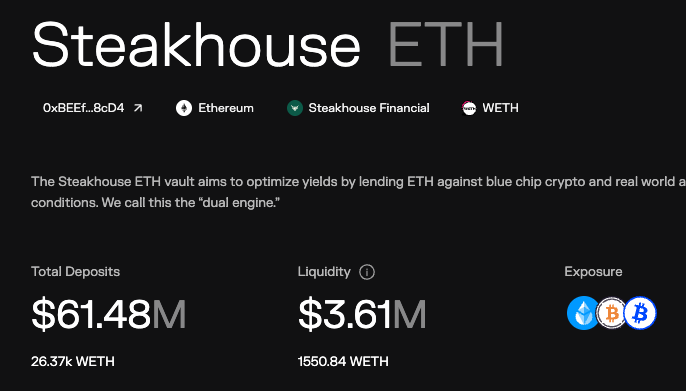

Steakhouse V2 vaults have begun to allocate directly to @morpho V1 markets.

V1 depositors remain unaffected through the transition, but there will be a decrease in V1 deposits, since V2 vaults won't be routing through these. Liquidity remains unchanged and aggregated at the market level.

We recommend all V1 users move their positions to V2. This is where Morpho incentives accrue, and where the ongoing developments will focus.

For V1 vault users, migrating to V2 is straightforward: visit app.steakhouse.financial, connect your wallet, and follow the migration path from the Portfolio page.

As part of a requested migration by Morpho, Steakhouse V2 vaults will progressively transition from allocating to Morpho Vault V1s to allocating directly to the Markets V1 Adapter in order to remain visible in the Morpho UI.

At present, most V2 vaults allocate to a V1 vault, which then allocates to V1 markets on Morpho Blue. This update removes that intermediate layer and simplifies the overall structure.

This is an operational and structural change only. It does not affect the underlying market exposures of the vaults, and it has no impact on users of the V1 vaults themselves. Over the coming weeks, Steakhouse will perform a significant number of curation operations to implement this migration across its V2 vaults.

25

3

25

5,559

I appreciate the call-out to @SteakhouseFi in the report. It was nonetheless very stressful. It continues to be a knife-edge until the teams involved, at their earliest convenience, find a reasonable resolution to unfreeze liquidity.

There is no victory lap or dunking possible about net flows to different places. We are not interested in shuffling musical chairs around. The overall movement of liquidity (>$10bn in net outflows from the system as a whole) is a verdict on the presumed cost of capital for operating in all onchain money markets.

Our response from @SteakhouseFi is definitive. We are already known to issuers for being a huge pain in the butt and we are proud of it. In the good cases, this attitude is appreciated by teams and feedback is taken onboard. People should expect this to escalate.

We will be ratcheting up the hurdle on issuers to demonstrate seriousness from a credit and market perspective but in particular from a security point of view. This includes the expectation of working with trusted third-party subject matter experts to review and monitor security practices.

We continue to advocate that Prime repo is priced reasonably efficiently - and indeed rates on Steakhouse Prime vaults played that out over the past few weeks. However, High Yield markets have an operational risk factor that is clearly not adequately captured by the market at the moment.

Our goal is to leverage our outsize position in the curation market to drive this change in a positive direction. So far, it has been encouraging to see a reciprocation in the response from issuers we have floated this to.

I am positive we can demonstrate that onchain capital markets can operate at greater speed, more transparency and significantly lower risk over time.

8

10

97

19,873