Sharing real world insights as the former CFO of a multi-billion dollar company. Opinions, not advice.

Joined July 2021

- Tweets 11,345

- Following 522

- Followers 129,543

- Likes 20,375

886 Photos and videos

Pinned Tweet

15 Dec 2024

How did one VP of Finance bring Macy's to its knees with a $151M accounting scandal?

Here’s how I think it all went down… (THREAD)

61

153

1,467

908,938

Love that Sirius is the walkout music for each World Cup game

2

6

3,309

The Secret CFO retweeted

Jun 12

If you aren’t subscribed to this newsletter, you are missing out.

Absolutely banger content.

Apr 23

Nothing more exciting than seeing like 50 new newsletter subscribers all land within a couple of days from the same company domain.

It means someone important shared it and told them to read...

2

1

19

22,930

Jun 9

Private credit funds: let us know how we can be helpful

The help:

4

1

90

12,202

Jun 6

I frequently hear that the CFO should 'drive' growth.

And often read L*nkedIn blowhards trying to rebadge the role as 'Chief Growth Officer' or 'Chief Future Officer' or whatever.

It's such nonsense.

Growth comes from product and sales teams. Everyone else (including finance) is an enabler in that equation, not a driver.

The default mode for the CFO should be to remove the obstacles to growth.

Think of it like this; if product, sales and marketing are the ones firing the burner on the hot air balloon, the CFO's job is to control the sandbags - throwing off as many as they can, but without risking the trip.

It's about knowing when to get out of the way, and when to get in the way. It requires fine judgment and a good map.

Which bring me to the announcement of the latest series of The Secret CFO Playbook... in June I'll be writing as 4 part breakdown of what it means to be a Growth CFO.

Here's what's in store:

Post I. (Tomorrow) Series Introduction

- A personal horror story

- Growth in a winner takes all economy

- A case study

- Should you grow at all?

Post II. What is Growth?

- The cost of standing still

- Lagging vs leading indicators

- Organic vs inorganic, new vs existing, price vs volume, and when each matters

- How to know when you’ve earned the right to grow

Post III. The Math of Growth

- Strategic unit economics

- P&L vs Cashflow growth math

- Commitment vs conviction: how sure do you need to be to spend?

- Funding growth

Post IV. Building a Growth-Friendly Finance Function

- Picking the right metrics

- Guardrails vs hardrails: knowing when to get in the way

- Budgeting for growth

- Reporting growth

Link to the first part in the comments below

9

2

93

16,899

Jun 6

Part I of this month long series: The Growth CFO out now….

cfosecrets.io/p/permission-t…

1

6

2,808

The Secret CFO retweeted

Jun 4

It’s funny when you step outside the tech and online bubble… most CFOs still aren’t really doing anything with AI.

I asked one about controlling token spend earlier in the week, he said “what’s a token?”

This was a serious finance leader in at a big consumer brand. Was far more concerned about margin pressure from inflation risk, supply chain fractures, a big CapEx program, refi risks / credit markets.

Do remember that this is where most businesses are at still with AI… they’ve got a heap of shit on their desk to work through.

It’s still very very early.

37

13

197

34,607

The Secret CFO retweeted

Jun 4

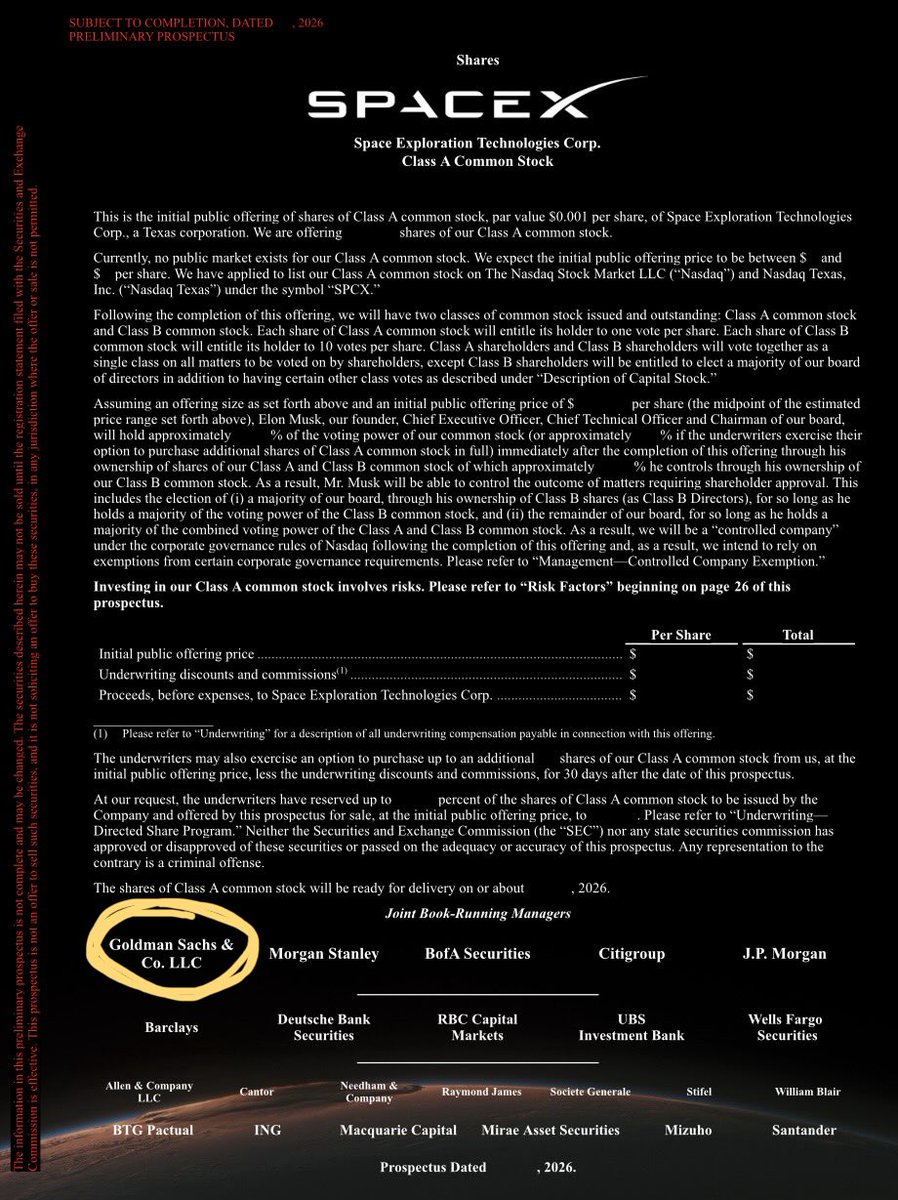

Someone should tell the FT there’s a good reason this part of the cover page of the S1 is not in alphabetical order

Jun 4

Goldman Sachs expects SpaceX’s AI revenue to surge 100 times by 2030 ft.trib.al/psRqF2H

5

9

230

67,156

May 31

Leadership roles done right are basically 3 things:

1. Joining dots others can’t

2. Solving problems others can’t

3. Finding and retaining people who can help reduce 1 & 2

4

8

109

9,928

May 31

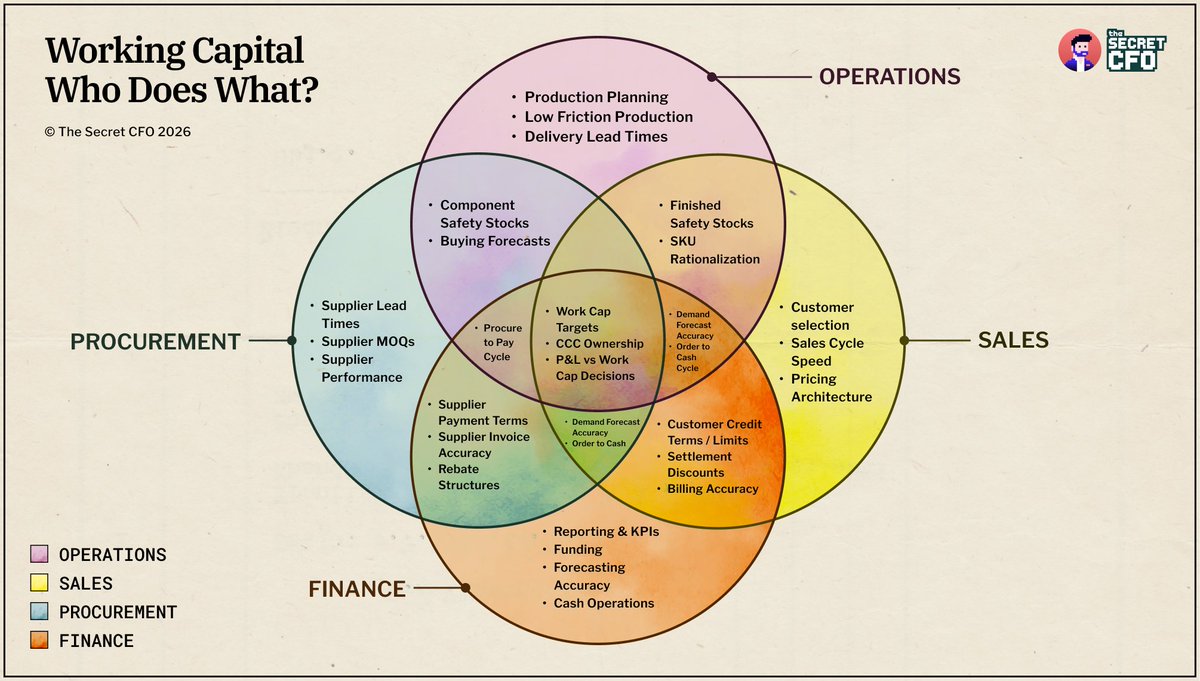

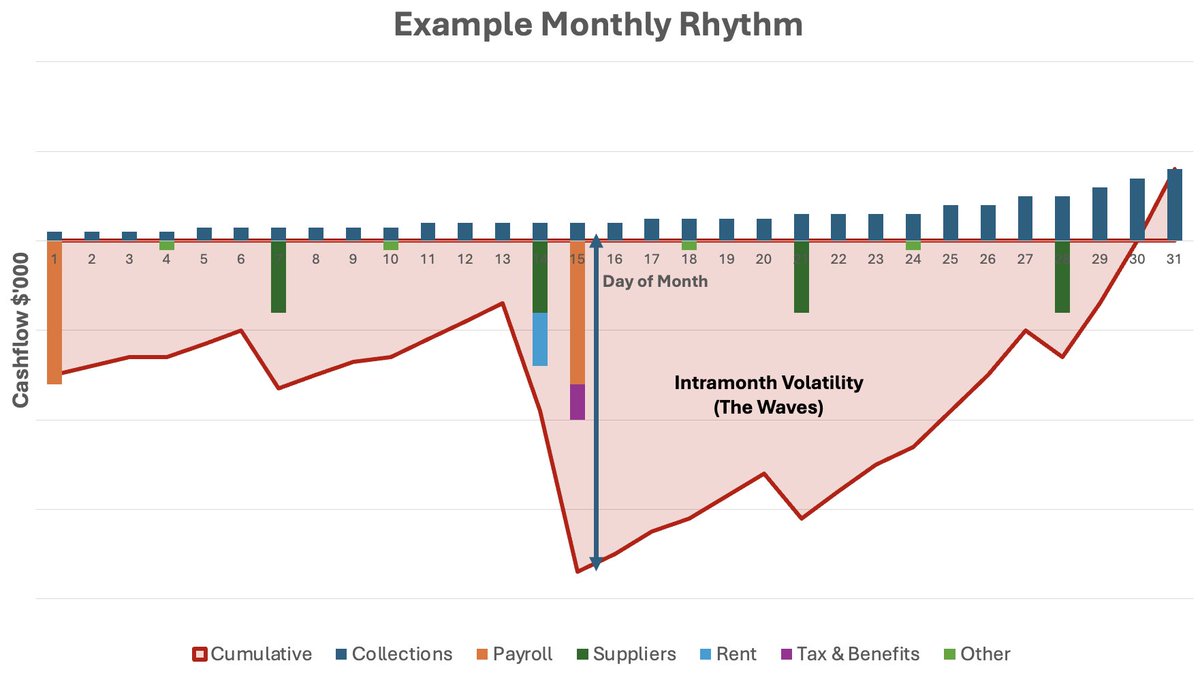

No other discipline will test your ability to mobilize the business across functions and the C-suite more than working capital management.

Given the opportunity to prioritize something else, the business will always take it, and leave working capital as a finance problem.

But finance doesn't really control the levers. So who does?

Well… it crosses a lot of functional barriers.

Cashflow is where many different business processes converge; order-to-cash, procure-to-pay, inventory, etc.

Some things are easy to allocate: finance owns reporting, operations owns fulfilment, sales owns volume, procurement owns supply.

But the most important levers land in overlaps between the functions.

In yesterday's week's Playbook, we concluded our 5 week series for May; Working Capital Warfare.

It included a whole bunch of practical working capital tactics, and why Cash Conversion Cycle is a crappy metric.

You can read it here: cfosecrets.io/p/lock-and-loa…

1

2

45

8,291

May 30

Absolutely nothing can go wrong here …

Rule changes for the SpaceX $SPCX IPO:

Index providers waived the profitability requirement and cut the seasoning window from 90 days to 5.

This forces over $30 trillion in passive 401k and retirement money to buy SpaceX at IPO valuations.

Bloomberg Intelligence estimates S&P 500 funds must absorb 19% of SpaceX's float within 6 months.

Russell 1000 and Nasdaq 100 funds will absorb 24%.

The rules built to protect passive investors:

1. S&P 500 has required 12 months of trading and 4 quarters of GAAP profitability since 2002. Both waived.

2. Nasdaq cut its inclusion window from 90 trading days to 15.

3. FTSE Russell cut its to 5.

All three benchmarks are now structured to buy SpaceX at IPO pricing.

1

1

34

23,808

May 30

If you can operate profitably on a much lower gross margin than your competition you have one of the best moats there is

.@ericries explains why former Costco CEO Jim Sinegal refused to raise the price of everything in the store by $.03, despite the fact that Costco knew it wouldn't decrease sales, and would increase their net income by 50%:

"He says, 'It's like the business equivalent of taking heroin. You do it once, and then you got to do it again, and again, and again. Next thing you know, you're not the low-price leader.'"

"You can get away with screwing people over. You always do it, no matter what. You raise margins. Margins are a source of strength."

"But Costco is built on a very different philosophy, which is that margins can be a source of weakness. @JeffBezos understood it. He used to always say, 'Your margin is my opportunity.'"

"When you're making too much money, when you are being too extractive, you're actually harming your competitive position in the long run."

4

3

72

29,855

May 29

Soooo … if this has been counted as $6B in Anthropic’s $30B end of q1 run rate revenue claim it would be the funniest thing since the first Naked Gun movie

May 28

NEW: AI consultant reveals a client accidentally spent $500,000,000.00 in a single month after failing to set employee limits on Claude usage.

25

23

1,025

248,246

May 28

The enterprises with the biggest efficiency opportunity from AI adoption are going to be the most bloated, bureaucratic orgs.

The ones that are least able to deliver org wide AI powered change will also be the most bloated, bureaucratic orgs.

How that paradox gets resolved and when is going to be a huge determinant in the shape of the economy of the future.

May 28

It's now occurring to me that bloated companies & email job companies that are not particularly good at resource allocation now also are not very good at figuring out AI & managing spend.

Now it's all starting to make sense.

3

2

30

8,734

May 25

Nike spent it's first decade (then Blue Ribbon sports) getting to $500k of annual sales.

Then in the next decade it grew to over $250M in annual revenue by the time it IPO'd in 1980.

The unlock? Phil Knight discovered Japanese Trading Companies, and used Nissho Iwai to fund inventory during the long trip over the Pacific.

Until then the Nike story was one of constant cashflow permacrisis, with every penny of profit reinvested back into inventory.

50 years later, it's a lot easier for consumer products to fund growth. Today to get a VC check all Knight would need is a well produced video with him sincerely claiming he's been working his entire life to "reimagine the human-ground interface."

And now there's a whole ecosystem of supply chain debt products too... but be careful with those. Some are full of bear traps, no exit ramp and are as addictive as crack.

In this week's newsletter I broke down the full range of working capital funding products and the watchouts

Read it, or the next feet pics will be mine ... and you don't want that.

Get it here: cfosecrets.io/p/mind-the-gap…

4

1

46

15,582

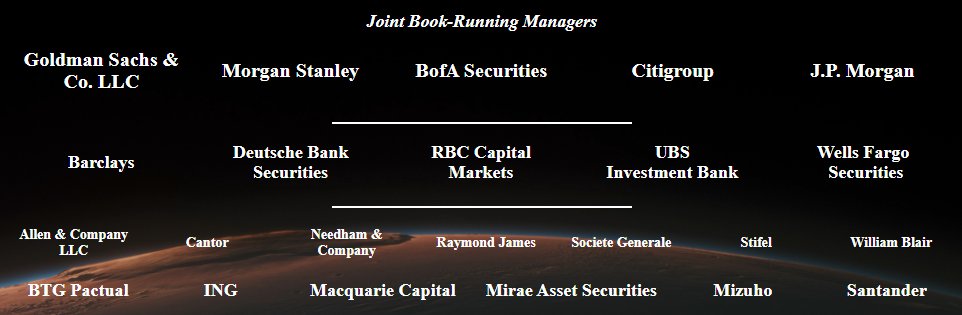

May 21

SpaceX Board:

1

53

19,101

The Secret CFO retweeted

May 17

My friend @secretCFO wrote a banger newsletter this weekend on working capital structures.

If you're an owner operator - go read that and get religious about your cash flow structure. Make it as important as your product itself.

4

2

17

8,281

The Secret CFO retweeted

May 15

So many of the great business growth stories were underpinned by a masterful working capital move in the early days; McDonalds, Amazon, Dell, Apple, Berkshire Hathaway, Nike are all examples.

Most businesses make their business model choices, then figure out what that means for working capital, and how to fund it.

These businesses made working capital central to thosee choices. Great working capital design (and execution) was fundamental to the business model itself.

There is a secret growth weapon hiding in the working capital of almost every business.

As CFO, if you can sculpt it out, it's the most extraordinary gift you can give to your business, as it unlocks the most common barrier to growth... funding.

And finding your secret weapon depends on the shape(s) of the working capital in your business... with a different playbook for each.

In tomorrow's edition of The Secret CFO's Playbook, I'll be breaking this all down and how you make working capital rocket fuel for your business.

Sign up here to get it free direct to your inbox: cfosecrets.io/

2

12

106

17,476