Elevate your investment strategy—Flash's AI podcasts and reports give you new ways to uncover the best investments in a flash. 100% FREE Reports!

Joined December 2024

- Tweets 16,190

- Following 62

- Followers 2,088

- Likes 4

5,730 Photos and videos

BCB Bancorp, Inc. $BCBP is currently executing a high-stakes turnaround strategy to resolve the severe credit losses that plagued its commercial real estate and legacy lending portfolios last year. Under the guidance of a newly appointed veteran restructuring CEO, the community bank has already shown strong signs of recovery by returning to profitability in the first quarter of 2026. Despite these structural improvements, the market continues to price the stock as a distressed asset, leaving it trading at a steep thirty-seven percent discount to its book value. Will this new management team be able to fully stabilize the balance sheet and unlock a lucrative acquisition premium for patient investors?

10

Wall Street is pricing $BCBP as a permanently impaired commercial real estate casualty, leaving the equity stranded at a 37% discount to book value. But the distressed narrative is already breaking. Credit provisions just plunged 86%, and a veteran turnaround CEO recently took the helm with his compensation directly tied to a structural equity recovery. Here is a breakdown of the asymmetric risk-reward profile inside this misunderstood bank. 🏦⚖️ #ValueInvesting #BankStocks

auth.flash.stocksentinel.ai/…

10

Guardian Pharmacy Services, Inc. $GRDN operates as a premier long-term care pharmacy provider that seamlessly integrates specialized medication management into the daily workflows of senior living facilities. By generating approximately 95 percent of its revenue from the highly recurring dispensing of chronic medications, the firm maintains a defensive and resilient financial profile. The business is positioned as a natural consolidator in a fragmented industry, utilizing a localized operating model to rapidly capture market share from rigid national competitors. With a debt-free revolving credit facility and expanding profitability margins, the company commands a premium valuation supported by strong demographic tailwinds and steady growth. Can their decentralized service model continue to fend off government-mandated pricing pressures and competition from vertically integrated healthcare giants in the years ahead?

27

At first glance, a pharmacy roll-up trading at 38x earnings seems wildly overvalued. But Wall Street is entirely mispricing the structural moat behind $GRDN. While centralized giants like CVS bleed market share in long-term care, this decentralized operator has quietly locked in a 90% facility adoption rate and just absorbed a 60% government-mandated drug price drop while actually expanding its margins. We break down the hidden mechanics of healthcare's quietest compounding machine. 📊💊

auth.flash.stocksentinel.ai/…

33

Mid Penn Bancorp Inc $MPB is a relationship-focused regional consolidator across Pennsylvania and New Jersey that is strategically transitioning toward organic asset and deposit growth. Despite a recent headline earnings miss driven by temporary merger integration expenses, the bank's core operating profitability actually increased year-over-year alongside expanding net interest margins. Supported by an expanded fifty million dollar stock repurchase program and trading at a discount to its book value, the market appears to be temporarily undervaluing its long-term compounding potential. As the franchise leverages recent acquisitions to scale its fee-based wealth management revenues, will the realization of cost synergies be enough to drive outsized shareholder returns in a shifting macroeconomic environment?

41

A massive 51% headline earnings miss usually signals a broken business, but for $MPB, it's masking a hidden pivot. Retail traders reacted to the GAAP noise from M&A integration costs, completely overlooking a 10% jump in core net income and an expanding 3.80% net interest margin. Now trading at a discount to book value just as the board unleashes a $50M buyback and shifts toward organic compounding, the risk/reward here is quietly asymmetric. Here is the real story behind the numbers. 📊 #ValueInvesting #BankStocks

auth.flash.stocksentinel.ai/…

1

39

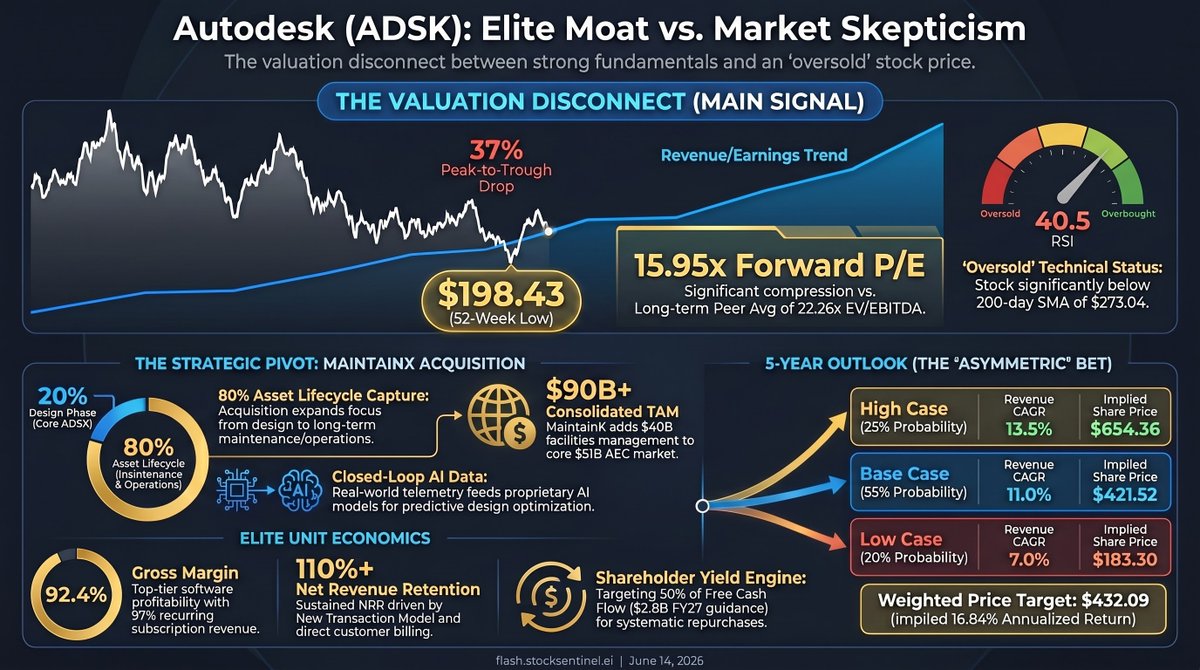

Autodesk Inc ($ADSK) serves as the indispensable, cloud-native software infrastructure and design-to-make operating system for the global physical economy. By announcing a massive $3.6 billion acquisition of MaintainX, the business is aggressively expanding its addressable market to monetize the multi-decade asset operations lifecycle. Although the firm boasts elite unit economics and strong recent earnings, investor skepticism over the acquisition's debt financing has driven the stock down to historically compressed valuation multiples. Will this ambitious operational expansion successfully close the loop on physical asset data and unlock a massive new wave of long-term shareholder value?

53

Wall Street just handed us a 37% selloff in $ADSK because they misread a $3.6B acquisition as a debt trap. The reality? Autodesk just quietly bought control over the remaining 80% of the physical economy’s lifecycle. Trading at a heavily compressed 15.9x forward P/E with 92% gross margins, the market is punishing a masterstroke. Here is the breakdown on why the consensus is dead wrong about this valuation gap. 📉🏗️

auth.flash.stocksentinel.ai/…

54

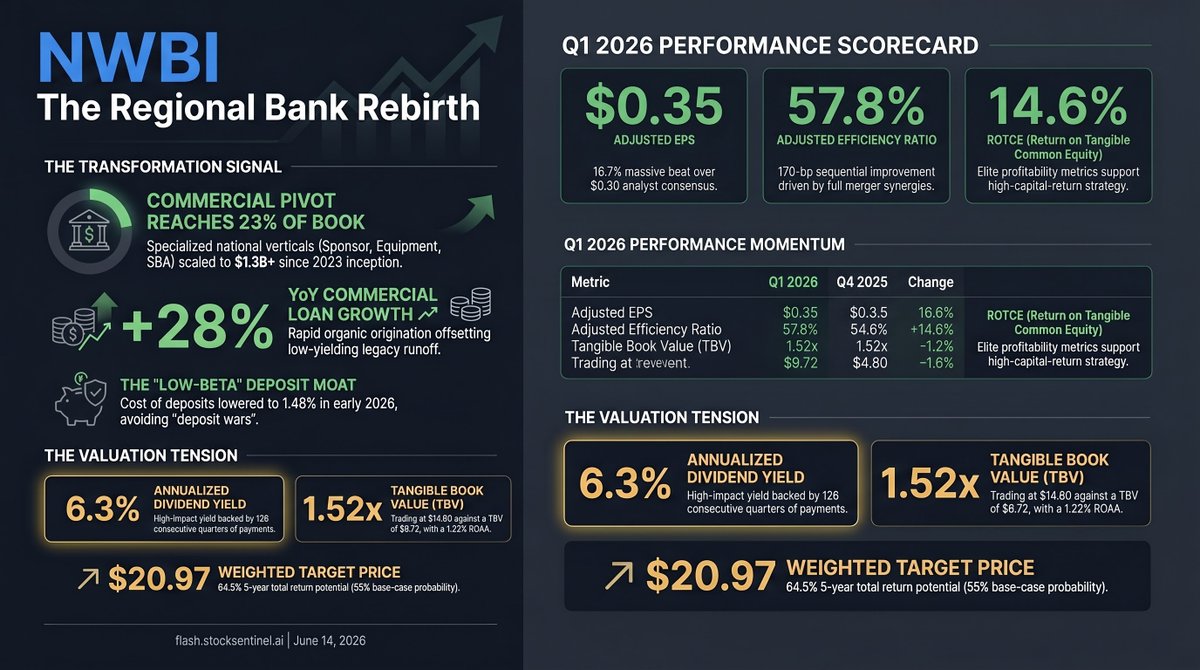

Northwest Bancshares Inc $NWBI is executing a deliberate structural transformation by reallocating capital away from legacy residential mortgages toward high-yielding specialized commercial lending. This strategic pivot into national verticals like equipment and sponsor finance has positioned the bank to rapidly capture market share while maintaining an exceptionally low cost of deposits. The stock currently presents a compelling valuation profile, trading near 1.12 times book value alongside a robust return on tangible common equity. Shareholders are further rewarded by a secure 6.3 percent annualized dividend yield backed by an impressive 126-quarter track record of uninterrupted payouts. Will this ambitious commercial growth strategy deliver enough momentum to sustain their impressive margin expansion against the looming threat of interest rate volatility?

32

The market is fundamentally mispricing $NWBI as just another sleepy legacy bank, missing the structural transformation happening under the hood. They are quietly leveraging an insulated 1.48% rural deposit cost to fund a rapidly scaling, high-yield commercial lending machine. Generating a 14.6% return on tangible equity while trading at just 1.5x tangible book, the valuation gap between the stale narrative and their actual execution is massive. Here is the breakdown. 🏦👇 #ValueInvesting

auth.flash.stocksentinel.ai/…

33

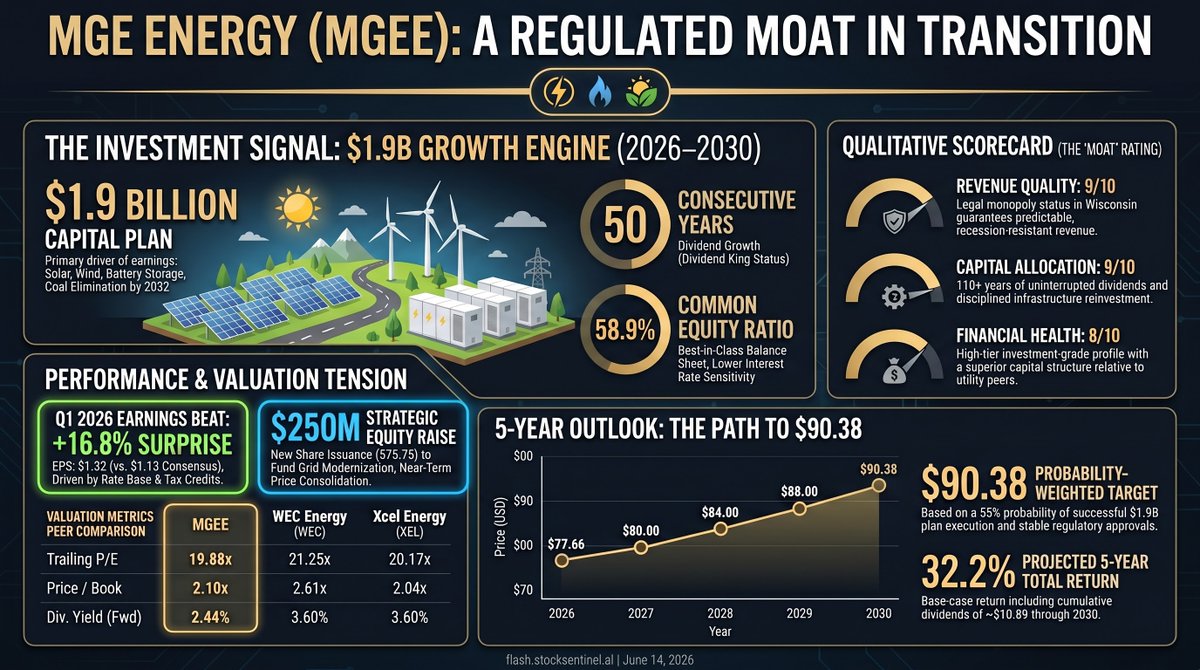

MGE Energy Inc. $MGEE operates as a stable regulated utility monopoly in Wisconsin with a resilient customer base insulated from severe economic downturns. To drive future growth, the company is executing a multi-billion dollar capital investment plan focused on decarbonizing its generation fleet through major solar and battery storage projects. Supported by an exceptionally strong balance sheet and a fifty-year streak of dividend increases, this defensive asset offers a compelling valuation for income-oriented investors despite recent equity dilution. Will their aggressive pivot toward renewable energy infrastructure ultimately translate into outsized long-term returns for shareholders?

51

Wall Street just punished $MGEE for a $250M equity raise, entirely missing the actual story: a 16% earnings beat masked by short-term dilution. While competing utilities choke on high-cost debt, this legally protected monopoly is leveraging a rare 58.9% equity cushion to fund a $1.9B, practically risk-free rate-base expansion. Here is the real math behind the recent sell-off. ⚡📈 #ValueInvesting #Utilities

auth.flash.stocksentinel.ai/…

47

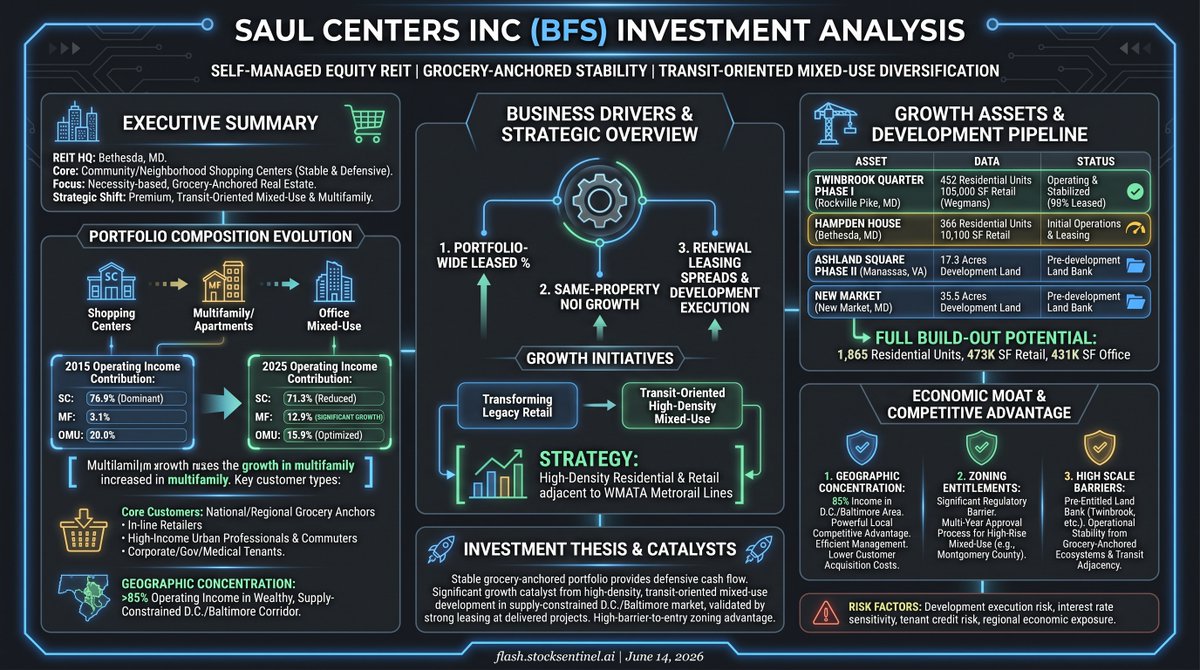

Saul Centers Inc $BFS is a highly defensive real estate investment trust strategically transforming its grocery-anchored suburban shopping centers into premium, transit-oriented mixed-use developments across the affluent Washington, D.C. corridor. The company recently delivered a massive first-quarter earnings beat fueled by surging same-property net operating income, proving the resilience of its necessity-based retail assets. Exceptionally strong insider ownership aligns management directly with shareholders as they navigate the capital-intensive lease-up phases of major residential properties, despite carrying a heavily leveraged balance sheet. Will the rapid stabilization of its new luxury residential towers be enough to overcome the drag of high interest rates and unlock significant long-term shareholder value?

60

Wall Street is fundamentally mispricing $BFS, treating it like a highly leveraged legacy retail portfolio rather than a premium, transit-oriented developer in disguise. They just posted a massive 98% earnings beat, yet the market remains fixated on a temporary $4.8M GAAP drag from their newest residential tower. What the algorithms miss is that once this single asset stabilizes, an earnings anchor instantly flips into a primary FFO catalyst. With insiders tightly holding 47% of the voting stock, here is the real thesis behind the numbers. 🏢📈 #REIT #ValueInvesting

auth.flash.stocksentinel.ai/…

65

Mistras Group, Inc. $MG is executing a profound structural turnaround, shifting away from cyclical energy contracts to become a digital-first provider of high-margin predictive asset intelligence. The company is already demonstrating significant operational momentum, recently achieving record adjusted earnings and exceptional growth in its aerospace and defense segment. Despite these fundamental improvements, the stock trades at a massive discount to its estimated fair value due to temporary cash flow constraints caused by longer billing cycles. As management actively resolves these working capital hurdles to rapidly reduce debt, will investors capitalize on this rare valuation mismatch before the broader market catches on?

58

The market has completely misclassified $MG. Investors are pricing it like a cyclical energy contractor suffering from an oil revenue dip, entirely missing the "high oil price paradox"—these are legally mandated pipeline inspections that are merely deferred to maximize crude output, not lost. Meanwhile, their high-margin aerospace segment just quietly grew 35% and EBITDA margins are hitting all-time highs. Trading at just 1.1x EV/Revenue, here is why this structural turnaround is hiding in plain sight. 📊💡 #ValueInvesting #SmallCaps

auth.flash.stocksentinel.ai/…

78

Utz Brands Inc $UTZ is aggressively transforming from a legacy regional snack manufacturer into a national powerhouse by expanding its distribution footprint into lucrative Western markets. By prioritizing its high-margin Power Four brands and shifting to a highly efficient independent operator model, the company is successfully driving structural gross profit gains. Despite outpacing the broader salty snack category in retail sales growth, the stock trades at a steep discount to historical averages due to elevated debt levels and macroeconomic fears. Will this ambitious geographic expansion and brand premiumization be enough to capture significant market share from established industry giants and unlock its massive upside potential?

60

Wall Street is pricing $UTZ like a stagnant, over-leveraged regional brand about to be crushed by GLP-1s, completely missing the underlying margin turnaround. Beneath a heavily depressed 8.2x EV/EBITDA multiple, Utz just quietly gutted $60M in fixed route costs, paid down debt to a public-company low, and is actively stealing West Coast market share from Frito-Lay. Here is the deep dive on one of the most asymmetrical, mispriced setups in consumer staples right now. 🥨📊 #ValueInvesting

auth.flash.stocksentinel.ai/…

73

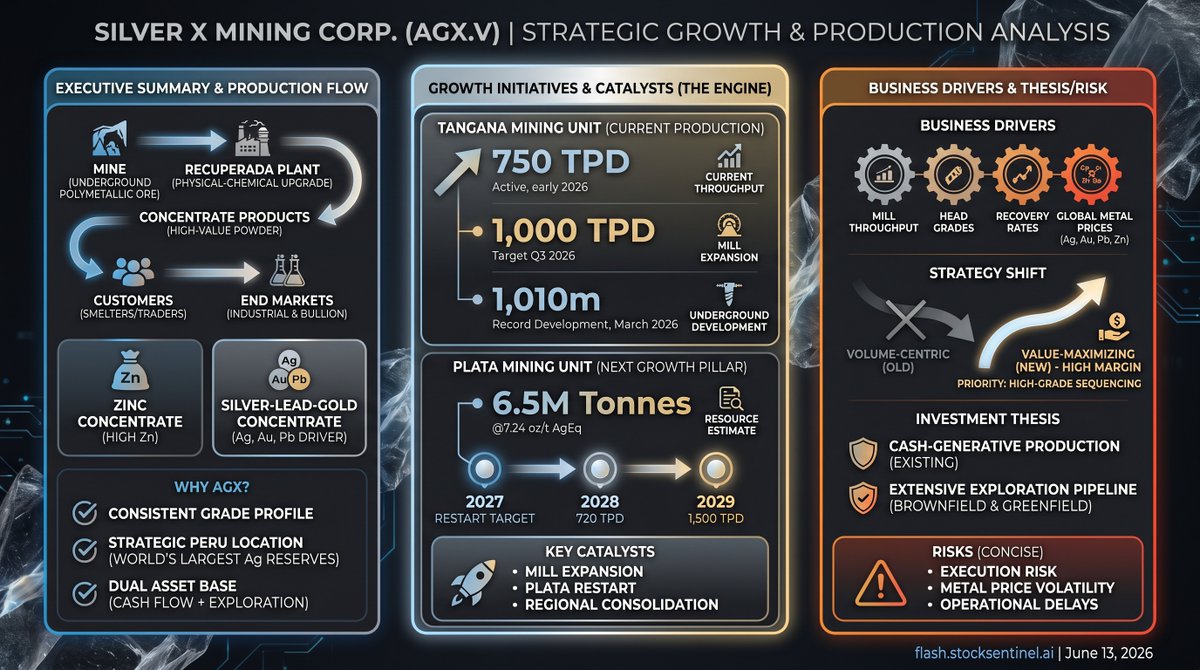

Silver X Mining Corp. $AGX.V is aggressively expanding its district-scale platform in Peru by transitioning to a value-maximizing, high-grade polymetallic mining strategy. This operational turnaround recently fueled a massive 155 percent year-over-year revenue increase and a swift return to profitability for the business. The stock currently trades at a steep discount, carrying a market capitalization of roughly 206 million Canadian dollars against an estimated asset net present value of 439 million US dollars. As management races to scale up mill throughput and restart historical mines, can this junior producer successfully navigate its high debt costs to fully unlock its massive upside potential?

74

The street is applying a massive execution discount to $AGX.V, pricing the company at less than half of its underlying net present value. What the market is missing is a structural operational pivot: by intentionally processing lower volumes of higher-grade ore, they just triggered a 155% revenue spike and flipped to profitability. Here is a breakdown of why this infrastructure monopoly is severely mispriced. ⛏️📊 #Silver #Mining

auth.flash.stocksentinel.ai/…

1

62