Understanding the tech behind the ticker. → signalchainmike.substack.com | not investment advice

Joined May 2026

- Tweets 151

- Following 168

- Followers 41

- Likes 154

4 Photos and videos

Pinned Tweet

A profitable biotech with a ~$1B drug, ~$710M net cash, and 5 Phase 3 programs, trading at roughly 11x earnings.

The current price appears to largely reflect the 2030 patent cliff with limited credit for the pipeline. I'm long. Here are the numbers from the DCF and rNPV.

$HRMY

Disclosure: I hold a long position in HRMY. I won't trade it for 5 business days after this post. Not investment advice, just for entertainment purposes . Full disclaimer on the Substack.

THE BUSINESS

WAKIX, the narcolepsy drug, is on track to cross $1 billion in annual revenue, up 17% last quarter. The company is profitable, holds ~$710M net cash against $160M debt, and funds its pipeline from operating cash flow.

WHY THE VALUATION LOOKS LOW

Two real overhangs: a 2030 patent cliff when generics can enter, and heavy revenue concentration in one drug. The stock trades around 11x earnings, a discount to the broader market and most profitable biopharma names.

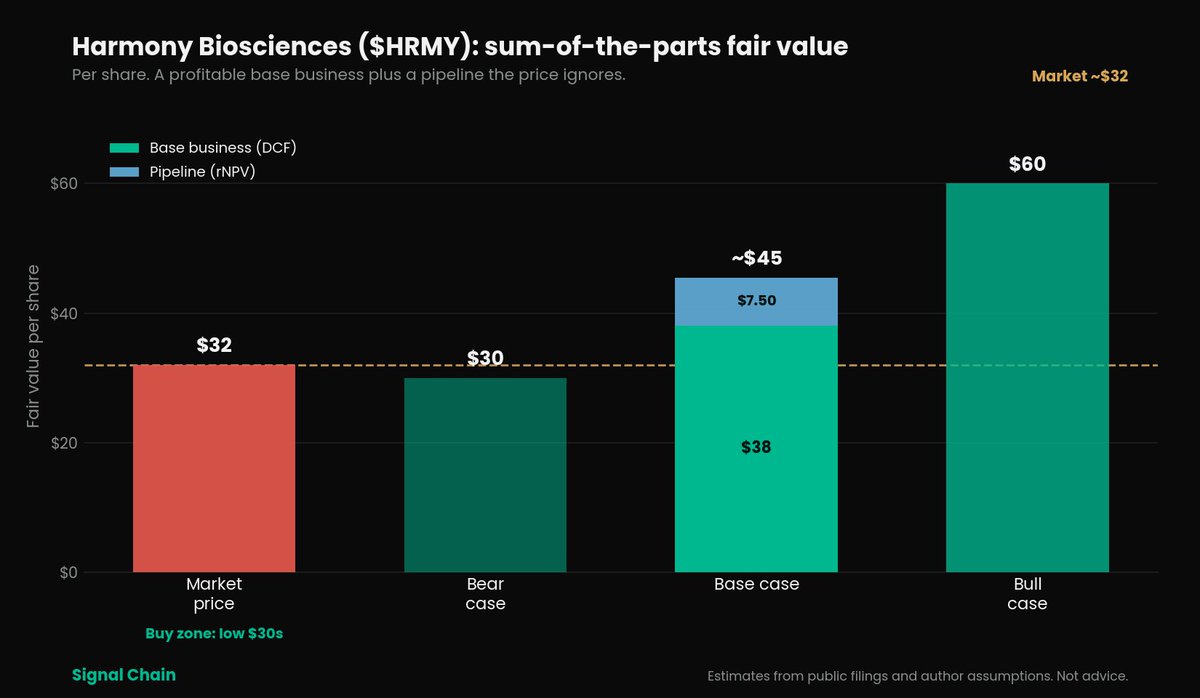

THE VALUATION

I broke it into two pieces. The existing WAKIX business, with the 2030 cliff modeled fully, comes to about $38 per share on a DCF. That is roughly the current price on its own.

The pipeline (5 Phase 3 programs plus next-gen formulations that can extend the franchise past 2030) adds about $7.50 per share on a risk-adjusted basis.

Base business $38 pipeline $7.50 = ~$45 base case. Bull case toward $60. Bear case near $30, close to where it trades now.

A graph of the valuation cases is attached to post

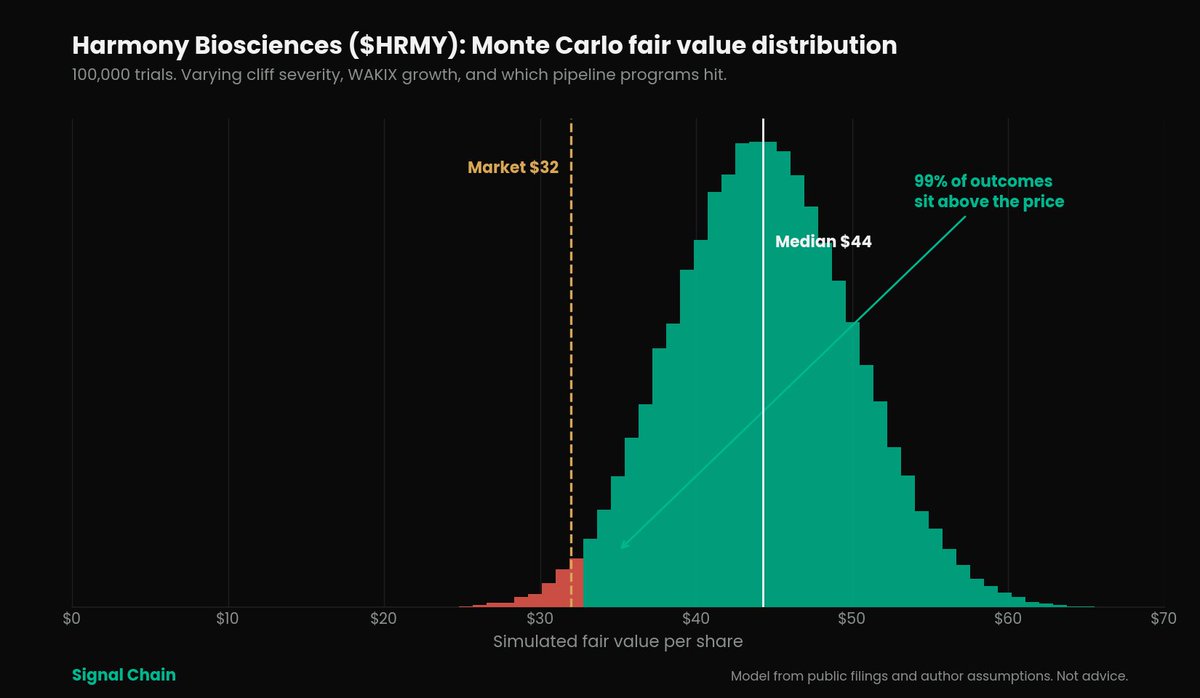

I also ran the model 100,000 times, varying the cliff severity and which pipeline programs succeed.

Median: ~$44 per share.

5th percentile: ~$35 (still above the current price).

Share of outcomes above the current price: ~99%.

The distribution centers above the price on these assumptions.

A histogram of the Monte Carlo is attached to post

THE READ

The downside is supported by the net cash position and the cash-generative base business. The main upside driver is successful execution on the pipeline, especially the next-generation formulations.

The stock has already run from its lows, so the margin of safety is thinner than it was earlier. The low $30s offered a clearer entry on the model. If the price has moved well past that zone by the time you read this, waiting for a better setup makes sense rather than chasing.

For the full science on how the drugs work, detailed pipeline review, complete model assumptions, and all the risks, check my profile for the link to Substack deep dive.

533

Given a critically important outcome, would you trust AI to give you a perfect answer without double checking?

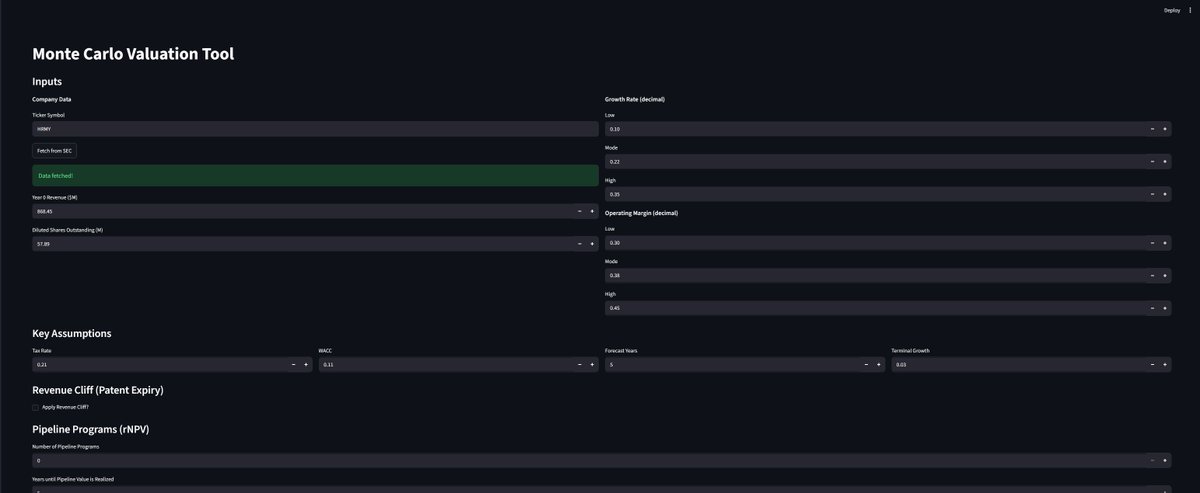

When evaluating companies I use a python program to quickly run the numbers on a DCF, rNPV and run a monte carlo simulation and give me a graph of the results.

AI wrote me the program, but believe me when I tell you I double checked all the work to make sure the way it calculated things was correct. This required me to have an understanding of Finance and understanding of Python.

Would you trust a financial adviser who took AI at its word without double checking? Would you trust a doctor? Architect? I sure as hell wouldn't trust my life savings on it, but I'd be a fool not to use it to make tools like this that can help me.

AI will be a productivity multiplier, we'll be able to do more in less time, but it'll still be us doing it.

14

Jun 14

Super happy to see the Knicks win it all, but the NBA has got some of the weirdest team names by a wide margin.

Teams named after pants, bodies of water, sailing ships. But anyway congrats to the most famous pants in the world.

98

Jun 14

Working on a deep dive on Atomera(ATOM) , a small cap semiconductor company with a high margin royalty business selling a unique process to fabs to improve their products without requiring any new equipment. Deep drive drops 6/16. $ATOM

273

Jun 13

if the knicks win tonight I'm calling my broker and telling him to sell everything and buy every safe-lite glass repair in NYC

90

Jun 13

Using export controls to cut access to Fable 5 globally actually has a weird precedent. In the 1990s encryption software was classified as munitions and had the same export controls. The result? slowed US competitiveness until the controls were relaxed. Same thing will happen here.

en.wikipedia.org/wiki/Crypto…

161

Jun 12

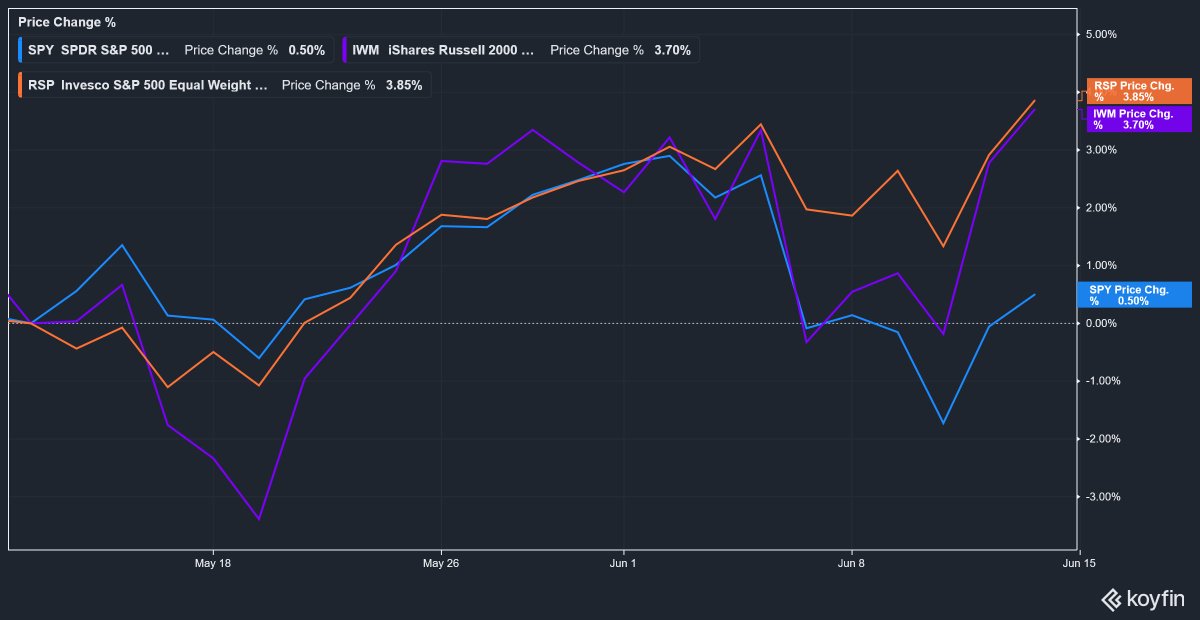

Interesting that the equal weight SP500 and Russell 2k outperformed again today. Small Caps in particular are having a good start to the year. Mega Cap tech might be stealing the headlines, but the small guys are doing okay.

Not investment advice.

174

Jun 12

All eyes will be on the spaceX IPO but I will be interested to see how equal weight SP500 and Russel 2k do today. Yesterday saw the Russell up big, be interested to see if small caps keep rallying along side large cap tech, or if we see a divergence

159

Jun 11

Tech lead the rebound today, but the equal-weight SP500 held up reasonably well against the normal cap weighted (1.61% for equal weighted vrs 1.75% market cap) Small caps in particular had strength with Russel 2k up almost 3%. Good to see more than just the mega cap tech rally.

124

Jun 11

SpaceX IPO will be all the talk for the next few days. Pricing today at that monster valuation. Love the ambition, but as someone who models DCFs and rNPVs and simulates outcomes using Monte Carlos, I'd kill for their visibility into future cash flows. High Growth at this scale is rare. Even if people don't want to admit Price does matter when buying stocks. first quarterly report in September should start to give some clarity of how much substance there is under the hype.

108

$HRMY deep dive dropping tomorrow.

A profitable biotech with a near-$1B drug, net cash, and multiple Phase 3 programs — yet trading at ~11x earnings.

I break down the 2030 patent cliff, the pipeline optionality, full DCF rNPV assumptions, and a 100k-run Monte Carlo.

Full analysis on my profile (Substack pinned).

I'm long. Not investment advice just for entertainment.

128

May payrolls came in at 172k (vs ~85k expected), with sizable upward revisions to prior months. This points to a resilient labor market and supports higher-for-longer rates. Result: elevated discount/hurdle rates for long-duration tech bets. Makes the risk-adjusted return math harder for tech. $NVDA $AVGO $MU

1

103

$QUIK is up ~274% in a year on a real defense story. The tech is legit. The price is not.

No position in $QUIK. Won't trade 72hrs after posting. Analysis not advice. DYOR. This post is not investment advice.

I built the model before chasing the chart, and the math says the market is paying for a near-perfect outcome the numbers do not support. Here is the financial case.

WHAT THE COMPANY IS

A fabless semiconductor shop that licenses embedded FPGA blocks as silicon-proven Hard IP, and is now launching its own radiation-hardened FPGA products for defense and space. It holds one genuinely rare asset: the first and only eFPGA Hard IP on Intel 18A, the leading-edge US foundry node.

THE Q1 2026 PRINT (reported May 12)

Revenue $5.05M, up 16.8% YoY and 35% sequentially

New products 85% of sales

GAAP gross margin 36.5%

GAAP net loss $2.2M, or -$0.13

Non-GAAP loss $0.08, missed the ~$0.05 estimate

The revenue beat was small, the loss ran wide, and margin compressed year over year as mix shifted toward early product.

THE NUMBER NOBODY IS WATCHING

Cash fell to $6.0M, from $18.8M at year end. There is a $125M shelf and a $20M at-the-market program sitting over the stock. For a company burning roughly $2M a quarter, dilution is not a tail risk. It is the likely funding path for the next phase.

WHY NOT A NORMAL DCF

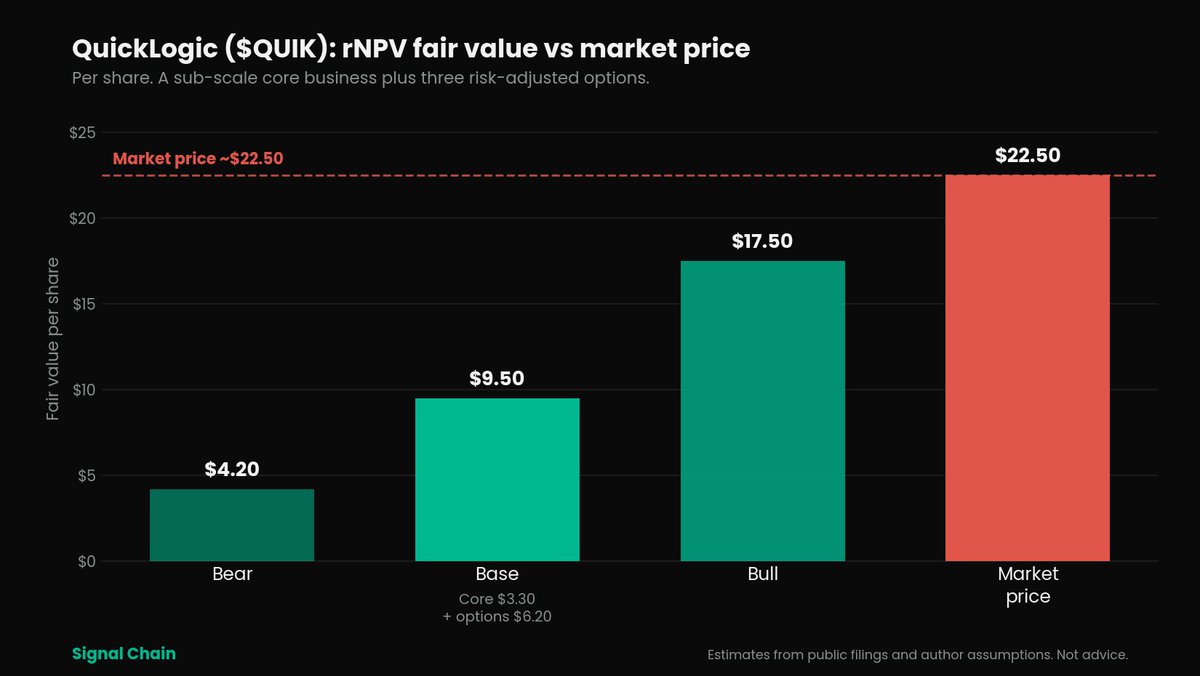

The core eFPGA and licensing business does not earn enough to cover its own ~$16M operating expense base. A standard five-year DCF just burns cash and buries every heroic assumption in terminal value. So I valued it the honest way, as a core business plus three separate call options, risk-adjusted. An rNPV.

THE rNPV (all discounted at 14%)

Core business: ~$60M, or about $3.30 per share

Storefront rad-hard products, 35% odds: ~$42M

Intel 18A first-mover position, 30% odds: ~$45M

SRH government expansion, 45% odds: ~$27M

Base case ~$9.50. Bull ~$17.50. Bear ~$4.20. The stock is at ~$22.50, above even the bull case.

A Graph of the rNPV is attached to this post.

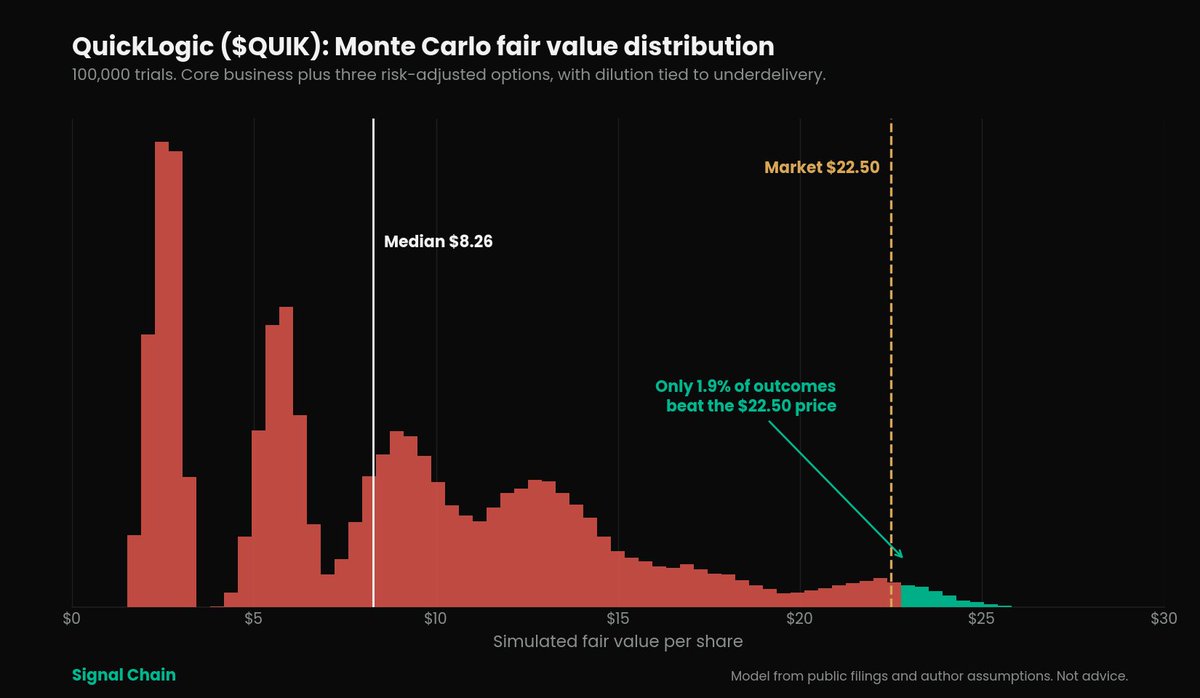

THE MONTE CARLO (100,000 runs)

I stress-tested it, letting each option hit or miss and each payoff vary, with dilution rising as options miss.

Median outcome: $8.26

Below $5: 27% of the time

Above the $22.50 market price: just 1.9%

That last number is the whole thesis. Across 100,000 runs of a model that gives QuickLogic full credit for three real options, only 1.9% of outcomes justify today's price. The market is not buying the middle of this distribution. It is buying the far right tail.

A graph of the Monte Carlo is attached to this post.

THE HONEST READ

The grounded analysts agree with the base case. Oppenheimer sits at $11. The low-$20s targets only moved up after the stock did, not before.

Real tech, a defensible niche, and a rare Intel 18A edge I respect. But the core does not self-fund, the entire equity value is a stack of options, and dilution is the plan rather than the risk. Fair value lands near $9.50. I would own this at $8 to $12. At $22.50 you are not buying a business, you are buying a clean sweep.

No position. Watching for a better entry.

Full breakdown is on my Substack: what an eFPGA actually is, how radiation flips a bit and why rad-hardening is hard, the Intel 18A angle, the complete rNPV and Monte Carlo, and every risk. Link on my profile.

Not investment advice, only for entertainment.

1

450

Quick overview on x86 vs ARM as $NVDA jumps into cpus.

x86 is CISC, complex variable length instructions built for raw single thread muscle and decades of backwards compatible.

ARM is RISC lean fixed length instructions built for performance per watt. That is why it owns mobile and is climbing into laptops and servers.

Driver support is the wild card. On a platform where owner controls the stack like servers or embedded no problem. On desktop where closed kernel mode drivers cannot be emulated like user space apps driver support is still a wildcard.

150

May 29

Huawei's new tau scaling law tries to tie chip progress to cutting signal delay instead of shrinking transistors. Its got real engineering behind the idea but LogicFolding (stacking logic to shorten RC path) is just existing 3D playback with a new name, not the death of Moore's.

95

May 28

$QUIK is up around 275% in a year on a real defense story. eFPGA, radiation hardened FPGA, only eFPGA on Intel 18A.

So I built the model, and a normal DFC completely falls apart on this.

Full breakdown and the DFC fix, Tuesday 6/2

Not investment advice. DYOR

111

May 27

Full deep dive with all 6 tables, MTJ stack breakdown, full sensitivity grid, and the technical section on why MRAM manufacturing is hard on my substack.

Disclosure: no position in $MRAM, no position in tickers mentioned. This is just for entertainment purposes and is not advice.

1

79