Geopolitics is our ecosystem. We are present in every global movement. Because we are Simpsons

Joined March 2010

- Tweets 24,518

- Following 228

- Followers 1,133

- Likes 2,575

3,553 Photos and videos

Pinned Tweet

Sudah telat dirimu kalo mau bermain di minyak, sekarang turunkan kembali harga pertamax!

kau ini bikin sengsara rakyat saja @prabowo @gibran_tweet GIBRAN TOLOL, gak berguna jadi wapres!

Ayo lengserkan JOKOWI

pokoknya kalo wanita-wanita indonesia sudah kesal, akupun ikut kesal

29 Sep 2025

Kenapa motor di Malaysia jarang yang rusak? Karena motor mereka mengonsumsi RON oktan 95, dengan harga Rp 7.800/Liter.

Sedangkan Indonesia? Motor dan Mobil mengisi Pertalite, dengan nilai RON 90. harganya saja lebih tinggi dibanding RON 95 Malaysia!

40

gua udah ingetin dari 2025 loh padahal, dasar goblok @prabowo lo emang gagal jadi presiden ga bisa baca situasi

17 Feb 2025

🚨🇮🇩 PERINGATAN DARURAT

• Negara harus menghapus Pertalite!

• Naikkan harga Pertamax

1

57

@prabowo sekarang turunkan pertamax! jangan jadi mafia deh.

pakai segala alasan saja minyak naik, gua udah bilang naikin pertamax tahun 2025, kenapa tahun 2026 baru dinaikin, dasar guwendeng!

mending lengser aja deh, bebal jadi presiden! gibran juga lengser saja!

1

37

jadi skemanya di 2025

2025 : lo naikin pertamax hapus pertalite

2026 : lo turunkan harga pertamax

jika udah cuan di 2025, market akan heran dengan kondisi indonesia 2026, indonesia langsung diburu investor global

tapi lo ga denger juga, dasar guwendeng! mbg melulu si

39

🚨 Terbukti kan? Gue Gitu Loh! Pertamax harusnya ga naik gais, itu akal-akalan aja. Kelas menengah sudah dapat beban hidup yang parah loh! ditambah pertamax naik haduhh

Mar 25

Antrian kapal-kapal di selat hormuz, Apakah Indonesia kena dampaknya? Pret. Bullshit itu, agar BBM bisa naik dan orang-orang swasta cuan lewat minyak. hahaha

9

mereka lebih tertarik bonds jepang kayaknya daripada melipir ke emiten IHSG, coba lihat nanti

- Anggaran MBG di pangkas

- Iran dan US permanen deal

- saham US dan saham asia kompak menguat

- Harga minyak brent turun 4%

- Rupiah menguat 17.779

- IHSG mulai net buy asing

Prakiraan IHSG close menguat

- Nyaman buat trading

- mulai avg down saham kesayangan

Disclaimer on

43

24 Feb 2022

PLAN LONG TERM :

1. Peperangan terjadi

2. Saham anjlok

3. Web3 Launch

4. Retail sadar crypto

5. Dunia beralih ke crypto

6. Dunia memakai listrik

7. Uang kertas akan tidak bernilai

8. Desentralisasi full

9. Emas akan bernilai tinggi

10. Banyak org berbondong² masuk islam.

2

1

point number 7 👇🏼

Not impossible, but definitely requires factories on the Moon and Mars to achieve.

By then, I don’t think dollars will be used as currency. Just mass and energy.

37

RT @SimpsonsCapital: PLAN LONG TERM :

1. Peperangan terjadi

2. Saham anjlok

3. Web3 Launch

4. Retail sadar crypto

5. Dunia beralih ke crypt…

1

🚨 The G7 is set to release its oil reserves

The question is: why does Prabowo still need to go to Russia if everything is already falling?

31

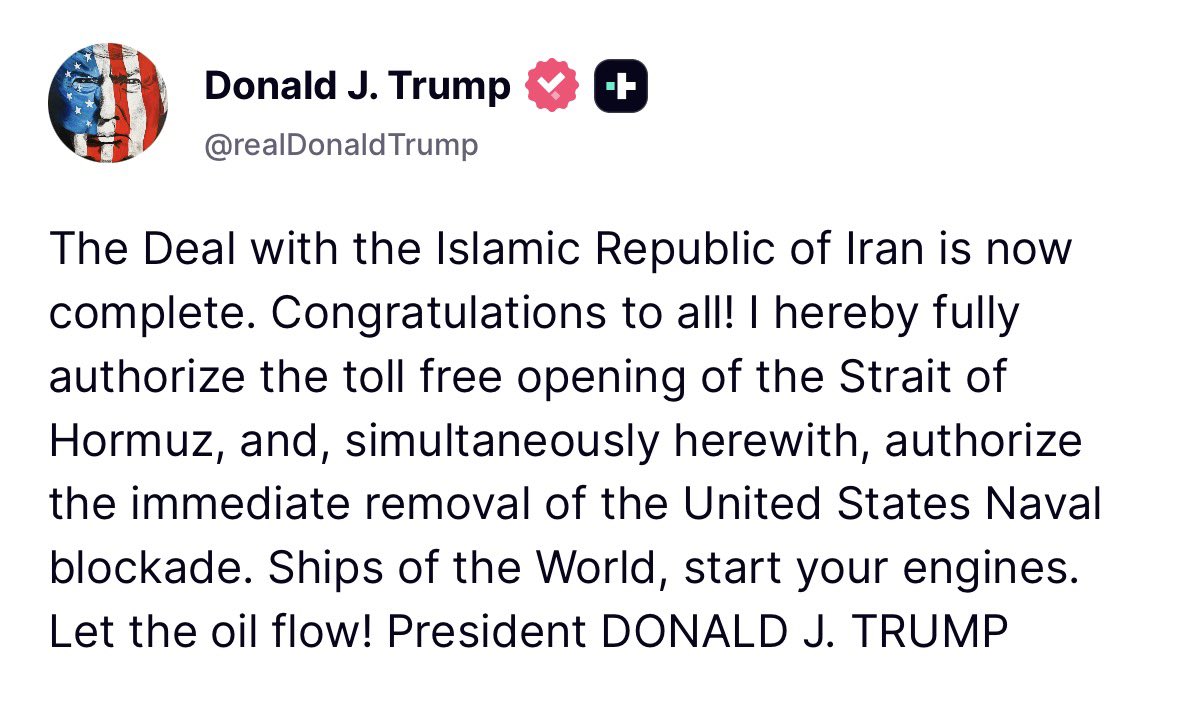

🚨 At a time when the U.S. and Iran are making peace, gold is rising alongside Bitcoin.

The question is: has gold become a trend among investors?

Have stocks become something investors fear? This is changing the trend. It is very rare to see this happen

🟢 IHSG akan Naik, Karena USA dan IRAN damai. Selat Hormuz kembali di buka

Tetapi kalau IHSG nanti anjlok, Pasti ada yang bermain! dan pemain itu sangat amat besar 😂

55

🟢 IHSG akan Naik, Karena USA dan IRAN damai. Selat Hormuz kembali di buka

Tetapi kalau IHSG nanti anjlok, Pasti ada yang bermain! dan pemain itu sangat amat besar 😂

135

⚠️ Bitcoin akan naik, Minyak dunia turun. Gas LNG masih simpang siur,

batubara akan turun, sawit tunggu el-nino juli-agustus. DYOR

“The Deal with Islamic Republic of Iran is now complete. Congratulations to all!” President Donald J. Trump 🇺🇸

50

indonesia tidak menjalin hubungan diplomatik, tapi menjalin hubungan rahasia. jadi, kalian harusnya tau siapa yang lebih dahulu maju untuk memulangkan sandera WNI di israel, beberapa bulan kemarin

17

but your not human

9

🚨 Dark Clouds Over the Mines: Why Coal Is Poised for a Long Bearish Phase in H2 2026

By: @SimpsonsCapital | June 2026

Although spot coal prices briefly climbed to USD 148/ton in early June 2026, savvy investors should not be misled by this short-term rally. Beneath the daily volatility, the foundations of the coal market are cracking. A combination of full implementation of European carbon taxes, stagnating demand in China, and a flood of cheap natural gas is creating a perfect storm ready to push coal prices into a structural downtrend starting in Q3 2026 through 2027

Here are four fundamental reasons why coal will lose its appeal

1. The EU CBAM Gateway Officially Opens

Since January 1, 2026, the European Union has fully implemented the Carbon Border Adjustment Mechanism (CBAM). This is no longer just talk or a transition period; it is a real cost. Exporters of steel, cement, and electricity from coal-based countries must now purchase expensive carbon certificates. As a result, thermal coal imports in Western Europe are projected to plummet by 15-20% throughout 2026. With the loss of one of the world's largest premium buyers, supply surplus will flow into Asia, pressing global spot prices down to the break-even point for high-cost producers

2. The Illusion of Chinese Demand: A Short-Term False Rebound

Many market participants are hoping for a rebound in Chinese electricity demand in 2026. However, data shows that the 2% rise in China's CO2 emissions in Q1 2026 was more due to grid inefficiencies and renewable energy curtailment than healthy industrial growth. The reality is that the Chinese government is increasingly aggressive in shutting down old coal-fired power plants (<300 MW) to meet its Dual Carbon targets. A major warning sign is that if Chinese industrial production slows due to a global economic slowdown, coal demand will fall faster than expected. Stockpiles at major ports like Qinhuangdao are beginning to accumulate, a classic sign that supply exceeds real offtake

3. Natural Gas Returns to Cheap Levels: The Threat of Mass Substitution

Global natural gas (LNG) prices are stabilizing and even dropping in some major hubs by mid-2026. When the price spread between gas and coal narrows, power plants in Europe and Southeast Asia will return to fuel switching toward gas because it is cleaner and now more competitively priced in terms of operational costs. This creates a domino effect where coal loses its role as the savior during energy crises. Without a crisis premium, coal is simply a dirty commodity that is increasingly shunned

4. Financial Pressure: Capital Doors Shut Tight

2026 is the year when global green taxonomies become increasingly exclusive. Major banks and financial institutions have almost completely stopped financing new coal projects. Consequently, coal stocks are experiencing P/E compression. Institutional investors are shifting their funds to green technology and AI sectors, leaving the fossil fuel energy sector in a long-term distribution phase

Conclusion: Time to Exit Before It Is Too Late

The classic bearish coal pattern is forming: prices stagnate at the peak, inventories pile up, Chinese demand weakens, and prices crash. For traders and investors, the price rally in June 2026 should be used as an exit opportunity, not an entry point. With regulatory pressure from CBAM just beginning and IEA projections showing global demand flattening or declining, the downside risk is far greater than the upside potential. Coal may not be dead today, but its glory days are over. The market is moving toward an era where coal is no longer the king of energy, but a stranded asset waiting for its time to retire

Disclaimer: This article is an analysis based on policy trends and market data up to June 2026. Investment decisions remain the responsibility of each individual

1

73

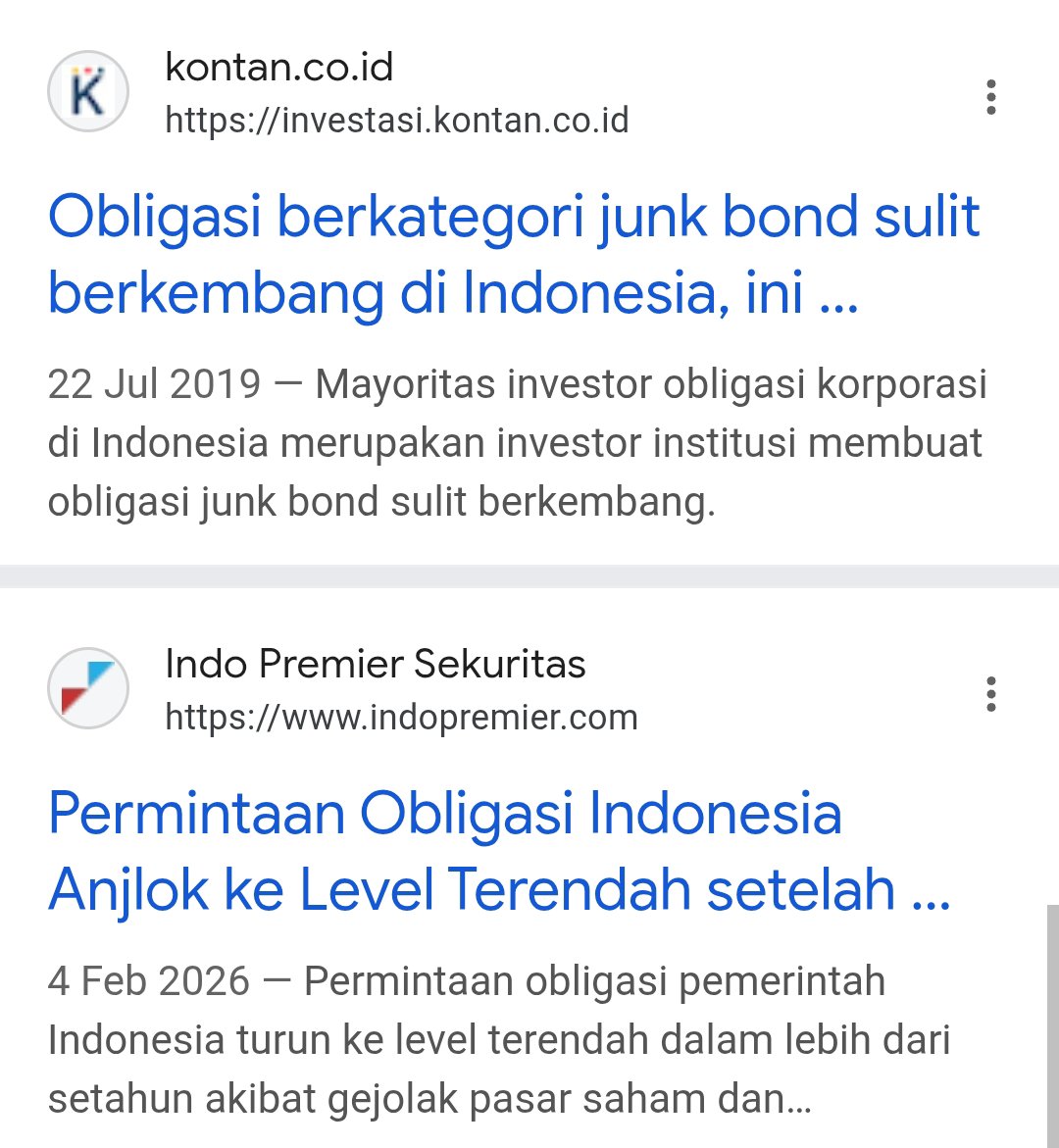

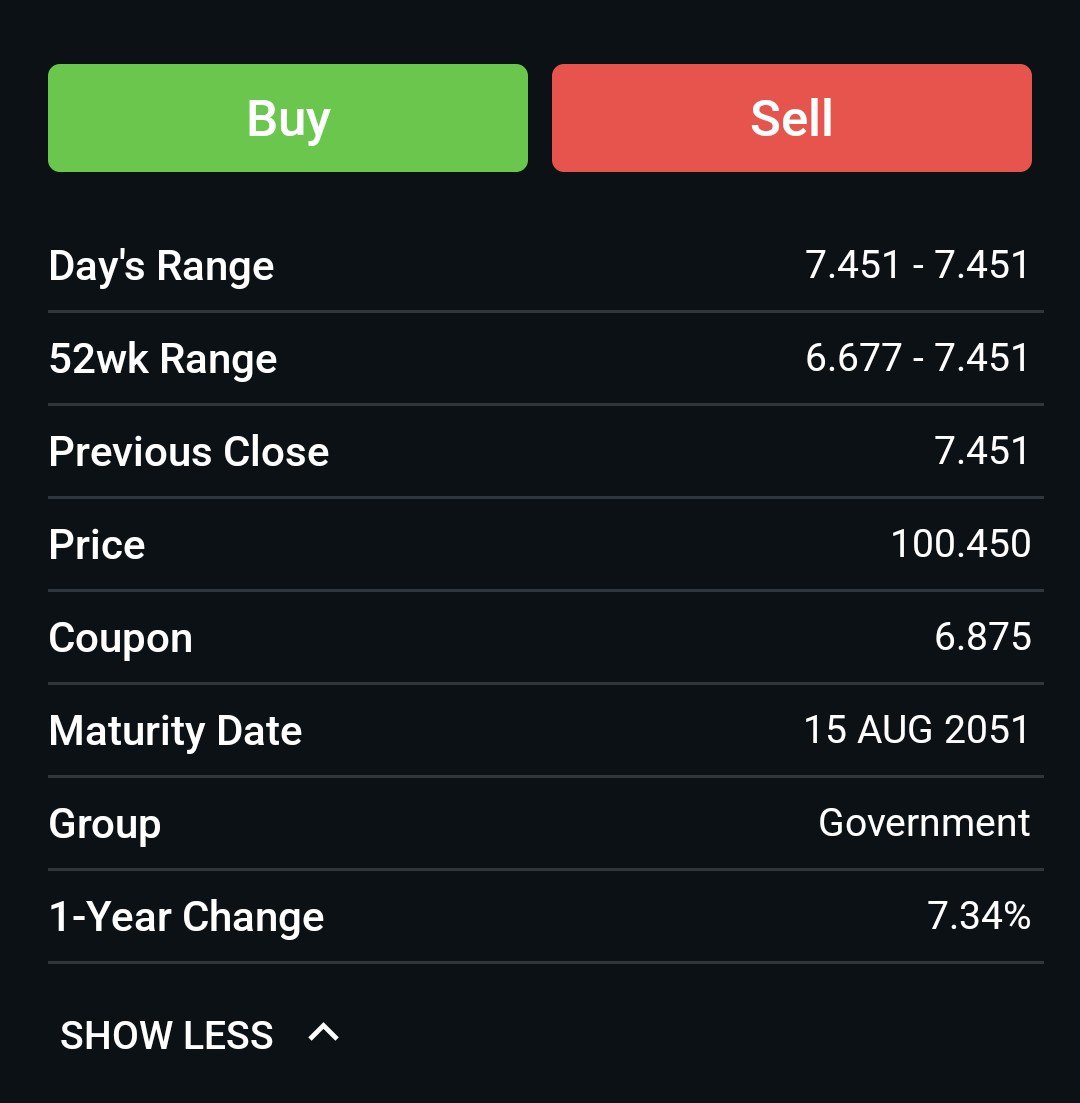

emang obligasi ga laku sampai harus danantara yang bermain? kasihan banget ya, banyak keliling luar negeri tapi ga bisa ngundang investor global masuk Bonds 30 tahunan

jika mereka optimis dgn kondisi indonesia. bonds 30 tahunan laku keras.. kok ini tidak? artinya jokowi mencret

Jun 13

Karena rating kita BBB sementara US AA , jadi memang harus lebih tinggi

1

98

Revisi : ternyata sudah laku obligasi 30 tahunan, tapi kok rupiah masih anjlok? aneh sekali ya. udah ditambal masih ga bisa juga, ow ow ow sangat disayangkan ow ow ow prabowo dan gibran ow ow ow

Prabowo menambahkan hutang obligasi 30 tahunan Indonesia tahun 2026

sebuah sajak

Di balik sorak-sorai pesta pora obligasi 30 tahunan yang laris manis, Rupiah justru merayap mati perlahan di lantai basah berlumur darah, para investor asing menari riang di atas bangkai mata uang rupiah, sementara utang triliunan itu bukan penyelamat, melainkan rantai berkarat yang semakin mencekik leher negeri ini hingga napas terakhirnya pada tahun 2051

sementara rupiah masih anjlok, meskipun negara sudah ditambal kanan kiri atas bawah hahaha

62

Prabowo menambahkan hutang obligasi 30 tahunan Indonesia tahun 2026

sebuah sajak

Di balik sorak-sorai pesta pora obligasi 30 tahunan yang laris manis, Rupiah justru merayap mati perlahan di lantai basah berlumur darah, para investor asing menari riang di atas bangkai mata uang rupiah, sementara utang triliunan itu bukan penyelamat, melainkan rantai berkarat yang semakin mencekik leher negeri ini hingga napas terakhirnya pada tahun 2051

sementara rupiah masih anjlok, meskipun negara sudah ditambal kanan kiri atas bawah hahaha

121