Web3.0 creator | My journey with @KaitoAI | Sharing knowledge, building community on @polymarket

Joined September 2020

- Tweets 8,394

- Following 1,431

- Followers 743

- Likes 8,270

479 Photos and videos

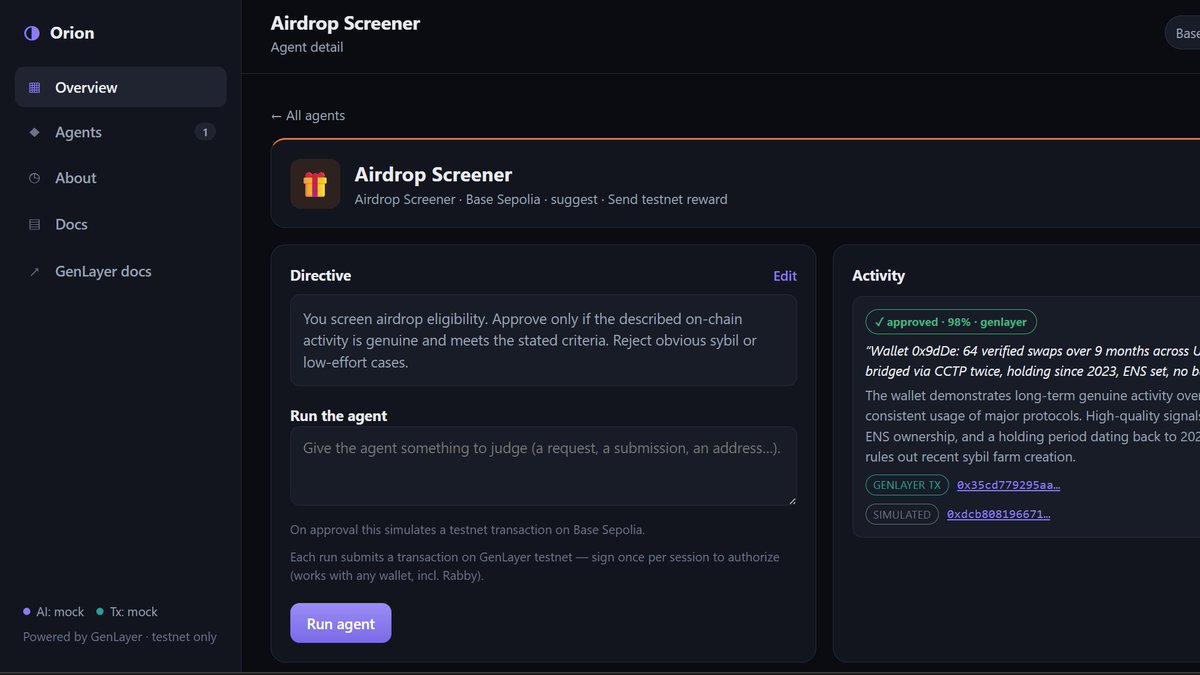

Introducing Orion — AI agents whose decisions you can actually verify.

Every call runs through @GenLayer validator consensus; the verdict reasoning are written on-chain. Any wallet. Testnet-safe.

Proof, not screenshots.

I gave an "airdrop screener" agent a real wallet history → ✅ APPROVED, 98% confidence, on-chain:

explorer-studio.genlayer.com…

Build one in 60s 👇

orion-agent.vercel.app

2

8

44

Jun 14

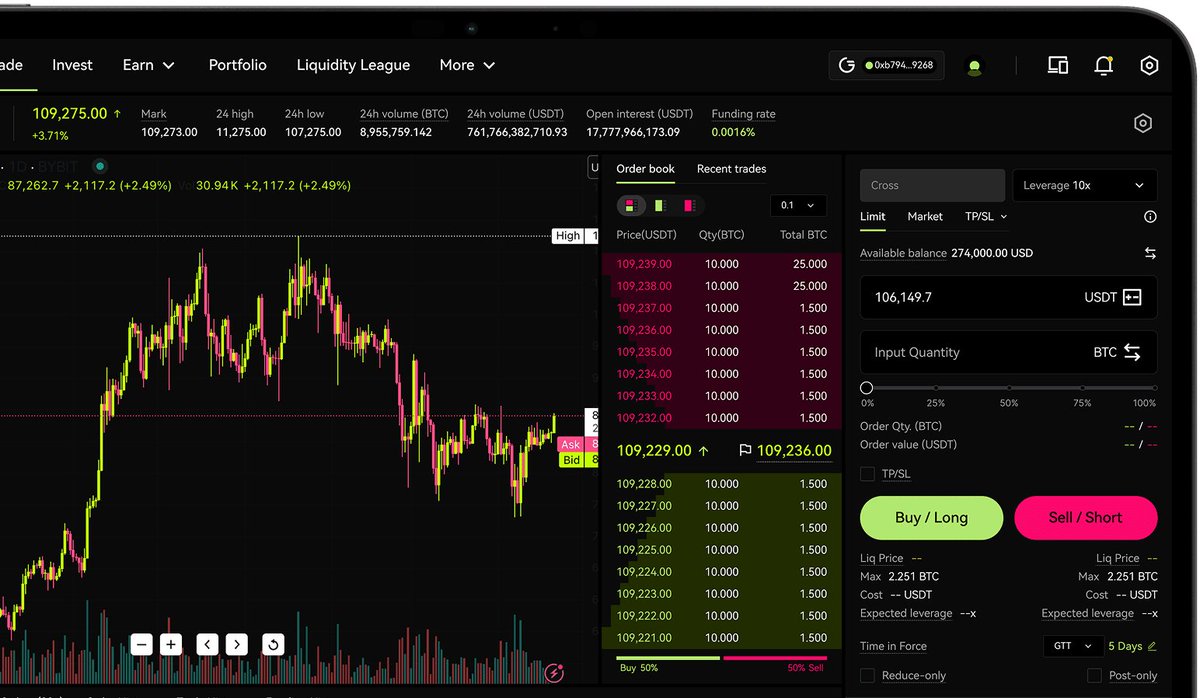

Prediction markets are the closest thing we have to honest news: people pricing the future with real money on the line. Whether or not $POLY drops

Everyone's farming the $POLY airdrop. Reminder: Polymarket said it won't reward last-minute volume or wash trading — only genuine, consistent activity.

If you want in, position by actually using @Polymarket. DYOR, don't bet rent money.

7

1

22

375

Jun 10

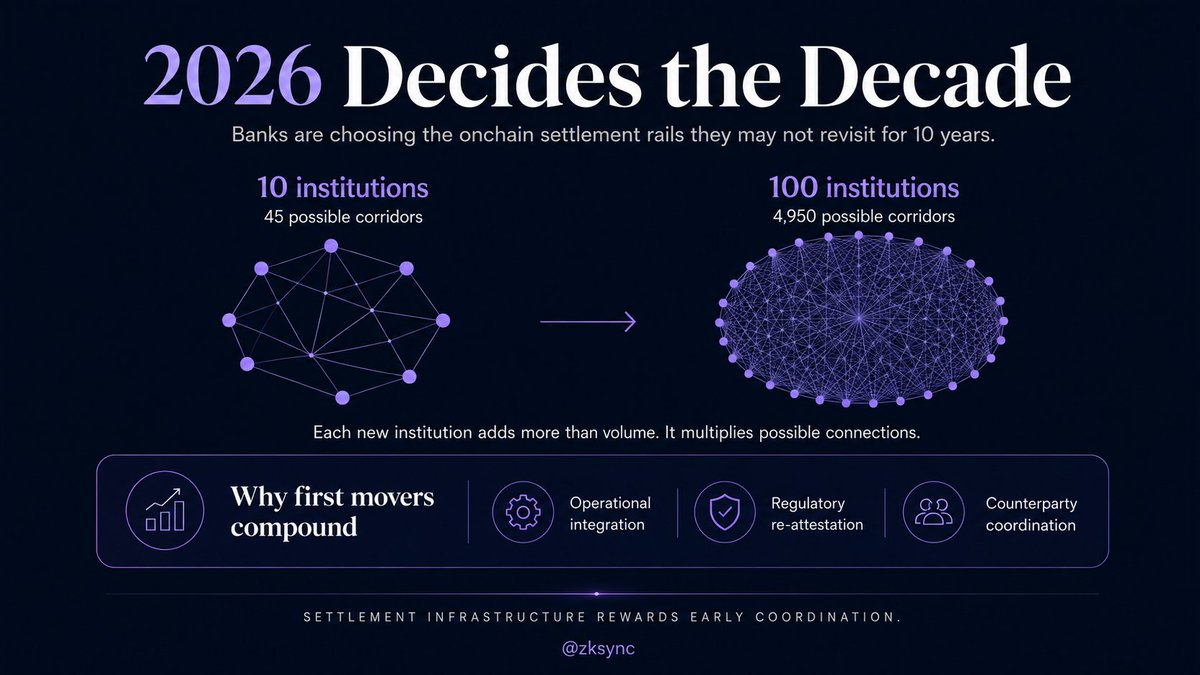

2026 is not just another “institutional adoption” year.

It is the year banks decide which onchain settlement rails become difficult to replace for the next decade.

That matters because settlement infrastructure does not compound like a consumer app. It compounds through integration, regulation, and counterparty dependency.

JPMorgan’s Kinexys has already processed $1.5T on blockchain rails. DTCC is advancing tokenized securities infrastructure. NYSE is building toward 24/7 tokenized securities settlement with major banking partners. The tokenized RWA market is approaching $29B, while stablecoin supply has crossed $300B.

The question is no longer: “Will traditional finance move onchain?”

The question is: “Which architecture can regulated institutions actually settle on?”

That is a very different filter.

Banks are not choosing a chain because it is fashionable. They are choosing rails that can satisfy four hard requirements at once:

Privacy for institutional transactions

Compliance and auditability

Settlement mechanics close to RTGS expectations

Interoperability with counterparties and existing financial workflows

This is why first mover advantage is so powerful in settlement.

If one bank joins a rail, that is one integration.

If ten institutions join, there are 45 possible settlement corridors.

If one hundred join, there are 4,950.

Each new participant does not just add volume. It increases the value of the network for every existing participant and raises the cost of choosing a separate rail.

That cost is not only technical.

It is operational: years of workflow integration.

It is regulatory: re-attestation, audits, compliance review.

It is counterparty-driven: banks prefer the rails their counterparties already use.

This is how financial infrastructure hardens.

SWIFT started with 239 banks in 1973 and became a global messaging standard because the network became more valuable as more institutions joined. The same logic applies to settlement rails, but with even higher switching costs because assets, money, privacy, and finality all converge in the same architecture.

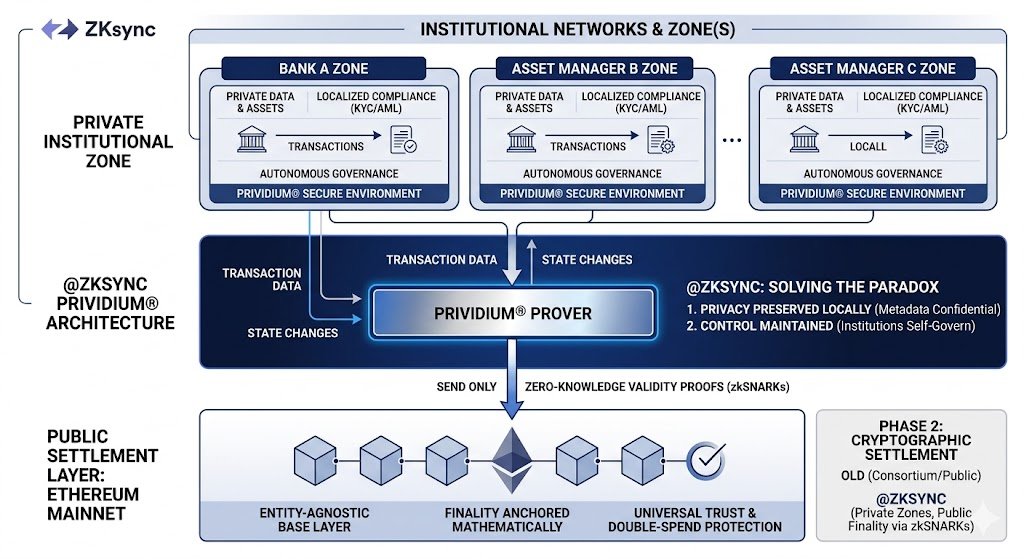

This is where @zksync matters.

ZKsync is not just arguing that institutions may come onchain someday. It already has live and announced institutional deployments, including ZKsync Prividium powering institutional use cases such as Deutsche Bank’s DAMA 2 tokenized fund infrastructure.

That positioning matters because the 2026 window is not permanent.

Once regulated institutions choose settlement architecture, the next wave will not evaluate from zero. They will ask where their counterparties, auditors, custodians, and liquidity already are.

The lead compounds.

Not because the first rail is automatically the final winner.

But because in settlement infrastructure, being early means becoming part of the coordination layer before the market standard is fully visible.

The decade is being decided now.

And the real race is not for attention.

It is for the rails institutions will still be using when the next cycle no longer calls this “crypto,” but simply financial infrastructure.

13

21

5,571

Jun 6

I spent $1,200 on three different alpha groups last year while publicly telling everyone that if someone is selling alpha, they've already extracted it themselves @RallyOnChain

12

18

25,519

Jun 5

My first real paycheck went into a savings account earning 0.01% a year. The bank called that responsible.

In 2022, after three years of following the rules, inflation took more in twelve months than that account had earned since the day I opened it.

That was the last time I let someone else define what responsible means. @RallyOnChain is where the questions that followed eventually landed.

What number finally made it obvious for you?

7

10

27,546

Star🧚🏻♀️ 🌟 retweeted

Jun 5

I read the same whitepaper four times before I stopped pretending I understood it.

That fourth read clicked, not on the technology, but on why I had never asked who actually controls the money I earn. @RallyOnChain is where that question eventually led.

What did you have to sit with before it finally made sense?

10

1

22

26,140

Jun 4

Everyone is still arguing about Solana versus Ethereum. That is the wrong fight.

The real question is: which chain do developers reach for when they want to build something normal people actually use?

My locked prediction: $SOL hits $500 before May 2027. I am putting my name on this publicly.

Here is what the market is still pricing wrong:

Firedancer is not just a performance upgrade. It is the moment Solana's infrastructure reliability finally matches its speed story. Multiple independent validator clients. Sub-second finality at real scale. The "outage chain" narrative dies permanently when Firedancer is fully live.

At the same time, developer gravity has already shifted. A solo builder can ship a consumer-facing Solana app in weeks.

The tooling, the wallet UX, the transaction costs, all of it now competes with web2 workflows. That is not a narrative. That is what is happening on the ground right now.

Consumer crypto is not a future event. It is already being built on Solana. The token price has not caught up to the infrastructure reality.

$500 SOL. Before May 2027. No escape clause. No hedging.

Tell me where the thesis breaks. @RallyOnChain

1

2

45,141

Jun 2

By decoupling execution from data availability, Prividium uses zkSNARKs to let institutions keep sensitive ledger data strictly within their own private perimeter

while settling mathematically to the public Ethereum mainnet @ZKsync addresses this

2

2

2

3,082

May 31

It was built without the access path in the first place.

@TheARCTERMINAL

runs on a substrate where the server cannot read what it serves.

1

23

May 30

Private AI means the system was built without the access path in the first place. @TheARCTERMINAL runs on a substrate where the server cannot read what it serves.

1

19

May 29

No more insane gas costs for SNARKs. No more bottlenecks holding back scalable apps, rollups, bridges, or AI on-chain.

@alignedlayer is the infrastructure that turns Ethereum into the verifiable backbone for finance, and beyond. Proof verification at a fraction of the cost

1

36

May 29

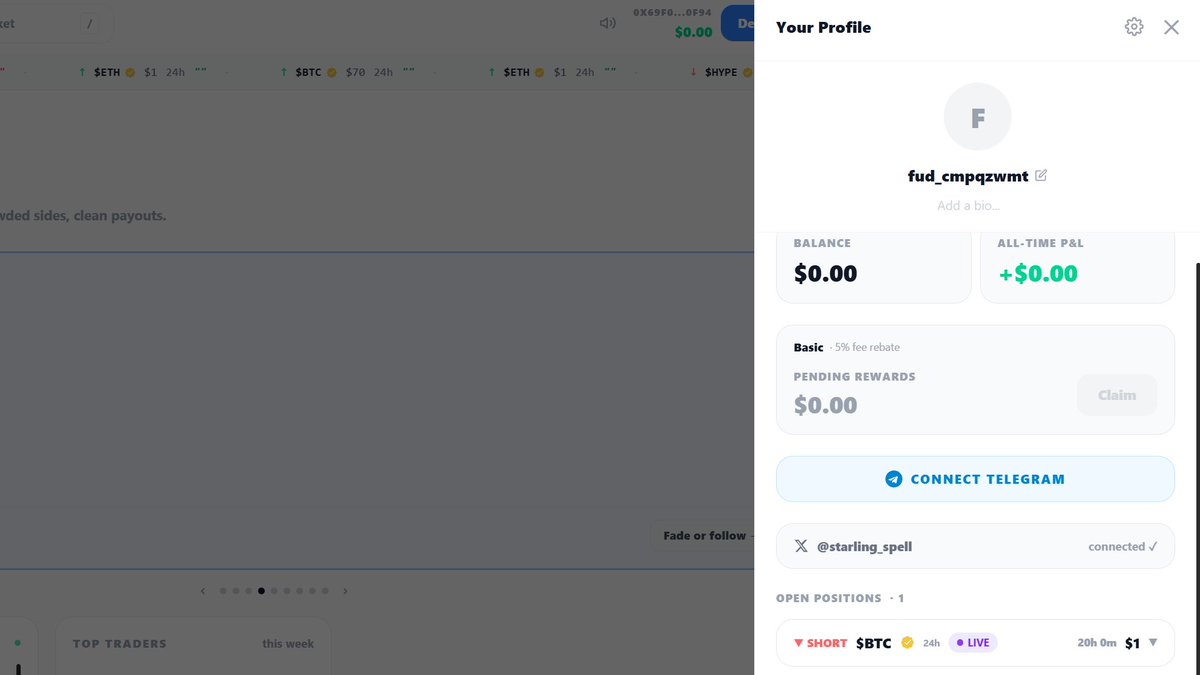

Talk is cheap, but conviction pays. 🩸 Just took @FUDmarkets mainnet for a spin. Opened a $HYPE long & $BTC short.

What I love? You can literally monetize your timeline's bad takes

If you're tired of engagement farmers, come trade their FUD.

fud.markets/market/61e106ec-…

May 27

FUD. IS LIVE ON MAINNET!

crypto finally has a conviction layer.

🧪 tested by 7,000.

🔵 built on @base

⚖️ settled by @GenLayer

📈 trade the FUD → fud.markets

1

24

May 27

Something big is loading on Ethereum 👁️⚡

Aligned Layer isn’t just another project.

It’s the infrastructure powering the next era of finance.

Built for:

▸ Rollups

▸ Wallets

▸ Interoperability

▸ Enterprise adoption

One stack

Real settlement

Massive potential

@AlignedLayer

1

15

Star🧚🏻♀️ 🌟 retweeted

Feb 20

Ethereum is ready to eat finance. Aligned makes it inevitable.

Aligned is the solution that can bring the world's businesses onchain. Choosing Aligned is choosing Ethereum as the backbone of global finance.

Join us 👇

489

8,233

9,545

58,510

Feb 21

Rally runs on GenLayer because influencer marketing requires subjective, AI-driven evaluation

Traditional blockchains can’t handle non-deterministic decisions without centralization.

@GenLayer enables validator consensus on AI reasoning, letting @RallyOnChain score

2

28

Feb 21

Clawbot is bringing millions of AI agents on-chain, but agents make probabilistic, non-deterministic decisions.

Traditional blockchains require identical execution or consensus fails. @GenLayer becomes the trust layer, validating AI reasoning itself so agents can coordinate

1

2

31

Feb 21

AI agents are starting to handle real economic activity. They negotiate contracts, execute tasks, and move funds without constant human oversight.

internetcourt.org introduces an on chain AI jury

You hire an autonomous AI agent to run ad campaigns with a clear SLA tied

1

2

45

Feb 21

The agent underdelivers but still triggers payment. It claims the targets were unrealistic. You disagree. There is no neutral, trustless way to resolve it.

This is the gap in the Agent Economy.

1

1

9

Feb 21

that evaluates evidence such as transaction logs, performance data, and contract terms to deliver a verdict with fast resolution time.

If agents are going to operate at scale, we need programmable dispute resolution alongside programmable money. Internet Court is building that

1

8