Joined March 2022

- Tweets 20,039

- Following 564

- Followers 664

- Likes 62,680

2,115 Photos and videos

Pinned Tweet

I've spent 40h during last 4 days in @ElderScrolls Skyrim. Most of that was because I was trying to apply all the mods from @NexusSites. Nevertheless, it's great time to be alive 😂.

31

Ludvík Stichenwirth retweeted

🚨 Wth?! 😱

An older spectator caused a seriously dangerous incident today at #SaarlandTrofeoJuniors by trying to get a better look and entering the course with her rollator while riders were flying past at full speed!

#LVMSaarlandTrofeo #Habkirchen #Saarland #Germany #Cycling

652

959

12,676

3,564,587

Ludvík Stichenwirth retweeted

Jun 12

well that didnt take long

82

87

1,493

44,854

Ludvík Stichenwirth retweeted

Jun 13

Nabiullina?

┓┏┓┏┓┃

┛┗┛┗┛┃\😭/

┓┏┓┏┓┃ /

┛┗┛┗┛┃ ノ)

┓┏┓┏┓┃

┛┗┛┗┛┃

┓┏┓┏┓┃

┛┗┛┗┛┃

┓┏┓┏┓┃

┛┗┛┗┛┃

┓┏┓┏┓┃

┛┗┛┗┛┃

┓┏┓┏┓┃

┛┗┛┗┛┃

┓┏┓┏┓┃

┛┗┛┗┛ |

53

193

2,151

47,557

Ludvík Stichenwirth retweeted

Jun 13

Absolute chaos in Crimea as fuel has totally run out.

Drivers line up for days with no hope of enough to leave the penninsula.

526

4,147

23,846

724,679

Ludvík Stichenwirth retweeted

Jun 13

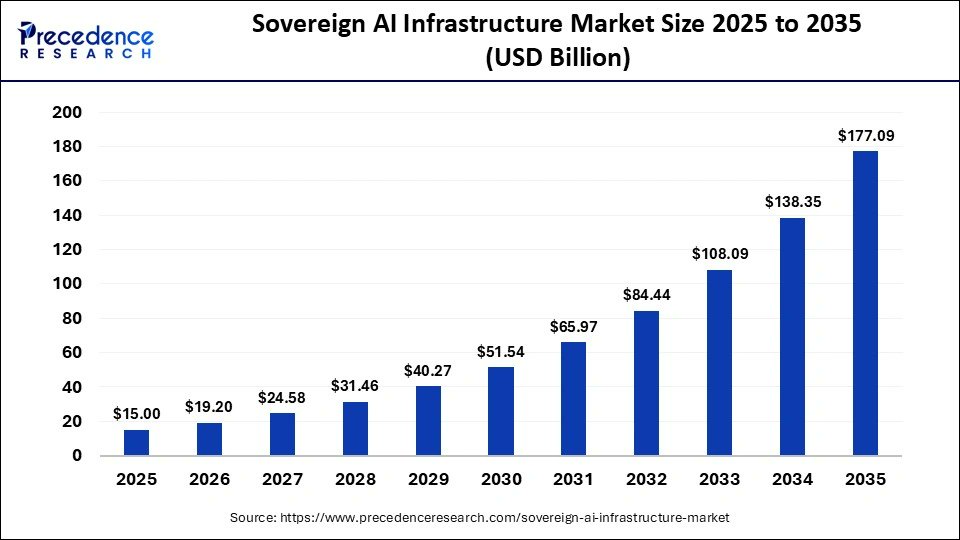

Invest in - "sovereign AI".

As the US keeps tightening export controls on advanced AI chips, technology and recently new frontier models (Fable 5), governments outside the US are realizing they can't depend on AI they don't control.

So they're racing to build their own. That means their own chips, data centers, and models, on their own soil. That's "sovereign AI," and it's become one of the biggest spending trends in tech.

1. The EU is going all in. Through its InvestAI plan, the EU committed €20 billion to build AI gigafactories, each with around 100,000 AI chips, to train Europe's own very large models instead of relying on US companies. They even have a Commissioner for Tech Sovereignty. The whole goal is for Europe to stand on its own as an "AI continent."

2. Australia too. Its National AI Plan pushes sovereign capability, meaning Australian data on Australian controlled infrastructure. Data center investment there is forecast to reach about AU$26 billion by 2030, and giants are piling in, with Microsoft investing A$25 billion and AWS A$20 billion to build local capacity. The same story is forming across the Middle East, India, and Japan.

3. So how does a beginner actually invest in this? The key insight: you don't need to guess which AI model wins. You invest in the "picks and shovels," the companies that build the chips, data centers, and power that every sovereign AI project runs on. They get paid regardless of whose model wins.

4. The simplest, lower risk way is an ETF. Instead of betting on one company, an ETF holds a whole basket.

For this theme, something like the Global X Data Center & Digital Infrastructure ETF $DTCR, which holds data center operators and digital infrastructure names, packages it into one ticker.

VanEck also just launched a data center supply chain ETF $RACK. This is usually the smartest starting point for a beginner.

5. If you want individual names (higher risk, higher reward), think in layers. For chips, there's Nvidia $NVDA, which sells the GPUs to nearly everyone, including the EU, since it has no chip production of its own yet. For the data center and "neocloud" layer, there's the big 3, $IREN Nebius $NBIS, and CoreWeave $CRWV, which build and rent out the actual compute.

6. Why IREN stands out on the sovereign angle.

It has power and data centers across the US, Europe (Spain), and Asia Pacific, the exact regions building sovereign AI. And its recent Mirantis acquisition added the software and Kubernetes orchestration layer that turns raw GPUs into a complete, standalone AI cloud a government or bank can run on its own terms.

> Hardware plus software plus global footprint.

NFA. DYOR.

23

31

249

85,321

Jun 12

Tohle jsem sjel za mlada, teď už to není ono. Ale pořád mám tu vzpomínku.

21

Ludvík Stichenwirth retweeted

Jun 11

If you own or trade $IREN, watch this.

It is trading at what I see as a discount and my Bull Cycle framework still points higher.

In the video I walk through the current setup, why I’m targeting 80 by late summer, and what would change that view.

38

55

817

188,666

Ludvík Stichenwirth retweeted

Již není třeba držet tajemství. Český záložní astronaut ESA Aleš Svoboda (@astro_ales) bude pilotem kosmické lodi Crew Dragon při komerční misi PAM-6. Velitelem mise bude francouzský astronaut ESA Thomas Pesquet. Z evropského pohledu jde o unikátní misi a roli jejich zástupců.

24

102

1,368

28,055

Ludvík Stichenwirth retweeted

Jun 6

🔥 More from Ust-Labutensk oil depot

15

263

2,154

76,463

Ludvík Stichenwirth retweeted

Jun 3

This whole $IREN vs $NBIS argument is actually pretty simple.

If you literally believe $NBIS will become the next AWS which means:

- it becomes a vertically integrated hyperscaler that not only provides next-gen compute GPU clusters but also services the long-tail of customers who just want to plug into an API for open source models and build applications on top of its platform

Then yes, you should invest in Nebius, even at this price.

I don't believe it has enough differentiation from AWS, GCP, Azure. And I fail to see why customers already locked into those contracts will want to take the humongous effort of migrating their entire tech stack to another vendor when open source models also exist on AWS, GCP, Azure.

I also am doubtful a ton of value when migrate to watered-down open source when it's pretty clear all of the value today is largely captured by Claude and then GPT. Keep in mind that if Anthropic / Open AI wanted to distill their models for more efficiency, they could just ... do that.

Also just look around in enterprise:

- nobody who codes use open-source -> it's all Claude or GPT (Meta / Google all use Claude instead of their internal models)

- in enterprise workflows it's really just claude. everywhere.

- the solo-pretreneur might use open source but open source does dominate enterprise. Claude /GPT (mostly Claude) does. Why do you think Open AI / Anthropic are starting to hire all of those FDE's?

Levels of customers:

- layer 1: Hyperscalers - these are the googles, Microsofts, Amazons of the world who just want bare-metal

- layer 2: AI Labs like anthropic open AI, also just mostly want bare metal

- layer 3: Jane Street, FireworksAI, TogetherAI, Tik Tok, Palantir -> Some want bare-metal-like performance with a managed Kubernetes/Slurm layer; some want full managed AI cloud primitives; some might just want pure bare-metal. (Here $CRWV > $NBIS > $IREN)

- layer 4: larger enterprises from finance / tech companies / real estate like JP Morgan to Salesforce to DR Horton. Salesforce uses all of AWS, GCP, Azure. Specifically, it builds a number of applications on top of AWS Sagemaker.

My view is that most of the value will come from layer 1 to layer 3 because the vast majority of the value from layer 4 will be captured by AWS, GCP, Azure.

And since this is my view, $NBIS can be reduced to an infrastructure play. Seems reductive, but I largely think this will be true over the next few years.

And if you view Neoclouds largely as an infrastructure play, then you're better off investing in $IREN.

And because that is my view, no amount of genius mathematician programmer CEO, or mid-tier software engineers will really make a difference will lead to higher-quality infrastructure faster data center development timelines.

I'll also mention that the smartest engineers in the world don't go and say "I want to work for Nebius". They work at these places, in higher to lower talent density (all high):

- anthropic -> today, everyone wants to work here

- open AI

- cursor

- databricks

- fireworks AI

- google

- meta

- stripe

- ramp

- decagon

- etc.

It's actually pretty simple.

You can say your a CEO is a genius at programming, you can say you have smart engineers, you can see Yandex is awesome, you can say you have cool subsidiaries, but it doesn't matter when you're engineers really aren't world-class and when that has nothing to do with your core-business: building real-world infrastructure to power AI workloads.

What has happened so far is that Nebius has done a good job of plugging in GPU's for Microsoft, even if they haven't come from Vineland. I applaud them for that. At the same time I think it's sus this compute is not coming from Vineland.

But that's the easy part of their portfolio. Someone tell me how they will deliver on their backlog when a site like Missouri doesn't even have an interconnect agreement there. Pretty sure this site will have to use BTM to bridge the gap as well. Someone tell me whether paying Data One for colocation and then paying Bloom Energy on top of Data One is a good or bad look.

I'll also be candid here about $IREN:

- they have had some growing pains

- horizon 1 is by far the hardest part of their portfolio because they're improvising as they go

- getting GPU's has been a bitch

- they still have to prove they can scale AI revenue from a meager 33 million last quarter to billions over the course of the next few quarters

- they still have to prove they can deliver and operate liquid cooled datacenters at scale

It's not like $IREN is perfect, but because I have an edge in knowing how the Horizon development is going company roots ability to source long-lead items the genuine differentiation it has with its huge portfolio, I see it as more de-risked from an infrastructure standpoint than Nebius.

For all of these companies - Nebius, Coreweave, Iren, my view is that they should not be evaluated as software companies, but as infrastructure first companies.

It follows that if you don't have an infrastructure first background, then you might win the early game, but you won't win the late game.

Good luck.

$NBIS CBO, Roman Chernin:

Is the growth sustainable longer term? Is there a differentiation between the hyperscalers and $CRWV?

Roman broke it down in to three tiers:

1. Hyperscalers just want broad compute. Just a few

2. AI Labs/Researchers who want to focus on research and training but need some infrastructure. Hundreds to thousands of companies

3. Costumers that don't want to talk clusters. They think in terms of the models they consume and for many reasons they move towards open source specialized models. Thousands to tens of thousands.

4. Solo builders, who need every service & product under the sun.

"We could just have bare metal compute but then it would only be limited to a few customers. We could stay on cloud but could only service hundreds of customers. We could stay on inference but then we can only be limited to tens of thousands. We believe there will be hundreds of thousands of builders and customers and our goal is to meet them there and provide them the services they need."

26

32

274

83,691

Ludvík Stichenwirth retweeted

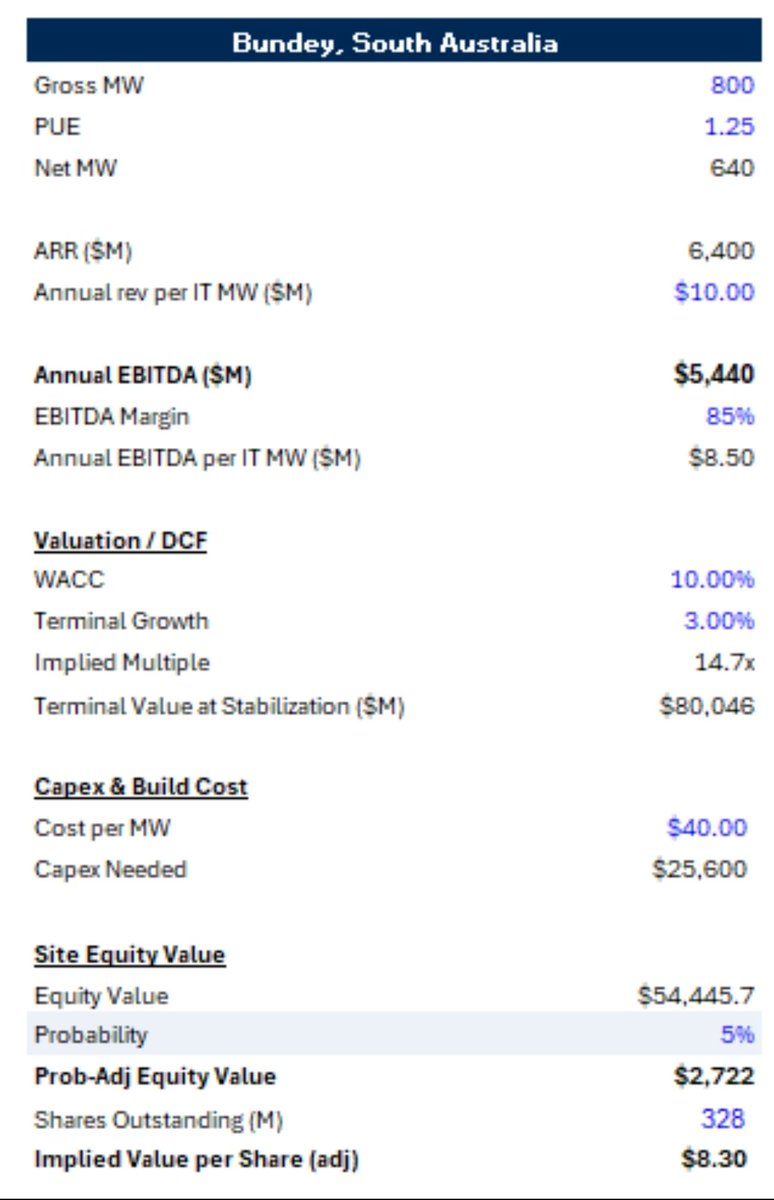

Even with just a 5% probability weighting for this project, we think it's worth $8/share to $IREN at current GPU economics.

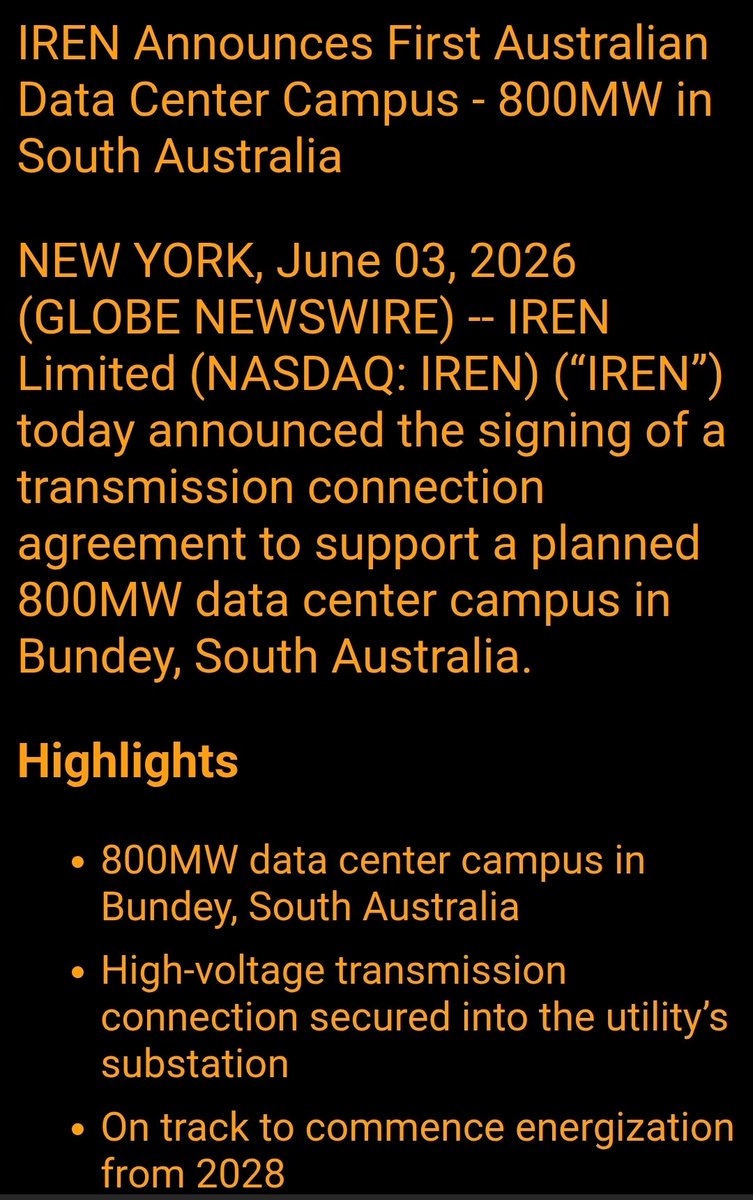

🚨IREN Announces First Australian Data Center Campus: 800MW in South Australia

15

33

300

63,480

Ludvík Stichenwirth retweeted

Jun 3

Good morning. What day is it ??

43

110

2,184

36,949

IREN has announced a planned 800MW data center campus in Bundey, South Australia.

This marks IREN’s first announced Australian data center project and one of the largest in the Asia-Pacific region announced to date.

Learn more: iren.gcs-web.com/static-file…

203

546

3,946

562,150

Ludvík Stichenwirth retweeted

Jun 3

$IREN SIGNS 800MW TRANSMISSION CONNECTION AGREEMENT FOR BUNDEY SOUTH AUSTRALIA DATA CENTER CAMPUS; ENERGIZATION ON TRACK FROM 2028

1

7

55

6,242

Ludvík Stichenwirth retweeted

Jun 1

New Era Energy & Digital ($NUAI): A bull case for an AI-infrastructure story the market is still underestimating

NUAI is a re-rating in progress. A former Permian Basin E&P that has pivoted into large-scale AI/HPC data-center development, the company is systematically retiring the legal and capital-structure overhangs that have kept institutional capital on the sidelines — while the equity still trades closer to the baggage than to the platform underneath it. The setup is the familiar small-cap asymmetry: a genuinely scarce underlying asset priced at a discount to its de-risked value because the market has not yet marked the clean-up to par.

The asset is Texas Critical Data Centers (TCDC), a ~492-acre campus in Ector County, Texas, with ~650 MW of capacity secured and a design that scales toward 1.4 GW. The thesis in one line: management is clearing overhangs faster than the stock has repriced, while assembling the financing, operating, and commercial partnerships needed to convert powered land into contracted, project-financed cash flow. The sections below lay out the de-risking, the platform being built against it, the capital-markets catalysts, the Street's early valuation work — and, in fairness, what has to go right for the gap to close.

The defense: clearing the overhangs

Sharon AI is gone — and paid in cash. The single largest structural overhang was NUAI's partnership obligation to Sharon AI in the TCDC joint venture. That chapter is now closed. NUAI consolidated full ownership of TCDC, and on April 24, 2026 it repaid the remaining $50 million senior secured convertible note to Sharon AI entirely in cash, plus accrued interest — eliminating the conversion-driven dilution that had been hanging over the share count. Total consideration on the buyout came in around $74 million, and crucially, Sharon AI retains no ownership, governance, or control rights in the campus. A messy, two-headed JV became a clean, wholly owned flagship.

The ATW structure has been de-risked. Earlier in the year the company scrapped a planned convertible preferred issuance — exactly the kind of variable-priced instrument that tends to grind small-cap charts lower — in favor of an amended waiver with ATW AI Infrastructure II that reset warrant exercise prices to a fixed $2.00. That converted a potentially toxic, open-ended dilution mechanism into a known, fixed-strike overhang that is now being worked down as warrants are exercised. It is not fully retired — there remain unexercised warrants on the books — but the shape of the dilution is dramatically friendlier than it was, and the worst-case path is off the table.

The New Mexico lawsuit is being settled. On May 28, 2026, the company announced a pending agreement that would dismiss every State of New Mexico claim against New Era — five claims in total — for a $1 million payment to the bankruptcy trustee, subject to court approval. The stock moved double digits in after-hours trading on the news, a sign of just how much the litigation cloud had been weighing on sentiment. This removes the corporate legal overhang that had made many institutions reluctant to underwrite the story.

The offense: building a platform that can execute

Removing overhangs only matters if there's something worth de-risking. Since March, the moves on the offensive side have arguably been more important than the defensive ones:

A real CFO for a capital-intensive business. In March, NUAI brought on Ted Warner as Chief Financial Officer. This is not a generalist hire — Warner ran Northland Capital Markets' Energy, Power and Digital Infrastructure practice, which since 2023 has structured more than $7 billion of financing for large-scale data-center development. For a company whose entire value-creation path runs through project finance and capital partnerships, hiring a banker who has actually closed this exact type of deal is a tell.

Macquarie validated the asset. Also closed in early April: a multi-tranche senior secured term loan credit facility of up to $290 million with Macquarie Group, earmarked for the TCDC flagship. A blue-chip infrastructure lender does not extend a facility of that size against a project it hasn't diligenced. Combined with a $115 million registered equity offering, management reported $80 million-plus in cash as of April 30 — runway to actually execute rather than survive.

The bench is now stacked with hyperscaler-native talent. What had been a thin team is being built out quickly. On June 1, NUAI named Evan Pierce as Chief Development Officer and Michael Johnson as General Counsel and Chief Compliance Officer — and the pedigrees matter as much as the titles. Pierce spent two decades on the customer-and-infrastructure side of this exact business: most recently leading data-center site and energy development for the Americas at EdgeConneX, and before that in energy, utility-engagement and capacity roles at Amazon/AWS and ByteDance, with a hand in planning more than 5 GW of data-center and power infrastructure. NUAI effectively just hired someone who has sat in the hyperscaler's seat and knows exactly how these tenants evaluate sites and procure power.

Johnson, the new GC, arrives from CoreWeave and, before that, Switch — two of the most relevant names in the industry — bringing three decades of data-center leasing, powered-land acquisition, construction and financing experience. Pairing a heavyweight GC with a dedicated compliance mandate also signals a deliberate institutionalization of governance, which is precisely what an investor base wary of the litigation overhang wants to see. You don't recruit people like this to sit idle; you recruit them to paper a lease and build.

A Tier-1 operator and institutional capital are circling — and a hyperscaler appears to be steering. On April 1, NUAI signed a non-binding LOI to form a development-and-financing joint venture for TCDC with Stream Data Centers, a top-tier U.S. data-center operator, alongside an institutional capital partner. New Era contributes site control and local execution, Stream serves as developer and operator, and the institutional partner provides equity and arranges the bulk of project-level debt. Two details elevate this above a routine LOI. First, Northland's research describes the pairing as effectively brokered by the prospective hyperscaler tenant itself — the customer pointing NUAI toward the partners it wanted building and financing the site, which is a meaningful tell on intent. Second, Stream was acquired by Apollo Global Management in late 2025 at a valuation of roughly $40 billion, and the institutional partner is believed (per Northland) to be Apollo — putting some of the most credible capital in infrastructure behind the structure. It is still an LOI, not a signed definitive, but the roster is what turns a development concept into a financeable platform.

The power story is validated. What differentiates TCDC is not the dirt — it's the power. NUAI's "behind-the-meter" (BTM) thesis received concrete substantiation through a 450 MW behind-the-meter generation plan at TCDC developed with named partners Thunderhead Energy and TURBINE-X Energy. In a market where the binding constraint on AI buildout is increasingly electrons, not acres, a credible path to nearly half a gigawatt of on-site generation is the asset.

The hyperscaler is in advanced negotiations — over secured capacity, not a concept. The event that would re-rate the whole equity is a hyperscale lease. Management has described advanced commercial discussions with a top-tier, credit-worthy hyperscaler — realistically one of the big four cloud builders (Alphabet, Amazon, Meta, Microsoft) — for a campus with roughly 650 MW already secured and a path beyond 1 GW. The acquisition of an additional 54-acre corridor adjacent to Vistra and Calpine power plants was itself a milestone within those lease discussions. Timing is framed conservatively around fall 2026, and conservatism here is a feature given how the market punishes overpromising. The backdrop is favorable: recent hyperscale leases in the sector have printed in roughly the $140–190 per kW per month range (at least one recent deal involving Google reportedly reached ~$188), while the big four are guiding to historic 2026 capex — Alphabet to about $175–185 billion and Amazon to around $200 billion — as demand outruns deliverable power. In that environment, a power-secured, near-shovel-ready site is exactly what is scarce.

The invisible bid: a capital-markets function, finally resourced

Not every driver of a stock is a press release. For most of its life, NUAI was too small and too underfunded to run the kind of investor-relations program that institutional money expects — sustained institutional outreach, non-deal roadshows, analyst targeting, the steady cadence of being in front of the right funds. Those functions weren't broken; they were simply never staffed. That is changing, and the upgrade is visible in the hires themselves.

The company's investor relations now runs through OG Advisory Group, where the engagement is led by Lincoln Tan — who previously ran investor relations and marketing at IREN through precisely the kind of transition NUAI is now attempting (a power-and-mining story re-rating into an AI data-center story), and who came to IR from Macquarie Capital. Pair that with CFO Ted Warner, whose career was built structuring data-center financings on Wall Street, and the company has, arguably for the first time, a team explicitly equipped to court institutional capital rather than simply collect retail attention.

The practical implication is the kind of "invisible" activity that rarely makes headlines but steadily changes a stock's character: institutional meetings, conference presence (B. Riley in May, Datacloud in June), and the normal rhythm of roadshows and analyst engagement that turns a thinly followed micro-cap into a name long-only funds can actually own. As the shareholder base broadens and deepens, two things tend to follow — a higher-quality register and lower volatility — as price discovery shifts away from fast retail money toward investors underwriting a multi-year build.

This compounds with the de-risking. Every overhang removed — the lawsuit, the dilutive structures — is one less reason for a fundamental investor to pass and one less piece of "hair" on the story. The explicit catalysts get the headlines; this quieter professionalization of the capital-markets function is part of what lets them stick.

What the Street is starting to see

Sell-side coverage is one of the clearest signs the professionalization is working. In April, Northland Capital Markets initiated coverage with an Outperform rating and an $11 price target — against a share price barely above $5 at the time, implying roughly 2x upside. The logic is a staged, project-finance valuation: Northland credits only ~283 MW of TCDC capacity (Phase 1 plus half of Phase 2), assumes NUAI retains ~45% of the JV, applies a ~19x EV/EBITDA multiple in line with listed data-center peers, and discounts back on a ~125 million fully-diluted share count. Notably, that target deliberately excludes the back half of secured capacity, all of Phase 3, and NUAI's entire ~7 GW wholly-owned New Mexico pipeline (a ~3,500-acre Lea County site with a small-modular-reactor angle via a Last Energy partnership) — meaning the bull case carries option value the published target doesn't pay for.

NUAI now has its first real institutional research footprint, and a company running a proper IR program with a clean-up story to tell typically attracts more coverage over time. Additional analysts picking up the name through year-end — plausibly several — would broaden the buy-side audience and is exactly the kind of slow, compounding tailwind the "invisible bid" is built on.

The catalysts ahead

The next few weeks and months offer a dense sequence of potential catalysts:

Datacloud Global Congress, June 2–4, Cannes. President & COO Charlie Nelson is scheduled to speak at the industry's marquee gathering — the kind of room where hyperscalers, Tier-1 operators, and institutional capital allocators are all present (in fact, the hyperscalers, Stream, and Apollo are all present). For a company in active lease and JV negotiations, the value of being on that stage, at that moment, is hard to overstate.

A Stream JV definitive agreement converting the LOI into something binding.

A hyperscaler lease, the single highest-impact event in the story.

Expanding analyst coverage. With one Outperform initiation on the board, additional firms picking up the name — potentially several by year-end — would deepen the institutional audience.

A still-growing team. The June 1 additions of a chief development officer and general counsel are likely an opening move, not the finish; further senior hires would keep signaling that management is staffing for execution and often front-run bigger announcements.

The picture

Step back and the pattern is consistent: every quarter, if not every month, a structural negative has come off the board and a structural positive has gone on. Sharon AI — cleared. The toxic-preferred path — scrapped. The state lawsuit — settling. In their place: a Macquarie facility, a Tier-1 operating partner, a validated power plan, a CFO and now a development chief and general counsel drawn straight from the hyperscaler and data-center world, and an $80 million-plus cash cushion. The market tends to discount a stock for its overhangs right up until the moment they're gone — and then re-rate it for the platform underneath. With the first sell-side target sitting at roughly double the recent price and explicitly excluding most of the pipeline, the gap between where NUAI trades and what a leased, financed platform could be worth is the heart of the opportunity. NUAI is converting overhangs into catalysts on a remarkably steady cadence.

15

41

212

27,269

IREN is working with @nvidia to build NVIDIA DSX-aligned AI infrastructure across its global data center portfolio.

• Advancing the Sweetwater campus as part of IREN’s AI infrastructure buildout

• Adopting NVIDIA DSX OS technologies, including NVIDIA Infrastructure Controller and NVIDIA Fleet Intelligence

• Establishing a reference deployment of k0rdent AI with NVIDIA DSX OS and @MirantisIT

• Joining the NVIDIA DSX Sim ecosystem, including simulation with NVIDIA DSX Air

Learn more about NVIDIA DSX: nvidianews.nvidia.com/news/d…

50

222

1,778

192,980