Joined August 2023

- Tweets 4,514

- Following 742

- Followers 9,991

- Likes 1,460

4,068 Photos and videos

Pinned Tweet

21 Oct 2025

HFBestIdeas.com is now live.

It’s free (for now), you just need to create an account.

Two main features:

1️⃣ Access to 1,000 quarterly fund letters

2️⃣ Around 500 stock pitches extracted from fund letters each quarter

21

20

216

93,623

Guinness Greater China Fund's latest quarterly letter — key takeaways:

• **Large-cap Chinese tech has suffered de-ratings due to AI competitive concerns and a shift away from crowded growth positions.**

• Taiwan's outperformance is largely attributed to TSMC, which has seen a 30% increase in capital expenditure, leading to significant index dispersion.

• The Fund is overweight Industrials and Consumer Discretionary while being underweight Communication Services, with no exposure to Energy.

• The portfolio trades at a forward PE of ~12.7x, compared to a long-term average of ~14.8x, indicating a compelling entry point given the fundamentals are improving.

• Managers believe markets are underestimating cyclical recovery and AI-linked upside in Industrials, expecting margin recovery driven by improving PPI and infrastructure demand.

• They do not foresee large-scale consumption stimulus in the next five years, focusing instead on manufacturing upgrades and public services, which supports their industrial and upgrading exposures.

• Initiated a position in Weichai Power to capitalize on data-centre and onsite power demand, as well as high-margin aftermarket services.

• The Fund’s equal-weight approach has created structural underweights to Tencent and Alibaba, benefiting relative performance amid their decline.

• Top contributors include Elite Material, Hangzhou First Applied, and Nari Technology, while Shenzhou, Meituan, and Baidu detracted from performance.

• The underweight to Taiwan/TSMC negatively impacted relative performance during its outperformance, while being underweight in Materials and lacking Energy exposure helped during sector weakness.

Read the full letter → hfbestideas.com/letters?open…

1

2

10

2,614

1 Main Capital's latest quarterly letter — key takeaways:

• **The recent AI-driven selloff, particularly impacting IWG, is viewed as an overreaction; the firm remains a high-conviction holding based on a multi-year thesis.**

• IWG's near-term free cash flow timing has shifted to 2025, yet its medium-term fundamentals are strong, targeting ≥4% top-line growth and low-teens EBITDA growth, with potential for ~$1bn EBITDA.

• The manager believes AI will serve as a tailwind for IWG by driving demand for short-term leases and creating long-term office space for management without significant capital investment.

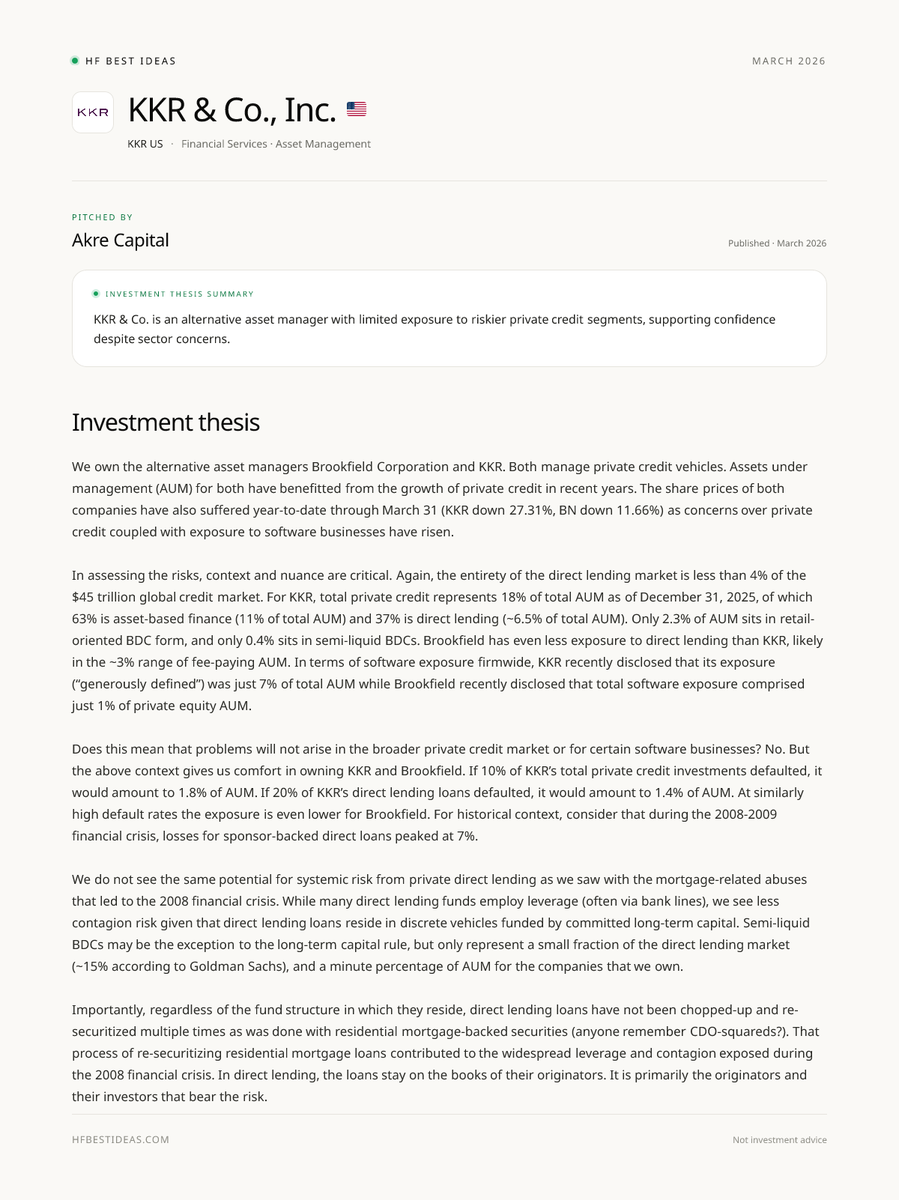

• Reinitiated a core position in KKR after a >30% decline, citing material AUM growth, diversified fee streams, limited direct-lending exposure, a recent $23bn NAX4 close, and insider buying as reasons for optimism.

• **The macro outlook indicates a bifurcation between expensive growth stocks and overlooked cash-generative businesses; geopolitical risks (notably in Iran and the Strait of Hormuz) pose a wildcard for oil, inflation, and Fed policy.**

• The manager believes fears surrounding private credit for KKR are overstated, predicting that mid-sized alternatives will be culled while mega-alternatives will capture increased flows from allocators favoring top-tier managers.

• The portfolio is highly concentrated, with the top five holdings comprising ~65% of capital, focusing on high-quality, cash-generative small caps capable of using downturns to acquire competitors and repurchase stock.

• The manager's approach emphasizes long-term, fundamentals-driven underwriting, opportunistic purchases during periods of indiscriminate selling, and prioritizing companies that can widen their competitive moats and generate free cash flow.

Read the full letter → hfbestideas.com/letters?open…

3

21

5,913

35 pitches found in hedge fund reports this week :

(link in bio)

🔹 Agilysys Inc (AGYS US) by Artisan Non-U.S. Small-Mid Growth Strategy

🔹 Amphenol Corporation (APH US) by Aristotle Large Cap Growth

🔹 Analog Devices Inc (ADI US) by Artisan U.S. Mid-Cap Value Strategy

🔹 Arthur J. Gallagher & Co. (AJG US) by Artisan U.S. Mid-Cap Growth Strategy

🔹 BE Semiconductor Industries NV (BESI NA) by Guinness Global Quality Mid Cap

🔹 Brenntag SE (BNR GR) by Artisan Non-U.S. Small-Mid Growth Strategy

🔹 Brown & Brown Inc (BRO US) by Artisan U.S. Mid-Cap Value Strategy

🔹 CME Group Inc. (CME US) by Alpha Wealth Funds

🔹 CoStar Group, Inc. (CSGP US) by Baron Asset Fund

🔹 CTT – Correios de Portugal SA (CTT PL) by Symmetry Invest

🔹 DraftKings Inc. (DKNG US) by Baron Discovery Fund

🔹 Envista Holdings (NVST US) by Aristotle Small Cap Equity

🔹 EQT (EQT US) by Andrew Hill Investment Advisors

🔹 Gartner, Inc. (IT US) by Baron Asset Fund

🔹 GE Vernova (GEV US) by Andrew Hill Investment Advisors

🔹 Gildan Activewear Inc. (GIL US) by Artemis US Extended Alpha Fund

🔹 Immunome Inc. (IMNM US) by Aristotle Core Equity

🔹 Indus Towers Limited (INDUSTOW IN) by Baron India Fund

🔹 IQVIA Holdings Inc (IQV US) by Artisan U.S. Mid-Cap Value Strategy

🔹 Johnson & Johnson (JNJ US) by Guinness Global Equity Income

🔹 KKR & Co (KKR US) by 1 Main Capital

🔹 Marsh & McLennan (MMC US) by Oakmark Select Fund

🔹 Nebius Group N.V. (NBIS US) by Baron Global Opportunity Fund

🔹 Ollie's Bargain Outlet Holdings Inc (OLLI US) by Artisan U.S. Small-Cap Growth Strategy

🔹 ONEOK (OKE US) by Andrew Hill Investment Advisors

🔹 Onto Innovation Inc (ONTO US) by Artisan U.S. Small-Cap Growth Strategy

🔹 Permian Resources Corp (PR US) by Artisan U.S. Mid-Cap Value Strategy

🔹 Prio S.A. (PRIO3 BZ) by Baron Emerging Markets Fund

🔹 Roblox Corporation (RBLX US) by Artisan Global Discovery Strategy

🔹 Targa Resources Corp (TRGP US) by Artemis US Select Fund

🔹 The Japan Steel Works, Ltd. (5631 JP) by Baron Emerging Markets Fund

🔹 TotalEnergies SE (TTE FP) by Aristotle Value Equity

🔹 Tradeweb Markets Inc (TW US) by Artisan U.S. Mid-Cap Growth Strategy

🔹 Weyerhaeuser Company (WY US) by Baron Real Estate Income Fund

🔹 Zedcor Inc. (ZDC CN) by Hood River International Opportunity Fund

2

1,198

Baron Technology ETF is long Lam Research Corporation $LRCX US

Extract from their Mar 26 letter

1

6

1,403

Baron Emerging Markets Fund on the niche companies they consider beneficiaries of the tightness in both memory and leading-edge logic:

leading-edge process complexity is driving adoption of HPSP Co., Ltd.'s high-pressure hydrogen annealing technology, while Park Systems Corporation's atomic force microscopes are among the few tools capable of characterizing features at sub-nanometer tolerances. On the testing side, ISC Co., Ltd.'s test sockets benefit from surging GPU and AI ASIC shipments as well as rising pin count per chip, while Chroma ATE Inc.'s system-level test equipment is among its fastest-growing product lines. ASPEED Technology Inc., whose baseboard management controller chips handle remote monitoring and management of servers, has seen its addressable market expand with every incremental increase in rack-level complexity.

Extract from their Q1'26 letter

1

1,202

SpaceX represents 25.5% of Baron Asset Fund at the end of Q1'26, valued at a $1,250B market cap. The position was initially acquired in 2020 at a $47B valuation and is now worth $845M.

1

1

1,065

35 pitches found in hedge fund reports this week :

(Link in the comments)

🔹 Accenture plc (ACN US) by Oakmark Equity and Income Fund

🔹 Acutaas Chemicals Limited (ACUTAAS IN) by Baron India Fund

🔹 adidas AG (ADS GR) by Artisan International Value Strategy

🔹 Ameriprise Financial Inc. (AMP US) by Gator Financial Partners

🔹 Anhui Yingliu Electromechanical (603308 CH) by Hood River Emerging Markets Fund

🔹 Apple (AAPL US) by Andrew Hill Investment Advisors

🔹 Axon Enterprise Inc (AXON US) by Nightview Capital

🔹 Beng Kuang Marine Limited (BKM SP) by Fairlight Alpha Fund

🔹 Blue Ant Media Inc. (BAMI CN) by Donville Kent

🔹 Centum Electronics Limited (CENTUM IN) by Baron India Fund

🔹 Century Aluminum Company (CENX US) by Riverwater Sustainable Value Strategy

🔹 Chevron Corporation (CVX US) by Aristotle Value Equity

🔹 Coherent Corp. (COHR US) by Aristotle Core Equity

🔹 Coherent Corp. (COHR US) by Baron SMID Cap ETF

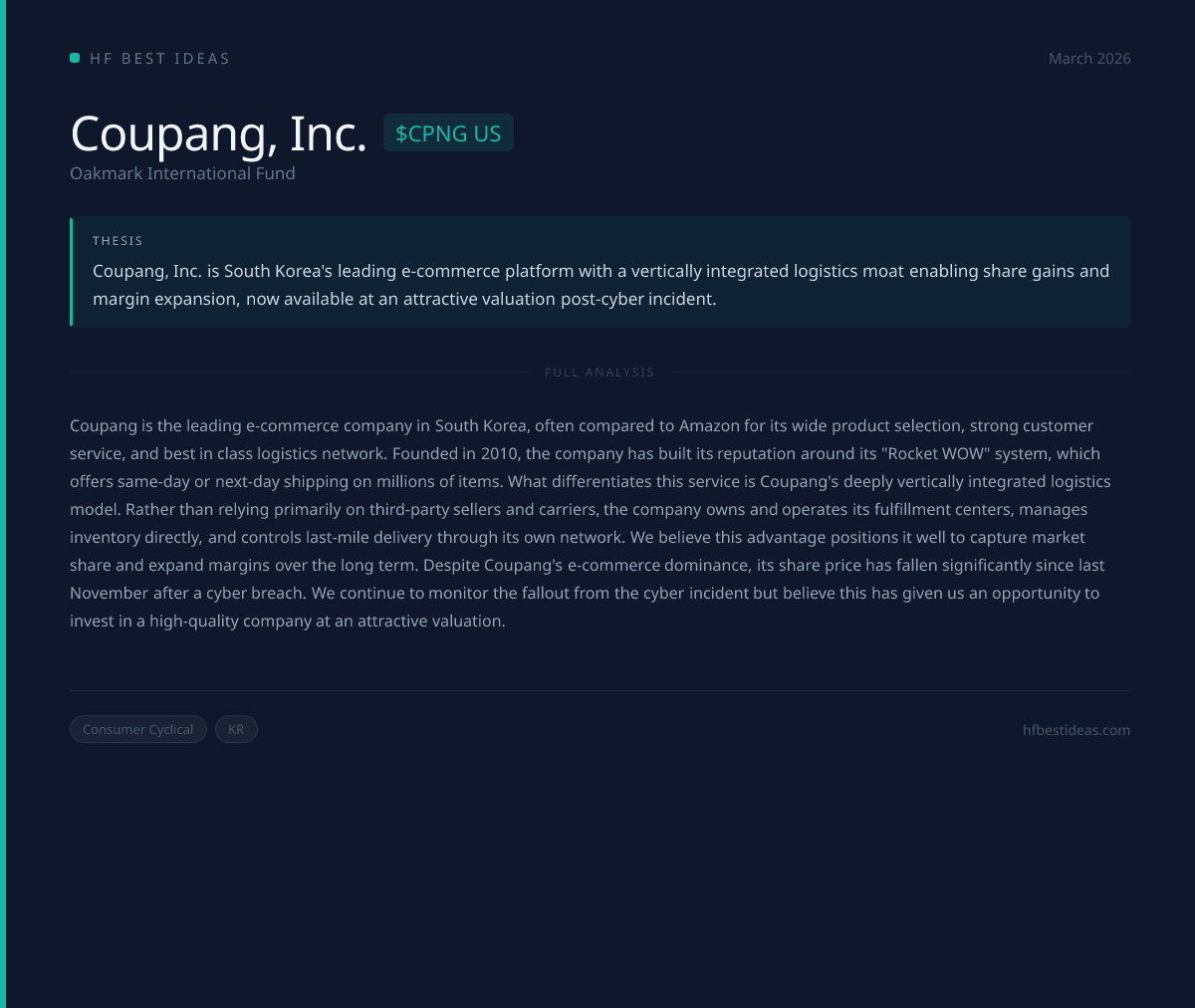

🔹 Coupang, Inc. (CPNG US) by Artisan International Value Strategy

🔹 Divi’s Laboratories Limited (DIVI IN) by Baron India Fund

🔹 Edwards Lifesciences Corp (EW US) by Artisan U.S. Mid-Cap Growth Strategy

🔹 Forgent Power Solutions, Inc. (FPS US) by Baron Discovery Fund

🔹 Fujikura Ltd (5803 JP) by Artisan Global Equity Strategy

🔹 Fujikura Ltd (5803 JP) by Bell Global Emerging Companies Fund

🔹 Gartner (IT US) by Oakmark Select Fund

🔹 J.B. Hunt Transport Services (JBHT US) by Artemis US Extended Alpha Fund

🔹 James Hardie Industries (JHX AU) by WS Amati Global Innovation Fund

🔹 Lumentum Holdings Inc. (LITE US) by Baron Technology ETF

🔹 Methanex Corporation (MEOH US) by Riverwater Sustainable Value Strategy

🔹 Olema Pharmaceuticals, Inc. (OLMA US) by Aristotle Large Cap Growth

🔹 Publicis Groupe (PUB FP) by Guinness Global Equity Income

🔹 RELX (REL LN) by Artemis UK Select Fund

🔹 Salesforce, Inc. (CRM US) by Hotchkis & Wiley Large Cap Fundamental Value

🔹 Semtech Corp (SMTC US) by Artisan U.S. Mid-Cap Growth Strategy

🔹 SiTime Corp (SITM US) by Artisan U.S. Mid-Cap Growth Strategy

🔹 Techtronic Industries Co. Ltd. (669 HK) by Aristotle International Equity ADR

🔹 Tempus AI, Inc. (TEM US) by Aristotle Core Equity

🔹 Veralto Corp (VLTO US) by Artisan U.S. Mid-Cap Value Strategy

🔹 Waters Corp (WAT US) by Artisan U.S. Mid-Cap Growth Strategy

1

1

9

2,847

Fairlight Alpha Fund's latest quarterly letter — key takeaways:

• **Middle East strikes and the closure of the Strait of Hormuz have triggered a sharp oil shock, resulting in regional supply disruptions and a divergence in crude prices, which has led to higher inflation expectations and a delay in anticipated Fed rate cuts.**

• The manager expects oil prices to remain elevated due to potential permanent damage to shipping and infrastructure, combined with limited insurance coverage, while also noting that structural demand from petrochemicals could diminish over time through electrification, biomaterials, and recycling.

• U.S. Treasury yields have risen modestly despite the oil shock; while equity volatility increased, U.S. large-cap equities displayed relative resilience, reinforcing the manager’s focus on idiosyncratic, low-correlation micro-cap investments.

• Continued emphasis on micro caps and “obscured” investments where company-specific fundamentals are prioritized over macroeconomic fluctuations; the firm is undertaking an active global search (both manual and AI-assisted) for underfollowed ideas.

• The fund has established a new position in Cematrix, citing its structural growth potential from cellular concrete, a robust order book, and an attractive mid-single-digit EBITDA multiple valuation compared to current year estimates.

• Beng Kuang Marine is progressing towards improved asset-light margins post-ASOM consolidation; management anticipates margin expansion due to a shift towards recurring FPSO maintenance revenue, having secured S$28m at ASOM against S$98m total group revenue last year.

• Despite underperformance among precious-metal juniors due to gold volatility and rising energy costs, the manager believes several names, such as Monument Mining, present value opportunities based on free cash flow metrics if energy supply remains stable.

• The firm is actively exploring AI agents to enhance idea generation but underscores the limitations of AI; they emphasize the necessity of human intuition, fieldwork, and rigorous fact-checking, treating AI as a complementary tool rather than a replacement.

Read the full letter → hfbestideas.com/letters?open…

6

1,336

Horizon Kinetics's latest quarterly letter — key takeaways:

• **Market crowds create persistent mispricings**, allowing patient investors to exploit deep, non-fundamental discounts left in the wake of episodic bubbles in sectors like tech and commodities.

• Emphasis on the **structural advantage of asset-light, high-margin businesses** such as royalty companies and exchanges, which are seen as strategic core holdings that compound profitably over decades.

• Income investors are emerging from a “**Great Yield Famine**” (2008–2022) with revived interest in higher short- and intermediate-term Treasuries now offering better income solutions.

• Event-driven opportunities highlighted include **buying Cheniere convertible notes** during credit stresses for bond-like downside and equity upside, and positioning in **Hawaiian Electric** as it approaches dividend reinstatement.

• Identification of persistent public-market income discounts due to market structure and investor policies, suggesting that yield premiums in vehicles like **royalty trusts and MLPs** may not accurately reflect fundamental credit risks.

• Private-market income strategies focus on short-term, collateralized **bridge and construction loans** for time-sensitive borrowers, and private royalty/mineral funds acquiring undervalued **Permian and Haynesville acreage**.

• A shift toward **CLO strategy** by purchasing senior AAA/AA tranches for floating-rate income, duration protection against rising rates, and historically low default rates, with retail access provided through fund vehicles.

• The investment process prioritizes **long-term, idea-driven sourcing** through direct engagement, producing unique opportunities and a willingness to maintain concentrated positions over index-like allocations.

Read the full letter → hfbestideas.com/letters?open…

2

32

5,398

Lakehouse Global Growth Fund is long MercadoLibre $MELI US

Extract from their Feb 26 letter

1

2

34

4,598

Artisan Non-U.S. Growth Strategy's latest quarterly letter — key takeaways:

• **Global markets showed mixed signals in Q1 2026, with initial optimism from easing European inflation and expectations for looser policy, yet late-quarter volatility arose from geopolitical tensions and rising energy costs.**

• AI is identified as a crucial structural driver, leading to sustained demand for semiconductors and data-center infrastructure, which the team links directly to investment opportunities due to rising power needs.

• The portfolio reflects a concentrated conviction in long-duration themes focused on electrification and defense/aerospace, where selective stock choices in industrials and IT contributed significantly to relative value.

• **Heightened geopolitical tensions have led to increased defense spending, benefiting Korean suppliers like LIG Nex1 and Hanwha Aerospace, which are experiencing growing export backlogs and higher-margin international sales.**

• The electrification strategy includes significant investments in grid expansion and data-center power infrastructure, highlighted by holdings in LS Electric and National Grid, driven by surging electricity demand and constraints in transformer supply.

• Stock-specific risk actions include trimming insurance positions and exiting Prudential and Allianz following strong performances, alongside exiting RELX due to perceived disintermediation risks from AI integrations.

• Opportunistic investments were made, including initiating a position in CSG after a selloff related to European ammunition exposure, adding Fujikura for fiber-optic technology linked to AI data centers, and purchasing Sun Hung Kai for anticipated recovery in Hong Kong real estate.

• Concerns remain around energy exposure, which affected relative returns amid rising oil prices, with mixed performances in financials, particularly with UBS facing pressure from potential Swiss capital reforms.

Read the full letter → hfbestideas.com/letters?open…

1,041

Fiduciary Management is long Booking Holdings Inc. $BKNG US

Extract from their Mar 26 letter

2

24

9,002

Spotlight on Dick’s Sporting Goods: At least 3 funds featured $DKS in their Q1'26 investor letters :

Riverwater Sustainable Value Strategy (Q1'26): Dick’s Sporting Goods is poised for growth supported by strong demand dynamics and strategic execution. The anticipated increase in discretionary spending due to higher tax refunds, particularly in athletic categories, offers a promising demand tailwind. Additionally, the upcoming FIFA World Cup in the U.S. is expected to drive interest in soccer-related products. The fund highlights the potential stabilization of vendor relationships, notably with Nike, as the retail landscape evolves. With a valuation of 14.9x estimated 2026 earnings, the fund believes DKS can maintain margin resilience while capitalizing on long-term growth opportunities.

Bell Global Emerging Companies Fund (Q1'26): As the largest sporting goods retailer in the U.S., Dick’s is strategically expanding its market presence through experiential retail and data monetization. The integration of Foot Locker is seen as a significant growth avenue, providing operational synergies and enhancing competitive advantage. The fund emphasizes the importance of the House of Sport concept in creating a unique shopping experience, which strengthens customer loyalty. The GameChanger platform is also noted for its potential to generate high-margin data revenue, further solidifying DKS’s position in the market.

KNA Capital (Q1'26): Dick’s Sporting Goods is recognized as a dominant player in a challenging industry, benefiting from recent shifts back to wholesale from suppliers, alongside rising youth sports spending. The fund outlines how Dick’s has learned from past industry failures, allowing it to sustain growth without reliance on debt. Notably, the GameChanger platform is highlighted as a unique asset that connects the company with youth sports markets, and the rollout of experiential stores is viewed as a way to enhance customer engagement. With upcoming global sporting events and a reasonable valuation, the fund believes Dick’s is well-positioned to continue gaining market share.

All $DKS analyses here : hfbestideas.com/?q=dks&page=…

8

1,342

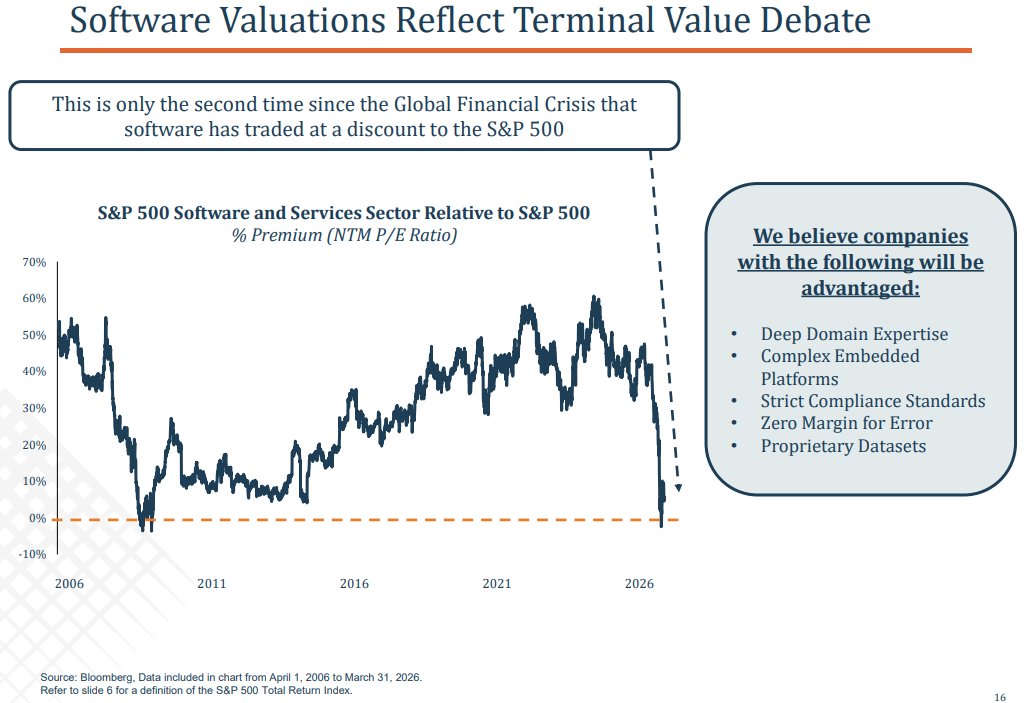

This is only the second time since the Global Financial Crisis that software has traded at a discount to the S&P 500 (Edgewood Q1'26 letter)

13

1,662

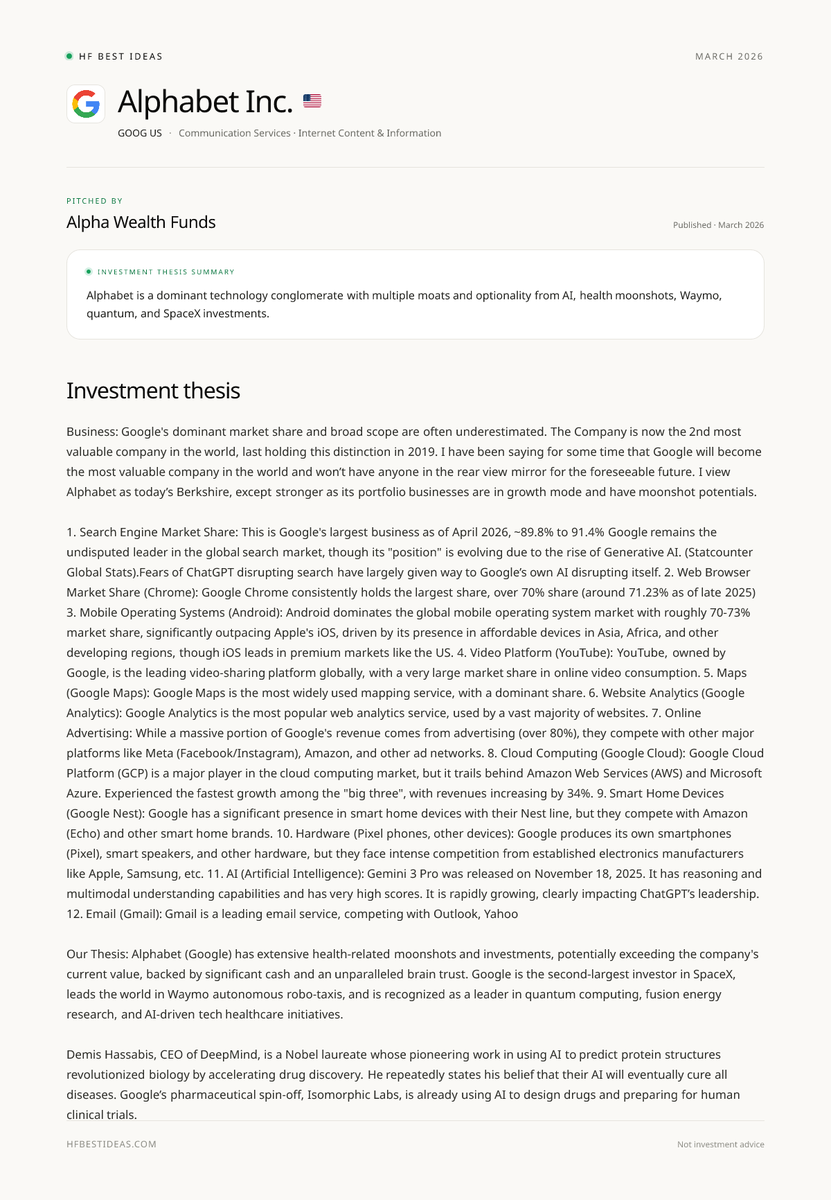

Alpha Wealth Funds is long Alphabet Inc. $GOOG US

"I view Alphabet as today's Berkshire, except stronger as its portfolio businesses are in growth mode and have moonshot petentials"

Extract from their Q1'26 letter

10

1,488

Praetorian Capital's latest quarterly letter — key takeaways:

• The manager introduces the macro framework of **“Economic Feudalism,”** explaining prolonged sluggish corporate performance and guiding portfolio adjustments towards asymmetric, inflecting opportunities.

• Immediate macro risk revolves around the **Strait of Hormuz reopening**; the manager remains agnostic on timing but highlights systemic risks from downside inventories and fertilizer shortages.

• The portfolio is strategically positioned for a **disrupted/inflationary environment**, focusing on long inflation beneficiaries, volatility, and increased exchange trading volumes; refiners are emphasized as large, profitable exposures post-war.

• Tactical adjustments include trimming some **Event-Driven equity** to create dry powder for wartime volatility, while the core portfolio remains largely unchanged since the conflict began.

• The investment philosophy highlights concentrated bets on businesses with **observable inflections and multi‑quarter visibility**, rejecting short-term trading narratives in favor of quantifiable probabilistic asymmetries looking 12–24 months ahead.

• **Marex (MRX)** is identified as a structural winner due to elevated commodities volatility, with expectations for an earnings inflection and significant multiple expansion as fundamentals reset.

• An **Emerging Markets basket** is positioned as a dollar-sensitive recovery trade, anticipating a weaker USD under new US policy changes to boost EM valuations and reduce dollar-denominated debt stress.

• Sector themes include **precious metals exposures** as a hedge against inflation and central bank trust, alongside two diversified refiners expected to benefit from tighter crack spreads, buybacks, and limited near-term refinery additions.

• Specific conviction play: **St. Joe (JOE)** is viewed as a promising land/real-estate investment, capitalizing on migration to the Florida Panhandle, expected AFFO growth, and inflation protection linked to wealthy relocation trends.

• The fund's risk posture involves maintaining **below-normal equity exposure** until clarity emerges on Hormuz and other geopolitical concerns, while remaining optimistic about potential upside if earnings acceleration continues, referencing “**Project Zimbabwe**” as a multi-quarter catalyst.

Read the full letter → hfbestideas.com/letters?open…

8

1,336

35 pitches found in hedge fund reports this week :

(link in bio)

🔹 Alphabet Inc. (GOOGL US) by Baron Technology ETF

🔹 Applied Materials, Inc. (AMAT US) by Alpha Wealth Funds

🔹 ASML Holding N.V. (ASML NA) by Baron Technology ETF

🔹 Bank of the Philippine Islands (BPI PM) by Ariel International DM EM

🔹 Coherent Corp. (COHR US) by Baron Technology ETF

🔹 Daifuku Co. Ltd. (6383 JP) by Ariel Global

🔹 Dianthus Therapeutics Inc (DNTH US) by Artisan Non-U.S. Small-Mid Growth Strategy

🔹 Ecolab Inc (ECL US) by Mar Vista U.S. Quality

🔹 Eli Lilly and Co (LLY US) by Artisan Global Opportunities Strategy

🔹 Ensign Energy Services (ESI CN) by Bison Interests

🔹 Guidewire Software, Inc. (GWRE US) by Baron SMID Cap ETF

🔹 HAL Trust (HAL NA) by East 72 Dynasty Trust

🔹 Insulet Corporation (PODD US) by Alpha Wealth Funds

🔹 JDC Group AG (JDC GY) by Symmetry Invest

🔹 Lam Research Corporation (LRCX US) by Baron Technology ETF

🔹 Linde plc (LIN US) by Artisan Global Opportunities Strategy

🔹 Marex Group plc (MRX US) by Praetorian Capital

🔹 Medline (MDLN US) by Artisan Global Discovery Strategy

🔹 Midac Holdings Co Ltd (6564 JP) by Ennismore Global Smaller Companies Fund

🔹 Rational AG (RAA GY) by Guinness European Equity Income

🔹 Samsara Inc. (IOT US) by Baron SMID Cap ETF

🔹 ServiceTitan, Inc. (TTAN US) by Baron Discovery Fund

🔹 Shopify Inc. (SHOP US) by Baron Technology ETF

🔹 Solaris Energy Infrastructure Inc. (SEI US) by Baron Technology ETF

🔹 Spotify Technology SA (SPOT US) by Artisan Global Opportunities Strategy

🔹 Sun Hung Kai Properties Ltd (16 HK) by Artisan Non-U.S. Growth Strategy

🔹 Tesla Inc (TSLA US) by Nightview Capital

🔹 Texas Pacific Land Corporation (TPL US) by Horizon Kinetics

🔹 Twist Bioscience Corp (TWST US) by Artisan Global Discovery Strategy

🔹 Vend (VEND NO) by Pontus

🔹 Vitalhub Corp. (VHI CN) by Donville Kent

🔹 Weichai Power Co., Ltd. (2338 HK) by Guinness Greater China

🔹 Wise plc (WISE LN) by Saga Partners

🔹 Workday, Inc. (WDAY US) by Hotchkis & Wiley Large Cap Fundamental Value

🔹 Zedcor Inc. (ZDC CN) by Donville Kent

6

1,263

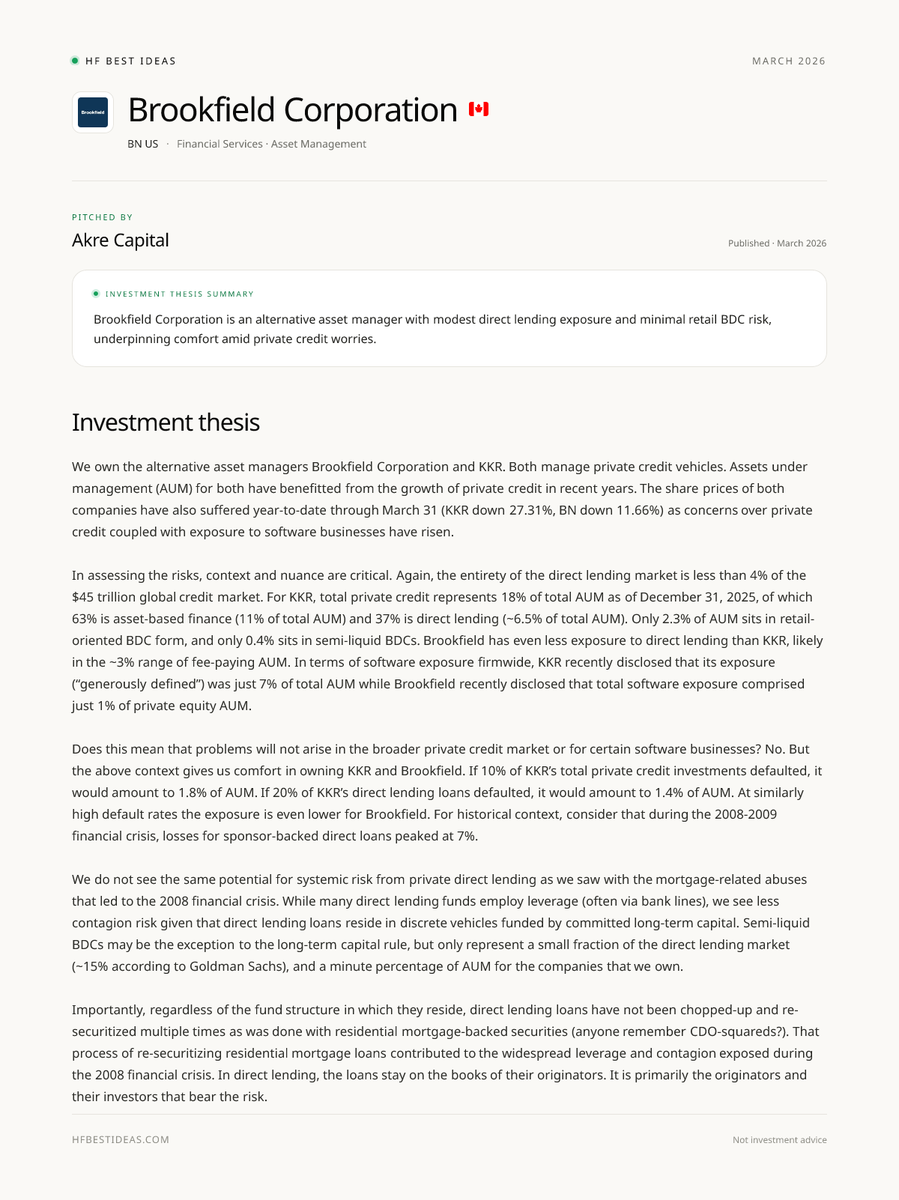

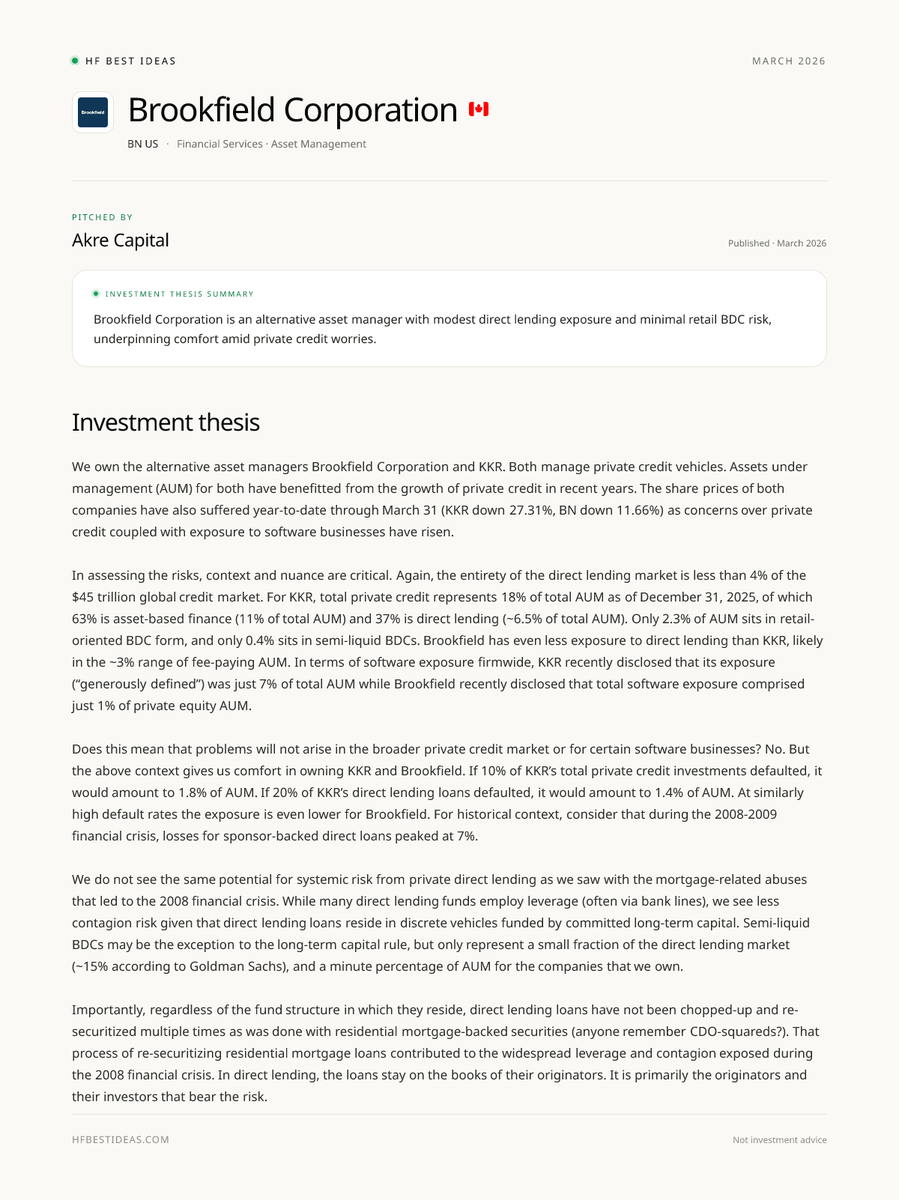

Akre Capital's Q1'26 letter : hfbestideas.com/letters?open…

1

3

870