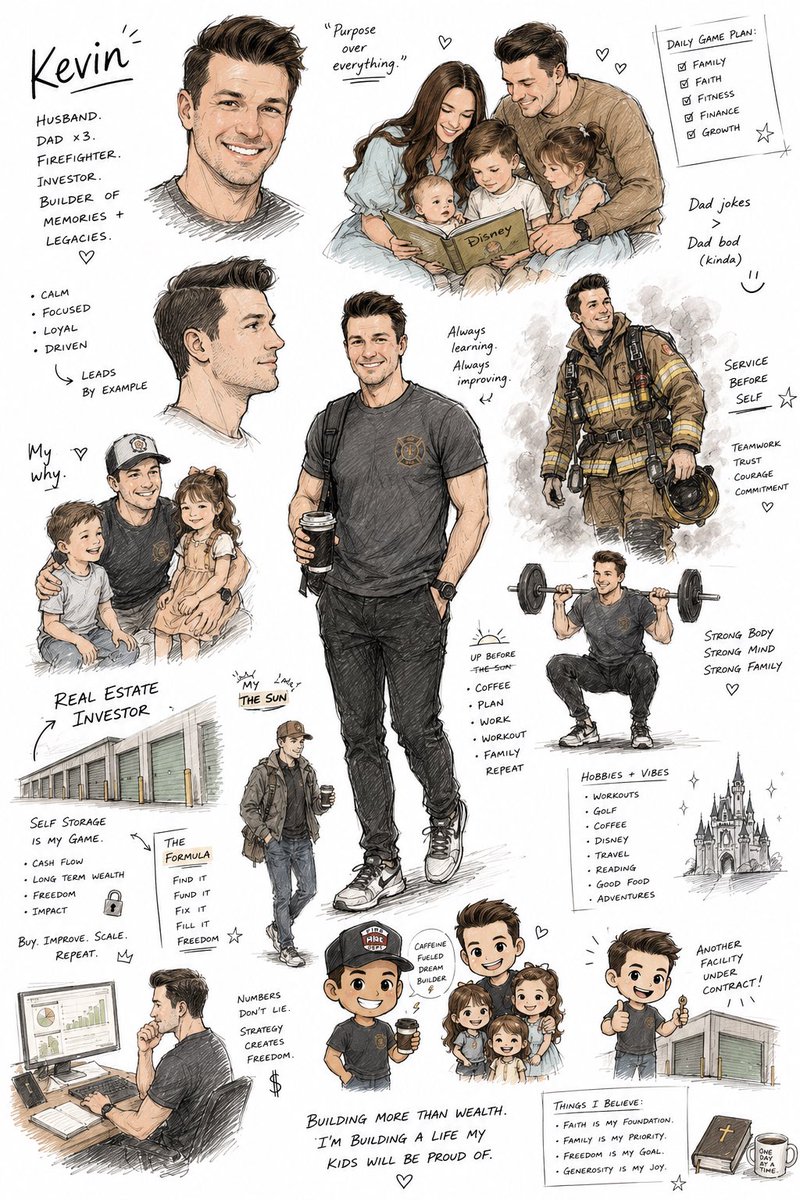

Own and operate self storage | Coach new self storage investors | Hard money lender | Husband, Dad, Fireman. California is home.

Joined October 2012

- Tweets 10,474

- Following 834

- Followers 5,747

- Likes 7,770

1,149 Photos and videos

Pinned Tweet

Quick reintroduction:

I’m Kevin. Firefighter. 36. Wife, 3 kids (5 and under)

I bought my first house at 19 during the worst housing crash in modern history.

Ended up buying about 50 more over the next 5 years.

Quit two corporate jobs before 25.

Moved to Australia for a year to figure out what I actually wanted. Turns out it wasn’t to sit behind a desk and work a 9-5 or to manage a bunch of homes.

Today I own 12 self-storage facilities across 4 states (acquiring more each year), run a hard money lending business, and coach people getting into storage.

Things I believe that most people in real estate won’t say out loud:

* High occupancy can be a trap

* Most coaching programs are marketing funnels disguised as education

* Real estate isn’t passive. Run from whoever tells you it is.

* A $500K storage facility in a small town will outperform a $2M multifamily in a “hot market” 9 times out of 10

* Automation is overrated if your processes are broken - you’re just automating chaos faster

* You don’t need to quit your W-2 to build real wealth

I post real numbers, real mistakes, real lessons learned, and real operations. No fluff.

What’s one question you have about self-storage or real estate investing? Drop it below or DM me - I’ll answer every one.

12

2

85

15,569

A new student of mine asked me a question yesterday.

"Do cap rates matter?

Some people say yes, some say no"

My answer to her:

The first facility I purchased was a 2.6 cap.

It also yielded well over a 50% un-leveraged return within 24 moths.

Cap rates only truly matter when buying stabilized assets. When there isn't a lot of appreciation and revenue to force/create, so all you have is your initial return on capital.

That's when a cap rate matter - it's your annualized return.

If you are buying a value add asset - where you can increase revenue (and ideally decrease expenses), cap rates matter much less.

A storage facility that is operating well below its potential is often worth more than say a 7 or 8 cap on its actuals.

That doesn't mean you should overpay.

That doesn't mean you shouldn't care about current revenue.

That doesn't mean you should pay for 100% of upside not yet created.

But, assuming I am confident enough in my ability to increase revenue significantly and force appreciation, I am willing to pay a premium on today's revenue.

Back to that first facility example.

We purchased for 705k

It was only doing 36k/yr in revenue

We then increased revenue to 150k/yr and sold it.

Had we only offered a price that was in line with current cap rates (8 in this case) on existing NOI (18k in this case) we would have never gotten the deal.

Our offer would have been $225,000

We payed $705,000 (not because we like overpaying), but because we knew we could get close to doubling our money in 2-3 years time.

Win for seller, Win for us.

All this to say: cap rates matter on stabilized assets, but they matter much less on value add assets. Offer accordingly.

4

1

31

3,561

I own self-storage facilities, multi family, and some single family homes.

I also run a small private hard money lending business - Founding Capital - that has approximately 5-10M actively deployed at any given time. Some operators look at that and assume the two businesses are unrelated. They are not.

Because I get alot of questions on this topic I figured I would post a deep dive. Here we go.

Here is how the two businesses actually strengthen each other, what the math looks like, and the structural decisions I'd make differently if I were starting today.

**Why a storage operator should look at hard money lending at all:**

Most operators reinvest free cash flow back into more storage. That's the obvious move and it's the right move for the first 5-8 facilities. But somewhere around facility 10 or so, two structural problems appear:

* Adding the 11th and 12th facility doesn't materially change your life. The operational complexity grows faster than the cash flow upside on that incremental deal.

* The capital you've accumulated is increasingly stuck in stabilized, low-velocity equity. You're rich on paper, but you're slow to redeploy when an opportunity surfaces.

A private lending business addresses both problems.

The capital deploys faster than real estate.

The operational complexity is lower than another facility.

And the relationship density it creates inside your network compounds into deal flow you can't manufacture any other way.

**The structure of Founding Capital:**

We typically run 5-10M of capital out across 12-18 active loans at any given time. The structure:

* Investors receive 10% annual interest, paid quarterly.

* Borrowers pay 12-13% annual interest and 2 points minimum at origination.

* The 2-3% spread plus the origination points is the business.

* We also invest our own capital in every deal alongside investor capital.

* Loan terms typically 6-12 months. Real estate-collateralized.

The borrower profile is mostly operators we know - typically other storage/small commercial operators or residential operators who need bridge capital for an acquisition, a value-add capex project, or a refinance gap.

These are not consumer loans.

These are not typically single-family flips (although 90% of them were when I started this). These are primarily commercial real estate operators with assets we can lien against and operating discipline we can verify.

**The performance numbers:**

Across all loans we've ever funded:

* Approximately 98% borrower performance - borrowers paying as agreed.

* Zero commercial foreclosures, ever.

* The 2% that has gone sideways has always been resolved through borrower-funded payoff, not through forced sale.

That track record is the entire reason investors return capital to us across multiple cycles. The 10% return is the headline. The zero-loss track record is the actual product.

**Why the two businesses strengthen each other (the part most operators miss):**

1. **Deal flow on the storage side improves.** Some of our hard money borrowers are storage operators whose deals we end up acquiring directly when the borrower can't take the deal to permanent debt. We have first look. We have already underwritten the asset. We already know the operator.

2. **Capital flexibility improves.** When I see a storage acquisition I want to move on quickly, I can fund the down payment from the lending side, then refinance the senior debt later. That's faster than raising fresh equity from outside investors.

3. **Relationship density compounds.** Every borrower becomes part of the network. They refer other operators. They tell us when they're hearing about deals. The lending book is the deepest source of high-quality storage deal intel I have.

4. **Counter-cyclicality.** When storage cap rates compress and acquisitions get harder, lending demand goes UP - because operators need bridge capital to compete on speed. The two businesses are slightly counter-cyclical, which reduces volatility across the combined portfolio.

**The capital structure decision I'd think harder about today:**

When we started, we used a single fund-style structure for investor capital. As we've scaled, the friction of pooled capital and individual loan participation has surfaced complexity I would have avoided with a different structure from day one.

If I were starting today, I'd consider:

* Loan-by-loan investor matching (each loan funded by a specific investor or small group, rather than pooled).

* A clearer separation of "patient" capital (12 month willing) from "bridge" capital (6-month preferences).

* Earlier investment in loan servicing infrastructure (technology, not staffing).

None of these are mistakes that broke the business. They're just friction I'd save someone else from.

**The borrower-side discipline that protects the business:**

*Real-estate collateralization is non-negotiable. We do not do unsecured loans.

* 1st position loans only

* We underwrite the operator as carefully as the property. A great asset with a weak operator is a losing loan.

* Personal guarantees on the borrowing entity's principal.

* Title insurance on every deed of trust.

* Property insurance with us as additional insured and loss payee.

* Real estate tax monitoring (we get notified directly if a borrower goes delinquent).

These are not unique to our shop. They are the discipline every lending operator should run. The shops that skip these are the ones that show up on the foreclosure dockets a year later.

**The honest constraint:**

This business is harder to scale than storage, at least for me. The hold-down on capital deployment is investor relationships, not deal flow. We could fund more loans than we currently fund. We don't, because building investor trust takes time and we'd rather grow slower with the right capital than faster with the wrong.

In 2026, our capital base is approximately 20-25 individual investors. Most are high-W2-income professionals (physicians, attorneys, executives) who want a meaningfully higher yield than the public market gives them, with a real-estate-collateralized downside profile. The others are primarily retired and investing out of retirement accounts.

**The strategic frame for storage operators:**

Most operators think of their second business as a horizontal expansion - adding more storage, adding multifamily, adding industrial. That's still real estate concentration.

The lending business is a vertical expansion. The cash flow is uncorrelated with real estate cap rates (to an extent you make safe loans). The labor is dramatically lower per dollar of revenue. And the deal flow it creates feeds the primary business in a way another acquisition never will.

For storage operators with 8 facilities who are looking for the next 5-year move: the lending business is worth a serious look. It's not the right move for everyone. It is genuinely the highest-leverage adjacent business I've ever added to a real estate portfolio.

I'm always curious - If you operate a real estate portfolio of any size and you've built a complementary cash-flow business - what's the second business that produced the most leverage on the first?

9

2

58

9,554

I’m confused..

Are we back at war?

Or have a peace deal?

I think the stock market is confused too

1

1

427

I walked a facility last month that penciled beautifully.

My AI model told me to buy it.

Then the manager mentioned, offhand, that half of building C floods every spring.

That's not in the rent roll. It's not in the T12.

It's in a 10-minute conversation on a gravel lot.

AI scales the math. But it's not a human replacement.

4

48

3,970

Is it okay to make your 6 year old who’s being disrespectful stay in the garage with a pair of scissors and break down the twenty boxes your wife gets delivered each week ?

Asking for a friend

4

10

919

If you’re ever having a bad day:

Remember that I bought AMD at $2.50

… And sold it at $10.

10

38

6,414

Email from a hard money borrower this morning:

"Need 30 more days. Sale fell through. Got another buyer lined up."

Loan is already past due by 42 days.

He's paying interest every month. Just not principal.

Last time someone said "sale fell through" I lost 7 months waiting.

This time we're starting foreclosure prep on day 60.

98% loan portfolio performance means you have to stay disciplined on the 2%.

21

85

29,620

No alarm. No inbox. No “real quick” calls.

Just a week away and my four favorite people.

7

58

6,120

Customer acquisition channels I tested for my local newsletter:

Cold calling. Zero advertisers.

Cold email. Zero advertisers.

Facebook ads to local businesses. Zero advertisers.

Google ads. Zero advertisers.

Instagram DM. Every advertiser I have had.

Same product. Five channels. One worked.

The lesson is not about Instagram.

The lesson is to stop arguing with the data.

3

11

1,749

Extra land is great.

Just don’t forget you have to mow it every 2 weeks in your underwriting.

Future home of some contractor garages.

7

1

44

4,095

"Buy mom-and-pop" is the most repeated advice in self-storage.

It is half right.

Mom-and-pop tells you ownership is tired. It does not tell you the market is awake.

A tired mom-and-pop in a town that lost 8% of its population over 10 years is not a deal.

It is a tired liability with a fresh coat of paint.

The deal lives where tired ownership meets a market still growing.

Find both. Or skip it.

2

1

24

1,943

Unpriced listings on Crexi are the biggest waste of time for everyone.

Why is this a thing?

7

36

4,140

In contract to sell this one.

It wasn't part of our deal for me to complete gravel work prior to close.

But it's worth the 9k to me to start out on a good foot with new owner, setting him up for success.

I'll be holding a note for him, so I too have a vested interest in his success.

Plus I always run the facility as if it's mine up until the day of close. I never assume a sale will go through.

Deferred maintenance compounds.

Mud ruts -> unhappy tenants -> bad reviews -> harder lease-ups -> lower NOI -> lower valuation.

A few loads of gravel fix all of it. Do the unsexy work.

1

1

33

6,370

A serious first pass on a storage deal used to take me 2-4 hours.

Now it takes no more than 20 minutes.

I built an AI project that reads the OM, pulls county data, builds a 5-year pro forma, and flags every line where the broker’s expenses are fake.

The ROI isn’t the time saved.

It’s the deals I see now that I used to skip because I didn’t have 4 hours to spend on a maybe.

More deals analyzed = more value-add stories found = more LOIs written.

What would you automate first in your deal flow?

5

29

5,754

I should give credit where credit is due.

@ItsAlexStarr is the genius behind anything and everything AI for businesses!

1

1

621

In case anyone wants to know what SFR Investor is up to these days:

7

39

7,719

Deferred maintenance compounds.

Mud ruts -> unhappy tenants -> bad reviews -> harder lease-ups -> lower NOI -> lower valuation.

A few loads of gravel fix all of it. Do the unsexy work.

3

32

10,085