RWAs & Tokenization Analyst ▪︎ I Decode How Real-World Assets Actually Work On-Chain ▪︎ Content and Growth Strategist for Web3 Projects

Joined June 2016

- Tweets 7,628

- Following 516

- Followers 3,081

- Likes 25,447

883 Photos and videos

Jun 13

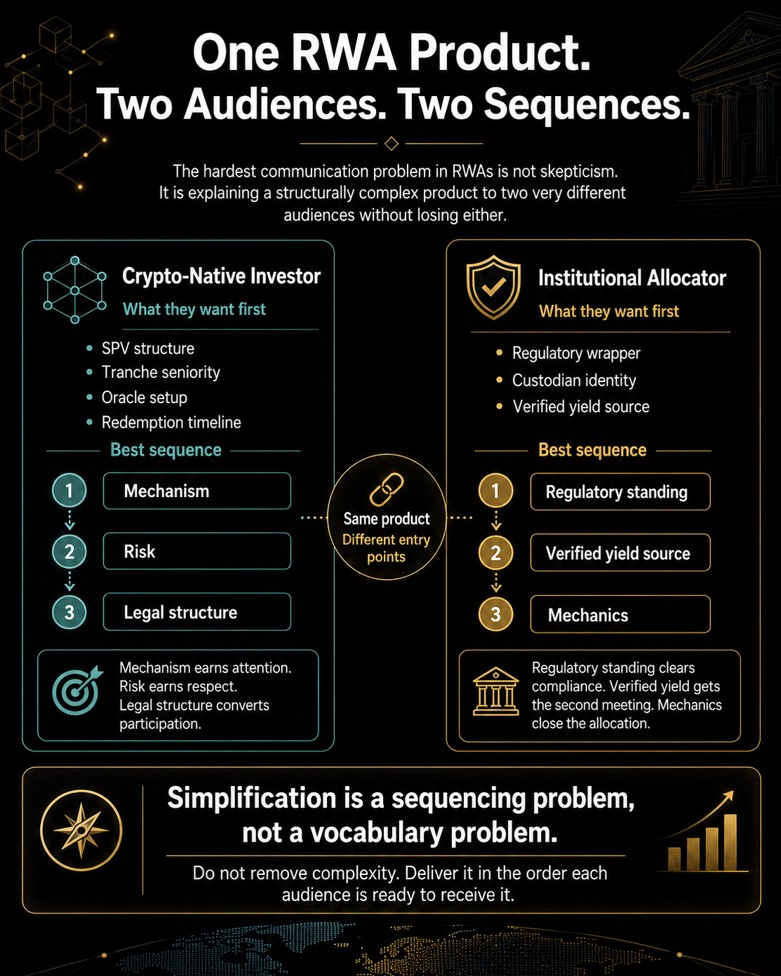

The hardest communication problem in the RWAs space is not convincing skeptics, but explaining a structurally complex product to two completely different audiences without losing either.

On one side, we have the crypto-native investor who wants the mechanics, specifically the SPV structure, the tranche seniority, the oracle setup, and the redemption timeline.

On the other side, we have the institutional allocator, whose compliance team needs the regulatory wrapper, the custodian identity, and the yield source verified before any conversation moves forward.

One person wants depth first, while the other wants legitimacy first, and these are not the same entry points.

The first instinct most RWA project teams have is to write one version of the explanation and hope it covers both audiences.

Unfortunately, that instinct almost always produces content that is simultaneously too technical for the allocator and too surface-level for the protocol-native reader.

The better approach is to treat simplification as a sequencing problem rather than a vocabulary problem.

You do not remove complexity from the explanation, but decide what order the complexity arrives in for each specific audience.

For the crypto-natives, lead with the mechanism, follow with the risk, and close with the legal structure.

The mechanism earns their attention, the honest risk coverage earns their respect, and the legal structure is what converts them into an actual participant.

For the institutional allocators, lead with the regulatory standing, follow with the verified yield source, and close with the mechanics.

The regulatory standing gets you past their compliance team, the verified yield source gets you a second meeting, and the mechanics close the allocation.

With this, you have the same product with two different sequences, and neither version removes anything from the explanation because each one gives the reader what they need in the order they are ready to receive it.

4

2

17

199

Jun 10

$360B in domain value. Illiquid for 25 years.

No market structure. No onchain access. DAVs fix that.

Sign up for early access 👇🏾

Jun 10

$360B in domain value. Illiquid for 25 years.

No market structure. No onchain access. DAVs fix that.

Sign up for early access 👇

→ dav.doma.xyz

2

7

121

Jun 10

Most people reading this announcement will simply read "260 tokenized stocks now swappable natively inside a hardware wallet".

The part that fewer people will notice is that the US, UK, and EEA are all excluded from access, which means the headline figure describes an offering available to only a fraction of Ledger users.

I think the distribution layer Ondo and Ledger are building here is genuinely impressive. No doubt.

However, the regulatory perimeter around it is equally real, so I will keep an eye out for the jurisdiction that cracks compliant tokenized equity access first 🫡

Jun 10

Tokenized stocks, now swappable natively inside @Ledger Wallet.

Powered by @1inch intent-based swaps, bringing gasless execution and hardware-backed clear signing to Ondo Global Markets.

Self-custody, now for 260 tokenized stocks, spanning the world's most in-demand assets.

2

6

645

Jun 9

Many of the RWA projects that will fail over the next three years will most likely collapse due to "lack of proper distribution."

A good number of RWA projects have genuine products with clean legal structures, real yields, and credible audits, yet for some reason, they keep ignoring the part that matters most.

This is why a team will spend 18 months building a tokenized credit product or a real estate fund, only to allocate roughly 6 weeks to figuring out who will hold it and why.

Meanwhile, a tokenized private credit pool is not like a crypto token that you can just list on an exchange and let speculation do the distribution work.

The target audience for such a product includes institutions, family offices, and sophisticated accredited investors who need to understand the legal wrapper, yield mechanics, custodians, and redemption terms before they allocate capital.

The RWA projects that will survive long enough to matter will be the ones that treat distribution as a parallel workstream from day one.

They can achieve this by building content, community, and credibility signals alongside the product infrastructure, rather than treating them as a post-launch phase that can wait.

I find this to be the most underserved problem in the RWA space right now, and it is almost entirely solvable with deliberate and applied strategies.

If you are building an RWA project, at what point in your roadmap did you first address distribution, and what does that strategy actually look like?

2

9

709

Jun 6

The MiCA transition relief period for crypto asset service providers operating under national laws officially ends on July 1st, 2026

This means that any crypto asset service provider operating under the transitional arrangements in EU member states must either have a license by that date or face serious consequences.

The conversation about this development in the Real World Assets (RWAs) community has largely been focused on what it means for stablecoin issuers.

However, the insight that should interest many community members is what it means for the competitive dynamics of RWAs' tokenization in Europe.

The clearest winners will be the protocols and platforms that have spent the past eighteen months building MiCA-compliant infrastructure rather than waiting to see how its enforcement will play out.

Securitize, which already operates as a regulated transfer agent across multiple jurisdictions, is better positioned than almost any other tokenization platform to absorb the new European institutional mandates.

The same applies to any RWA protocol that structured its EU-facing products through ESMA-registered entities early enough to have a compliance track record rather than a compliance promise.

The protocols that will face new challenges are the ones that have relied on transitional arrangements to continue operating while keeping their compliance investment minimal.

They now face a choice between accelerating their licensing timelines under real enforcement pressure or exiting the EU market entirely, and neither option is cheap or fast.

The broader implication of this development is that MiCA's enforcement phase is likely to consolidate the European RWAs market around a smaller number of well-capitalized and properly licensed players faster than anyone would have anticipated.

That is not necessarily bad for the space overall, but it does mean that the protocols with the deepest pockets and the most established regulatory relationships are about to widen their competitive moat significantly.

2

8

807

Jun 6

Took a short break to reflect and re-strategize on a few things.

Glad to be fully back 🫡

Expect some RWAs banger content soon :)

2

6

71

Taioo 📝 retweeted

Jun 4

Tokenized stocks are now productive capital.

“When Ondo tokenized stocks meet an operating system built for them, markets like STEY become possible.”

Explore how @SentoraHQ made Ondo tokenized stocks usable as collateral on @eulerfinance ↓

17

79

510

24,507

Taioo 📝 retweeted

Jun 3

How does a vault work when it holds a tokenized real-world asset?

Tokenized Treasuries, private credit, and regulated funds all run on settlement delays: subscriptions clear when the wire lands and the NAV strikes, not when the block confirms.

ERC-4626 is the vault standard for atomic settlement.

✅ Deposit > receive shares

It works because onchain-native assets settle instantly, and that shared interface is why @aave, @MorphoLabs, and @eulerfinance interoperate: any protocol can read a vault position, route to it, build on top of it.

Real-world assets don't settle instantly, so they need more from the interface. A vault can't mint shares against a NAV that hasn't struck yet.

ERC-7540 splits each operation into two steps:

✅ Request a deposit or redemption

⏳ The asset settles on its own timeline

✅ Claim when it clears

Same interface underneath, same core functions, so a protocol already integrated with ERC-4626 adapts with minimal changes.

Composability is the whole reason to put an asset onchain: an asset that speaks the standard can be read and used by every protocol, with no custom integration.

That's why async vaults are spreading across DeFi. And now @OpenZeppelin has shipped an implementation, open to any developer building real-world assets onchain.

The asset settles like a fund and composes like a token.

9

20

89

7,667

Taioo 📝 retweeted

May 30

DAVs are built to make premium domain exposure simple.

Instead of buying one domain at a time, traders can access a full premium portfolio through one tokenized asset. NAV is set at ~30% of retail aggregate value.

Sale proceeds flow to staked DAV holders.

The result: structured exposure to premium domains with clear pricing and proceeds participation.

Apply or join the waitlist 👇

dav.doma.xyz/

3

9

46

1,903

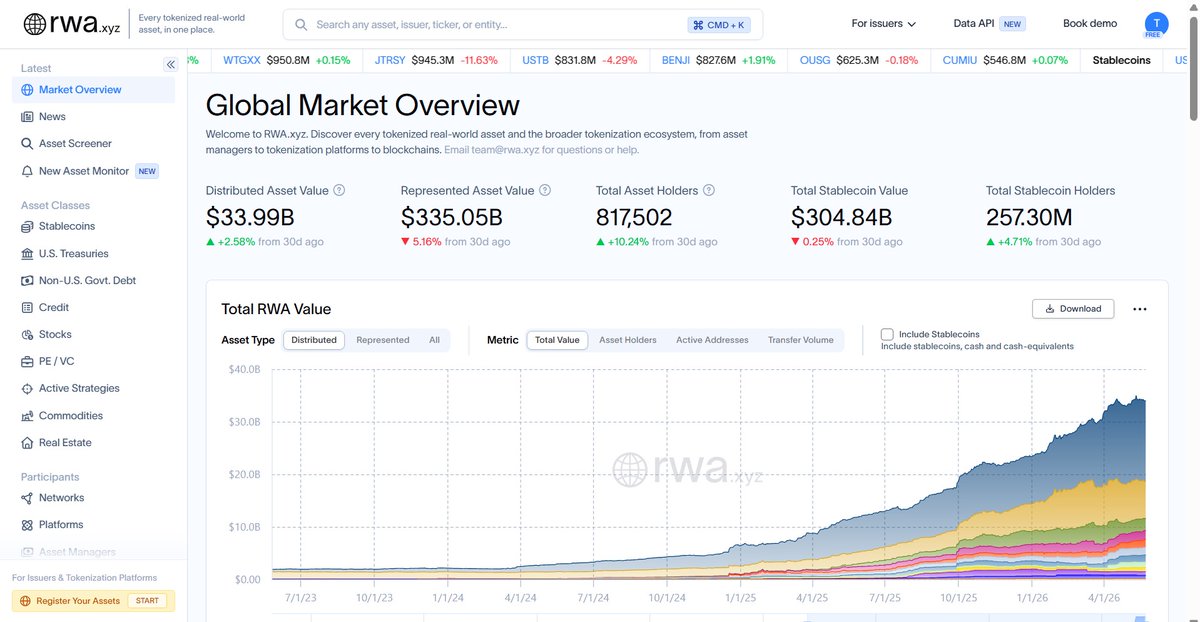

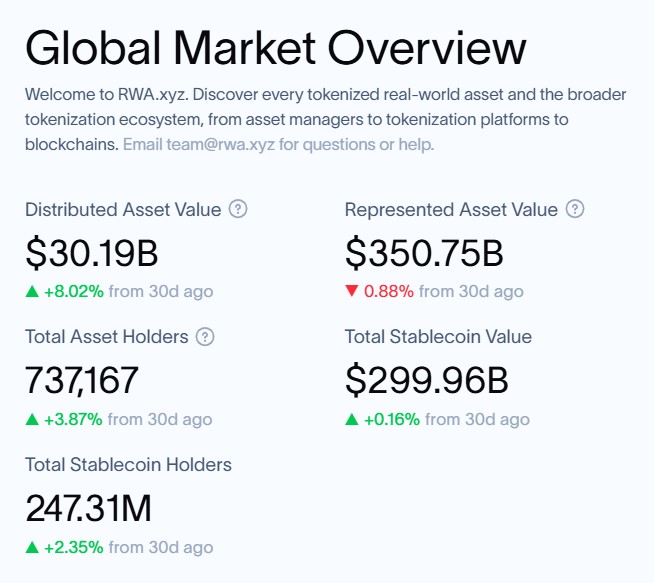

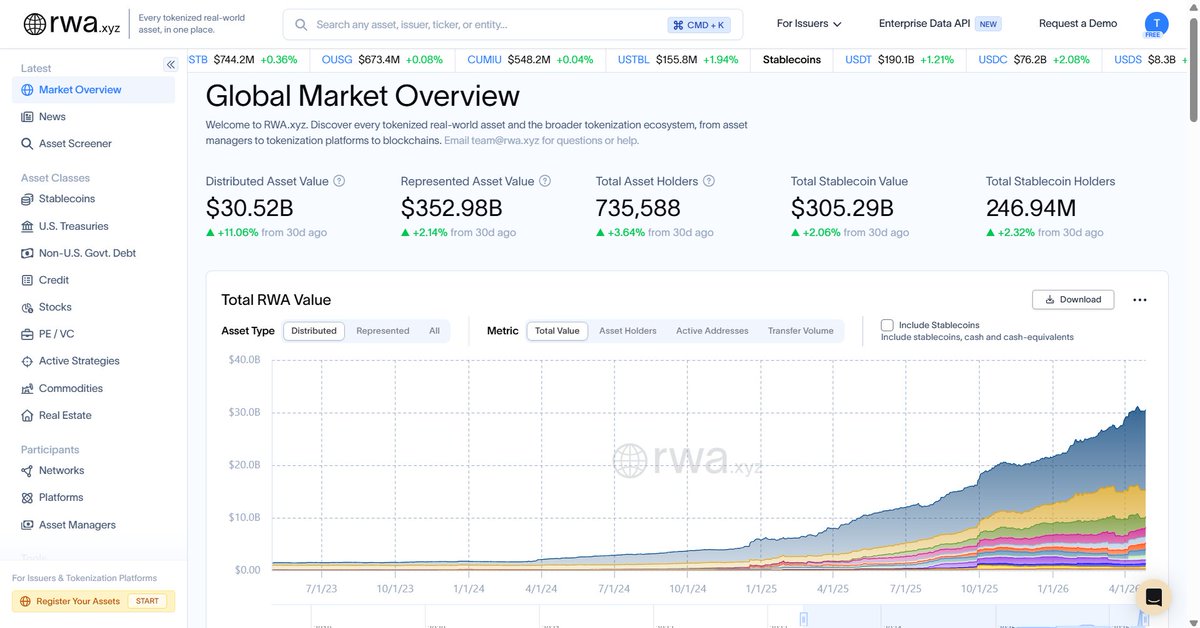

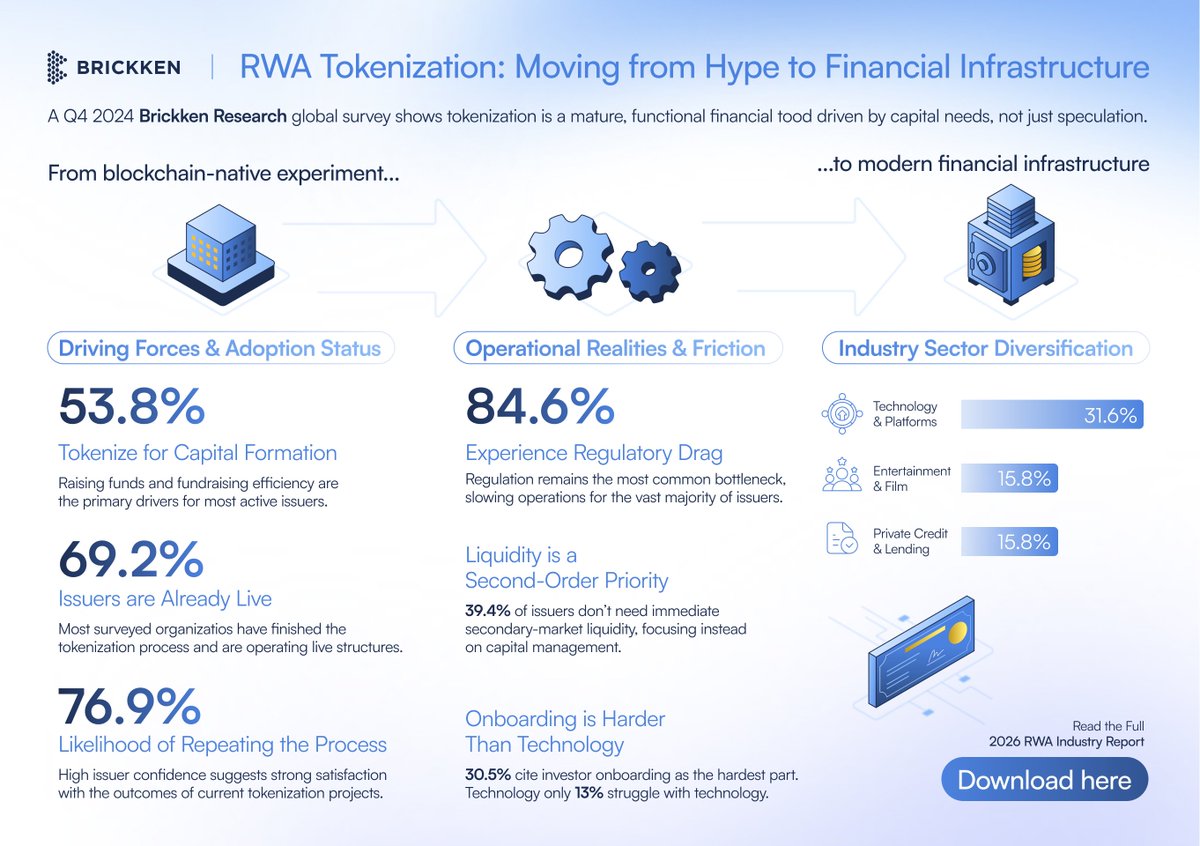

Forget the theory. We surveyed active issuers to uncover the operational realities of RWA tokenization in 2026.

The consensus is clear: tokenization is an active vehicle for capital formation, but scaling it comes with distinct friction points.

A look at the data:

• 69.2% of surveyed issuers are already live.

• 53.8% are leveraging tokenization primarily for fundraising.

• 84.6% cite regulatory drag as their primary bottleneck, drastically outpacing technology struggles (13%).

Technology is no longer the hurdle.

Regulation and investor onboarding are.

23

41

82

3,402

Taioo 📝 retweeted

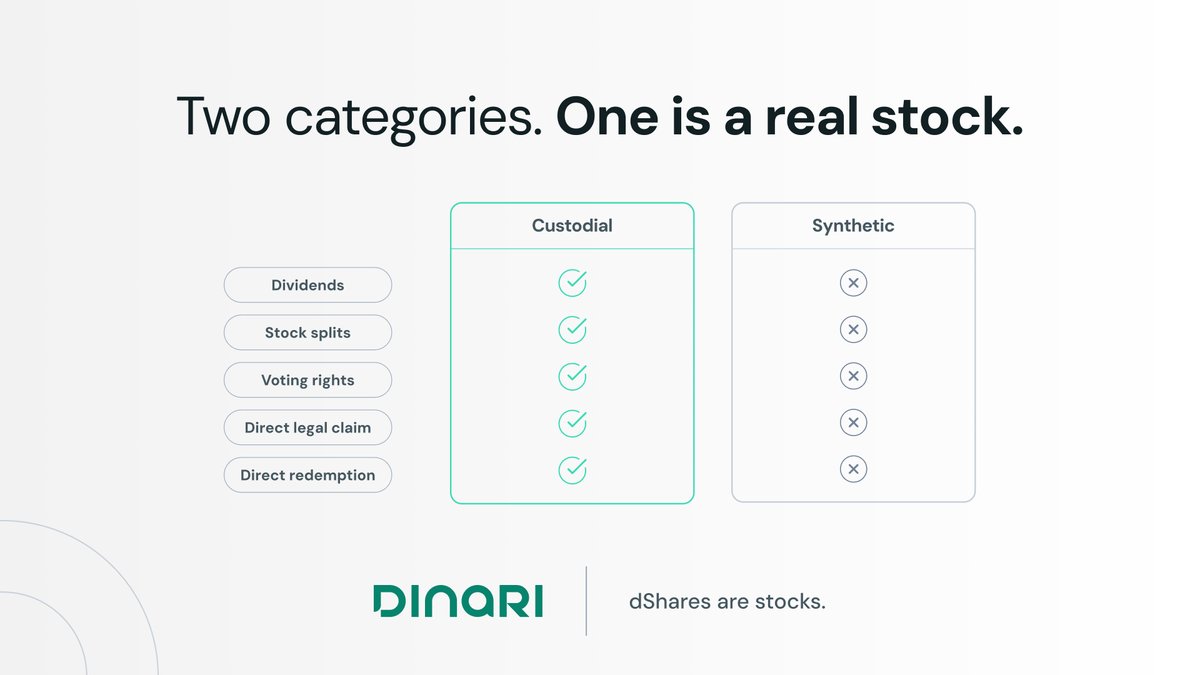

May 27

Two different models for tokenized stocks are now clearly defined by the SEC.

One gives you dividends, stock splits, voting rights, direct legal ownership, and direct redemption. The other doesn't.

dShares™ are stocks.

4

20

4,081