Exclusive Insights into China’s Tech & Innovation Landscape. Trips, bespoke research, and an investor-focused newsletter.

Joined June 2018

- Tweets 3,953

- Following 352

- Followers 13,904

- Likes 569

833 Photos and videos

Pinned Tweet

Jun 13

In the mobile era we saw Tencent and allies vs Alibaba. Is it happening again in the age of AI agents?

On June 8, 2026, WeChat opened its AI platform to mini-program developers. The update lets users swipe right on the main screen and ask an AI assistant to book rides, order food, book tickets, shop and pay through natural language. Meituan, JD.com, Dewu and Ctrip are among the partners.

This move pits WeChat’s vast mini-program ecosystem—over four million apps across 108 industries, reaching more than a billion monthly users—against Qwen’s “one-sentence” transaction approach. Qwen proved its strength (with subsidies) during the 2026 Lunar New Year: its AI processed 10 million orders in nine hours, 15 million on the first day and almost 200 million overall, while serving 166 million monthly users by March. The question is whether another platform can match that scale. WeChat already facilitates large volumes of orders through its traditional mini-program interface; adding a conversational layer could replace taps and menus with voice or text commands while using the existing payment, advertising and cloud revenue model. Subscriptions or revenue sharing for agent interactions may follow.

Meanwhile, on June 3, Qwen announced it would allow third‑party agents and skills, with brands like Luckin Coffee, KFC and Mixue among the early testers. Both platforms are moving toward similar agent-driven ecosystems.

1

3

30

2,205

Jun 13

In the mobile era we saw Tencent and allies vs Alibaba. Is it happening again in the age of AI agents?

On June 8, 2026, WeChat opened its AI platform to mini-program developers. The update lets users swipe right on the main screen and ask an AI assistant to book rides, order food, book tickets, shop and pay through natural language. Meituan, JD.com, Dewu and Ctrip are among the partners.

This move pits WeChat’s vast mini-program ecosystem—over four million apps across 108 industries, reaching more than a billion monthly users—against Qwen’s “one-sentence” transaction approach. Qwen proved its strength (with subsidies) during the 2026 Lunar New Year: its AI processed 10 million orders in nine hours, 15 million on the first day and almost 200 million overall, while serving 166 million monthly users by March. The question is whether another platform can match that scale. WeChat already facilitates large volumes of orders through its traditional mini-program interface; adding a conversational layer could replace taps and menus with voice or text commands while using the existing payment, advertising and cloud revenue model. Subscriptions or revenue sharing for agent interactions may follow.

Meanwhile, on June 3, Qwen announced it would allow third‑party agents and skills, with brands like Luckin Coffee, KFC and Mixue among the early testers. Both platforms are moving toward similar agent-driven ecosystems.

1

3

30

2,205

Jun 13

We just wrote about this. Read our take here:

- Tencent's AI Bet Is Not a Chatbot. It Is WeChat as an Action Layer (Jun 2026): techbuzzchina.substack.com/p…

And an earlier piece on Alibaba's efforts:

- The Taobao Inside Qwen: Why Alibaba's AI Gambit Is About Re-Architecting the Internet: techbuzzchina.substack.com/p…

2

555

Jun 12

Meituan Longzhu partner Wang Xinyu says China's embodied AI investment is "too little, not too much", a contrarian take given over 50 companies in the space are valued above RMB 10 billion (~$1.4B). Longzhu entities are Unitree's largest external shareholder, with over RMB 400 million (~$55.2M) cumulatively for roughly 9.65%. The firm also backed Moonshot AI (Kimi) from July 2023 onward.

Wang's framework, three verticals (AI, semiconductors, energy) by three horizontals (EV, robotics, next-gen terminals), is broad, but the interesting part is the founder archetype he names: the "young big brother." Young in age, but with a decade of deep domain expertise. He cites Unitree's Wang Xingxing and Moonshot's Yang Zhilin as examples. The claim is that a new generation of passion-driven founders, not purely commercial motives, will push China from cost-efficient imitation toward genuine innovation.

Wang also predicts a "GPT-3.5 moment" for robotics, where robots work smoothly and naturally, within one to two years, at most three. That timeline is aggressive and contradicts the industry's history of overpromising, as the article itself notes with autonomous driving. The hardware advantage (Unitree's cost discipline, manufacturing scale) is real, but the software layer, manipulation, generalization, remains unproven.

The deeper bet is on the "chain leader" in embodied intelligence, which may not be the robot OEM itself. Comparable to CATL capturing more profit than any Chinese EV maker. Longzhu is placing multiple bets across the stack to capture whichever layer becomes the bottleneck. If the real value accrues to a component or chip supplier rather than robot assemblers, the current valuations of robot companies may be betting on the wrong layer.

---

9

831

Jun 12

ByteDance is spinning out its AI drug discovery unit into an independent entity, retaining majority control. The core team of roughly 50 people, along with algorithms, the tech platform, and existing pipeline assets, will transfer to the new company. Compute support from Volcano Engine continues.

This is an organizational admission that AI4S (AI for Science) operates on a fundamentally different rhythm than consumer internet. Drug discovery requires longer capital cycles, specialized talent that competes with biotech rather than Big Tech, and decision-making that tolerates years without a product launch.

The unit has released models including Protenix, Seedfold, PXDesign, and the Anew Labs platform. In April, Anew Labs disclosed an IL-17 small molecule project claiming the first global small-molecule blockade of three IL-17 family dimers. That claim is company-announced and unvalidated. The unit has no approved drugs or disclosed clinical trial data.

The structure lets ByteDance retain upside while the unit raises external capital at biotech valuations and attracts domain talent. Compute dependency on Volcano Engine creates a cloud revenue loop regardless of drug outcomes.

1

9

705

Jun 12

Zhipu AI's market capitalization briefly exceeded HKD 700 billion (~USD 89 billion) on May 28 before falling below HKD 600 billion (~USD 76 billion) by June 5, a roughly 34% pullback from its peak. During the same period, the company announced plans to raise RMB 15 billion (~USD 2.1 billion) in mainland China as part of its push toward an eventual A H dual listing.

The gap between market expectations and current business fundamentals is hard to ignore.

Zhipu reported 2025 revenue of RMB 724 million (~USD 100 million), a net loss of RMB 4.7 billion (~USD 650 million), and negative operating cash flow of RMB 2.25 billion (~USD 310 million). Gross margin declined from 56.3% in 2024 to 41% by the end of 2025. API revenue—the scalable, higher-margin business that underpins comparisons to OpenAI and Anthropic—accounted for just 26.3% of total revenue, versus roughly 80% at Anthropic.

At its peak, the valuation implied a business that does not yet exist: a company driven primarily by high-margin API consumption at scale rather than enterprise projects, customized deployments, and other services-heavy revenue streams.

One metric does stand out. API gross margin improved from 3.3% to 18.9% over the same period, while GLM token usage increased 15-fold in six months. Alibaba, Tencent, and Baidu are among the reported users. If API revenue grows to more than half of total revenue and margins continue to improve, the business could eventually support a premium valuation.

If not, the valuation is likely to continue converging toward current fundamentals rather than future expectations.

15

1,016

Jun 12

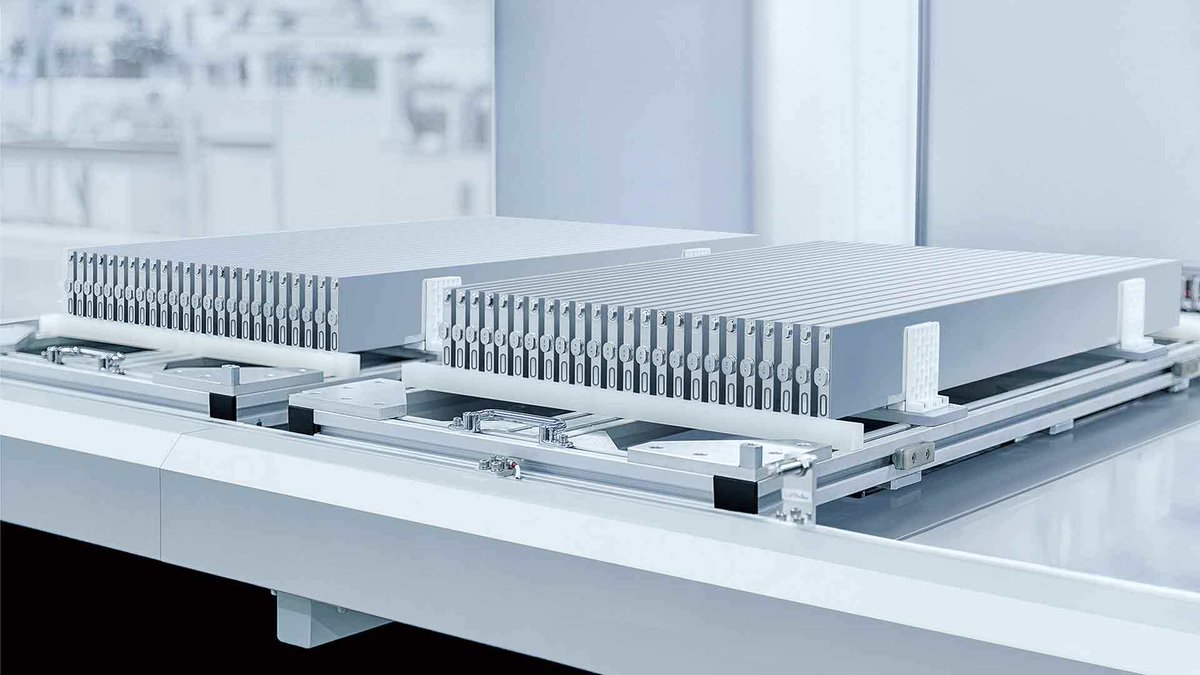

In the months we've been tracking BYD, the dominant concerns were demand-side: inventory buildup, margin compression, price-war exposure. But now the limiting factor has changed. According to BYD's latest investor relations record, orders surged after the March launch of the second-generation Blade Battery, and capacity "cannot meet demand." Chairman Wang Chuanfu told shareholders that 2026 vehicle sales will depend on battery production capacity, which is currently ramping at 20,000,30,000 units per month.

The specs explain the pull: 10% to 70% charge in 5 minutes at room temperature, 10% to 97% in 9 minutes, and at -30°C, 20% to 97% in 12 minutes. If the flash-charging technology works at scale, it addresses the most tangible barrier to EV adoption: charging time, in a way that pure range extension never did.

This updates the story from our July 2025 piece, which noted that beneath BYD's volume growth lay squeezed margins and an unproven premium push. A technology that creates enough demand to make production the bottleneck is a different kind of problem.

The open question: if battery capacity is now the main limitation, does BYD's vertical integration become a moat (controlling its own supply chain at the most critical node) or a capital trap, especially as CATL fast-charging cells become available to competitors? The answer depends on how fast BYD can turn battery output into vehicle sales without letting rivals catch up on charging speed.

$002594.SZ $1211.HK @BYDCompany

1

1

18

1,571

Jun 12

A few related TBC pieces help fill in the context around China's local-commerce and instant-retail fight:

- China 2025 Outlook: E-Commerce Trends and Electric Vehicle Leap (Jan 2025): techbuzzchina.substack.com/p…

- From Scale to Strength: Can BYD Win in 2025? (Jul 2025): techbuzzchina.substack.com/p…

From Underdog to Contender Price War Inventory vs.

1

729

Jun 11

Our partner @WeijinResearch pointed out a key risk for Apple AI in China 👀

"5. The China gap is fundamental because Apple can localize on-device and Apple Silicon cloud models, but AFM 3 Cloud Pro’s dependence on full-spec Nvidia GPUs runs into export controls. If those GPUs can’t enter China, Apple faces a choice: ship a weaker cloud model or find a Chinese chip partner, risking a bifurcated Apple Intelligence experience."

$AAPL

1

2

10

1,414

Jun 11

Read their full piece here or subscribe to their substack!

x.com/WeijinResearch/status/…

1

1

881

Jun 11

According to Chinese tech media reports, WeChat's AI agent will let users swipe right to invoke an assistant that calls Mini Programs to complete tasks: ride-hailing via Didi, food delivery via Meituan, flight booking via Ctrip, shopping via JD.com. The project is in closed testing, with those service providers reportedly already integrating. Tencent is also said to be in talks with Huawei, Honor, and Xiaomi about Agent-to-Agent connections so phone-level voice assistants can route requests into WeChat's service layer. Honor, the most aggressive on AI phones, has reportedly completed its A2A integration.

The scale of what's available as atomic capability matters. WeChat hosts several million Mini Programs covering payments, identity, location, ordering, ticketing, and logistics. Each one is a service endpoint an agent can call without the user ever needing to install, open, or navigate within a standalone app.

When we wrote about Alibaba's Qwen-powered "one-sentence" transactions in April, the observation was that AI was becoming the first touchpoint for user intent, capturing what analysts called the most expensive commercial real estate in the AI era. The WeChat Agent project extends that logic to a different architecture. Instead of routing everything through Taobao, Alipay, Fliggy, and Amap as Alibaba did during Spring Festival, Tencent is making the agent a neutral-ish dispatcher across competing service providers inside its own ecosystem.

The strategic value may land less on chatbot metrics and more on distribution control. Tencent already captures payment fees, advertising, and cloud revenue from Mini Program traffic. An agent that routes more service requests through that same infrastructure extends the existing business model rather than requiring a new one. One way to interpret the timing is that as foundation-model technology converges, the differentiation shifts to who owns the service endpoints an agent can actually call and who controls the routing decision.

What the article calls the "WeChat Moment for AI" comes with an irony worth noting: Alibaba's Qwen captured over 200 million one-sentence transactions during Spring Festival inside its own commerce stack. Tencent is building essentially the same capability, but inside the super-app where users already spend their time, and with service providers who compete with one another for the agent's selection. The unresolved question is whether businesses that pay for placement in WeChat's service grid today will pay differently when the selection is driven by an agent rather than a menu of icons."

$PDD

1

2

24

7,197

Jun 11

The prior TBC context that seems most relevant here:

- The Taobao Inside Qwen: Why Alibaba's AI Gambit Is About Re-Architecting the Internet (Apr 2026): techbuzzchina.substack.com/p…

- Tencent’s e-Commerce Revival. Part 3: Challenges & Outlook (Sep 2025): techbuzzchina.substack.com/p…

438

Jun 11

Power cost is becoming a critical constraint for China's AI infrastructure, right alongside chip access. A new data point: Alibaba has reportedly approached a nuclear power state-owned enterprise about building small modular reactors to power its Hangzhou Renhe data center, according to an SOE insider cited in Chinese media.

Renhe, opened in 2020, is a large full-immersion liquid cooling facility and China's first 5A green liquid cooling data center. The economics of dedicated nuclear power face a structural barrier: current policy requires self-owned power plants to connect to the public grid at roughly 0.58 yuan (~$0.08) per kWh. At that price, the cost advantage disappears.

We flagged this dynamic in our November 2025 piece "AI's Bottleneck Is Power": the power problem is as much about policy as physics. The discussions remain exploratory and unimplemented, but the fact that a cloud giant is even exploring this route suggests the grid-cost constraint is biting.

If Alibaba could secure dedicated power below grid rates, it would improve data center margins and reduce token costs, strengthening its cloud AI competitive position. Without regulatory change, that mechanism is blocked. The advantage may go to whoever can best manage grid-price exposure or locate in regions with cheaper power.

$9988.HK $BABA @AlibabaGroup

1

3

18

2,405

Jun 11

The prior TBC context that seems most relevant here:

- AI’s Bottleneck Is Power. The US and China Feel It Differently. (Nov 2025): ruima.substack.com/p/ais-bot…

The White House later incorporated this idea, writing into its “Building America’s AI Infrastructure” section that the U.S.

- China in the Orbital Compute Stack: Where Value Accrues (Feb 2026): techbuzzchina.substack.com/p…

The exchange underscores rising tension in 2026: is space really the next frontier for computing, or is it a high-cost distraction from terrestrial solutions?

- Why China Won’t Get Its Nvidia (Jan 2026): techbuzzchina.substack.com/p…

Content After Nvidia’s Exit The Real Map of China’s AI Chip Market Two Markets: Sustaining the Installed Base vs.

483

Jun 10

DeepSeek-V4 inference cost is down 73% vs V3.2, thanks to a self-developed algorithm adapted to Huawei Ascend 950PR chips. Cache-hit price now sits at 0.025 RMB per million tokens (~$0.0035) (roughly 1/14960 of GPT-5.5 long-context version). The result: a dev team that spent $500/month on Claude Sonnet now pays $50/month using DeepSeek.

Meanwhile, Zhipu raised API prices three times in 2026, each 30% . Tencent Cloud CodeBuddy enterprise edition up 154%. Alibaba Cloud raised AI compute/storage 5-34% in March. Video generation costs per 15-second clip have risen from 0.65 RMB to 5 RMB (~$0.09 to ~$0.69) (6.7x).

These two strategies reflect opposite bets on value capture: DeepSeek builds a developer ecosystem through cost engineering, hoping to lock in workflows before competitors catch up on domestic chip optimization. Enterprise vendors raise prices, betting that integrated tool suites (CodeBuddy, WorkBuddy) create enough switching costs to retain customers.

DeepSeek's cost lead may close in 2-3 months as competitors optimize domestic stacks. That makes the current advantage a window, not a moat. Enterprise price increases carry their own risk: Doubao MAU declined ~6.1M after price hikes, suggesting low tolerance among Chinese users.

Which bet holds: a developer ecosystem built on a ticking clock, or an enterprise suite facing churn on every price update?

6

12

62

6,700

Jun 10

For readers following China's AI model and deployment landscape, these are the earlier pieces to pull up:

- DeepSeek: Rewriting the AI Playbook for the World (Mar 2025): techbuzzchina.substack.com/p…

We made the related point there this way: "By giving complete control to external developers and organizations, DeepSeek has accelerated innovation and broadened adoption across the AI community."

- Why is China’s Video AI Industry So Good? (Mar 2026): techbuzzchina.substack.com/p…

1

540

Jun 10

You can read more about Zhou Jingren, the new Alibaba Chief Scientist, here at our China AI Atlas:

ai.techbuzzchina.com/profile…

2

496

Jun 10

Alibaba merged its Tongyi Large Model Division and Future Life Lab into a new unit called **Token Foundry**, reporting directly to group CEO Wu Yongming. The organizational change, announced June 8, also moves Zhou Jingren, the architect who built Qwen from scratch and became a partner last year, into the newly created role of Chief Scientist, where he will lead an Alibaba AI Future Institute focused on frontier research.

Zheng Bo will bring the Happy Horse and Happy Oyster teams into Token Foundry, consolidating a broader set of AI resources under one operating structure.

One way to read the restructuring is that Alibaba now considers the current generation of Qwen models commercially mature enough to warrant a CEO-direct business unit, while carving out a separate institute for longer-horizon exploration. The name itself, Token Foundry rather than Model Lab or AI Division, points to compute consumption as the organizing logic, not research output.

Zhou's shift from operational leadership to a chief scientist role reinforces that interpretation. He built the Qwen series from zero, and his elevation to what Alibaba calls the highest academic title in its technical system moves him from delivery to frontier discovery just as the company reports its AI business has crossed into commercial returns, citing Qwen-3.7's coding benchmarks as evidence.

The organizational architecture now mirrors what Alibaba has been building at the product level: a vertically integrated system where the model layer, cloud infrastructure, and commerce applications sit under one corporate roof. The open question is whether Token Foundry can convert that integration into durable cloud consumption and enterprise retention at scale.

$BABA

1

1

12

1,512

Jun 10

Huawei Cloud used its INSPIRE 2026 partner event to launch new AI solutions for manufacturing, finance, and retail, along with a support program for partners covering technology, marketing, and commercial development.

Huawei says its global business revenue grew more than 20% in 2025 and that it now works with more than 4,000 partners worldwide. The company's goal is for half of its revenue to come through partners rather than direct sales.

The broader strategy is straightforward: use partners such as system integrators and software vendors to bring AI into enterprise workflows. Instead of selling AI models directly, Huawei wants partners to build and deploy industry-specific solutions on top of Huawei Cloud.

One example highlighted by Huawei was Hengyue Cloud, which reportedly grew from zero to RMB 300 million ($41 million) in revenue over five years.

This follows Huawei Cloud's recent emphasis on enterprise AI deployment over model pricing. The company appears to be betting that adoption will be driven less by who has the cheapest model and more by who has the strongest ecosystem of partners helping customers implement AI.

One important caveat is that all of the revenue and partner figures come from Huawei itself. The company has not disclosed how much of that growth comes specifically from AI versus traditional cloud services.

The key question is whether Huawei's partner-led approach can help it deploy AI across enterprises faster than rivals that rely more heavily on direct sales or consumer products.

2

12

649

Jun 10

The departure of XPeng Robotics’ product planning lead Shi Xiaoxin is being read by some as a red flag for the IRON humanoid robot program. The company says progress is unaffected, and XPeng Chairman He Xiaopeng recently reiterated that the next-generation IRON is on track for a Q3 debut and year-end mass production, starting with in-store trials.

Shi was there from the beginning, through the integration of Pengxing Intelligence, the formation of the broader robotics unit, and the IRON’s full product definition cycle. His exit leaves the team without its most senior product-side voice at a moment when hardware design, software convergence, and launch sequencing are all being locked down.

What makes the loss notable but perhaps not crippling is where XPeng’s humanoid bet is concentrated. He Xiaopeng has been unusually direct: most robot companies have not solved the “cerebellum” problem, and XPeng’s counterpart is building precisely that layer. The IRON’s progress into the ET2 hardware-software convergence phase is, in XPeng’s framing, more about integrating perception, planning, and fine motor control than about the hardware shell.

A product planner’s departure creates uncertainty over near-term roadmap timing and feature scope. It does less damage to the stack that matters most if the company’s bet is correct: that XPeng can transfer assisted-driving AI into physical-motion intelligence faster than rivals can close the gap on the “cerebellum” itself.

The real question for IRON remains the one it was before Shi’s exit. Can XPeng turn a product built on algorithmic depth into something commercial customers will pay for, and can it do so on a timeline that makes the robot a meaningful contributor to revenue before the broader humanoid hype cycle catches up with economic reality?

2

5

1,070

Jun 10

One earlier piece is useful here:

- China's Tesla: Beyond the Car, The Structural Battle for Humanoid Robotics (Dec 2025): techbuzzchina.substack.com/p…

358