Tech investor for ~25 years. Ran large hedge fund for 10 of those. Here to help. Not investment advice. I never reach out to sell ANYTHING.

Joined July 2018

- Tweets 1,826

- Following 414

- Followers 18,836

- Likes 2,072

591 Photos and videos

Pinned Tweet

18 Nov 2024

I think there are basically 2 prevailing strategies in the market.

1) Earnings revisions

Only two questions matter near-term: Is the story getting better or worse, and are numbers going up or down? That's it.

For momentum names, in either direction, that's all that matters -> is the story continuing to improve w/ beat and raises, or is the story continuing to erode with misses / guidance reductions.

There is more complexity at extremes (ie second derivatives) that also works -> the story has stopped getting worse and numbers are no longer going down so upside optionality, or narrative no longer improving and downside risk to numbers so downside optionality.

Earnings revisions work because they are reflexive. The company is doing well, estimates are moving higher and the stock is rising. More investors do work on the name and the due diligence will be positively biased as they generally ask more favorable questions to understand the strengths of the company. This leads to more buying and the increased stock price reinforces the bullish narrative. Hopefully, management is smart enough to set forward guidance at beatable levels and the step-ups continue.

Same is true for reflexivity on the downside. A company is struggling and missing its own guidance and expectations. The stock moves lower as obviously more people sell than buy. Investors do more work but are naturally more focused on the reasons for corporate underperformance and corresponding risks. Further stock price declines fuel the negative narrative which feeds on itself. Companies often don't take their medicine as far as fully disclosing bad news and the negative revisions continue.

So again, the playbook for this is simply 1) is the story getting better or worse?, and 2) are numbers going up or down?

2) Valuation

From time to time, stocks get too cheap or expensive relative to fundamentals such that the disconnect is very interesting (let's say can make at least 50% to get back to conservative valuation target in either direction within 12-18 months).

Very often, large disconnects occur when earnings revisions are unclear to everyone (stock is really cheap but no one has any clue when numbers stabilize, stock is really expensive but everyone thinks company will continue beating / raising).

However, the insight here is that valuation is interesting in and of itself for the right kinds of companies (solid business, transitory issues, acquisition candidates, etc.). And that no one has visibility into near-term numbers is already in the stock and why the valuation is so compelling.

This opportunity also always arises in tough macro periods where everyone is frozen bc who can predict how the great financial crisis or covid pandemic plays out - so that uncertainty is shared by everyone and more than represented in stock valuations. And that is why the opportunity exists - because everyone is worried about the same imponderable thing and it's already in the stock price. The only advantage you need here is a deep understanding of and conviction in the business, and freedom / willingness to buy it for the long-term (and the returns never take as along as you think).

Reality

My experience is most investors typically only pursue one of above strategies (and might only be allowed to pursue one or the other). So they won't / can't buy $WDAY at 20x FCF bc they think guidance might be lowered (company misexecution, tough macro, etc.), or they won't sell $WDAY at 35x FCF bc they are confident everything is great and company will continue beating.

I also have found earnings revisions investors tend to have nearer-term horizons and be less valuation sensitive. This is because it's hard to fill a portfolio with names that will both beat earnings and trade at reasonable valuations. So, on balance, these investors will compromise on valuation.

Valuation investors have longer-term horizons and are by definition valuation sensitive and less sensitive to revisions. This is because it's hard to fill a portfolio with names that are both cheap and that will beat earnings. So, on balance, these investors will compromise on earnings visibility.

Optimal

I have found earnings revisions offer the most explanatory power near- to mid-term. I want to be long stocks where numbers are moving higher and short stocks where revisions will be lower.

But I also want think it is an advantage to be able to cast that strategy aside and buy companies at valuation extremes. This is when a good company is "too cheap" even if I'm not sure of near-term revisions. There are other criteria that need to be in place for this to work -> solid business w/ reasonable estimation capabilities, potential negative revisions are manageable and likely in the stock, less risk of permanent impairment over a 12-18 month horizon, balance sheet in order and not indebted, etc.

Finally, the intersection of the two is where you can nail inflection points in businesses / stocks. A company is too cheap and is about to start beating numbers which will drive both estimates and the multiple higher. That's where the big money resides.

Anyway, this overall thinking is why I structure my notes as follows:

Is this a bad, good, or great business?

Is the story getting better or worse?

Are numbers going up or down?

What is the risk / reward?

14

33

478

95,455

Well. This was wrong. SaaS shorts win again.

Update: SaaS short value 97b in total up from 90b on Friday's close. Ouch.

Weird because isn't one of the 10 Commandments "SaaS shall not trade up with Semis"? I guess it isn't ordained:)

Maybe semis and saas can make money from agents?!

2

12

9,894

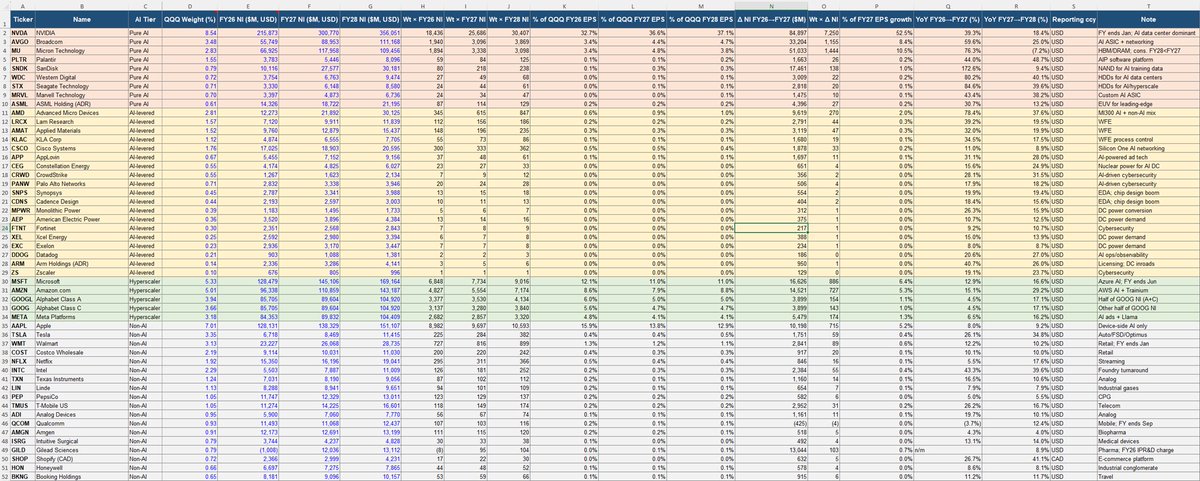

So my prior analysis was completely incorrect. And by "my", I mean "Claude and my".

You can't just take a position's weighting in the index and multiple it by each company's net income. The missing variable is the P/E for each company which moves around the underlying EPS for the bench.

So, yeah, you need to double check AI just like a person.

Interestingly, $FDS has an EPS aggregation screen for ETFs where the math is done carefully and has human-written explanatory notes. So still value in the console as well.

Revised view: QQQ is ~33% exposed to semis while SPY is ~20% which might be the cleanest way to look at it. If semis were to get cut in half, that would be a ~17% QQQ drop and ~10% SPY drop. Could be less if other names inflate as money rotates into them, could be more if it just brings everything down with it including overall multiples.

Pretty crazy that $NVDA is 33% of $QQQ 2026 EPS and 37% in 2027.

Also wild that $NVDA $AVGO $MU are 40% of $QQQ 2026 EPS and 46% in 2027.

Something to be aware of although not sure what to do with it.

Certainly relevant re @RealJimChanos pov.

2

1

14

8,329

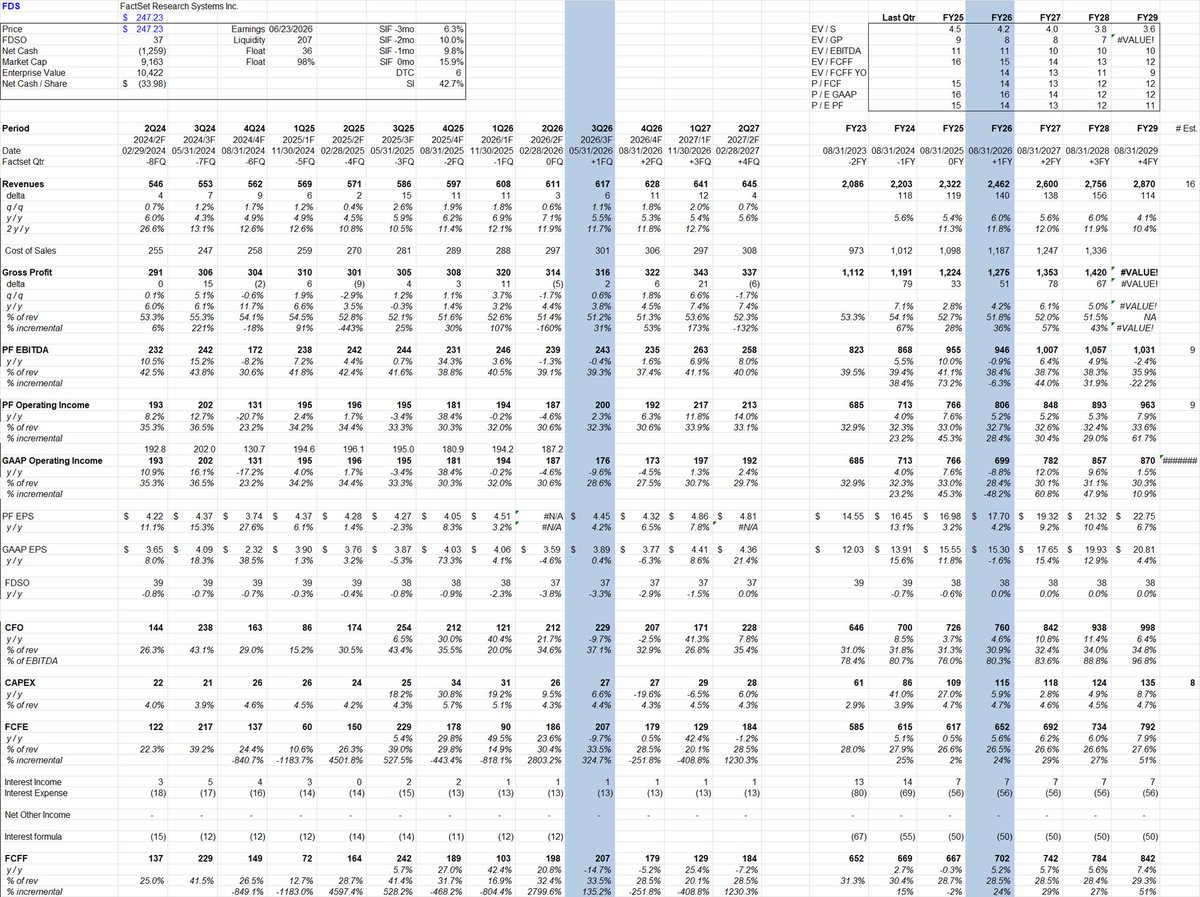

If you are a $FDS customer, be sure to call your rep.

Mine says nearly all clients are trialing the MCP, and 100% of completed trials converted to paying for the connector. 100%.

List price for the connector is a 20% uplift to contract value for the first 10 seats and then drops to an incremental 15% for additional seats. Said there has been 0 pushback on price. Single seat pricing still a work in progress as that is a minority of their business.

Stock trades at 14x this year's GAAP EPS estimate which is likely too low, and 13x next year which is highly likely to be too low...

12

2

96

22,160

Update: SaaS short value 97b in total up from 90b on Friday's close. Ouch.

Weird because isn't one of the 10 Commandments "SaaS shall not trade up with Semis"? I guess it isn't ordained:)

Maybe semis and saas can make money from agents?!

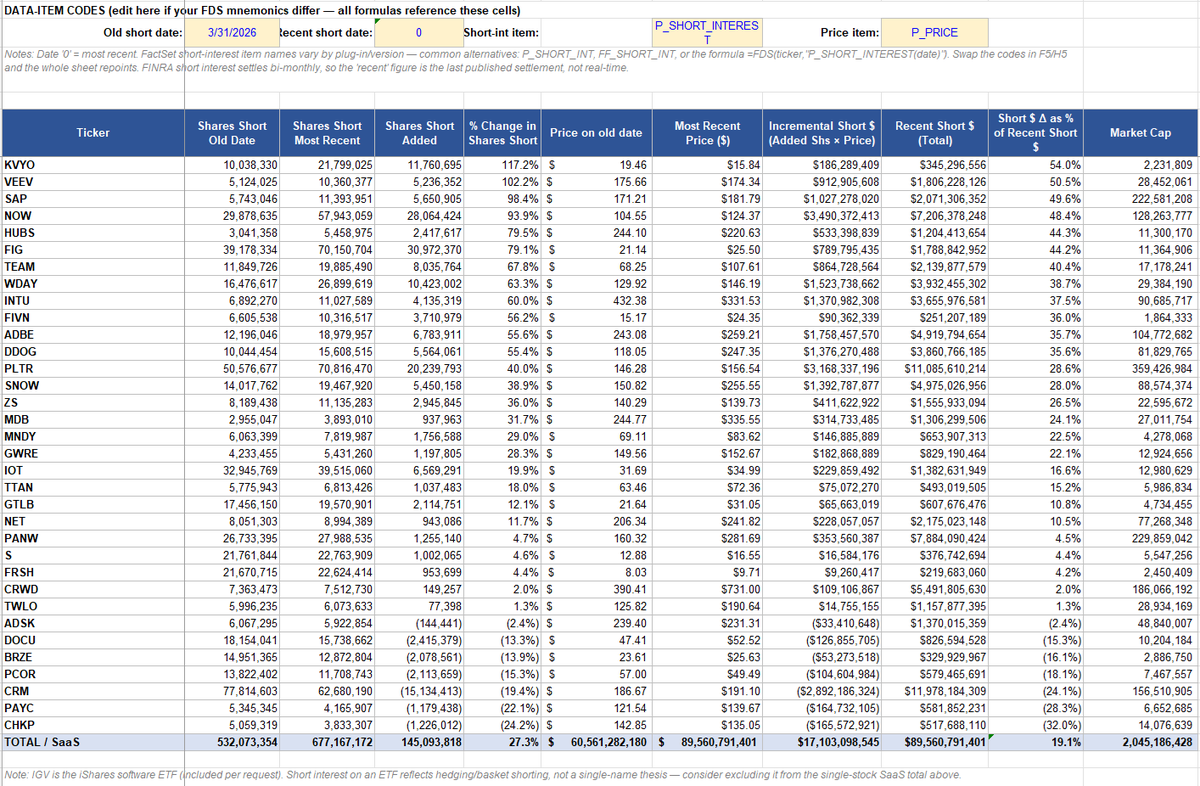

I had Claude / $FDS whip up a spreadsheet showing me how short interest in SaaS has changed since 3/31 which was more or less the bottom.

Total shares short are up 27%. Single stock short interest increased by 102% for $VEEV, 98% for $SAP, 94% for $NOW, 63% for $WDAY...

If you take the market value of shares short on 3/31 and compare it today, it has gone from ~60b to ~90b.

That's not nothing.

Market tends to do whatever causes the most pain...

(And let's be clear, if you're long semis / short SaaS, you've already made a killing so might just be time to give some back, or not).

18

16,241

I had Claude / $FDS whip up a spreadsheet showing me how short interest in SaaS has changed since 3/31 which was more or less the bottom.

Total shares short are up 27%. Single stock short interest increased by 102% for $VEEV, 98% for $SAP, 94% for $NOW, 63% for $WDAY...

If you take the market value of shares short on 3/31 and compare it today, it has gone from ~60b to ~90b.

That's not nothing.

Market tends to do whatever causes the most pain...

(And let's be clear, if you're long semis / short SaaS, you've already made a killing so might just be time to give some back, or not).

5

3

54

15,759

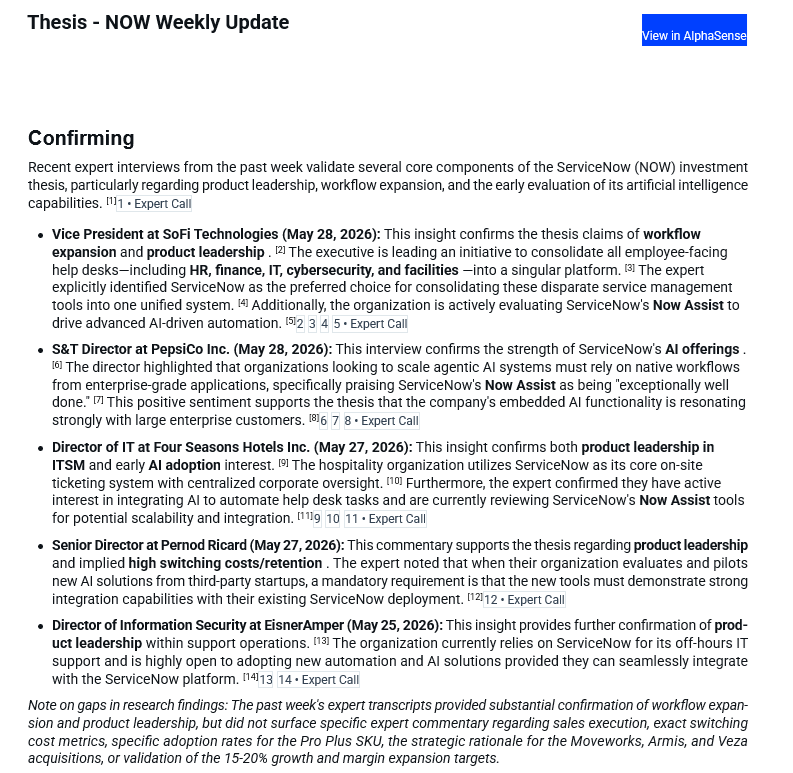

AlphaSense has proprietary expert interviews with an increasing number of them conducted by AI (which generally lowers quality per interview but more than makes up for it with additional volume).

I have an "agent" set up for each of my portfolio positions. The prompt includes my concise 1-2 paragraph investment thesis. I then have it review all relevant expert transcripts, summarize what confirms and disconfirms my thesis, and email me the result for Sunday afternoon reading.

Pretty useful.

Below is for $NOW:

9

10

194

28,084

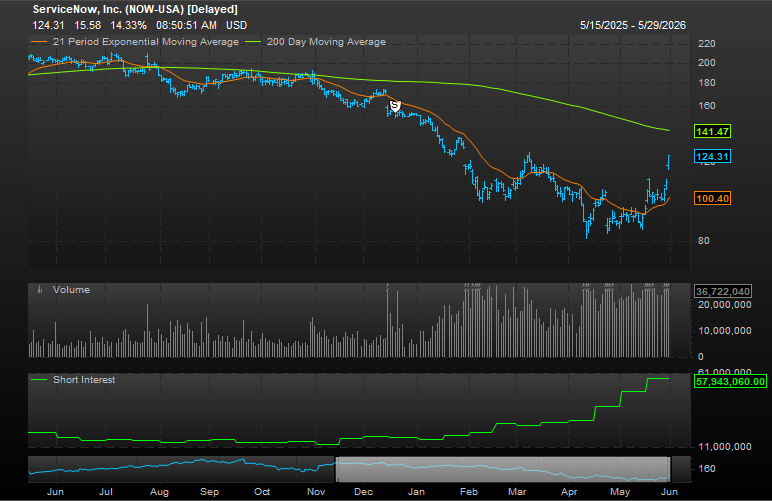

As a former and recovering short-seller, one of the best ways to know if I had overstayed a profitable short was to ask myself whether "it was too easy".

The tricky thing about a short being too easy is it's also too natural to let the downward price action tell you that your fundamental view is correct and reinforce your conviction - sometimes falsely so.

Shorting is very hard so, if it's too easy, watch out.

Because the next stage sometimes is a reversal of the crowd and that false intellectual reinforcement from the downward price action alone can trap you...

Check out these SaaS charts. They all look like this. Short interest went up ~5x - AFTER the bottom was put in. So 80% of shorts are underwater here.

Most people just can't move that quickly intellectually (myself included). Pretty hard to be yapping about how SaaS is dead all based on future projections, put on a short position, tell everyone you know about how SaaS sucks, and then quickly change your mind simply because the stocks are now going up.

Who knows if this is the start or end of a SaaS rally - just pointing out a lot of people are intellectually stuck short.

(I don't think the CRM rise in shares would be due to dealer hedging the ASR at this point but could be wrong).

3

2

49

8,854

I mean how is this not AGI?

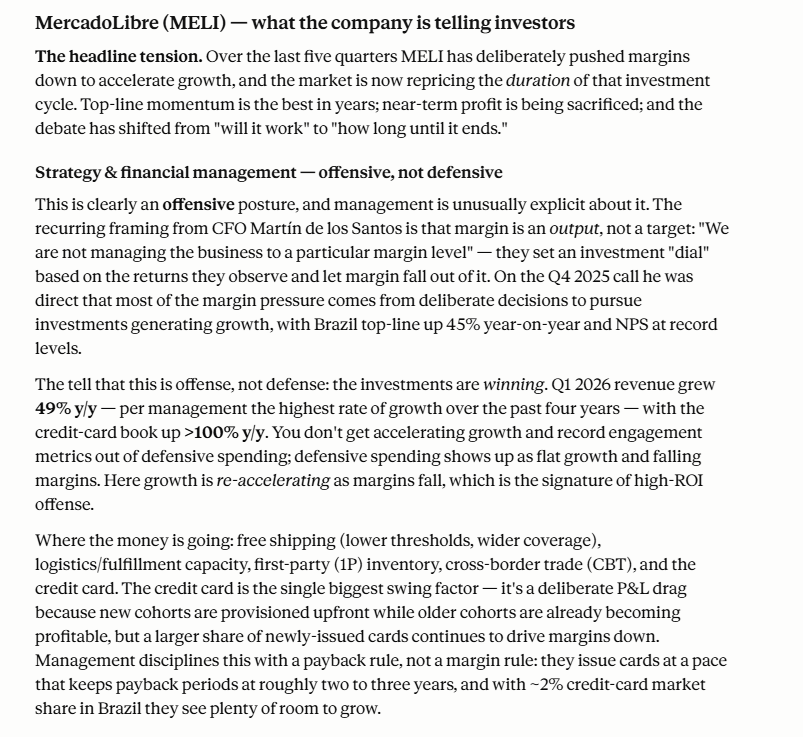

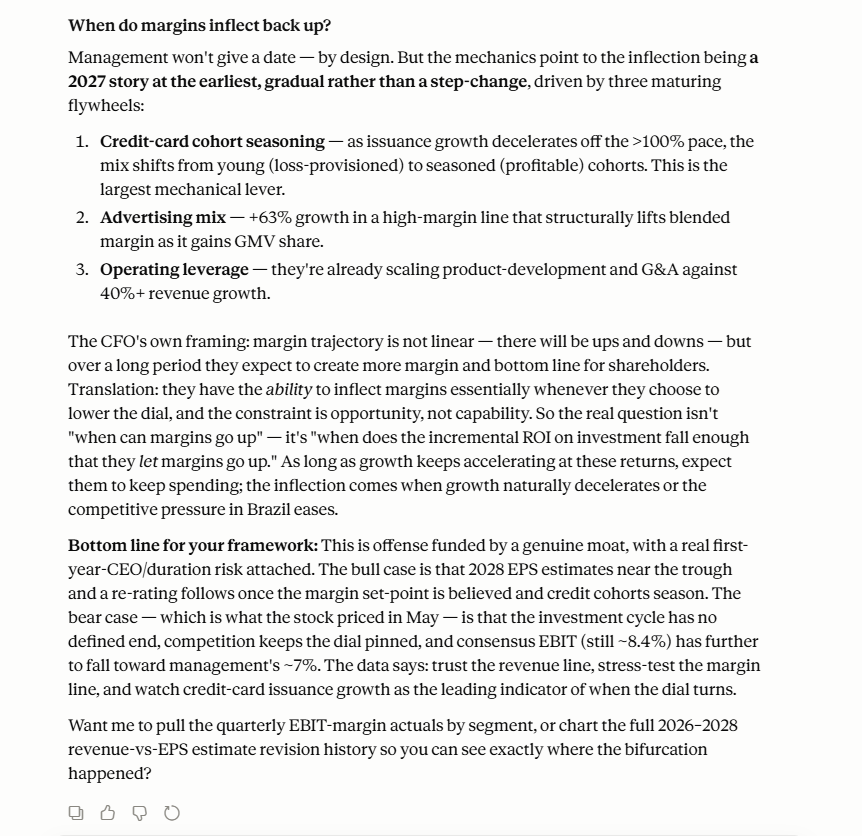

I haven't gone through MELI's last qtr. Rather than spend 1-2 hours doing that, I just asked Claude the following (w/ only $FDS MCP in the back end):

Pull the last 5 transcripts for MELI along with all conference presentations and news. Tell me what is happening with strategy, team, product, sales, competition, financial management (growth vs margins). Is the story getting better or worse, and are estimates for 2028 going to increase or decrease from here? My understanding is they are taking margins down to invest in the business so is that offensive or defensive, and when will margins increase again? Do not just rely on analyst estimates but interpret what they are telling investors and the competitive dynamic to help me think about it.

Done. In this case, risk / reward pencils out, AI says this is an investment cycle mostly in the stock, mgmt said blah blah blah, stock peaking above the 21 day EMA -> buy it. On to the weekend.

11

2

104

14,556

Follow up:

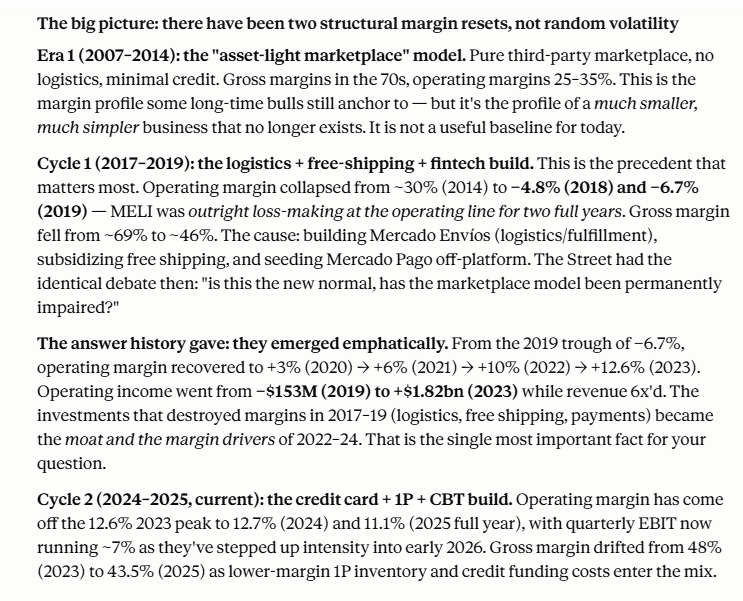

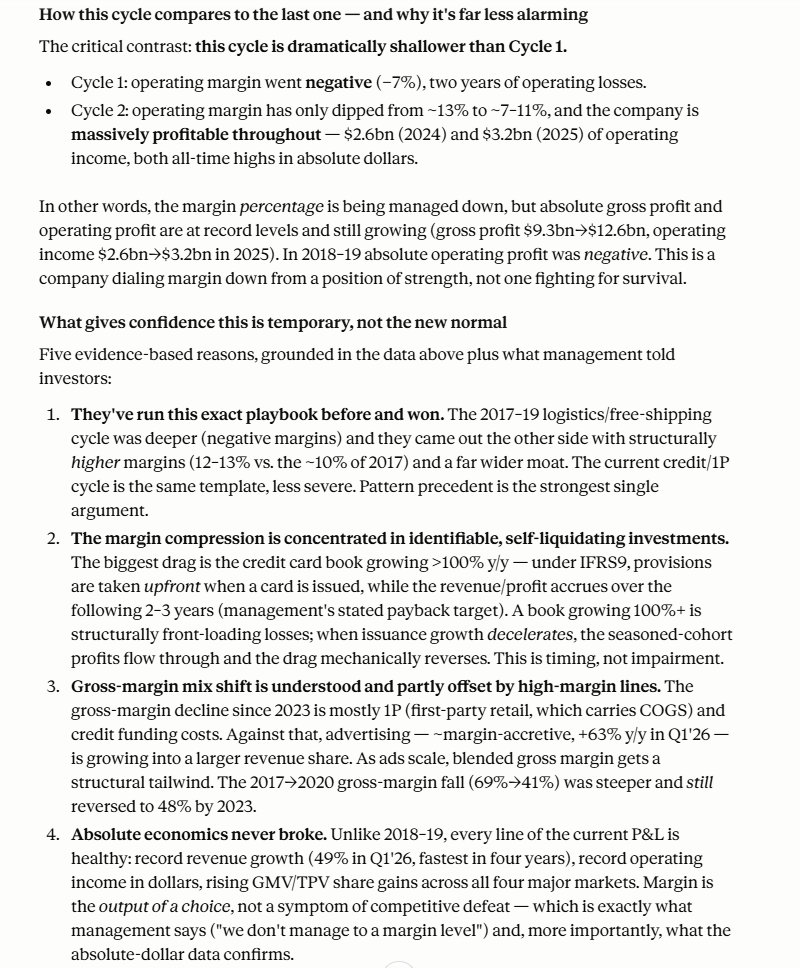

Look as far back as possible at MELI financials and focus on gross and operating margins. How does this investment cycle compare to prior ones? What gives us confidence they will emerge from this and this lower-margin isn't the new normal for the company?

Ok - maybe the stock isn't a buy yet. Turns out this investment cycle is going to on for a while. Come back to it at end of year.

3

12

2,515

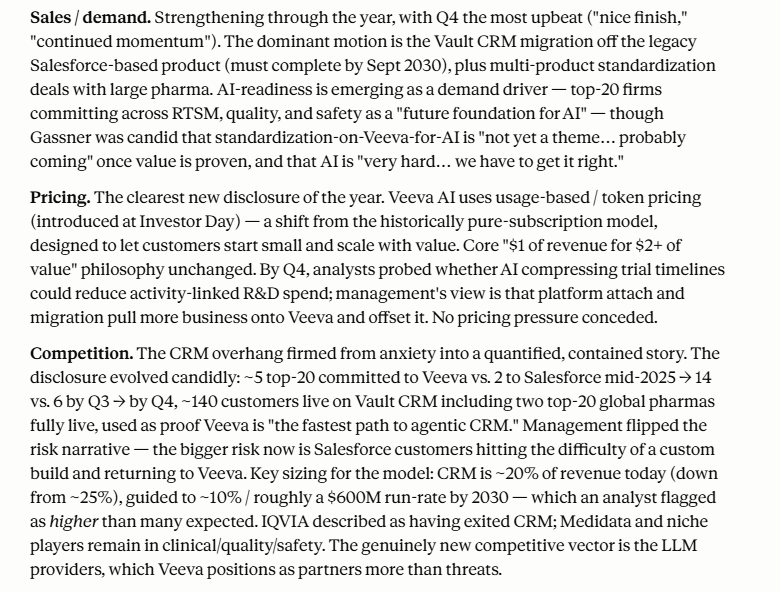

I don't know who needs to hear this but AGI is already here.

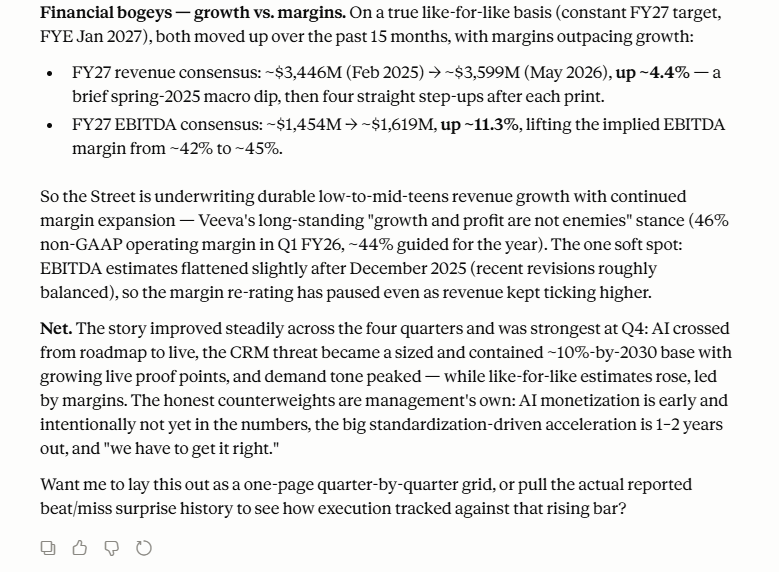

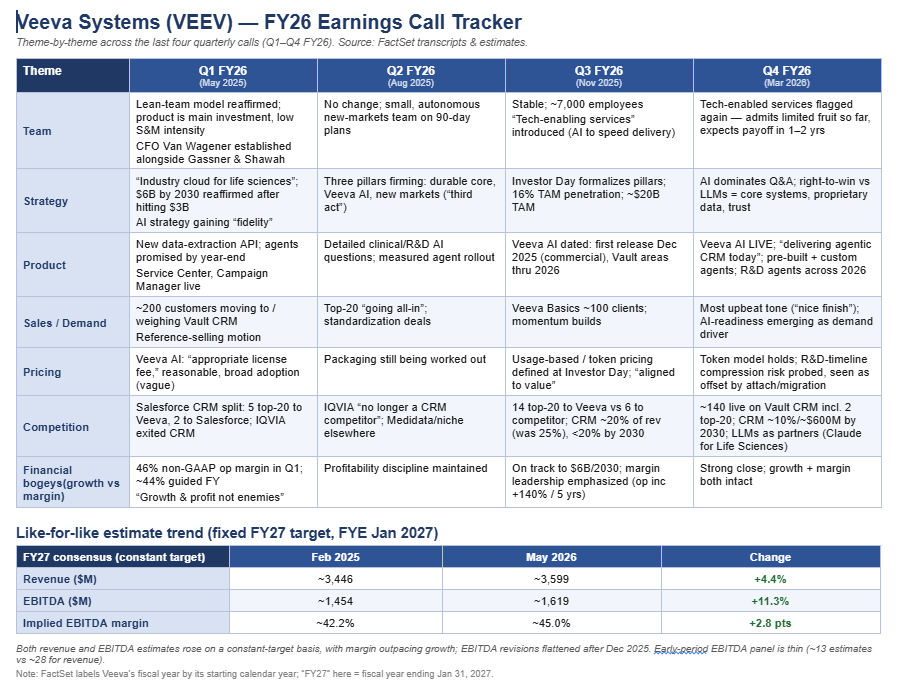

$FDS just made unstructured data available via MCP and I asked it to read four transcripts for $VEEV, update me on what's going on, tell me if the story is getting better or worse, and whether numbers are going up or down.

If this response isn't AGI, I don't know what is.

Claude costs $240 / year. $FDS MCP costs $1,500-2,500 / year.

Claude has serious COGS underneath that $240. $FDS MCP has de minimis incremental COGS.

And people are bearish on important SaaS with critical data?

Now I wonder if semis third deriv just turned negative... If all the big LLMs hit AGI within the next 12 months, the focus might shift to efficiency pretty hard.

20

10

170

33,256

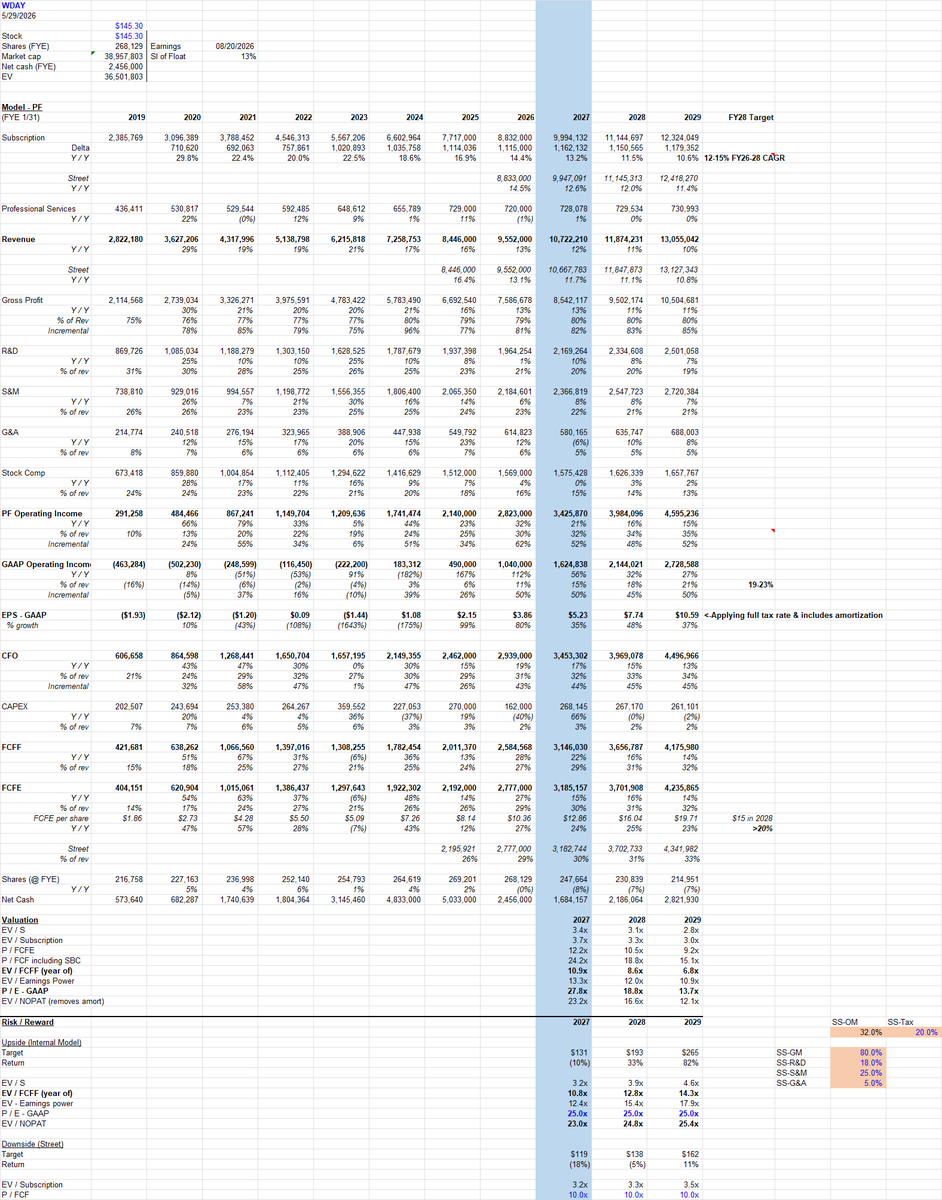

$WDAY reported a perfectly fine Q1 which is also their most irrelevant, smallest qtr.

Subscription rev grew ~13% yy cc organic and they highlighted "record NNACV" which is not what you would expect in a seasonally weak qtr that had a global conflict and all-eyes-on-Anthropic-spend.

They highlighted headcount at their customers was flattish - layoffs in tech offset by growth elsewhere.

And they highlighted that net new business drove 40% of subscription growth while 60% came from expansion. Turns out, there are still plenty of companies (mid-market) and verticals (government) that want to modernize their HCM / ERP software.

Layering AI on top of critical data / workflows is still an exploration process but their AI business is approaching 500m ACV or 5% of revenue while net new ACV in AI is growing 200% yy.

Like the rest of the industry, they are building proprietary agents, acquiring them, and largely providing them for free to start via a flex credit model. If the agents add value, then customers will pay once they cross included thresholds.

They are promoting leaders from acquired companies to infuse entrepreneurial spirit into the company which seems like a smart idea.

PF OM of 31.8% improved from 30.2% last Q1. SBC of 16.1% down nicely from 18.6%. GAAP OM of 13.3% up nicely from 9.2% and has, you know, a long way to go since the business ought to be generating 35% GAAP margins pretty easily and at this level of growth.

For the second qtr in a row, they spent ~1.5b on buy-backs. Nice to see.

Story is kind of the same here. Leading cloud HCM / ERP provider growing at a more mature rate but also managing margins more "maturely". Business is more about upselling modules across their heavily locked-in customers. But there remains white space in the mid-market, government and abroad.

AI is a tailwind as far as decreasing implementation cost for new customers, improving product velocity, and increasing upsell via new functionality introduced. But this isn't a company that's going to grow at very high rates like AI infra (and it also won't go through as rough a period when the AI infra build out cools).

Risk / reward remains stupid - even up here. Worth noting this is likely a 10-12% top line grower w/ expanding margins that drive profit growth of 25-30%.

Stock trades at 17x NOPAT on CY2027.

Upside of 80% to 25x CY2028 GAAP EPS which equates to 18x earnings power.

Downside of 5% to 10x street CY2027 FCF.

AI is the bear case or "who cares" case. If you're truly concerned about AI impact, I'd recommend hanging out with Linda in HR or Rodger in Finance to hear how excited they are to take on additional work / headaches displacing WDAY rather than just doing their jobs and planning their kids' birthday parties.

1

18

4,035

Here is the plan for $FDS:

All of you who have a FactSet terminal should immediately call your sales rep to turn on a trial of the MCP with Claude. Play with it for a day and you'll see it is the easiest value-add unlock for investing out there.

Ask yourself if your firm is going to switch from $FDS anytime soon and whether any analysts have been laid off because of AI. Answer is no to both for 99% of you - so the core business is obviously fine.

Then buy the stock ahead of the MCP ramp accelerating revenue at high margin flow-through trading at 15x NTM GAAP EPS consensus which is too low.

Then have your firm purchase the MCP from $FDS. Then call your friends who use Bloomberg which has no MCP and tell them how far behind they are (NGMI).

And then have the $FDS investment more than pay for the cost of the MCP for your investors.

12

5

133

32,588

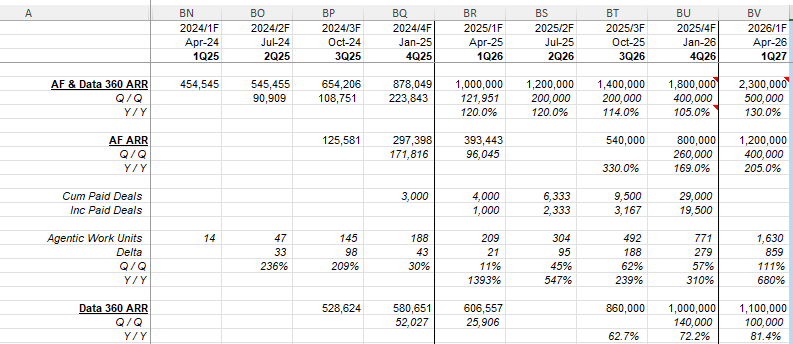

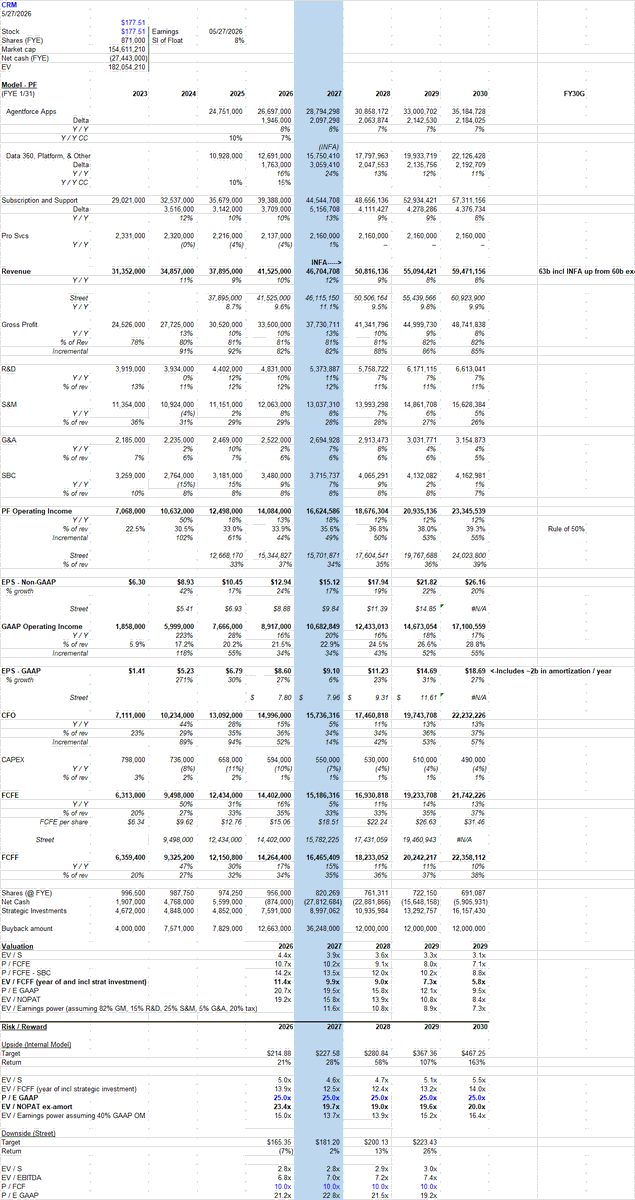

$CRM reported a fine quarter – Q1 is relatively inconsequential.

They reclassified rev segments so tougher to know exactly what's going on.

Subscription rev of 10.6b grew 7.5% yy cc organic up from 6.9% last qtr.

Under the covers, AgentForce (AF) reached ARR of 1.2b up 205% yy and added 400m in ACV in Q1 up from 260m in Q4 and 96m last Q1. It’s now up to 4% of revenue.

Data 360 reached ARR of 1.1b up 81% yy and added 100m in ACV down from 140m in Q4 but up from 26m last Q1. 50% of AF and data cloud bookings were customers re-upping credits which is a good sign about the product working in mature accounts.

They disclose an agentic work unit which is a proxy for AI consumption that is growing 680% yy. The top 10 customers of these work units increased their spend by 1.5x in the last year. Also a good sign.

As far as AI seat impact, they disclosed that total seats for both sales and service clouds increased yy and that 7 of their 10 largest deals added new seats in the qtr.

NNACV was ahead of subscription growth in Q1 as it was in 2H of last year.

The CRO seemed pretty bullish and kept reiterating that they are seeing what they expect to drive a 2H re-acceleration (although likely will be a pretty modest one).

GAAP GM of 76.9% was the same as 77.0% last Q1 so no impact from the increased AI consumption.

PF OM of 34.7% up nicely from 32.3% last Q1, SBC of 7.8% down from 8.1% last Q1, and GAAP OM of 21.8% up nicely from 20.1% last Q1. Still tons of room to go since this business ought to have 35% GAAP OM quite easily.

Avg shares outstanding decreased 7% in the qtr and will be down another 6% in Q2.

Guidance for the year was effectively kept the same. Q2 will show similar growth rates in cRPO and subscription rev as Q1, w/ an inflection in 2H. Margin guidance kept the same at 34.3% PF OM. Cash flow will grow 5-6% instead of 9-10% as they incur interest on the 25b buyback. Fine.

Thoughts

Bear case is SaaS is dead, CRM is a slow-moving conglomerate, AI won’t work, seats will contract, margins stall as they miss growth bogeys, maybe they overlever if they do big acquisitions, and who cares?

Bull case is CRM is a core system of record, AI further entrenches their position if not enhances their growth vectors, margins can double, and stock is cheap.

Seems like bear case is fully in the stock here.

Trades at 10x FCF, 14x FCF-SBC and 16x EV/NOPAT - all on this year's numbers.

So basically either mgmt. is totally lying and stock will be here at year-end, or they aren’t and stock goes up 50%. Probably will know on the Q3 print.

7

5

99

18,975

Should have also added a picture of the AI development. It's certainly solid.

1

15

6,313

Pretty crazy that $NVDA is 33% of $QQQ 2026 EPS and 37% in 2027.

Also wild that $NVDA $AVGO $MU are 40% of $QQQ 2026 EPS and 46% in 2027.

Something to be aware of although not sure what to do with it.

Certainly relevant re @RealJimChanos pov.

5

4

53

18,075