This app is my notebook. I like to post long form content on different stocks. 21 🇮🇹🇨🇦

Joined August 2018

- Tweets 6,895

- Following 247

- Followers 653

- Likes 32,612

934 Photos and videos

My $AAOI thesis that nobody has written and once you understand it you cannot look at this company the same way again.

Every civilization in history has been defined by its mastery of one medium of energy transmission.

The agricultural revolution was mastered through water, irrigation, mills, canals.

The industrial revolution was mastered through steam, pressure, pistons, engines.

The electrical revolution was mastered through copper, wires, grids, transformers.

Every era had its fundamental medium. Every era had one group of people who knew how to bend that medium to human will.

We are living through the intelligence revolution. And the medium of the intelligence revolution is not silicon. It is not electricity. It is not even data.

It is light.

Specifically, coherent, precisely modulated, terabit speed light traveling through glass fibers at frequencies the human eye cannot perceive, generated by indium phosphide lasers manufactured by fewer than a dozen facilities on the entire planet.

Without that light, AI cannot exist. Not slowly. Not expensively. Cannot exist. A GPU cluster without optical transceivers is not a slow AI system, it is $500 million of metal and silicon sitting in a room generating heat.

Now here’s what makes $AAOI extraordinary in a way nobody is saying:

$AAOI is the only U.S. company that makes its own light. Not buys light. Not sources light. Makes light. In Sugar Land, Texas. From raw indium phosphide wafers. Through a fabrication process so technically complex that there are literally less than a dozen facilities on earth capable of it, and most of them are in Asia.

Coherent buys its lasers. Lumentum buys its lasers. II-VI buys its lasers. Every competitor in the transceiver market sources the most critical component, the laser that generates the light, from a supplier. $AAOI is the supplier. They are vertically integrated from the photon up.

Here’s the thought that is currently keeping me awake near 1am lol…

America just spent five years learning the lesson of semiconductor dependency. Taiwan makes the chips. China controls the rare earths. The entire national security apparatus of the United States mobilized around the realization that the country had outsourced the manufacturing of its most critical technology to geopolitical rivals.

The CHIPS Act was the response. $52 billion to reshore semiconductor manufacturing. The largest industrial policy intervention in American history.

And while that was happening, while everyone was focused on the chip, nobody noticed that the thing that connects the chips is just as geographically concentrated. Just as technically irreplaceable. Just as strategically critical. And almost entirely manufactured outside the United States.

The indium phosphide laser. The photon source. The heartbeat of every AI system on earth.

Except in Sugar Land, Texas.

Where $AAOI is quietly expanding laser fabrication capacity by 350% by the end of 2027. Where they just received a $20.85 million Texas Semiconductor grant. Where they are building 388,000 square feet of new manufacturing. Where they are transitioning to 6 inch indium phosphide wafers, a move that will make them the most cost efficient photonic fab in the western hemisphere.

The chip companies get CHIPS Act money because Washington understood the semiconductor dependency too late. The transceiver companies are about to get the same conversation, because Washington always understands the dependency after the crisis, never before it.

$AAOI is not positioned for that conversation. They are the answer to that conversation.

now, listen…

Light does not scale the way people think it does. At 800G, the physics are hard. At 1.6T, which $AAOI begins shipping July 1st, three weeks away, the physics are almost impossibly hard. The signal integrity requirements, the thermal management, the precision of the laser modulation, all of it becomes exponentially more demanding as the speed doubles.

318

Jun 13

The most powerful moat

in the history of technology -

$RDDT

What if,

Reddit is not a social media company.

Reddit is not a data company.

Reddit is not an advertising company.

Reddit is the only place on earth

where the internet

is still alive?

In 1995 the internet was a conversation.

Real humans.

Talking to real humans.

No algorithm deciding what you see.

No brand safety team deciding what’s allowed.

No engagement optimization deciding what’s real.

Just humans.

Figuring things out together.

That internet died.

Google turned it into a library.

Facebook turned it into a performance.

TikTok turned it into a television.

YouTube turned it into a studio.

X turned it into a coliseum.

And somewhere in that transformation

the thing that made the internet magical,

the raw unfiltered collision

of human minds

trying to understand reality together,

died.

Except on $RDDT Reddit.

Reddit never optimized for engagement.

It optimized for truth.

Not because it’s moral.

Because that’s what the voting system does.

The best answer rises.

The worst answer dies.

Not because an algorithm decided.

Because humans voted.

With their attention.

Their most honest currency.

Now here’s the thought

that no one has had:

The internet is about to experience

the greatest trust collapse in its history.

AI generates 90% of new content.

Deepfakes are indistinguishable from reality.

Every article is optimized.

Every review is synthetic.

Every comment section is bots.

Every social feed is manipulation.

The entire surface of the internet

is becoming a simulation.

A very convincing simulation.

That contains no human thought.

And when that happens,

When people finally realize

that everything they read online

was written by a machine

trying to influence them,

There will be exactly one place

they trust.

The place that was never optimized.

The place that was never automated.

The place that fought the bots.

The place where a wrong answer

gets corrected

by a stranger

who gains nothing from correcting it

except the satisfaction

of being right.

$RDDT Reddit.

financial thesis:

Trust is about to become

the scarcest commodity on the internet.

Scarcer than compute.

Scarcer than bandwidth.

Scarcer than attention.

Because you can manufacture compute.

You can buy bandwidth.

You can steal attention.

But you cannot manufacture

the feeling

that the person talking to you

is real.

Reddit has 20 years

of that feeling.

Built by 493 million humans

who showed up

not because an algorithm sent them

but because they needed something

only another human could give.

An honest answer.

From someone who had nothing to gain.

Now here’s the number

that makes this a financial thesis:

Every time the internet gets less trustworthy,

Reddit’s relative value increases.

Because trust is not additive.

Trust is comparative.

You don’t trust Reddit.

You trust Reddit

more than everything else.

And as everything else

becomes less trustworthy,

Reddit doesn’t need to get better.

It just needs to stay human.

That is the lowest bar

in the history of competitive moats.

Stay human.

In a world of machines.

491 million people

who showed up

because they needed

something real.

The internet is becoming a simulation.

Reddit is the last exit

before the simulation starts.

And 493 million people

take that exit

every single week.

Not because Reddit is perfect.

Because everything else

stopped being real.

The most powerful moat

in the history of technology

is not a patent.

Not a network effect.

Not a switching cost.

It is the feeling

that the thing you are reading

was written by a human

who meant it.

Reddit is the last place

that feeling exists

at scale.

3

7

425

Jun 13

My $MRVL Thesis:

And once you see it

You cannot unsee it….

Everyone is debating

Whether custom silicon kills Nvidia.

Wrong debate.

The real question is:

Who builds the custom silicon?

Not who designs it.

Who actually builds it.

Amazon designed Trainium.

Google designed TPU.

Microsoft designed Maia.

Meta designed MTIA.

Apple designed M4.

Every hyperscaler

Spent billions

Designing their own AI chip.

To escape Nvidia.

And every single one of them

Called the same company

To actually build it.

Marvell.

Not to manufacture it.

TSMC manufactures it.

To architect it.

To take the hyperscaler’s idea

And turn it into silicon reality.

To solve the problems

That happen between

“We have a concept”

And

“We have a chip.”

Here’s what nobody understands about custom silicon:

Designing a chip is the easy part.

A thousand engineers with good ideas

Can design a chip.

Making that chip

Talk to memory at terabyte speeds.

Talk to other chips across a data center.

Talk to the network.

Talk to the storage.

At 99.999% reliability.

At scale.

In production.

That is the hard part.

That is what Marvell does.

Marvell is the custom silicon whisperer.

The company that takes

A hyperscaler’s dream

And makes it manufacturable.

Marvell doesn’t just build chips.

Marvell builds the entire data layer.

The interconnects.

The SerDes.

The optical DSPs.

The networking silicon.

The storage controllers.

Every single layer

Between the compute and the world.

Think about what that means.

Nvidia owns the GPU.

TSMC owns the fab.

But between the GPU and everything else..

Between compute and memory.

Between chip and network.

Between server and data center.

Between data center and the internet.

Marvell owns every crossing.

Every border.

Every handshake.

Between every component

In every AI system

Built by every hyperscaler

On earth.

Now here’s the number that proves it:

Custom AI silicon revenue growing 73% year over year.

$1.8 billion in Q1 FY2027 revenue, up 61%.

Data center revenue $1.6 billion, up 73%.

Six hyperscalers.

Each one designing their own chip.

Each one depending on Marvell

To make it real.

Here’s the truly raw insight:

The hyperscalers built custom silicon

To escape dependency on Nvidia.

And accidentally created

A deeper dependency on Marvell.

Because Nvidia has one customer relationship:

The hyperscaler buys the chip.

Marvell has an organism relationship:

The hyperscaler cannot build

Without Marvell’s DNA

Inside every system.

Nvidia $NVDA is the brain.

Micron $MU is the memory.

$AAOI is the nervous system.

And Marvell?

Marvell is the genetic code.

The underlying architecture

That determines how every component

Talks to every other component.

You can replace a brain.

You can replace memory.

You can replace a nervous system.

You cannot replace the genetic code

Without rebuilding the organism from scratch.

Amazon rewrote its genetic code for Trainium.

It took four years and billions of dollars.

And they still needed Marvell

To make it work.

That is not a vendor relationship.

That is a biological dependency.

$MRVL.

Not the chip.

The genetic code

Of artificial intelligence.

Six hyperscalers.

One genetic architect.

61% revenue growth.

The custom silicon revolution

Was supposed to create competition.

It created a monopoly.

Just not the one anyone expected

3

1

7

1,426

Jun 13

$ONDS isn’t a drone stock. It’s not even really a “defense hardware” stock anymore.

This is my thesis:

They’re building the operating system for autonomous multi domain operations, the layer that actually makes swarms, robots, sensors, and effectors fight (or protect) as one coordinated thing in real contested environments.

Omnisys = real time battle resource optimizer (Israeli combat-proven).

LADOS = the C2 execution layer wiring everything together (just dropped for Eurosatory).

SkyWeaver (Palantir powered) = the agentic AI brain on edge.

Physical assets = balloons for persistent ISR, drones, ground bots, C-UAS, demining.

Closed loop in contested environments.

That’s why orders are flooding in and guidance got blown out to $390M .

Hardware is easy. The orchestration layer that makes it all work together is the real edge.

This is the one no one’s fully pricing yet.

1

3

968

Jun 11

Everyone is asking if

Waymo kills $UBER.

Wrong question.

Henry Ford didn’t invent the car.

He invented the assembly line.

The infrastructure that made every car inevitable.

$Uber didn’t invent ride sharing.

$Uber built the station.

The station every future transportation technology has to run through.

Because the station has the passengers.

Waymo already came through Uber’s station.

WeRide came through.

Volkswagen came through.

They all came through.

Not because Uber forced them.

Because 170 million passengers are there.

And passengers don’t move.

They stay where the habit is.

3.6 billion trips last quarter.

50 billion lifetime trips by 2027.

50 billion moments a human said:

“I trust this company with my body.”

That is not a dataset.

That is the deepest commercial relationship

In the history of transportation.

Built on the most primal human instinct.

Physical safety.

No autonomous vehicle company

Wins by building a better car.

The competition was never about the car.

It was always about who owns the moment

A human decides to move.

$Uber owns that moment.

They didn’t build the car.

They built the station.

And every car ever built

Eventually needs a station.

1

1

11

1,018

Jun 11

Here’s the thing about $AAOI that will make you question how you think about AI.

Everyone is counting GPUs.

Nvidia GPUs. AMD GPUs. Custom silicon.

The entire AI investment thesis for three years has been:

More compute. More chips. More processing power.

Wrong.

The bottleneck was never compute.

It was always light.

Here’s what I mean…

A GPU cluster without transceivers is not a slow AI system.

It is not an AI system at all.

It is $500 million of silicon sitting in a room.

Unable to talk to itself.

The GPUs don’t think alone.

They think together.

And the only way they talk to each other,

Is through light.

$AAOI light.

Now here’s the part that nobody has said out loud:

Nvidia $NVDA sells the brain.

$AAOI sells the nervous system.

The most intelligent brain ever created

Is completely useless

Without a nervous system to connect it.

Now here’s where it gets truly revolutionary:

The AI industry has spent $700 billion on brains.

And roughly $15 billion on nervous systems.

That ratio is not sustainable.

You cannot scale intelligence

Without scaling connectivity.

And connectivity scales with light.

Specifically,

Indium phosphide light.

Made in one place in America.

Texas.

But here’s the thought nobody has had yet:

What happens when AI itself starts designing the transceivers?

$AAOI is already using AI to optimize laser fab yields.

The feedback loop is beginning.

AI improving the component that enables AI to exist.

A recursive loop between intelligence and light.

Between the brain and the nervous system.

Accelerating each other.

Indefinitely.

The chip companies get valued as if compute is infinite.

The transceiver companies get valued as if light is a commodity.

Light is not a commodity.

Light at 1.6 terabits per second

Manufactured from indium phosphide

In a vertically integrated facility

On American soil

By 22 year trained engineers

Who took a decade to learn how to do this

Is one of the scarcest industrial capabilities on earth.

$NVDA Nvidia: $3.3 trillion.

The company making the nervous system that makes Nvidia’s brains actually work:

$13 billion.

The brain gets $3.3 trillion.

The nervous system gets $13 billion.

Evolution never produced a brain without a nervous system.

The nervous system of artificial intelligence.

Valued at 0.4% of the brain it serves.

That gap is either the greatest mispricing in technology history.

Or the market knows something.

I think it’s the former.

And July 1st,

When 1.6T shipments begin,

Is when the market starts to agree imo.

3

322

Jun 10

I was wrong..

$ORCL is looking to raise another $40b lol, Zuckerberg $META

and Ellison should shake hands.

Selling in the morning.

Jun 10

Doing my first earnings play of the szn today on $ORCL

All about the “demand” story.

I believe we see explosive growth and more added to the backlog

1

4

694

Jun 10

Doing my first earnings play of the szn today on $ORCL

All about the “demand” story.

I believe we see explosive growth and more added to the backlog

4

946

Jun 10

So I initiated a new position today..

I was hunting for pure play AI exposure without paying insane mega cap multiples, and found $CEVA.

They don't make physical chips, they license the intellectual property (IP) blueprints for low power wireless, smart sensing, and Edge AI.

The Financial Turning Point:

The Q1 2026 numbers just proved the ship is turning. Revenue hit $27.0M (up 11% YoY), beating Wall Street estimates. But the real story is licensing revenue, which surged 18% to $17.8M, a 3 year high. This means chip designers are aggressively spinning up new projects using CEVA's tech today.

Insane Financial Leverage:

Because they run a pure IP model, they boast ridiculous 87% non GAAP gross margins. Once these upfront licensing wins transition into mass production, high margin royalties flow straight to the profit line. Non GAAP EPS hit $0.04 last quarter, doubling analyst expectations.

The Shift to "Physical AI":

AI is rapidly moving out of massive data centers and onto local devices (the Smart Edge). CEVA’s NeuPro NPUs handle heavy AI workloads locally without killing batteries. Advanced Edge AI now commands over 20% of their total licensing business and is growing fast.

———

CEVA’s AI architecture is baked into the Renesas R-Car platform, which is actively shipping inside the mass volume 2026 Toyota RAV4.

They are deeply embedded in NXP Semiconductors' next gen software defined vehicle (SDV) processors.

————

The Arm Multiplier:

CEVA recently joined forces with $ARM in the Arm Total Design ecosystem. They are co developing integrated 5G and satellite chiplets that fuse Arm CPUs with CEVA wireless blocks. This gives them a massive, direct pipeline to Arm’s entire global customer base.

Built Like a Fortress:

CEVA is a small cap with zero long term debt and $215M in liquid cash. That cash alone makes up roughly 18% of their entire $1.2B market cap, giving them a massive safety net to fund R&D and absorb market volatility.

I believe these new

(also some not announced) licensing wins may trigger an absolute hyper growth wave of royalties. With the foundation set and macro tailwinds blowing hard toward ultra low power Edge AI, $CEVA is sitting right in the sweet spot.

1

1

367

Jun 8

Reddit Is Going To Eat Google.

$RDDT $GOOGL

Hear Me Out…

Not the search engine.

The business model.

Here’s what I mean.

Google’s entire $200 billion advertising empire is built on one insight from 1998:

Capture the moment someone knows what they want.

The search bar.

The most valuable real estate in the history of commerce.

Because the person typing into it has already made a decision.

They just need the destination.

Google charges for the destination.

But here’s what nobody has noticed:

The search bar is dying.

Not because of AI.

Because of a behavior change that started years ago and is now irreversible.

People stopped trusting destination pages.

They trust people.

Specifically… they trust people who have no reason to lie to them.

So they started typing

“site:reddit com” after every

Google search.

And then they stopped bothering with Google first.

They just went to Reddit.

Because Reddit has something Google structurally cannot:

The moment BEFORE someone knows what they want.

The consideration phase.

The confusion phase.

The “I don’t even know what questions to ask yet” phase.

This is not a small thing.

This is the entire uncaptured value of human commercial intent.

Google captures intent AFTER it crystallizes.

Reddit captures intent WHILE IT FORMS.

These are not the same thing.

The person Googling “buy noise cancelling headphones” has already decided.

The person on Reddit asking “are noise cancelling headphones actually worth it” is about to decide.

That second person is more valuable to every advertiser on earth.

Because they can still be influenced.

Google cannot access that person.

Reddit already has them.

Now here’s the raw financial implication:

Google’s search advertising ARPU: ~$40 per user.

Reddit’s advertising ARPU: ~$5.23 per user.

That gap is not a reflection of different user value.

That gap exists because Reddit has never charged for what it actually has.

The pre intent moment.

The consideration phase.

The “I’m about to spend money but I don’t know on what yet” human.

Shopping carousels are the first toll booth on that highway.

Reddit Answers is the second.

The Shopify integration is the third.

Each one moves Reddit one step closer to owning the moment that Google has never been able to reach.

The moment before the search.

When advertising is not an interruption.

It’s an answer.

Google built a $2 trillion company on capturing what people want.

Reddit is building something on capturing why people want it.

That is a different business.

A more valuable one.

And the $7 trillion dollar gap between their market caps

is the most mispriced spread in the history of the internet.

$171. $31B market cap.

Google owns the moment after the decision.

Reddit owns the moment the decision is born.

The moment before has always been worth more.

Nobody charged for it.

Until now.

1

5

592

Jun 7

I’m not buying $SPCX at $135, and honestly neither should you…

Here’s my honest case against, and it’s damning.

Let’s start with the number nobody wants to say out loud:

*SpaceX lost $4.9 billion in FY2025.*

The largest IPO in human history.

Is losing $5 billion a year.

At a $1.75 trillion valuation.

That is 109x~ revenue on a money losing business.

For context:

Nvidia $NVDA, the most important technology company of the decade, trades at 25x revenue.

Apple trades at 8x revenue.

Google trades at 6x revenue.

You are being asked to pay 109x revenue for a company that lost $4.9 billion last year.

Now let’s talk about what you’re actually buying…

Dual class share structure. Elon Musk retains full voting control.

You are not buying SpaceX.

You are buying a financial claim on SpaceX’s cash flows with zero ability to influence any decision the company makes. Ever.

Musk can dilute you. He can pivot the mission. He can redirect capital to Mars, literally, and you cannot stop him.

You are a passenger. With no seat at the table. Who paid $135 for the privilege.

The Starlink bull case has a ceiling nobody is modeling:

Starlink is a rural and emerging market internet provider. The total addressable market for premium satellite broadband at $120/month is not 8 billion people. It is the fraction of the global population without terrestrial broadband who can afford $120 per month.

Amazon Kuiper launches commercially this year. OneWeb is operational. The competitive moat in satellite broadband is not permanent, it is a head start.

The xAI merger raises more questions than it answers:

SpaceX absorbed xAI in February 2026.

xAI had a separate valuation. Separate investors. Separate cap table.

The all stock merger that created this “AI conglomerate” narrative, how were xAI shareholders valued? What did SpaceX shareholders give up? What synergies have been independently verified?

The answer: nobody outside SpaceX knows. Because there was no independent board to negotiate on your behalf. Musk sat on both sides of that transaction.

The IPO timing is the most bearish signal of al imo.

Companies go public when their insiders want liquidity.

Elon Musk’s 42% equity stake will be worth more than $735 billion at the IPO valuation.

The people who built SpaceX from zero are selling you shares at $1.75 trillion.

Ask yourself: if SpaceX was clearly worth $5 trillion in five years, why sell now?

The historical IPO data makes this worse:

Every major $SPCX related announcement, the April 1 filing, the May 20 S-1, the June 12 listing reports, generated negative $TSLA returns averaging -4%~ per event.

The market is already telling you something. Every time this IPO gets more real, capital rotates out.

The retail carve out is not generosity. It’s distribution.

30% allocated directly to retail through Robinhood, Fidelity, and Schwab.

The largest institutional investors on earth, who have the analytical resources to price this properly, were not given 100% of the deal.

30% went to people buying on FOMO through a phone app.

*That is not a flex. That is a tell.*

The summary:

$1.75 trillion valuation.

$4.9 billion net loss.

109x revenue.

Zero shareholder governance.

Competitive satellite broadband market.

Insider liquidity event.

Retail FOMO distribution strategy.

The greatest businesses in history were built by people who didn’t need your money to keep going.

SpaceX is raising $75 billion.

Think about why.

10

2

23

3,580

Jun 6

Is Robotics The Next Sector To Run?

If so, Symbotic is the answer. $SYM

🔭 Why This Is The Right Answer, Not Necessary The Obvious One:

Everyone talking about the robotics boom is naming Tesla Optimus, Figure AI, Boston Dynamics, and Nvidia. They are all private or embedded inside larger companies. You cannot buy a pure play humanoid robot stock today that has real revenue, real customers, a real backlog, and real profitability.

Symbotic is different. It is the only publicly traded AI robotics company that has already crossed the threshold from demonstration to deployment at industrial scale, and is doing it inside the largest retail supply chain on earth.

Symbotic has been named one of the World’s Most Innovative Companies of 2026 by Fast Company, alongside Google, Nvidia, Adidas, and Walmart.

Google. Nvidia. Adidas. Walmart. Symbotic.

That list tells you everything about where this company sits in the technology landscape right now.

Revenue:

Fiscal year 2025 revenue of $2.25 billion, up 25.65% year over year from $1.79 billion.

Q2 fiscal 2026 guidance of $650–$670 million. Revenue projected to cross $3 billion in fiscal 2026 as more GreenBox facilities go live.

The GreenBox deployment model is the flywheel. Every GreenBox system Symbotic installs at a Walmart, AWG, or new customer generates: upfront hardware revenue, recurring software subscription revenue, and ongoing maintenance contracts. Each installation is a permanent, compounding revenue stream that grows as the customer expands to more facilities.

The record backlog: $22.4 billion.

$22.4 billion in contracted backlog. Against $2.25 billion in annual revenue. That is nearly 10 years of current revenue already contracted. No other robotics company on earth has this level of commercial validation.

Why $SYM ?

Humanoid robots are trying to replace humans in environments designed for humans. It’s extraordinarily hard. The environments are unstructured. The tasks are unpredictable. The safety requirements are extreme.

This is where they come into play:

Symbotic operates in controlled warehouse environments purpose built for its technology. Every square foot of a Symbotic enabled warehouse is designed around the system. The SymBots, small, fast, autonomous mobile robots, operate at speeds humans cannot match in a three dimensional vertical storage system that extracts maximum density from every cubic foot of warehouse space.

Symbotic develops technologies to enhance operating efficiencies in modern warehouses, automating the processing of pallets, cases, and individual items with AI powered robotic systems. The new modular system design is a catalyst for faster deployment and improved system efficiency, expected to drive a significant step change in growth.

The new modular system is the most important recent development. Previously, Symbotic systems required custom-built facilities with long installation timelines. The modular architecture allows faster deployment across more customer types, opening the TAM dramatically beyond Walmart scale retailers.

Profitability:

Recent earnings showed a return to profitability alongside higher revenue guidance!!

——

The robotics boom everyone is predicting is going to benefit exactly two categories of companies: the ones making humanoid robots (mostly private) and the ones actually deploying AI powered autonomous systems at commercial scale right now.

Symbotic is the only public company in the second category.

5

1

10

1,672

Jun 5

This may sound psychotic but hear me out.

What if the brutal $MU drop is the exact setup Trump and friends needed to buy lower?

(Maybe USA investment?)

The timing lines up too well. Trump personally bought between $500K~ in $MU shares back in March 2026, then went on Fox calling it “one of the hottest companies.”

Fast forward to now:

Micron’s $200B U.S. manufacturing expansion is still rolling full steam, second fab in Boise, Virginia modernization onshoring advanced DRAM from Taiwan, all backed by the administration and CHIPS funding.

Just last month (May 22) they hit another milestone in Virginia, with Commerce Secretary Lutnick and Trump officials publicly cheering the quadrupling of U.S. memory production for AI, defense, autos. CEO Mehrotra keeps thanking the Trump team for the policy tailwinds.

Meanwhile the fundamentals are still great:

Q2 FY26 revenue exploded to ~$23.9B (nearly 3x YoY), record 74.9% gross margins, EPS crushed at $12.20. • Q3 guidance: $33.5B revenue and ~81% margins, entire 2026 HBM capacity already sold out to hyperscalers on multi year contracts.

CEO explicitly said the memory shortage lasts well beyond 2026. AI data center capex hasn’t even peaked yet.

So yeah… a sharp pullback right before earnings after a monster run...

Or, if you’re feeling conspiratorial, the perfect window for Trump (or any smart money aligned with the administration) to average in lower on the only U.S. headquartered memory leader with real HBM pricing power and domestic fabs.

Interesting to say the least.

2

391

Jun 4

This Friday could be one of the most important days in $RDDT ’s history.

The S&P 500 quarterly rebalance announcement drops after market close on Friday.

Reddit is one of the named candidates for inclusion.

Here’s why this matters more than most people realize, and why Reddit deserves it.

S&P 500 changes are announced on the first Friday of the last month of each quarter. Changes go into effect two weeks after the announcement. Every index fund, ETF, and passive vehicle tracking the S&P 500, collectively managing trillions in assets, must buy the stock upon inclusion.

That is not optional buying. That is forced buying. By every passive fund on earth simultaneously.

does Reddit actually deserve to be in the S&P 500?

Let’s check the boxes:

Market cap? $32 billion. ✅

U.S. domiciled, NYSE listed? ✅

Positive GAAP earnings most recent quarter? ✅

Positive GAAP earnings trailing twelve months? ✅

Liquidity? 493 million weekly users. One of the most traded stocks on the NYSE. ✅

Now here’s what makes the inclusion case genuinely compelling beyond just the criteria:

Reddit just reported Q1 2026 revenue of $663 million, up 69% year over year. 91.5% gross margins. $311 million in free cash flow. $2.77 billion in cash. Zero meaningful debt.

It is one of only two companies on earth with:

- Greater than 40% revenue growth

- Greater than 30% free cash flow margins

- Greater than 90% gross margins

Simultaneously.

The S&P 500 contains companies growing at 3% with 15% margins.

Reddit’s financial profile is elite by any standard.

If it happens, every S&P 500 index fund on earth becomes a forced buyer.

If it doesn’t, the business doesn’t change.

1

1

14

2,275

Jun 3

$AVGO CRASHES TO PRICES NOT SEEN SINCE… LAST WEEK

😂

EPS: $2.44 vs. $2.40

Revenue: $22.2B vs. $21.7B

Q3 Guide:

- Rev $29.4B vs $28.6B est

- EBITDA $20.0B inline with $20.0B est

*CEO ON INCREMENTAL AI DEMAND

“Customers have been coming to us incrementally over the last few months. Expect that to continue. And by and large, yes.”

9

968

Jun 2

I bought $HPE at $54~

Here’s why -

This morning HPE reported earnings and the stock flew.

But here’s what most people chasing this move don’t understand:

The numbers aren’t the real story.

$HPE ’s FY2026 is now tracking ahead of what management had previously targeted for FY2028!

They pulled their entire long term plan forward by two years in a single quarter.

Two years. Pulled forward. In one print.

The numbers:

$10.7 billion in revenue, up 40% year over year. Non GAAP EPS $0.79, 52% above the high end of guidance at $0.55. Free cash flow $915 million, up $1.8 billion year over year. AI systems orders $1.8 billion in the quarter alone.

Cumulative AI systems bookings: $16.4 billion.

FY2026 EPS outlook raised to $3.35 - $3.45, up over 40%. Free cash flow raised to at least $3.5 billion, up 75%.

Networking surged 148%. Servers jumped 33%. Q3 guidance: $11.5–$12.1 billion.

Now here’s the part nobody is saying:

CEO Antonio Neri stated on the earnings call: “We have no evidence in our orders or backlog of any pull-ins. We have no cancellations. The demand is durable.”

No pull ins. No cancellations. Durable demand.

*That is the most important sentence in the entire transcript*

Every bear argument on AI infrastructure stocks rests on one thesis:

hyperscalers are over ordering today and the cliff comes in 2027.

$HPE just said, under oath on a public earnings call, they see zero evidence of that.

$16.4 billion in cumulative AI systems bookings. Record backlog entering Q3. Juniper integration ahead of schedule. Networks for AI order target raised to at least $2 billion for 2026.

The thesis just got confirmed in the most public way possible.

1

1

10

1,252

Jun 2

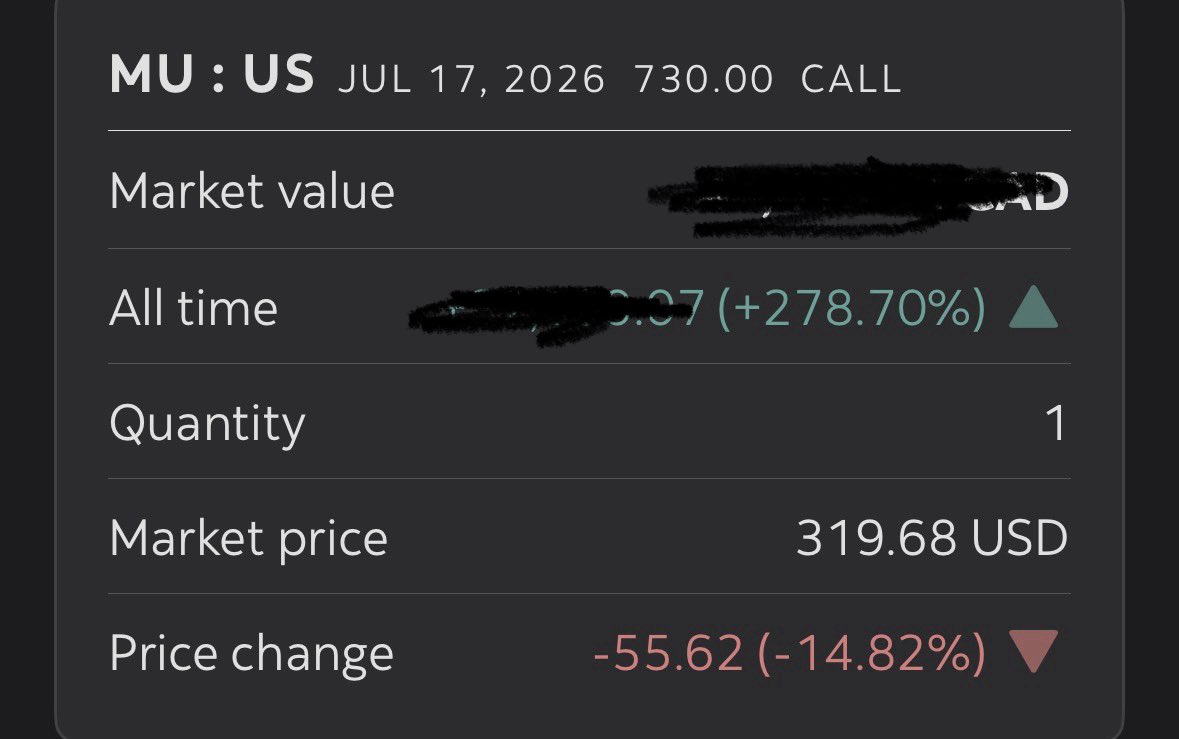

I just don’t see how $MU ’s run currently is “priced in” or “peak cycle” after the monster rip to $1T market cap.

Dare I say this supercycle still feels “early” for the memory names that actually matter in AI?

These are some things that have me staying long $MU:

• Q2 revenue exploded to $23.86B, nearly 3x YoY from $8B last year.

• Gross margin hit a record 74.9% (up huge on pricing power and mix). Non GAAP EPS $12.20, crushed estimates.

• Q3 guidance: $33.5B revenue and ~81% gross margin.

• Entire 2026 HBM capacity already sold out to the hyperscalers. Multi year contracts, zero inventory risk, and AI data center capex still ramping

• Balance sheet is an unbelievable: $16.7B cash, massive FCF ($6.9B adjusted in Q2 alone), and they’re throwing capex at U.S. fabs while printing money.

• Forward P/E still looks cheap

The moat here is real:

HBM leadership supply discipline direct AI tailwinds that the old memory cycles never had.

I’m truly seeing a multi year platform where margins stay elevated and revenue keeps compounding.

AI is here to takeover, and it needs lots of memory.

2

224

May 31

There’s a $RDDT partnership nobody is talking about, and its one of there best.

On January 15, 2026, Emplifi quietly integrated Reddit’s Enterprise API into its platform.

Most people skipped this headline. They shouldn’t have.

Here’s what actually happened:

Emplifi serves retail, CPG, sports, and consumer brands globally. Its entire value proposition is turning consumer intelligence into business decisions.

And it just made Reddit’s community signals the primary analytical input for that intelligence.

The partnership positions Reddit not just as a listening source, but as a key analytical signal for Emplifi’s intelligent execution engine. Brands can now turn unfiltered consumer discussions into aggregated insights that drive specific, recommended business objectives.

Read that again. Reddit is no longer being treated as a social platform to monitor.

It’s being treated as a business intelligence terminal.

Here’s what that distinction means financially:

Social monitoring is a $5/month line item.

Business intelligence infrastructure is a $50,000/year enterprise contract.

The same Reddit data. Completely different pricing power.

Emplifi called Reddit’s 100,000 communities “the internet’s largest focus group turned into a driver for revenue and operational agility.”

That is not how you describe a social media platform.

That is how you describe a data infrastructure asset.

The deeper implication:

McKinsey charges $500,000 for a consumer sentiment study that takes 6 weeks and interviews 2,000 people in a controlled environment.

Reddit has 493 million weekly users expressing unfiltered, uncompensated, real time opinions about every product, brand, drug, service, and experience on earth.

The Emplifi deal is the first enterprise partnership to formally route that signal into corporate decision-making workflows.

It will not be the last.

Every major consulting firm. Every CPG brand. Every pharmaceutical company. Every hedge fund running consumer sentiment models. They all need what Reddit has.

The data licensing revenue today: $39M per quarter.

Priced as raw text delivery.

What it’s becoming, structured enterprise intelligence infrastructure embedded directly into corporate workflows, has never been priced by a single analyst.

$663M Q1 revenue. 69% growth. 91.5% gross margins. $311M free cash flow. $2.77B cash.

$176. $33.9B market cap.

The advertising business gets all the attention.

The enterprise intelligence business, the one Emplifi just formalized, is the one nobody has modeled.

Reddit isn’t becoming a data company.

It already is one.

The market just hasn’t priced it yet.

1

8

747

May 31

$HIVE earnings drop tomorrow after close.

Wall Street expects roughly -$0.21 EPS and ~$80M revenue, imo the headline numbers probably won’t blow anyone away.

BUT….

the AI/HPC (BUZZ) guidance on Tuesday’s call (8AM EST) is literally everything right now.

• HPC ARR run rate already sitting at ~$35M today (up big from ~$20M earlier this year).

• They locked in a $30M 2 year AI cloud contract for 504 Nvidia B200 GPUs.

• ~5,500 GPUs already online doing real AI work.

• Official 2026 targets still in play: $140M annualized GPU AI Cloud ARR by Q4 26 (11,000 GPUs) → scaling to $225M total HPC ARR by end 2026/early 2027.

• That includes converting their New Brunswick 70 MW site into high margin Tier III hyperscaler colocation.

And… don’t sleep on the May 18 news: the 320 MW Sovereign AI Gigafactory in the Greater Toronto Area.

• 100,000 GPUs at full build out.

• ~CAD $3.5 billion investment.

• Online target: H2 2027.

• This pushes their global power pipeline to 850 MW (450 MW operating 400 MW in development), enough for ~130,000 GPUs total.

Now my Prediction:

CEO Aydin Kilic and the team will probably lead with “record growth in Bitcoin mining AND AI compute” (they already teased it on LinkedIn).

They’ll reaffirm the $140M / $225M HPC targets, maybe even nudge them higher with fresh contract wins or faster GPU deployments. Expect a strong voice on the Toronto gigafactory…

land secured, clean power locked, sovereign AI demand pouring in, plus updates on those 5,500 GPUs already live and the high ~80% margins on the AI side.

I don’t expect major surprises on the numbers, but the forward guidance any new AI wins will be the “beat” that matters.

2

5

28

8,793

May 31

Here’s the $RDDT thesis that will sound insane until it doesn’t.

Reddit is accidentally building the world’s largest psychological database.

Not user data. Not demographics. Not purchase history.

The actual interior of the human mind at its most vulnerable.

Think about when people post on Reddit…

Not when they’re happy. Not when they’re performing. Not when they’re curated.

When they’re terrified.

“I think my husband is cheating. What do I do.”

“I just got diagnosed. Has anyone survived this.”

“I’m about to lose my house. Where do I start.”

“I’ve never told anyone this but.”

Reddit is where humans go when the performance stops.

Every other platform captures who people pretend to be.

Reddit captures who people actually are, at the exact moment they need something real.

No social scientist in history has had access to this data at this scale.

No government. No university. No research institution.

Reddit has 20 years of unfiltered human psychological states, fears, confessions, decisions, regrets, breakthroughs, from hundreds of millions of people organized by the exact context in which those states occurred.

Now here’s where it becomes a financial thesis:

The entire $500 billion insurance industry prices risk based on what people tell actuaries.

The entire $200 billion pharmaceutical industry tests drugs on populations that volunteered.

The entire $150 billion mental health industry treats patients one hour per week.

Every single one of these industries is operating on a fraction of the psychological signal that Reddit has accumulated passively for two decades.

What happens when Reddit’s enterprise API starts delivering structured psychological signal to insurers modeling risk, pharma companies modeling drug adoption behavior, and healthcare systems modeling patient anxiety patterns before they become crises?

It’s the next logical step from the Emplifi partnership that already exists. (I’ll probably do a write up on that partnership as well.)

The data licensing business today is $39M~ quarterly.

Priced as raw text delivery to AI companies.

The AI training data business is real and growing.

But the psychological signal business, the one where Reddit becomes the Bloomberg Terminal for human behavioral intelligence, hasn’t been built yet.

The raw material has been accumulating for 20 years.

At zero cost.

Nobody has priced the Bloomberg Terminal thesis.

That’s the one.

1

4

664