23 | Finance student | Long-term growth investor | STOCKER20 - 20% off first sub👇| NFA 🕷️

Joined July 2024

- Tweets 2,322

- Following 257

- Followers 2,403

- Likes 3,441

174 Photos and videos

Pinned Tweet

Feb 24

My current long-term holding allocation with their current share price as of today:

$TSLA 24% (397$)

$SOFI 15% (18$)

$AMD 15% (216$)

$HIMS 10% (15$)

$OSCR 9% (12$)

$ZETA 7% (15$)

$PLTR 6% (130$)

$NBIS 5% (100$)

$LMND 5% (50$)

$PATH 4% (10$)

I’m not selling a single share of any of these before 2031 unless my long-term thesis changes.

I’m aiming for 4–10x by 2031 across this basket, with a couple names having real 10x upside.

7

1

51

13,922

$HIMS up 10% today.

I think the next few months are extremely important.

1) Peptides expected in July

2) Q2 shows the real impact after the Q1 GLP-1 reset

3) Growth needs to re-accelerate

4) Margins need to stabilize

Jun 8

My previous high-conviction bets have already moved:

$OSCR: $14 to $26.25

$ZETA: $16 to $21.91

$NBIS: $85 to $232.60

The next two stocks I believe can make major moves are $HIMS and $SOFI.

$HIMS at roughly $27 has two massive catalysts coming:

Peptide therapy: $HIMS is preparing to expand beyond its traditional categories into longevity and personalized treatments. Peptides could open another large recurring-revenue category, and the company is already adding medical leadership with direct experience in this space.

Q2 earnings: This will be the first major look at how the business is performing after the GLP-1 reset. The market is treating $HIMS like the entire company depended on one weight-loss product, while its core categories, international expansion and personalized-care platform continue growing.

Then there is $SOFI at roughly $16.44.

The stock price is lagging while the fundamentals are exploding:

Q1 revenue grew 43% YoY to $1.1B.

Adjusted EBITDA grew 62% to $340M.

Members grew 35% to 14.7M.

Products grew 39% to 22.2M.

$SOFI delivered its 10th consecutive profitable quarter.

Ignore the short-term noise. When fundamentals keep compounding while the stock goes sideways, the gap eventually closes.

My next two high-conviction runners are $HIMS and $SOFI.

1

50

3,264

I bought the $ASTS dip Friday.

Looking to add more tomorrow.

- Space sector got sold off after the SpaceX IPO hype faded

- $ASTS got dragged down with the group

- Thesis is still intact

- BlueBird 8, 9, and 10 launch is scheduled for June 17

- A clean launch could flip sentiment fast

This pullback into a major catalyst looks very interesting.

Jun 12

$ASTS is starting to look interesting for a swing.

This selloff feels more like a reset than a thesis break.

The stock ran hard into the SpaceX hype, and now space stocks are getting hit after the IPO became a “sell the news” event.

But the real question for $ASTS is not what happens in one red day.

The real question is:

Can they successfully launch, deploy, and commercialize direct-to-device satellite broadband?

That is the bull case.

If BlueBird 8, 9, and 10 launch successfully on June 17, I think sentiment can flip quickly.

This is the type of stock where fear and hype move fast in both directions.

A clean pullback into a major catalyst is exactly where swing setups can appear.

High risk.

But very interesting.

2

1

66

9,186

Jun 12

$ASTS is starting to look interesting for a swing.

This selloff feels more like a reset than a thesis break.

The stock ran hard into the SpaceX hype, and now space stocks are getting hit after the IPO became a “sell the news” event.

But the real question for $ASTS is not what happens in one red day.

The real question is:

Can they successfully launch, deploy, and commercialize direct-to-device satellite broadband?

That is the bull case.

If BlueBird 8, 9, and 10 launch successfully on June 17, I think sentiment can flip quickly.

This is the type of stock where fear and hype move fast in both directions.

A clean pullback into a major catalyst is exactly where swing setups can appear.

High risk.

But very interesting.

1

16

10,729

Jun 12

$IREN continues to look strong.

This is why I added it as one of my current swing positions.

The AI trade is not only chips.

It is power.

It is data centers.

It is infrastructure.

It is who can actually support the compute demand coming over the next few years.

That is where $IREN gets interesting.

The market is slowly realizing that AI infrastructure is not just $NVDA, $AMD, and $NBIS.

There is another layer underneath it:

Energy and compute capacity.

That is why my current swing basket remains:

$CRWV

$IREN

$NU

High risk names, but the theme is clear.

AI infrastructure is still the trade I want exposure to.

$IREN was trading around $60.34 today, up about 6.4% intraday when checked.

3

27

2,289

Jun 12

$NBIS is now being added to the Nasdaq-100 too.

For $NBIS, the math is what matters.

Management is targeting 7B-$9B in annualized run-rate revenue by the end of 2026.

If $NBIS hits that and the market values it at 10x ARR, that implies a 70B-$90B valuation.

At ~254M shares outstanding, that is roughly:

$276/share on $70B

$354/share on $90B

If the market gives it a premium AI infrastructure multiple, say 12x ARR, the range becomes roughly:

$331/share to $425/share.

That is why I still think $NBIS can trade higher if they execute.

The risk is also obvious:

Massive CapEx.

Funding needs.

Execution risk.

Valuation already pricing in a lot.

But if $NBIS keeps scaling revenue, signing major customers, and proving demand is real, I think the market can continue rewarding it.

Nasdaq-100 inclusion is just another layer of validation.

$NBIS has guided toward 7B-$9B ARR by end-2026, and had about 253.9M shares outstanding as of March 31, 2026.

Jun 12

$CRWV getting added to the Nasdaq-100 is not a small signal.

Index inclusion does not change the business overnight, but it does change visibility, liquidity, and institutional attention.

I bought $CRWV as a swing trade because the setup is simple:

AI compute demand is still insane.

Backlog is massive.

Revenue visibility is improving.

And now passive/index flows enter the picture.

Yes, the bear case is obvious:

Debt.

CapEx.

Customer concentration.

Execution risk.

But that is why this is a swing trade for me, not something I am blindly calling risk-free.

As mentioned last week, my current swing positions are:

$CRWV

$IREN

$NU

$CRWV being added to the Nasdaq-100 just made the setup a lot more interesting.

$CRWV reported $99.4B of revenue backlog as of Q1 2026.

3

82

10,643

Jun 12

$CRWV getting added to the Nasdaq-100 is not a small signal.

Index inclusion does not change the business overnight, but it does change visibility, liquidity, and institutional attention.

I bought $CRWV as a swing trade because the setup is simple:

AI compute demand is still insane.

Backlog is massive.

Revenue visibility is improving.

And now passive/index flows enter the picture.

Yes, the bear case is obvious:

Debt.

CapEx.

Customer concentration.

Execution risk.

But that is why this is a swing trade for me, not something I am blindly calling risk-free.

As mentioned last week, my current swing positions are:

$CRWV

$IREN

$NU

$CRWV being added to the Nasdaq-100 just made the setup a lot more interesting.

$CRWV reported $99.4B of revenue backlog as of Q1 2026.

1

1

7

11,790

Jun 11

More notes on my $OSCR thesis:

This is why I keep repeating the same thing with $OSCR:

Keep MLR controlled.

Hit guidance.

At today’s price around $28-$29, $OSCR is roughly a $9B company.

If they can do anywhere near the upper end of their long-term earnings potential, I don’t think a 13B-$15B market cap is crazy.

That would imply roughly 40-60% upside from here.

Depending on share count, that puts $OSCR in the $40 range.

That means the market would only be valuing $OSCR at about 0.7x 2026 revenue if they hit the low end of their 18.7B-$19.0B revenue guidance. For a company growing revenue, improving MLR, and becoming profitable, that’s not an insane multiple.

$OSCR already doubled for me.

I still don’t think the story is done.

1

59

3,855

Jun 11

$HIMS is exactly the type of stock where sentiment can change very fast.

Right now everyone is focused on the margin reset.

Q1 revenue was $608M, up only 4% YoY, adjusted EBITDA fell to $44M, and they swung to a net loss because of the weight-loss transition and upfront investments.

That’s the bear case.

But the long-term bull case is still very clear.

Management is still guiding for $2.8B to $3.0B in 2026 revenue and $275M to $350M adjusted EBITDA.

The market is basically asking one question:

Was this a temporary reset, or did the growth story break?

For me, Q2 and Q3 matter a lot.

If $HIMS shows weight-loss demand is still strong, margins stabilize, subscribers keep growing, and international expansion starts adding another layer, I think the market starts looking at this completely differently.

The upside case is not just GLP-1s.

It’s personalized healthcare, peptides, sexual health, hair loss, dermatology, mental health, international markets, and eventually a much larger consumer healthcare platform.

That’s why I still think $HIMS can be a 10x long-term investment.

The next few quarters decide how fast the market starts believing again.

1

6

64

3,868

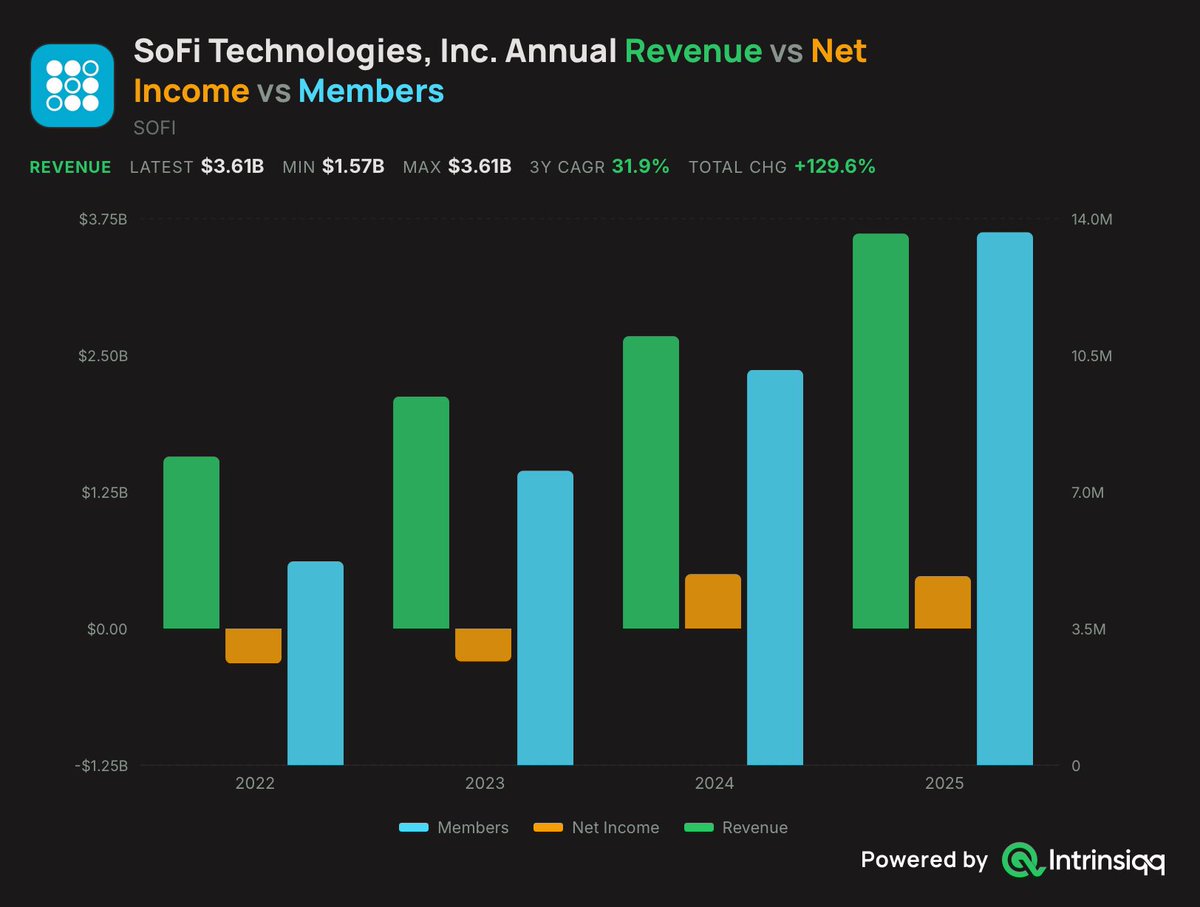

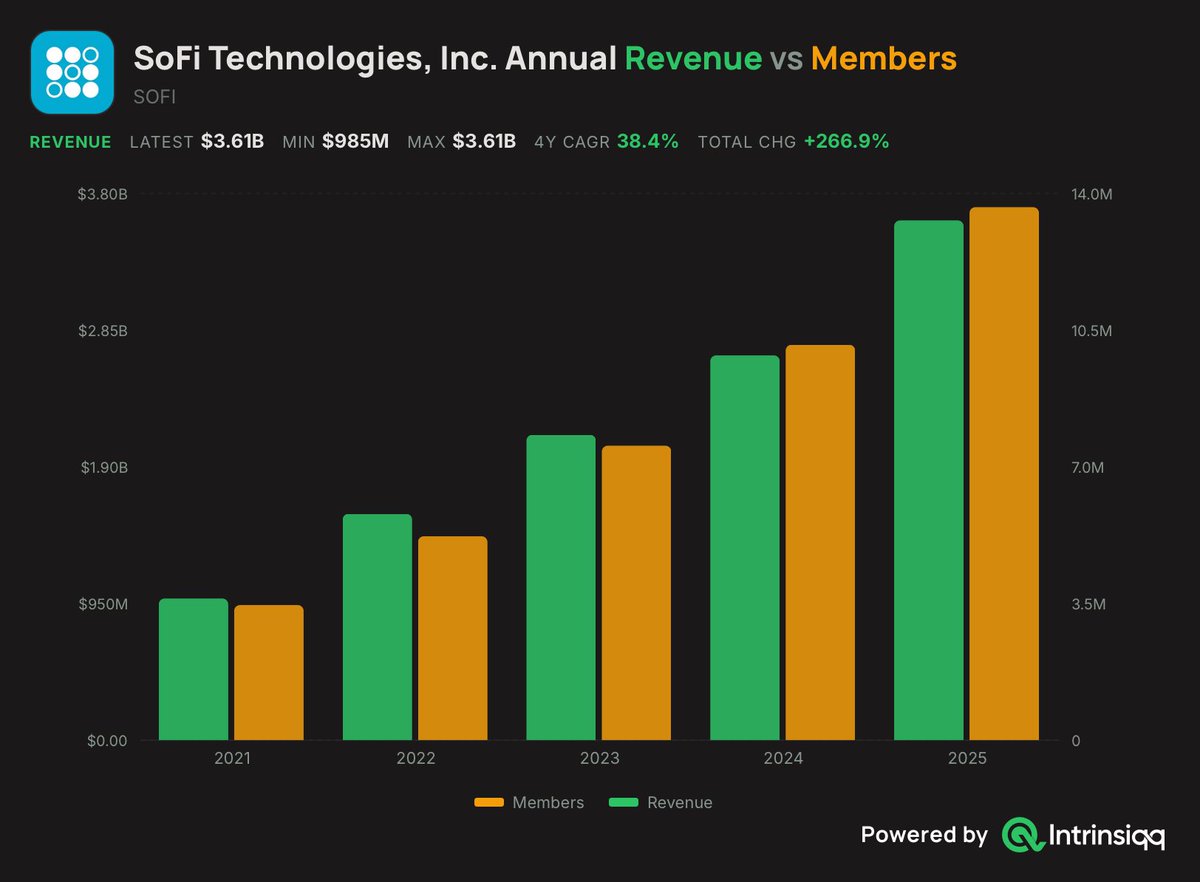

Jun 11

I don’t like throwing out random price targets.

But $SOFI to $40 is not some insane number if you actually do the math.

$SOFI is now around 14.7M members, just did $1.1B in quarterly net revenue, and management still expects around $4.66B in 2026 revenue with $0.60 EPS.

At today’s price around $16, the market cap is roughly 22B.

If $SOFI gets to $4.66B revenue this year, then a 5x sales multiple puts the company around 23B.

That’s basically where it trades now.

But this is the problem: the market is still pricing $SOFI like a normal lender, not like a financial services platform growing members, products, fee revenue, and tech infrastructure at scale.

If $SOFI can keep growing revenue 25-30% , expand margins, and push EPS higher into 2027, a 50B market cap is very realistic.

That would put the stock around $35-$40 , depending on dilution.

This is why I keep saying:

The first major rerate for $SOFI is not $100.

It’s the market finally accepting that $40 is mathematically possible.

8

1

118

10,519

Jun 10

There are 2 types of people in $SOFI right now.

1) The people letting poor macros, high rates, share dilution, and low sentiment scare them out.

2) The people using that same short-term noise as an opportunity to buy while the business keeps executing.

Yes, dilution matters.

Yes, rates matter.

Yes, macros matter.

But if the business keeps compounding revenue around 30%, keeps adding millions of members growing 35% YoY, keeps expanding products, and keeps improving profitability, the long-term thesis is still intact.

That is why I have said $40 is not some crazy target. It comes down to execution.

So the question is simple:

Are you selling because of short-term macro noise?

Or are you taking advantage while the numbers keep improving?

3

38

2,826

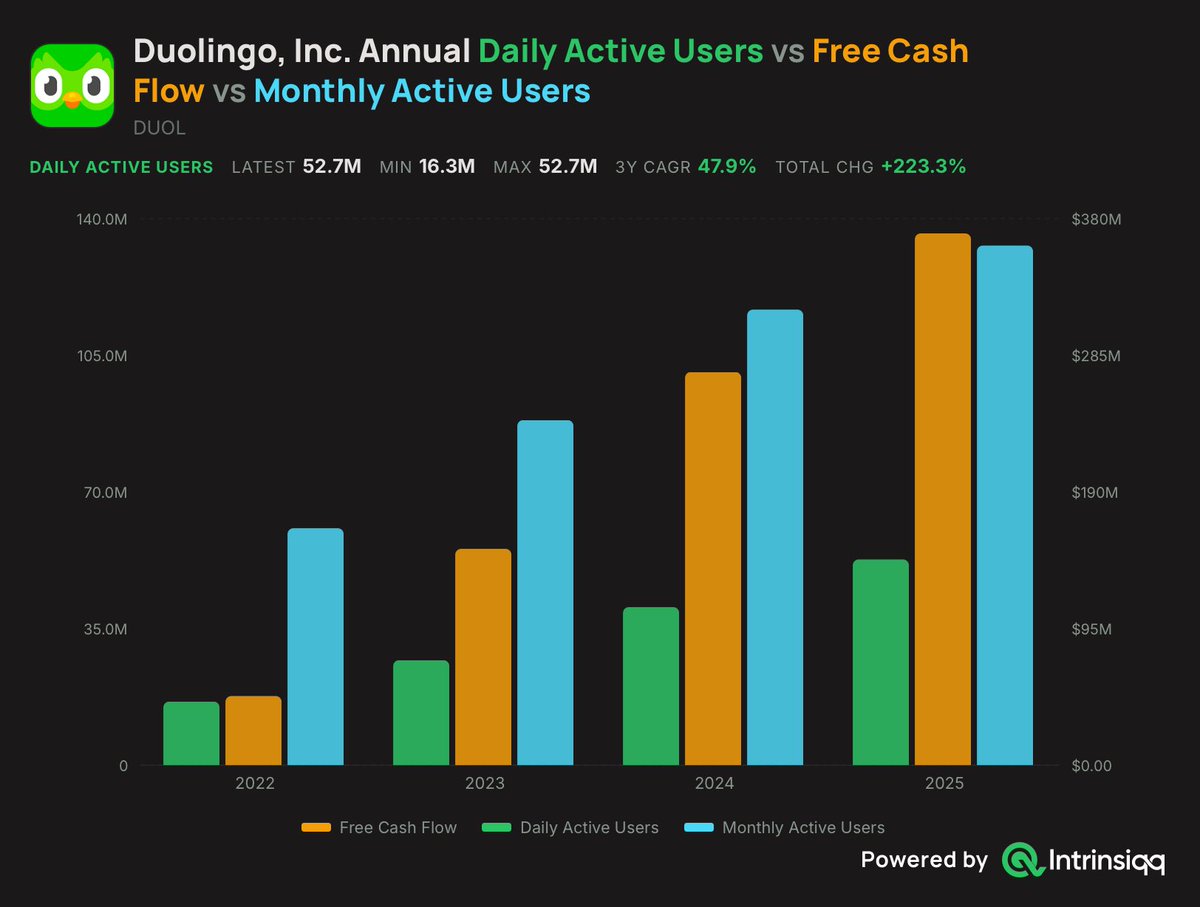

Jun 10

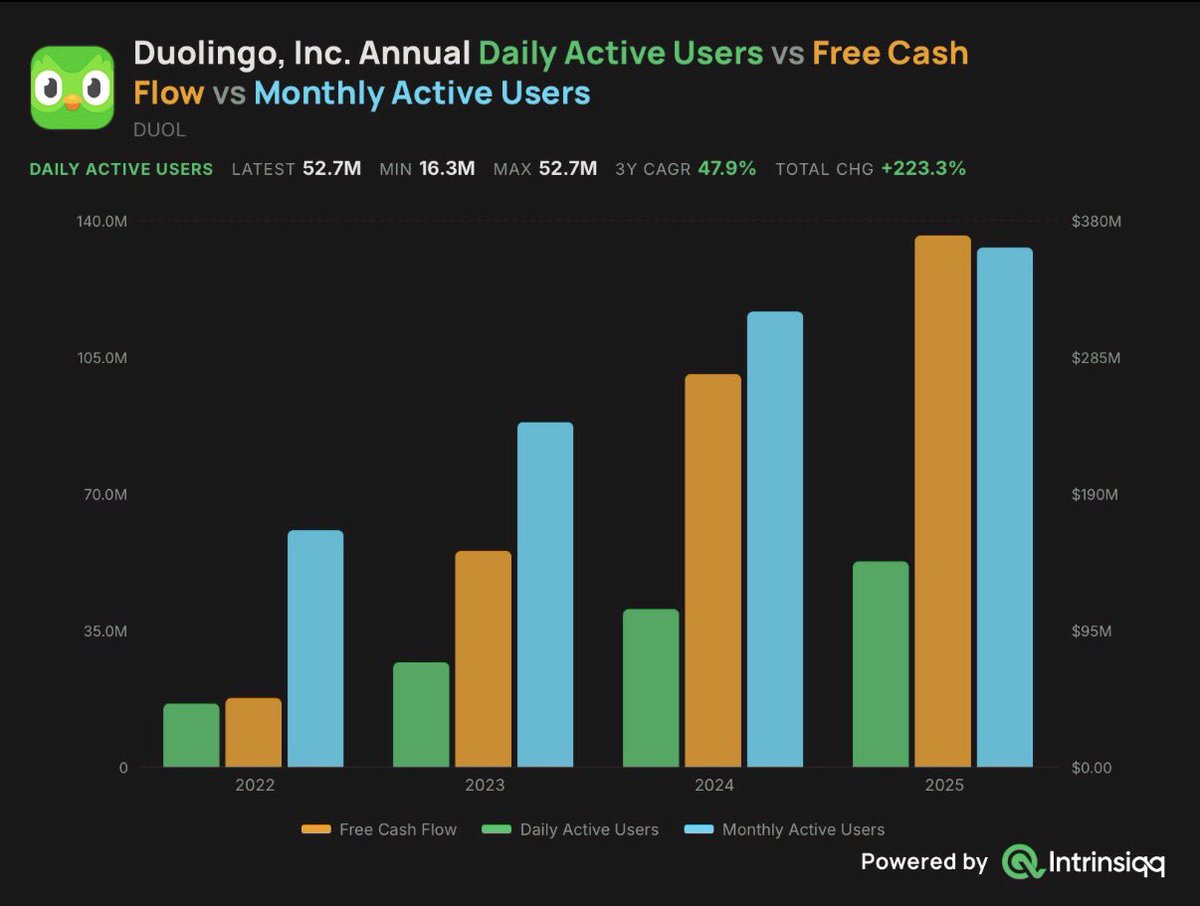

$DUOL is now up 41% from its 6-month lows.

Remember management’s long-term plan:

- Expand beyond language learning

- Scale Math, Music and Chess

- Grow paid subscribers globally

- Increase adoption of Duolingo Max

- Use AI to create more content at a lower cost

- Turn Duolingo into a complete education platform

The market was focused on short-term spending and margin pressure.

Management was focused on building a much larger business.

Long-term vision matters.

Jun 9

Anybody looking at $DUOL?

The stock sold off after each of its last two earnings reports because management intentionally chose long-term user growth over short-term bookings and margins.

Now $DUOL is up roughly 30% over the last two months. Is the market finally understanding the strategy?

The plan is simple:

Grow daily active users from 56.5M toward 100M by 2028, make AI-powered speaking features available to more users, improve retention and slowly convert that larger audience into paid subscribers over time.

$DUOL is also expanding beyond languages into chess, math and music… building an education platform rather than remaining a single-product language app.

Q1 revenue still grew 27%, paid subscribers grew 21% and the company expects more than $350M in free cash flow this year.

Management is sacrificing some near-term monetization to build a much larger ecosystem for 2027 and beyond.

The market hated that decision two quarters in a row. It may finally be starting to understand it.

15

1,339

Jun 10

I now have 3 stocks in my long-term portfolio that are up more than 100% YTD:

$NBIS

$AMD

$OSCR

What’s next?

Jun 10

I am officially up 100% on $OSCR.

Based on $OSCR 2026 guidance, $40 is attainable.

Here is the math:

$OSCR is guiding for approximately:

- $18.7B–$19.0B in revenue

- $250M–$450M in operating earnings

- 82.4%–83.4% MLR

- 15.8%–16.3% SG&A ratio

At roughly 299M basic shares outstanding, a $40 share price would equal an $12B market cap.

That would value $OSCR at only:

$12B ÷ $18.85B revenue = 0.64x sales

Even using roughly 330M diluted shares, $40 represents a $13.2B valuation, or approximately 0.70x revenue.

For a company that just reported:

- Revenue up 53% YoY to $4.65B

- Membership up 56% YoY to 3.17M

- Q1 operating earnings of $704M

- Q1 net income of $679M

- SG&A leverage continuing to improve

… I do not think a valuation below 1x sales is aggressive.

The earnings math also works.

At the high end of guidance, a $12B valuation would be roughly 27x 2026 operating earnings. However, $OSCR is still early in its margin-expansion story. If operating earnings eventually reach $750M–$1B as revenue scales and administrative leverage improves, $40 would represent only 12x–16x operating earnings.

The formula remains simple:

Keep MLR controlled.

Deliver the 2026 guidance.

Continue leveraging SG&A.

Prove profitability is sustainable.

I am up 100%, but I do not believe the long-term rerating is finished.

$40 remains attainable.

13

1,726

Jun 10

I am officially up 100% on $OSCR.

Based on $OSCR 2026 guidance, $40 is attainable.

Here is the math:

$OSCR is guiding for approximately:

- $18.7B–$19.0B in revenue

- $250M–$450M in operating earnings

- 82.4%–83.4% MLR

- 15.8%–16.3% SG&A ratio

At roughly 299M basic shares outstanding, a $40 share price would equal an $12B market cap.

That would value $OSCR at only:

$12B ÷ $18.85B revenue = 0.64x sales

Even using roughly 330M diluted shares, $40 represents a $13.2B valuation, or approximately 0.70x revenue.

For a company that just reported:

- Revenue up 53% YoY to $4.65B

- Membership up 56% YoY to 3.17M

- Q1 operating earnings of $704M

- Q1 net income of $679M

- SG&A leverage continuing to improve

… I do not think a valuation below 1x sales is aggressive.

The earnings math also works.

At the high end of guidance, a $12B valuation would be roughly 27x 2026 operating earnings. However, $OSCR is still early in its margin-expansion story. If operating earnings eventually reach $750M–$1B as revenue scales and administrative leverage improves, $40 would represent only 12x–16x operating earnings.

The formula remains simple:

Keep MLR controlled.

Deliver the 2026 guidance.

Continue leveraging SG&A.

Prove profitability is sustainable.

I am up 100%, but I do not believe the long-term rerating is finished.

$40 remains attainable.

9

1

71

5,456

Jun 10

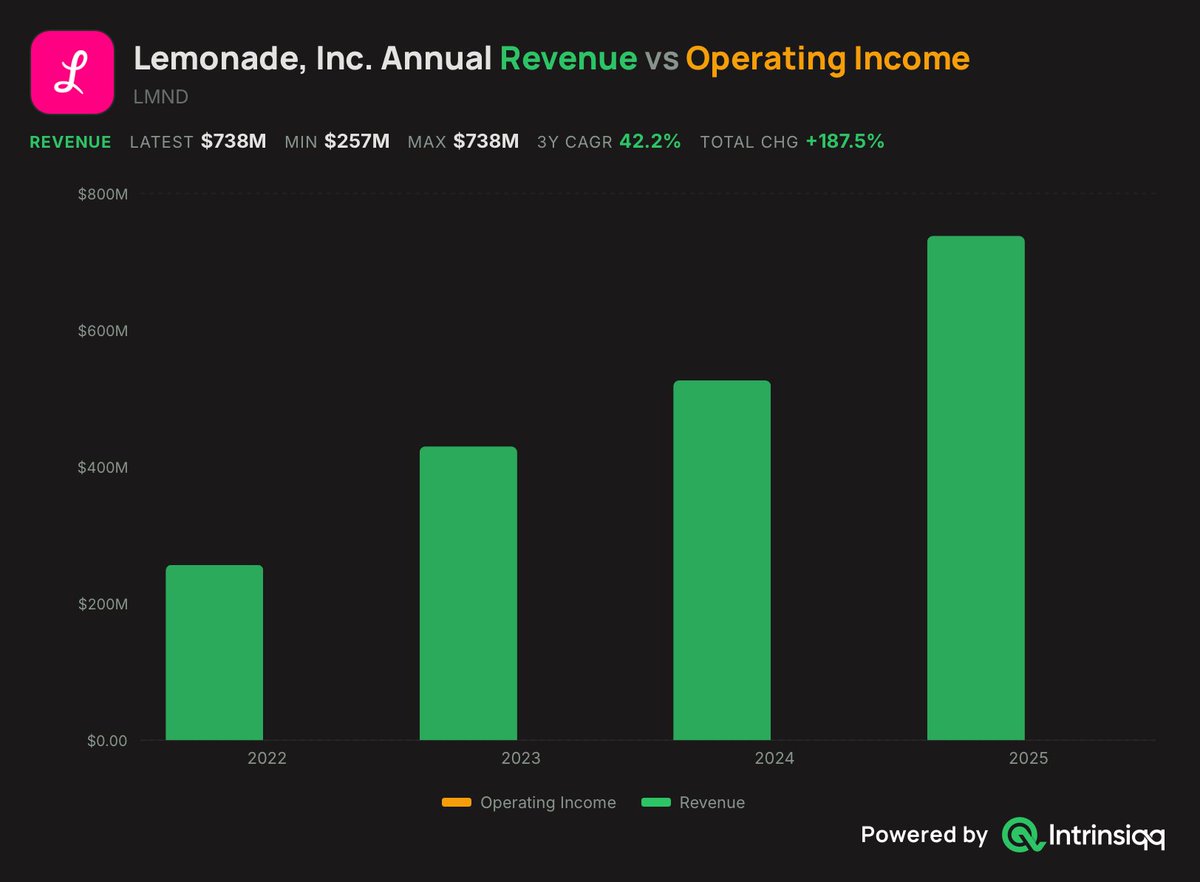

I strongly believe $LMND has the potential to become a long-term 10x.

Here is the actual 10x math:

$LMND currently has a market cap of roughly 4.4B.

A 10x would value the company at approximately:

$4.4B × 10 = $44B

With approximately 76M diluted shares, that would translate to roughly:

$44B ÷ 76M shares = $579 per share

Dilution could lower the eventual per-share result, but that is the general target required for a 10x from today’s valuation.

So how could $LMND ever justify a $40B–$45B valuation?

Start with the operating momentum.

In Q1 2026:

- Revenue reached $258M, up 71% YoY

- Gross profit reached $100M, up 159%

- In-force premium reached $1.33B, up 32%

- Customers reached 3.14M, up 23%

- Gross loss ratio improved from 78% to 62%

- Adjusted EBITDA loss narrowed from $47M to $17M

- Net loss improved from $62M to $36M

Revenue is growing much faster than operating expenses, which increased only 25%. That is the operating leverage investors have been waiting to see.

$LMND now expects approximately $1.2B in 2026 revenue and $1.63B–$1.64B in year-end in-force premium, while targeting positive adjusted EBITDA during Q4 2026.

But the long-term opportunity is much larger.

Management has laid out an ambition to eventually reach approximately $10B in premium volume.

Growing from $1.33B of IFP to $10B would mean increasing the insurance book by roughly:

$10B ÷ $1.33B = 7.5x

At 25% annual growth, that would take approximately nine years.

At 30% annual growth, it would take approximately seven years.

That is aggressive, but $LMND IFP is currently growing above 30%, and the company is still small relative to the overall homeowners, renters, pet and auto insurance markets.

Now assume $LMND eventually produces $7B–$8B in annual revenue from that larger premium base.

At a mature adjusted EBITDA margin of 12%–15%, it could generate:

$7B × 12% = $840M EBITDA

$8B × 15% = $1.2B EBITDA

Apply a premium 35x–40x multiple to a profitable insurance platform still growing faster than traditional insurers:

$840M × 35 = $29.4B

$1.2B × 40 = $48B

That produces a potential valuation range of approximately $30B–$48B.

The upper end is around the level required for a 10x.

This is where AI matters.

$LMND is not simply adding a chatbot to a traditional insurer. Its technology is integrated throughout the operating model:

- AI helps determine which customers to target

- Pricing models improve as more claims and behaviour data enter the system

- Automated claims reduce the cost of servicing smaller, frequent claims

- Direct distribution removes much of the traditional broker infrastructure

- Automation allows premium volume to grow without headcount increasing at the same rate

$LMND recently reached approximately $1M of IFP per employee, nearly tripling that figure over four years. Management has also maintained roughly a 3:1 lifetime-value-to-customer-acquisition-cost ratio, even while aggressively increasing growth spending.

That is the structural advantage.

More customers create more data.

More data can improve pricing and risk selection.

Better underwriting lowers loss ratios.

Lower loss ratios expand gross profit.

Automation allows that gross profit to scale without expenses increasing proportionally.

The 10x thesis is therefore not “AI hype.”

It requires Lemonade to:

- Continue compounding IFP around 25%–30%

- Keep its loss ratio near the low-to-mid 60% range

- Reach and sustain EBITDA profitability

- Scale Car without destroying underwriting discipline

- Control customer-acquisition costs

- Limit dilution

- Eventually approach $7B–$8B in revenue and approximately $1B in EBITDA

The path is now visible.

5

5

75

7,542

Jun 9

Anybody looking at $DUOL?

The stock sold off after each of its last two earnings reports because management intentionally chose long-term user growth over short-term bookings and margins.

Now $DUOL is up roughly 30% over the last two months. Is the market finally understanding the strategy?

The plan is simple:

Grow daily active users from 56.5M toward 100M by 2028, make AI-powered speaking features available to more users, improve retention and slowly convert that larger audience into paid subscribers over time.

$DUOL is also expanding beyond languages into chess, math and music… building an education platform rather than remaining a single-product language app.

Q1 revenue still grew 27%, paid subscribers grew 21% and the company expects more than $350M in free cash flow this year.

Management is sacrificing some near-term monetization to build a much larger ecosystem for 2027 and beyond.

The market hated that decision two quarters in a row. It may finally be starting to understand it.

1

14

2,247

Jun 9

If you missed $NOW under $100, you’re getting another chance to buy it under $110.

Here’s why I like $NOW:

The company is still growing subscription revenue above 20%, while cRPO reached $12.64B and total RPO hit $27.7B, both growing above 20% YoY. That gives $NOW incredible visibility into future revenue.

The AI thesis is also getting stronger. Now Assist customers spending over $1M annually grew more than 130% YoY. This is not a software company being replaced by AI… it is becoming the platform enterprises use to actually deploy AI across their workflows.

$NOW expects to generate roughly $15.7B–$15.8B in subscription revenue this year and is targeting more than $30B by 2030.

I already made over 50% swing trading $NOW once. I’m watching this pullback closely.

1

4

684

Jun 9

$HIMS is up 4% in red market.

Relative strength like this always catches my attention.

While most growth stocks are getting sold, buyers are stepping into $HIMS ahead of peptides, international expansion and Q2 results that should give us a clearer picture of the GLP-1 reset.

The long-term thesis continues to strengthen.

1

3

50

3,541

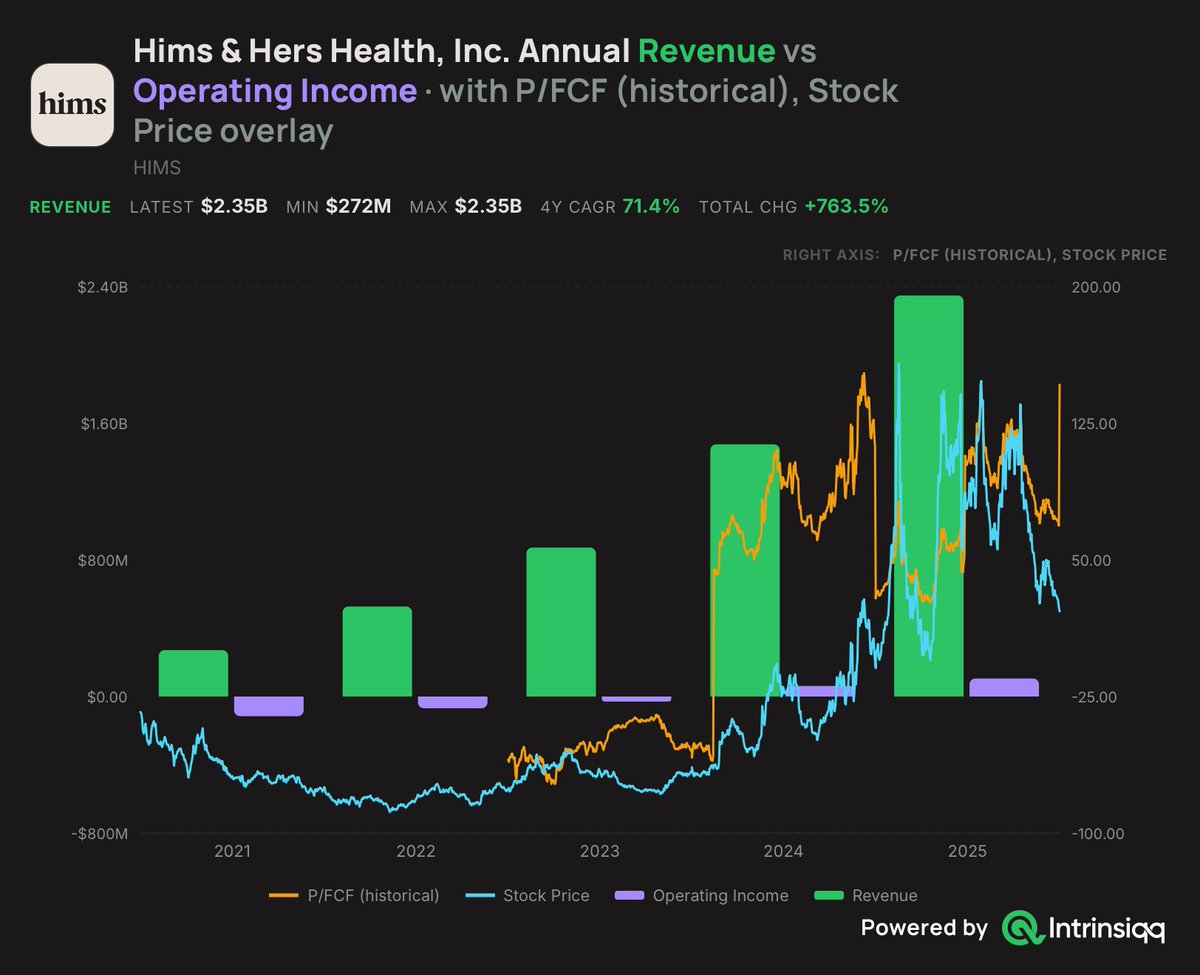

Jun 8

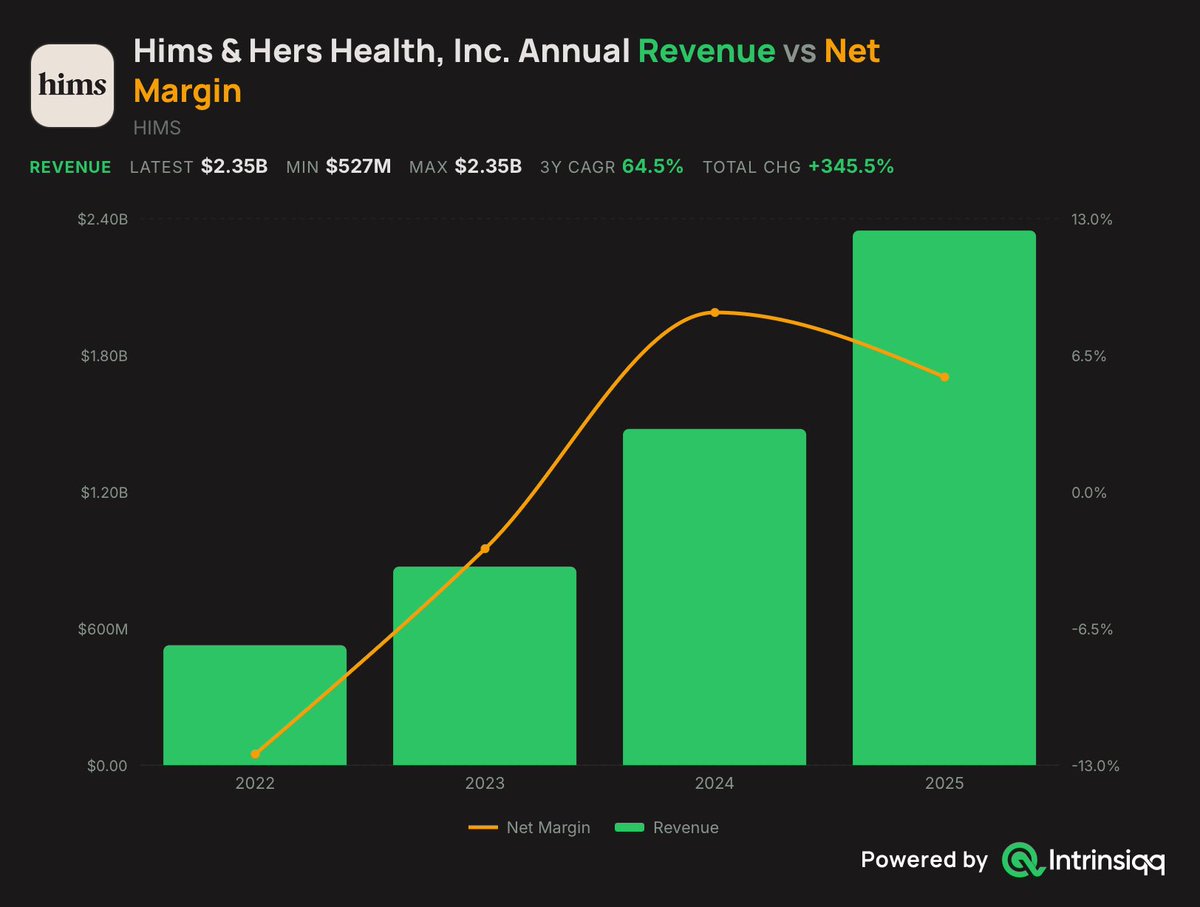

This chart is exactly why I remain so confident in the long-term $HIMS thesis. (Everything to know heading into Q2)

Revenue has grown from $527M in 2022 to $2.35B in 2025.

That is approximately 345% total growth in only three years, with a revenue CAGR of roughly 64.5%.

But the more important part of this chart is the transition underneath the revenue growth.

In 2022, $HIMS generated a net loss of approximately 66M.

In 2023, that loss narrowed to approximately 24M.

In 2024, the business reached full-year profitability with $126M in net income.

And in 2025, net income remained positive at approximately $128M while revenue increased another 59%.

At first glance, the decline in net margin from approximately 9% to 5% may look concerning.

But there is important context.

The 2024 result included a roughly $54M income-tax benefit, largely related to the release of a deferred-tax valuation allowance. That provided a significant boost to 2024 net income that did not repeat at the same level in 2025.

Meanwhile, $HIMS was investing heavily in customer acquisition, technology, fulfillment capacity, international expansion and new product categories.

Marketing increased 35%.

Technology and development spending increased 89%.

Operations and support spending increased 54%.

General and administrative expenses increased 63%.

Despite all of that investment, adjusted EBITDA increased from approximately $177M to $318M, with adjusted EBITDA margin improving from 12% to 14%.

That tells me the core platform continued becoming more profitable, even though the GAAP net-margin line declined.

Now, Q2 and Q3 of 2026 become extremely important.

Q1 showed the impact of the GLP-1 reset clearly:

Revenue grew only 4% YoY to 608M.

Gross margin declined from 73% to 65%.

The company recorded a $92M net loss.

Adjusted EBITDA fell from $91M to 44M.

I will be watching whether Q2 and Q3 show:

Revenue growth reaccelerating after the GLP-1 transition.

Gross margins beginning to stabilize.

Adjusted EBITDA recovering.

Subscriber growth continuing.

The new branded weight-loss model gaining traction.

International expansion and newer categories beginning to contribute.

I do not need margins to immediately return to their previous peak.

I need evidence that the Q1 pressure was transitional rather than structural.

If $HIMS can return to stronger growth while gradually rebuilding gross margin, adjusted EBITDA and free cash flow, the long-term thesis remains fully intact.

I believe $HIMS has the potential to become a 10x investment over the long term.

I am investing in the possibility that $HIMS becomes one of the largest personalized healthcare platforms in the world.

Q2 and Q3 should tell us a lot about whether the next stage of that thesis is beginning.

3

5

54

3,099

Jun 8

As I mentioned last week, I started buying $CRWV.

I want to go deeper because I think $CRWV may be one of the only major AI infrastructure names where the market is still pricing in a serious amount of failure.

The bear case is easy to understand:

1) Massive debt.

2) Massive capital expenditures.

3) Heavy interest expense.

4) Customer concentration.

5) Execution risk.

But stopping the analysis at the debt completely misses what $CRWV is building and the contracted demand supporting that investment.

$CRWV ended Q1 with $98.8B in remaining performance obligations, up from just $14.7B one year ago.

Add another $0.6B of estimated future revenue from committed contracts, and total revenue backlog reaches $99.4B, up 284% YoY.

Backlog can include amounts subject to future delivery and capacity requirements. RPO is the stronger accounting measure because it represents contracted obligations that have not yet been recognized as revenue.

$CRWV generated only $2.08B of revenue in Q1, yet it now has nearly $99B of contracted future revenue sitting ahead of it.

The market is valuing the company based on today’s debt load while the business is being built around tomorrow’s revenue base.

And the backlog is not entirely pushed into some distant future:

Around 36% is expected to be recognized within 24 months, another 39% between months 25 and 48, and 25% beyond 48 months.

That gives $CRWV something most hypergrowth infrastructure companies do not have: long-term revenue visibility before the capacity is fully online.

The demand is also becoming more diversified.

$CRWV signed more than $40B of new customer commitments during Q1, including a new $21B Meta commitment, a multi-year Anthropic agreement and expanded relationships with Cohere, Jane Street and Mistral.

This is why I do not view the debt as automatically bearish.

$CRWV is not borrowing heavily because demand is disappearing. It is raising capital because customers are asking for more compute than its current infrastructure can provide.

The company has now surpassed 1 GW of active power, secured more than 3.5 GW of contracted power, and believes it can exceed 8 GW by 2030. It also secured an $8.5B investment-grade-rated delayed-draw facility and received a $2B equity investment from $NVDA.

The risk:

$CRWV spent $6.8B on capital expenditures in Q1 alone. Interest expense reached $536M, equal to roughly 26% of quarterly revenue, and the company recorded a $740M net loss.

The thesis is that revenue growth can eventually outpace the growth in financing costs.

$CRWV still produced $1.16B in adjusted EBITDA during Q1, representing a 56% margin, despite being in one of the most aggressive infrastructure expansion cycles in the market.

As the contracted capacity becomes active, $CRWV can recognize more of that RPO as revenue without needing corporate expenses to grow at the same rate.

That is where the operating leverage can eventually appear.

The real questions are:

Can it deploy capacity on schedule?

Can it convert the $98.8B RPO into revenue?

Can revenue growth eventually reduce interest expense as a percentage of sales?

Can it diversify customers while protecting margins?

High risk, but I think the potential reward is being underestimated.

Jun 7

I’ve been really focused on adding cash into my swing trading account.

My current swing trades are:

$IREN

$CRWV

$NU

Here is why I like all three:

$IREN:

- Targeting up to $4.4B in annualized run-rate revenue

- More than 4.5 GW of secured power

- 810 MW operational

- 2.1 GW under construction

- Recently secured $3.65B in GPU financing

- Added a planned 800 MW Australian campus

The opportunity is massive, but so is the execution risk. After the recent pullback, I like the risk-to-reward for a swing.

$CRWV:

- Q1 revenue: $2.08B, up 112% YoY

- Revenue backlog: $99.4B, up 284% YoY

- Adjusted EBITDA: $1.16B

- Adjusted EBITDA margin: 56%

- More than 1 GW of active power

- Targeting more than 8 GW by 2030

The debt and spending remain the biggest risks, but nearly $100B of backlog gives the company incredible revenue visibility. I think $CRWV could see another major rerating if it continues converting that demand into revenue.

$NU:

- More than 135M customers

- Added roughly 4M customers during Q1

- Q1 revenue: $5.3B

- Q1 net income: $871M

- ROE: 29%

- Net interest income: $3.25B

- Activity rate: 83%

- Efficiency ratio improved to 17.6%

The fundamentals continue getting stronger while sentiment and macro concerns have pressured the stock. That disconnect is exactly why I have been adding.

So my swing account currently gives me exposure to two different setups:

AI infrastructure growth through $IREN and $CRWV.

Fundamental mispricing through $NU.

Three higher-risk positions, but each one has numbers supporting the thesis.

1

7

1,190

Jun 8

This company was never meant to stay a US telehealth app selling a few medications.

The real vision is to become a global, vertically integrated consumer healthcare platform.

Global expansion is already happening. Through Eucalyptus, $HIMS is gaining exposure to markets like Canada, the UK, Germany, Australia and Japan instead of building every operation from zero.

Then come peptides.

$HIMS acquired a US peptide facility, giving the company more control over manufacturing, supply, personalization and potentially margins. Peptides could eventually expand the platform into areas like metabolic health, hormonal health, recovery and longevity, depending on regulatory and clinical progress.

The thesis is becoming clearer:

Expand globally.

Enter more healthcare categories.

Own more of the supply chain.

Use AI and data to personalize treatment.

Build long-term relationships with customers across multiple parts of their health.

The market keeps judging $HIMS based on short-term GLP-1 noise.

I’m focused on what this platform could become over the next five to ten years.

This is exactly why $HIMS remains one of my next high-conviction growth bets.

Zava is getting ready to launch the wegovy pill in the UK

$HIMS

2

3

27

3,017