building the world’s fiat rails

Joined August 2023

- Tweets 1,091

- Following 298

- Followers 845

- Likes 1,169

56 Photos and videos

May 30

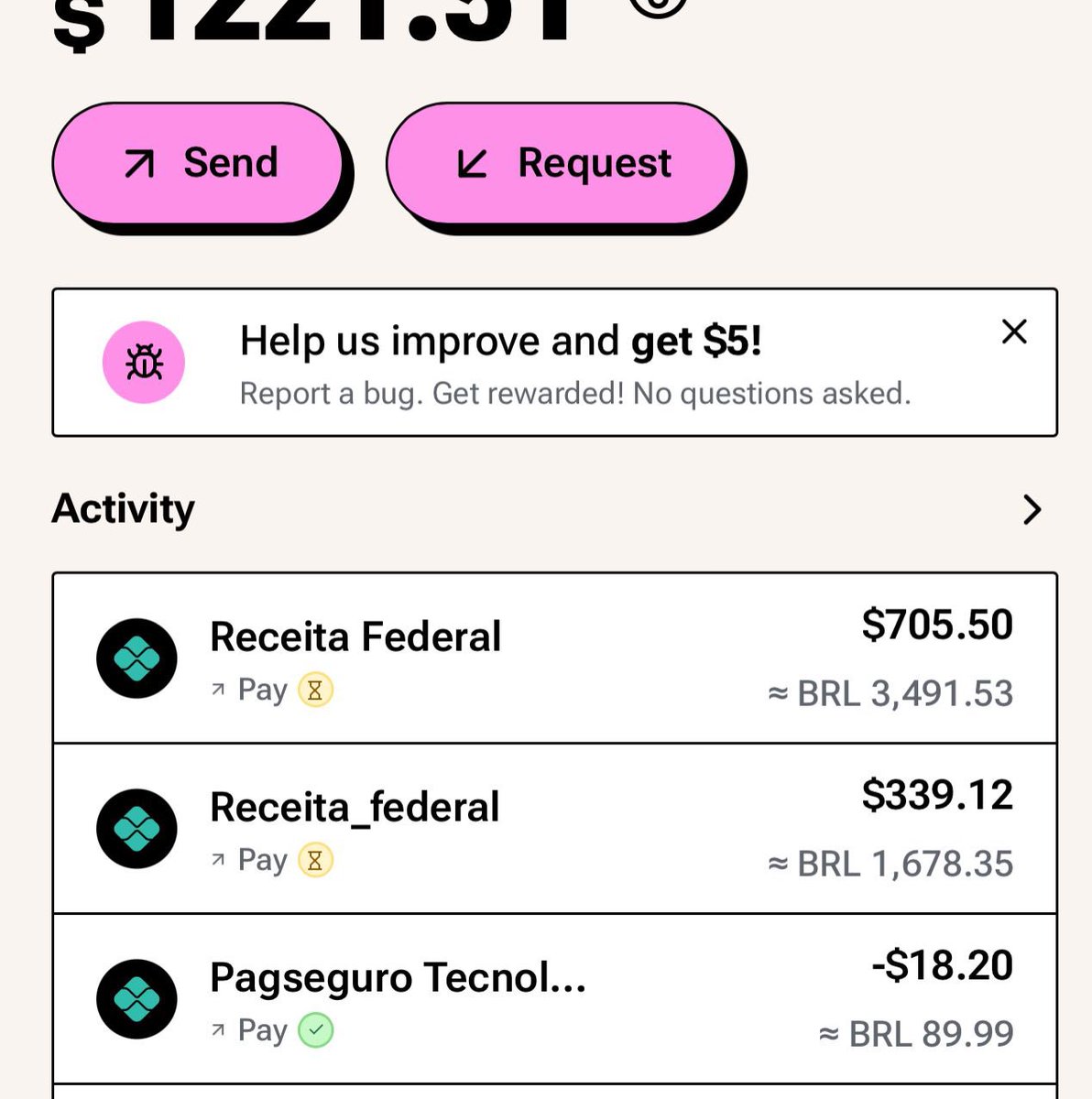

Brazil has 81 million delinquent adults, half the adult population, with roughly $100 billion in defaulted debt.

Banks legally deduct from their accounts automatically, before they decide what to pay.

Five of the country's ten most profitable companies are banks. Itaú alone made R$46.8 billion in profit in 2025, the highest in the history of Brazilian banking, equivalent to R$128 million per day.

Brazilians don't control their own income.

How crazy is that?

3

1

7

562

May 27

O problema do incompetente irrelevante é se tornar relevante pela própria incompetência.

1

9

346

May 18

We are living a debt epidemic, and it has become so common that most people no longer recognize it as one.

Four out of every five Brazilian families are in debt right now. Half of them have no way to pay it back. The same pattern, in different forms, is repeating across most of the world.

- In Brazil, 80.2 percent of families carry debt, the highest level in 16 years of tracking.

- 85 percent of that debt sits in credit cards, where revolving interest routinely crosses 400 percent a year.

- Among families earning up to three minimum wages, 38.9 percent are already behind on bills, and nearly one in five says they have no ability to pay them next month.

- Globally, total debt sits above 235 percent of world GDP.

This is the steady state.

The bear market and the migration of attention toward AI have pulled the conversation in crypto away from the things that originally made it matter. That is a natural cycle. But it is worth using this moment to remember why these tools were built. The use case that justifies their existence is not somewhere in the future. It is in the inbox of every family staring at a bill they cannot pay.

The most common explanation for the debt epidemic is that people lack financial education. This is wrong. The United States runs the largest financial education infrastructure on the planet. Personal finance is taught in public schools. Television networks, podcasts, and bestselling books are dedicated to teaching ordinary people how to manage money. And yet US household debt reached 21.2 trillion in Q1 2026, with credit card balances at a record 1.277 trillion, and 37 percent of Americans cannot cover a 400 dollar emergency without borrowing. If education were the missing variable, the country that produces the most of it would have the lowest debt. It has the opposite.

The problem is not informational. It is structural. People know they should not be in debt. People know they should save. The issue is that the system makes acting on that knowledge nearly impossible, because the money never sits long enough in the household's hands for any plan to take effect. Telling someone to budget when their salary is already partially deducted before it arrives is not education. It is theater.

The mechanism is simple. In the current setup, the creditor decides the order of payment. When a family owes money on a credit card, an overdraft, a personal loan, a buy now pay later plan, and an installment for an appliance, the bank decides what gets collected and when. The salary lands in an account held by the same institution that holds the debts, and the institution applies its own priorities to that money before the worker sees it. The family spends the rest of the month reacting to whatever pressure arrives next.

This is the structural fact that matters. The order of payment is decided by whoever holds the money, and in the current system that is almost never the household itself.

Every serious framework for getting out of debt rests on the same idea. You list what you owe, you decide the order, you attack one debt at a time until it is gone, then you move to the next. The math of which debt to pay first matters less than the act of choosing. The frameworks work because they put the household back in control of the sequence. But they only work if that control actually exists. In a system where the bank holds your salary, your debts, and the right to deduct payments before you see the money, you do not have the freedom to sequence anything. The bank already sequenced it for you. Without the ability to hold your own income, every debt elimination framework becomes motivational content. With it, the same framework becomes executable strategy.

We need better tools tho.

Self custody is the technical capability to hold your own money outside an institution that has competing claims on it. If your income lands in a wallet you control, in a stablecoin you choose, you decide which debt to pay this month, in what amount, and in what order. The bank stops being the operating system of your finances and becomes one counterparty among several.

This is not an ideological position. It is the structural position that wealthy households already occupy through lawyers, accountants, and separate accounts that let them direct their own cash flow. Self custody gives the same position, in a much simpler form, to people who never had access to those tools.

The second piece is how the money gets spent. Credit cards are the most expensive form of household borrowing on the planet, and they are the default way most people transact. Non custodial alternatives are the opposite. You can only spend what you actually have. There is no revolving balance compounding while you sleep. Paying becomes a deduction from your own assets, not the creation of a new liability.

The technology to deliver this already exists, they have the rails, the wallets, and the user interfaces to put self custody in the hands of ordinary people. What is still missing is the framing. Most of these products are positioned as crypto tools for crypto users. The real opportunity is to position them as what they actually are, which is a way out of the debt epidemic for households that have no other way out. That shift in purpose is not a technical problem. It is a question of who these products decide they are building for, and what proposition they put at the center of their work.

Together, these pieces give a household something the current system does not. A place to hold income that no creditor can touch first. A way to spend that cannot turn into debt. And the freedom to decide the order in which obligations get paid. That is the entire structural difference, and it is enough to change what is possible.

The population using these tools today is small relative to the population that would benefit. That is the natural state of any new technology. The work that comes next is making the same capability available to people who do not have the time or technical background to learn the underlying machinery. The onboarding has to be shorter than opening a bank account. The interface has to assume the user does not want to learn what a private key is. The product has to work for somebody three months behind on a bill, earning a minimum wage, who has never opened a wallet.

The debt epidemic is not going to be solved by the same institutions that produced it, and it is not going to be solved by teaching people lessons they have already heard a thousand times. The solution is a shift in who holds the income and who decides where it goes, delivered through tools simple enough that the shift can actually happen.

2

15

575

May 12

Quick update: I'm leaving @p2pdotme.

Thanks for the team who showed up every day

The circle admins who built local trust where none existed

The merchants who put their reputation on the line so strangers could move money back home and

The content creators who helped us tell the stories.

Building crypto payments only works when real people trust each other, glad to see how far we got building this.

Not leaving the crypto space tho.

Onwards :)

28

1

79

7,829

May 5

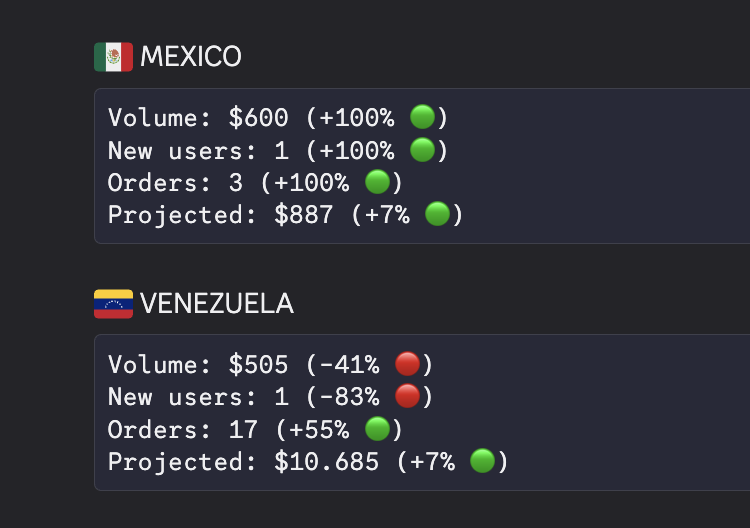

🙏 Gracias, Venezuela

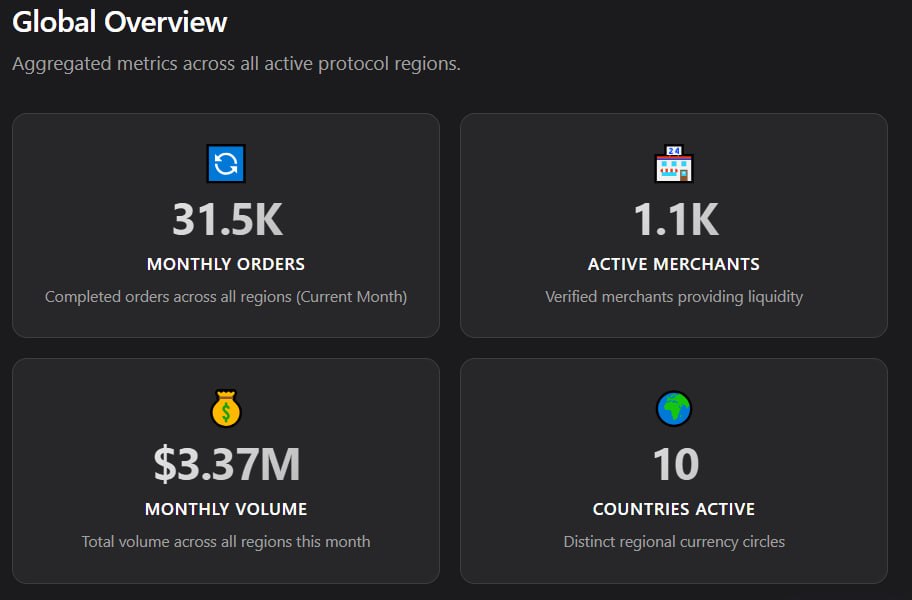

🇻🇪 Venezuela users have grown 30x since the start of 2026.

Reminder: You can move between Bs. and stablecoins directly on P2P.me without KYC.

5

5

37

2,127

Apr 30

A common critique of P2P fiat-crypto systems is that the fiat rail itself, like Pix in Brazil, is inherently traceable, so anything built on top inherits that traceability. The critique is partially correct and worth taking seriously. But it transfers by inertia to architectures that don't share its assumptions, and the conflation hurts honest discussion of what privacy is actually achievable. Brazil's Pix has the strongest publicly documented forensic surface of any major instant payment system, so it's a useful case study, and the lessons generalize.

The critique gets a lot right. Pix participants must retain XML message contents for 10 years. DICT query logs persist for 2 years with mandatory headers tying queries to payer CPF via PI-PayerId and PI-EndToEndId. AML records under Circular 3.978 require at least 10 years. For systems where the crypto user is the direct Pix payer, this is decisive: their CPF lives in payer PSP logs for a decade. For systems with centralized fiat-to-token issuance, correlation is even cleaner because the issuer holds the mapping between payer identity and on-chain destination. For systems requiring federated peg-out, additional choke points exist as forensic clocks. This is correct forensic analysis.

But the critique assumes specific architectural choices: crypto user as direct Pix payer, centralized issuer, federated bridging, KYC custodial wallets at endpoints. Change those assumptions and most join points disappear.

Consider an alternative architecture, abstracted from any specific product. On-chain matching with stake-based reputation and no custody. Pix validation via zkTLS, where the protocol receives proof the Pix occurred without seeing the data. Smart account wallets with no KYC anchor and no CEX endpoints. A pulverized network of human merchants with volatile application caches. Off-ramp flows where the client sells crypto and receives Pix into a legitimate third party's account, never directly handling Pix with their own CPF.

Apply the same forensic framework. EndToEndId and DICT logs still exist but bind the merchant's CPF to the third party's CPF. The crypto client appears in neither field. The 10-year payer PSP record is irrelevant to identifying the client. Centralized issuer doesn't exist, so there's no entity that holds the payer-to-address mapping. Federated peg-out doesn't exist, so no administrative timing windows as forensic clocks. On-chain clustering heuristics like multi-input and peel chains require KYC anchors to bootstrap entity identification, and AA wallets without co-mingling degrade these significantly.

I'm not claiming absolute privacy. What remains is real. Temporal correlation between Pix settlement and on-chain transaction enables statistical matching, mitigated by volume but not eliminated. Live cooperation from subpoenaed merchants before caches expire still yields information. Heavy users create patterns identifiable even without explicit KYC. Real, but qualitatively different from "tax authority queries CPF and sees everything." Directed investigation has to start from outside the system and depends on human cooperation at each hop.

Privacy in P2P fiat-crypto rails is stratified, not binary. Against pure chain analysis, high with AA wallets and no CEX endpoints. Against tax authority CPF queries, high in third-party off-ramp mode. Against long-term application retention, high with volatile caches. Against directed investigation, medium, depends on pulverization and human cooperation at each hop.

The blanket claim that fiat rails leak so all P2P built on them leaks equally is wrong in a way that matters for users making real decisions. Architecture choices change which forensic paths exist. The user offramping into a third party's account through a non-custodial protocol with a non-KYC wallet is in a structurally different position from the user buying tokens directly from a centralized issuer with their own bank account. The discussion worth having isn't whether privacy in P2P fiat-crypto is real. It's which threat models specific architectures defend against, where they degrade, and what users can reasonably expect at each stratum.

3

5

22

2,640

Apr 29

Thanks for the review, really appreciate it!

Apr 29

Sin Binance, ¿cuál es la alternativa para hacer P2P en Venezuela?

Ayer hice este post sobre lo que significa que Sunacrip regule Binance en Venezuela y varios me preguntaron sobre alternativas

Desde la semana pasada (antes de los rumores), he estado probando una alternativa que me vienen recomendando hace unas semanas: @p2pmevenezuela

Este protocolo descentralizado es muy usado en India, Brasil, Argentina y Colombia y hace poco llegaron a Venezuela

Luego haré un post más detallado y técnico, pero mientras te cuento rapidito lo que me gustó y lo que no:

Lo que me gustó:

•Me tomó menos de 10 minutos abrir la cuenta, comprar USDC desde mi banco con Pago Móvil y tenerlos disponibles

•Es perfecta para micropagos: pagué directo al QR del pago móvil del vendedor desde mis USDC y el comerciante recibió los Bs en su banco, todo en menos de 3 minutos. Con Binance u otro CEX hubieran sido 15-20 minutos buscando comerciante, pagando, liberando...

•El protocolo p2pme hace todo el trabajo sucio (matching de órdenes, pagos y liberación). Ni tú ni el comerciante se enteran de los detalles técnicos, se siente como pagar directo con USDC a tasa "Binance"

•Es privado y descentralizado: Usan pruebas ZK y no almacenan ningún dato tuyo (identidad, teléfono, cédula). No hay base de datos que hackear o exponer

•Es verdaderamente autocustodia: puedes exportar tu wallet e importarla en cualquier otra billetera. Incluso si el protocolo llegara a fallar, siempre tienes acceso a tus fondos

Lo que no me gustó:

•Es una ladilla cuando el vendedor quiere una captura del pago. Solo me pasó una vez entre 7 compras. Le expliqué que era un sistema nuevo y le mostré la transacción en la wallet. Ella ya había recibido la notificación normal en su banco, así que se resolvió rápido

•Tienen un solo proveedor de verificación social ZK. Eso es un punto de centralización que no me gusta. Sin embargo, el whitepaper menciona explícitamente el uso de “Reclaim y otros ZK verifiers” y habla de un verifier registry on-chain para agregar más proveedores en el futuro. Ojalá lo implementen pronto

•Las tasas: en el momento de este post la diferencia de precio entre Binace p2p y P2pme es de 0.6% para la compra de usdc y 1.7% para la venta. En teoría conforme haya más adopción debería cerrarse más

En resumen, no es perfecto y todavía hay cosas por pulir

Pero después de leer la documentación completa y probarlo en vivo, siento que la propuesta va en la dirección correcta: Menos confianza en empresas, más confianza en código, incentivos y matemáticas

Sobre todo, para mí gana por ser fácil y rápido

Si alguna vez te ha pasado que tienes liquidez en cripto pero no tienes moneda local y te da la misma ladilla que a mí lidiar con el P2P de Binance para un pago pequeño, vas a agarrarle el gusto a p2pmevenezuela.

3

1

21

1,222

Apr 29

Colombia 🇨🇴 (not Columbia) is live.

Follow @p2pmecolombia

Test the app

Share on X

Earn $5

6

5

37

1,266

Apr 28

If you're a creator this message is for you:

We are giving away $4.000 in Venezuela @p2pmevenezuela, Nigeria @p2pmengn , Mexico @p2pmemexico and Colombia @p2pmecolombia for creators to test @p2pdotme and produce content.

Follow these accounts to learn more.

13

8

59

2,629

Apr 28

If you're Venezuelan:

Buy and sell USDc with your pago movil without any government intervention.

@p2pmevenezuela is fully private, descentralized and you OWN YOUR MONEY.

Apr 27

🇻🇪 Venezuela diseña un nuevo mecanismo de compra-venta de divisas a través del Banco Central (BCV). El sistema estaría diseñado tanto para personas naturales como para las empresas.

3

6

43

2,832

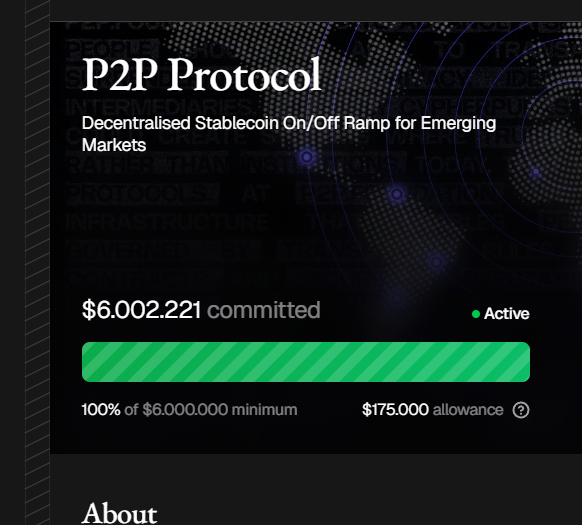

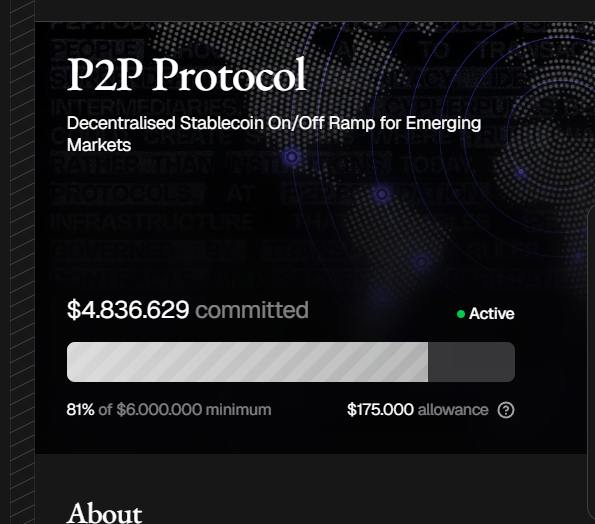

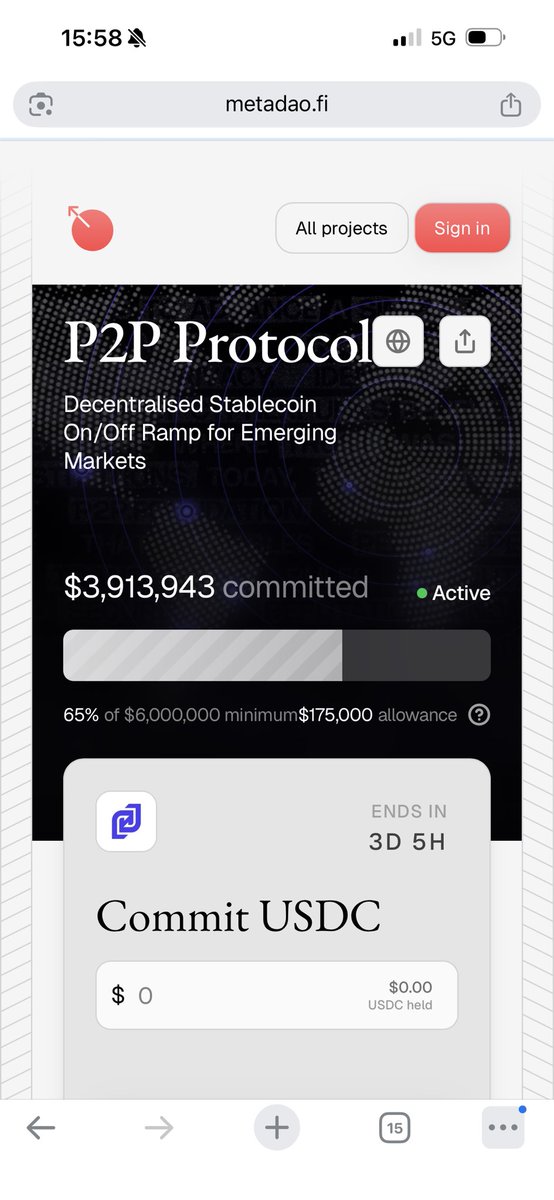

Starting this month, we’re refining our rewards structure to build a more sustainable ecosystem:

• $20/month → Top 500 users globally (previously top 1000)

• $50/month → Top 100 P2P merchants globally

We’ve slightly reduced the number of user rewards to strengthen long-term sustainability and redirect value back into our Futarchy treasury.

Appreciate the continued support - we’re building this together 💪

23

12

74

14,113

don retweeted

Apr 26

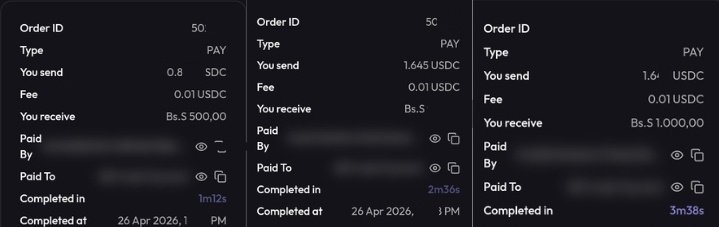

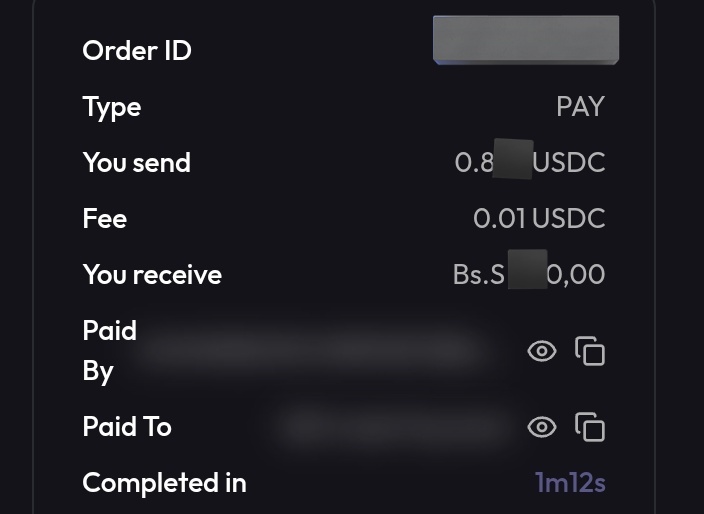

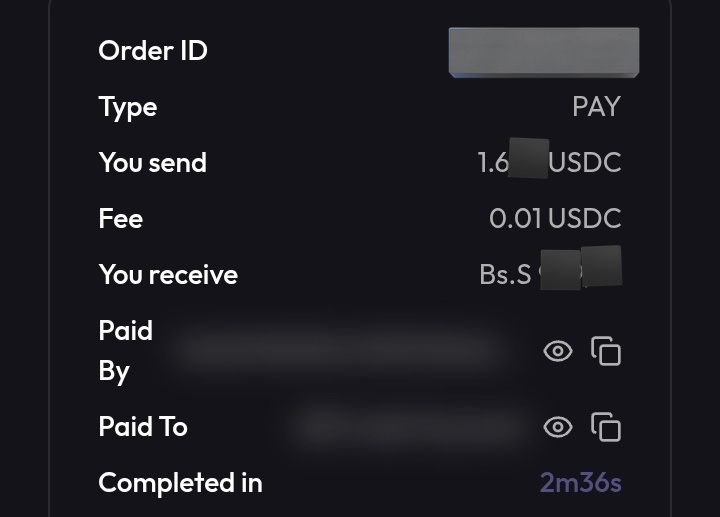

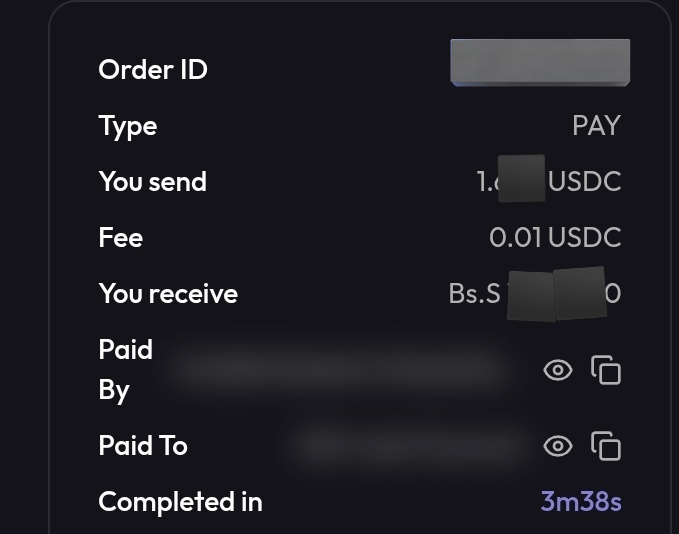

Domingo de pasear y probar un protocolo p2p que me llamó la atención

Es una rampa rápida Cripto->moneda local transparente para el vendedor, pagué directo a su QR

Hasta ahora ha funcionado muy bien como solución para micropagos: Un café en un sitio, una empanada en otro y un jugo en un tercer kiosko

Tiempo promedio: 2min23seg desde que se descuentan mis USDC hasta que el vendedor recibió Bs en su cuenta

En la tarde me siento en el blockexplorer y dune a revisar el Onchain

9

4

27

2,507

Apr 26

I just supported @isaacvarzim on @buymeacoffee! 🎉

You can support them here — buymeacoffee.com/isaacvarzim…

1

11

295

Apr 24

Decentralized, private and self custodial.

If you don't see value on these, the app's not for you.

Apr 24

Un minuto y medio para pagar un café, prefiero pagar impuestos

2

3

18

763

don retweeted

Apr 23

Para todos los que nos gusta hacer transacciones por fuera del sistema.

Encontré una plataforma de pagos con QR que es 100% anónima donde podes hacer pagos en USDC sin pasar ninguna verificación de identidad.

Podes:

- Pagar con USDC

- Comprar USDC

- Vender USDC

- Aportar liquidez y generar un 1.25% por operación.

De lo mejor que he visto.

@p2pmeargentina @P2Pdotme

Les dejo el video en el cual la uso y les explico como se usa.

youtu.be/HVOMHRVNTs0

5

9

48

4,729

don retweeted

Apr 24

KYC tradicional já tem dias contados.

Esse modelo atual de provar identidade não é mais útil.

Quem possui capital em plataformas centralizadas que possuem modelos atuais convencionais de verificação, deveria se preocupar mais com autocustódia.

7

14

203

18,478