Global asset allocator at @NYLIManagement | Institutional Customized Solutions | Digital Assets | RWA | Global Market Strategy

Joined November 2025

- Tweets 53

- Following 493

- Followers 86

- Likes 90

36 Photos and videos

Jun 15

Three cash-flow-negative AI companies entering an already concentrated, high-valuation market will test investor conviction and market liquidity.

AI and infrastructure companies have become market-defining businesses while remaining largely inaccessible to public markets. Companies have chosen to stay private longer, shifting a larger share of value creation away from public markets.

When companies this size enter passive indexes, forced selling begins. SpaceX's Communication Services classification means Meta and Alphabet face mechanical selling pressure to make room.

Watch bitcoin and Tesla as the early pressure valves. If they crack around the IPO window, speculative capital is being rotated, not added.

Our team's #MacroMonday report below:

nylim.com/insights/gms-weekl…

1

25

Jun 12

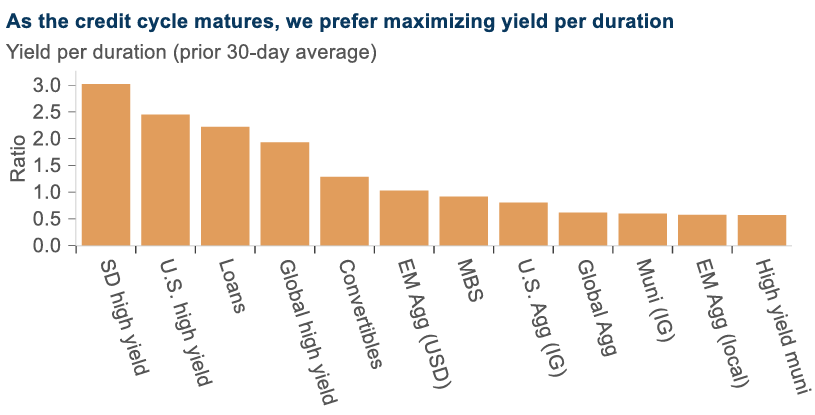

Cash has lost yield potency, driving a clear incentive toward buy-and-hold total return opportunities in credit.

Saying again➡️ buy-and-hold total return

- The credit cycle is healthy today, but macro risks have risen and the credit cycle has matured. We also expect ongoing yield curve volatility. Our “solve” for both concerns is to stay short duration across credit types in the U.S.

- Upside risks to long rates remain: we are staying on the short side of neutral in duration, seeing buying opportunities above a ~4.6% threshold on the 10Y yield.

- We prefer to balance short duration Treasuries, convertibles, and corporate credit exposure with longer duration in securitized credit, where we see long-end exposure as better rewarded.

1

20

Jun 10

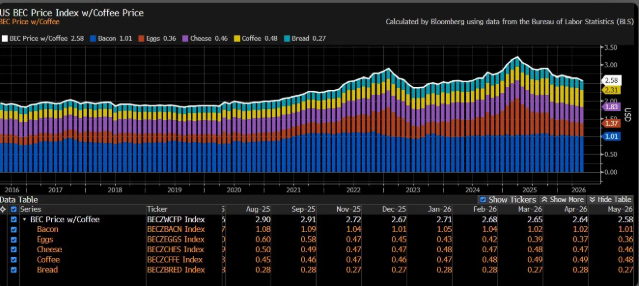

Here is a relatable inflation indicator - the Bacon Egg & Cheese w/Coffee Index. You don’t need a CPI report to feel inflation, just make breakfast.

Markets largely looked through the inflation print, with Treasury yields little changed following the release.

Attention now turns to next week’s FOMC meeting where policymakers will weigh the highest inflation print in three years against a resilient labor market.

In the coming months, we remain focused on second-order inflation effects, specifically whether higher energy prices will feed into transportation and other energy-intensive categories, ultimately pushing core inflation higher.

1

27

Thomas Sy retweeted

Stand With Crypto and over 200 organizations sent a simple message to Senate leadership: it's time for the Clarity Act.

The community is unified — large companies, startups, associations, and grassroots groups across the country are counting on their lawmakers to deliver rules of the road for crypto in America.

The Clarity Act passed the Senate Banking Committee with bipartisan support.

Now it needs to cross the finish line. Tell your Senators you want Clarity 👇

52

341

1,187

312,538

Jun 8

Markets are caught between two stories:

🐂The optimist: May payrolls 172k vs. 89k expected. AI earnings still delivering. U.S. equities near all-time highs. Financial conditions loose.

🐻The realist: Hormuz still not normalized. Consensus now pricing a rate HIKE. CPI came in 🔥; inflation stickier, impact on input costs. Geopolitical risk hasn't gone away.

In this week’s #MacroMonday, my team discusses how allocators can tackle both stories:

➡️U.S. equities: diversify without abandoning the US growth story. Market-weight neutral. AI and earnings justify participation, not concentration. Rotate into high quality small caps and ex-U.S. with latent cash.

➡️Fixed income: yields are attractive, but don’t extend duration until the 10Y hits 4.60–4.70%. Rate volatility isn’t done.

➡️Commodities and infrastructure: increase allocation; when stock-bond correlations tighten in an inflationary shock, you need a third diversifier.

Broad beta is over.

Full report:

nylim.com/insights/gms-weekl…

46

Thomas Sy retweeted

Jun 5

WSJ: JPMorgan, Bank of America, Citi, and Wells Fargo are building a tokenized deposit network to compete with crypto.

The goal is to keep deposits inside the banking system while offering speed and 24/7 settlement.

The network will be operated by The Clearing House, and it sounds like the underlying blockchain hasn’t been selected yet.

27

22

149

21,751

Jun 4

My team discusses macro implications of digital assets and our broader tokenization goals in this week’s Market Matters podcast.

podcasts.apple.com/us/podcas…

2

46

Jun 2

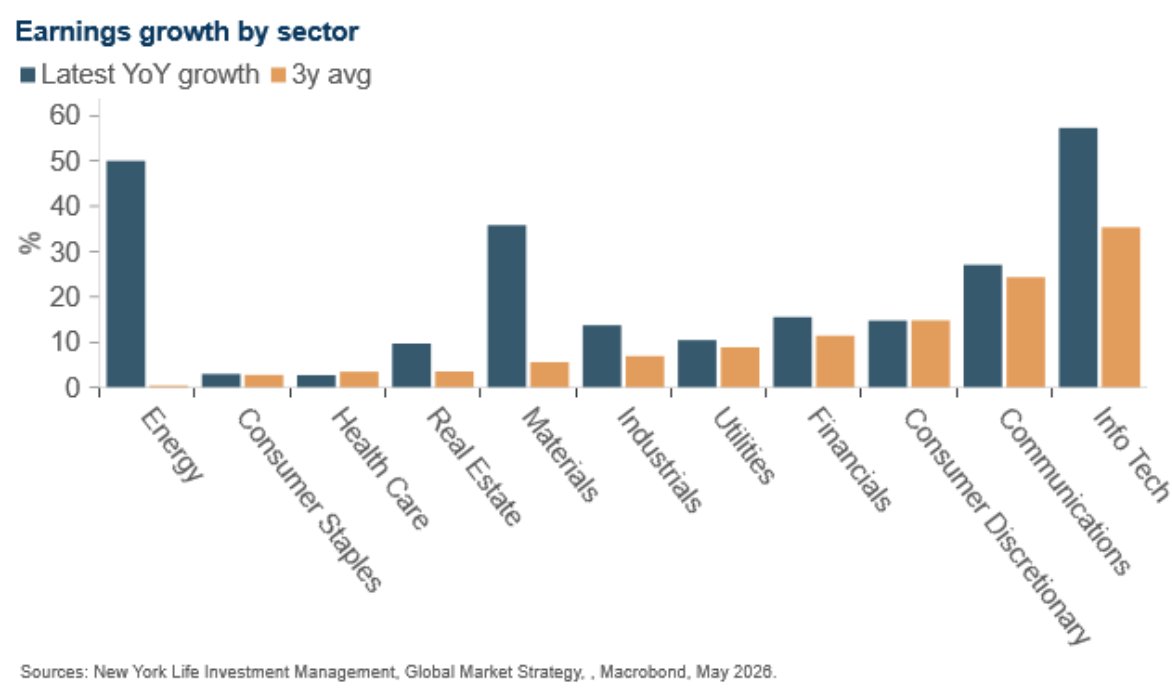

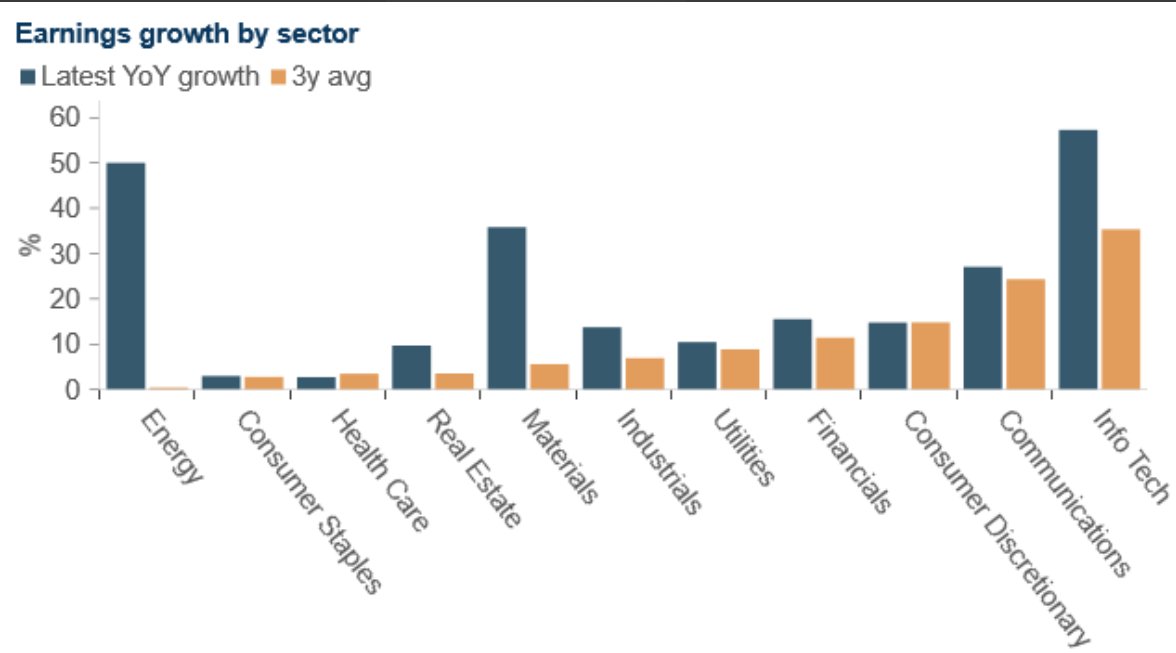

Julia Hermann discussing our team's out-of-consensus view on @markets that 1 fed cut over 12 months is still on the table.

- Two sectors carrying the entire S&P index: Energy - 38% and Technology - 22%

- Rising input costs as a key risk for sector positioning going into Q2.

- Markets are focused on near-term inflation even as U.S. debt has crossed 100% of GDP — potential shift toward steepening ahead.

bloomberg.com/news/videos/20…

43

Jun 2

When liquidity dominates, traditional signals break down. Correlations shift. 60/40 fails. Price discovery distorts.

This is the environment when #tokenization matters more:

- 24/7 continuous price discovery

- real-time liquidity signals onchain

- programmable collateral that responds to liquidity conditions instantly

- daily-liquid credit products that don’t gate when regimes shift

Jun 1

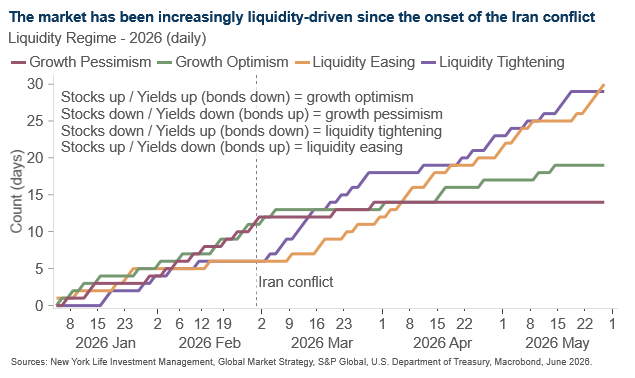

Since the onset of the Iran conflict, markets have been increasingly liquidity-driven.

Stocks and bonds have been moving in patterns that look less like a clean growth signal and more like a shift between liquidity easing and tightening.

#Liquidity

1

70

Jun 1

When a $800B insurance company starts writing about market structure and digital assets — it's not hype. It's infrastructure.

The bottom line:

Separate long-term infrastructure potential from near-term hype. The direction of travel is clear; the timeline is not.

nylim.com/insights/gms-weekl…

25

Jun 1

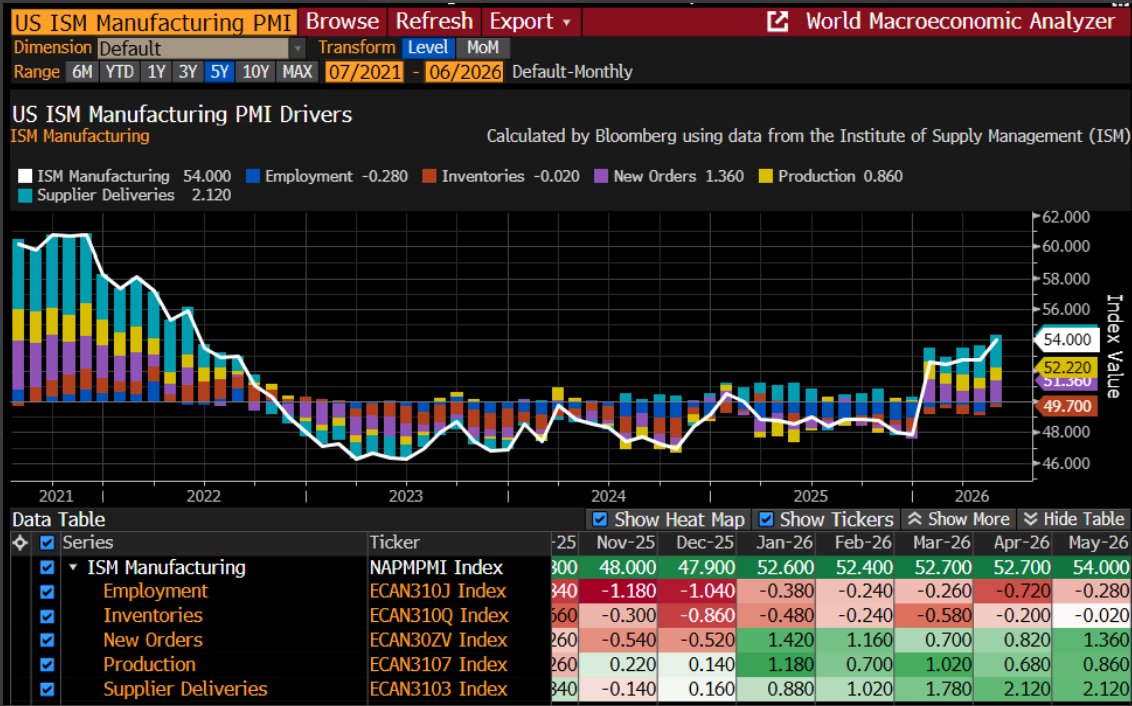

US ISM Manufacturing just printed 54.0 — highest since 2021. The supplier deliveries line is the sharpest signal — tightening supply chains in a geopolitical conflict environment means inflation pressure is building from the bottom up.

→ New Orders: 1.36 — demand accelerating

→ Production: 0.86 — factories responding

→ Supplier Deliveries: 2.12 — supply chains tightening again

→ Inventories: -0.02 — lean, restocking cycle ahead

⚠️ Employment: -0.28 — only soft spot

28

May 27

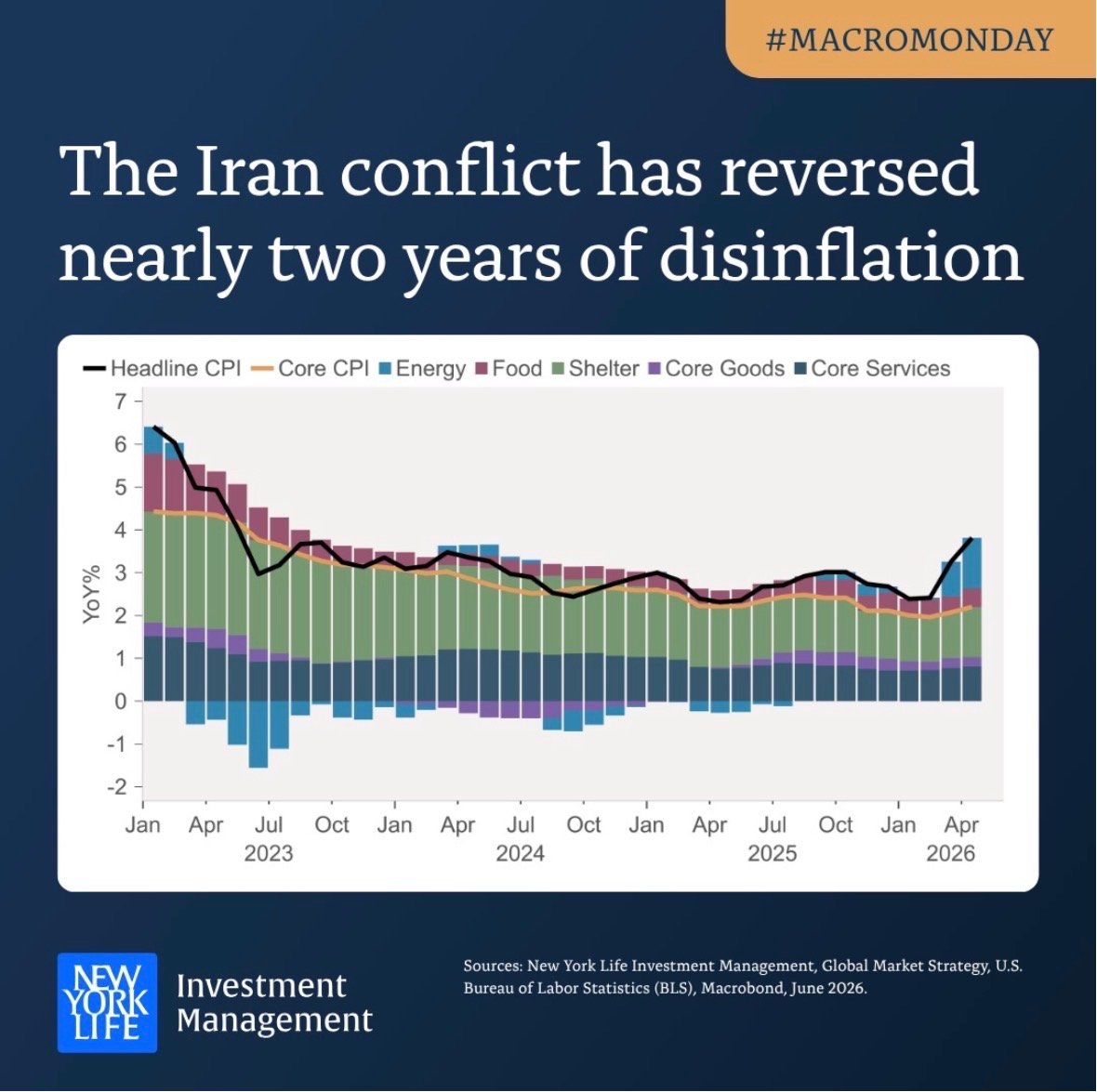

The Iran conflict is a symptom of a much larger shift. In this @CNBC article, my team with @Macro_Mike_ discusses how policy is being written in real time as we work through this geopolitical regime change.

China weaponizing supply chain access. Europe rearming after Ukraine. Japan abandoning postwar restraint. The U.S. linking trade, alliances, and industrial capacity directly to national power — and moving from setting rules to taking equity stakes in critical outcomes.

This is a structural reset that has three profound investment implications:

1️⃣ Resilience is replacing efficiency

The 30-year era of prioritizing cost and supply chain optimization is over. Companies and governments are now paying a premium for redundancy and domestic capacity. Security-sensitive infrastructure, critical minerals, defense, semiconductors, and logistics are strategic national investments. Capital flows are being redirected accordingly.

2️⃣ Structural inflation risk is rising

Shortened supply chains. Vulnerable energy routes. Aggressive government intervention in trade and industry. The bias is toward stickier prices and greater commodity and currency volatility — not a return to the low-inflation world of 2010–2020. The Hormuz blockade accelerated this. But the underlying forces preceded it.

3️⃣ Geopolitical leverage has diminishing returns

China weaponized market access. The U.S. weaponized the dollar after Ukraine. Iran weaponized Hormuz. But there is a limit. Push too far and the system adapts: more pipelines that bypass Hormuz, more storage, more dollar alternatives, more supply chain diversification.

The short-run effect is leverage. The long-run effect is fragmentation ➡️leads to higher structural costs ➡️ leading to permanently priced into shipping, trade, and energy.

The range of outcomes in a more contested world is structurally wider than it was in a globalized one.

cnbc.com/advertorial/2026/05…

45

Thomas Sy retweeted

May 26

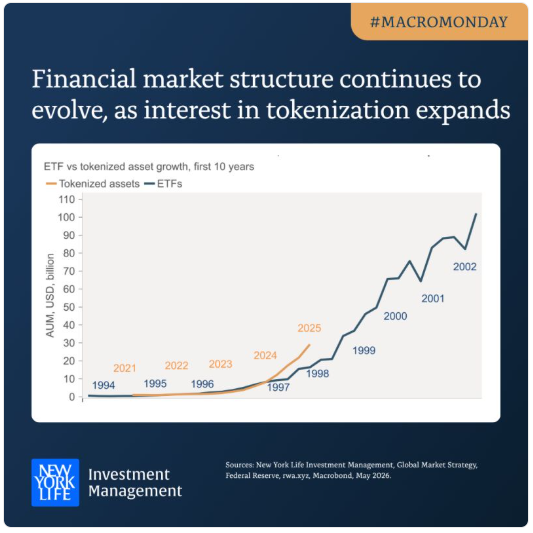

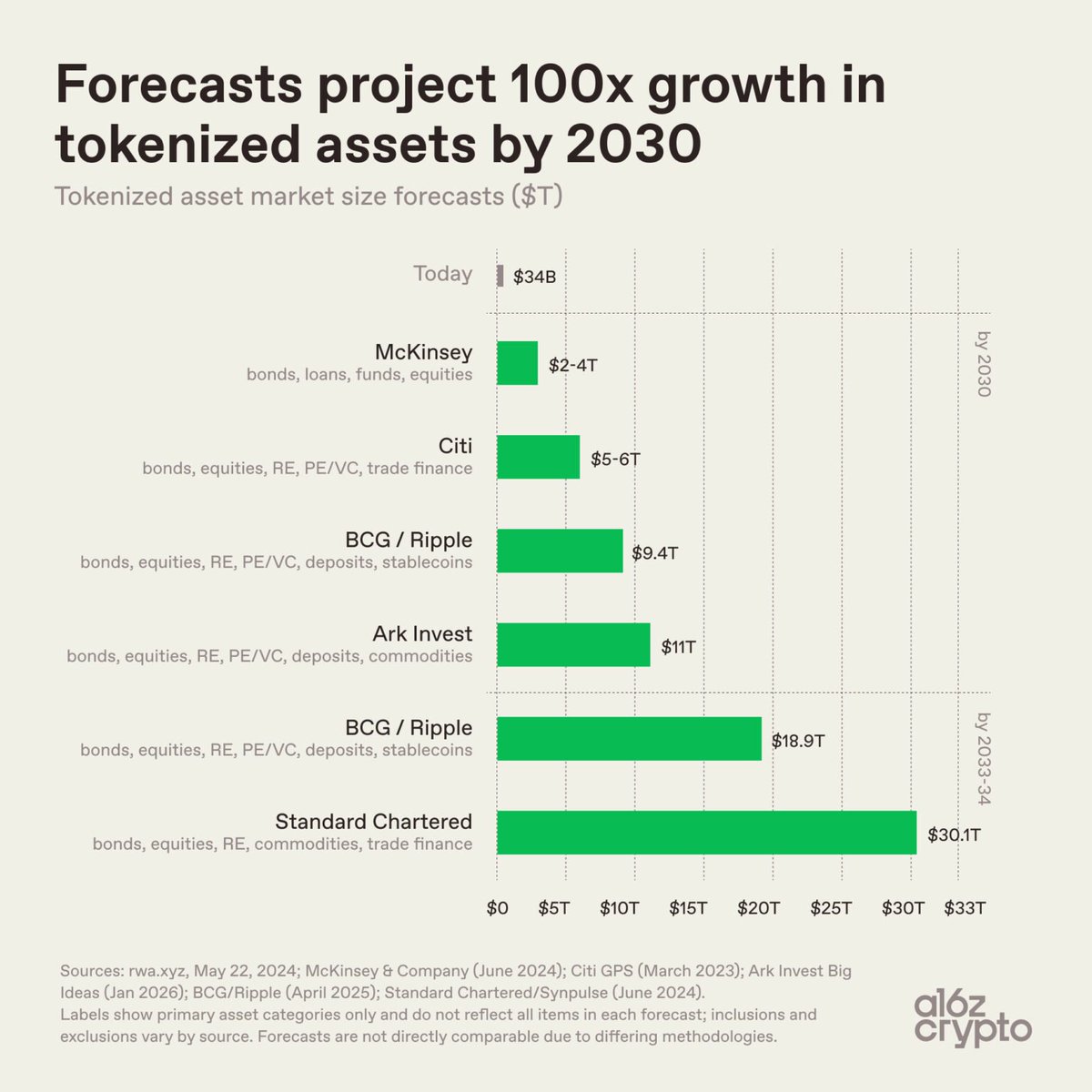

Looking ahead, forecasts for tokenized assets vary a lot but they all point in the same direction: growth.

McKinsey: $2–4T by 2030.

Ark Invest: $11T by 2030.

BCG/Ripple: $9.4T by 2030, $18.9T by 2033.

Standard Chartered: $30T by 2034.

The gap between $2 trillion and $30 trillion is more about definitions than adoption.

Different institutions are measuring different things. McKinsey focuses mostly on bonds, loans, funds, and equities. Standard Chartered adds commodities and trade finance. BCG and Ripple include deposits and stablecoins alongside more traditional asset categories.

Despite these differences, the broader trend is consistent: Asset tokenization is expected to expand.

56

110

521

101,680

May 26

"Any day now"

- Recession Bears🐻

May 26

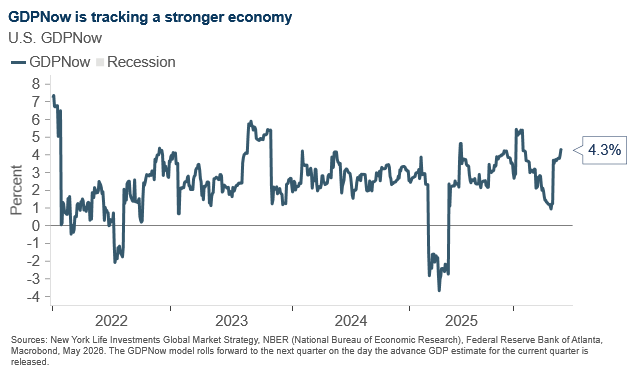

The Atlanta Fed’s GDPNow model is tracking U.S. growth at 4.3%.

Nowcasts can move around, but the direction matters: growth expectations have firmed rather than faded.

For an economy that keeps being described as fragile, the incoming data still looks surprisingly resilient.

29

May 22

“Only hawks get to go to central banker heaven” - former Dallas Fed President Bob McTeer

At the end of the day, Warsh is a policy hawk. His more dovish comments last year were all about campaigning for the job. His focus will shift to his legacy - that means ensuring price stability.

The word cloud below is based on Warsh’s prior communications.

50

May 21

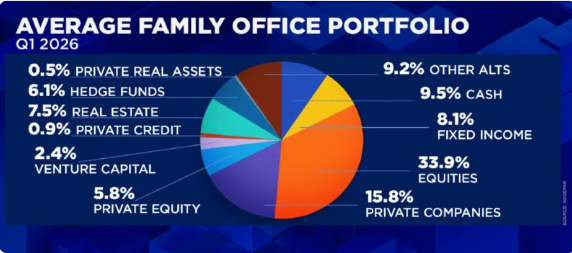

Addepar and CNBC created the Family Office Portfolio Tracker – the first ever snapshot of the actual portfolios of family offices.

57% of UHNW investors are in illiquid and opaque asset classes. #Tokenization doesn’t change what they own but how they own it.

We now have a better benchmark on the $6T family office market.

60/40 portfolio should really not exist in 2026.

61

May 20

The steepening is here - globally. 10Y at 4.70% is starting to look like an entry point.

→ Long end: 4.70% on 10Y = compelling entry to selectively extend duration

→ Short end: still room to fall — creates a curve twist

→ Both bear AND bull steepeners are in play simultaneously

The two paths to a Fed cut:

🟢 Hormuz normalizes → CBs resume pre-conflict easing path

🔴 Hormuz stays blocked → demand destruction does the work

Either way: one cut over the next 12 months stays on the table.

nylim.com/insights/gms-weekl…

1

47